10 Expert Strategies for Securing Your Dream Car Loan: A Comprehensive Guide

10 Expert Strategies for Securing Your Dream Car Loan: A Comprehensive Guide Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is incredibly exciting. Whether it’s a sleek new sedan, a rugged SUV, or a practical family car, the prospect of new wheels can ignite anticipation. However, for most of us, this dream often involves navigating the world of car loans. Securing the right auto loan is not just about getting approved; it’s about finding terms that align with your financial health and future goals.

Understanding the intricacies of car financing can feel overwhelming, but it doesn’t have to be. As an experienced financial content writer and enthusiast, I’ve seen firsthand how a well-informed approach can transform a potentially stressful process into a smooth, empowering experience. This comprehensive guide will equip you with 10 crucial strategies, designed to give you a significant advantage in securing the best possible vehicle loan. We’ll delve deep into each point, offering actionable insights, professional tips, and common pitfalls to avoid, ensuring you’re ready to drive away with confidence.

10 Expert Strategies for Securing Your Dream Car Loan: A Comprehensive Guide

1. Understand Your Credit Score: The Foundation of Your Car Loan Journey

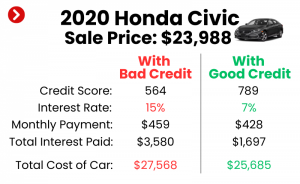

Your credit score is arguably the most critical factor lenders consider when you apply for a car loan. It acts as a financial report card, indicating your reliability as a borrower. A higher credit score signals lower risk to lenders, often translating into more favorable interest rates and better loan terms.

Based on my experience, many aspiring car owners overlook the importance of checking their credit score before they even start car shopping. This is a common mistake that can lead to disappointment or accepting a less-than-ideal car loan offer. Take the proactive step to obtain your credit reports from the three major bureaus—Experian, Equifax, and TransUnion. Review them carefully for any inaccuracies or discrepancies, as these could negatively impact your score.

Pro tips from us: If your credit score isn’t where you want it to be, dedicate some time to improving it. This could involve paying down existing debts, making all payments on time, and avoiding opening new credit lines. Even a small increase in your score can make a significant difference in the interest rate you qualify for, potentially saving you thousands over the life of your auto loan.

2. Determine Your True Budget and Affordability

Before you even glance at a car dealership’s inventory, it’s essential to establish a realistic budget. This isn’t just about the monthly car loan payment; it encompasses the total cost of car ownership. Many people mistakenly focus solely on the monthly payment, forgetting about other significant expenses.

Beyond the principal and interest of your vehicle loan, consider insurance premiums, fuel costs, maintenance, repairs, and potential registration fees. These ancillary expenses can quickly add up, turning an "affordable" monthly payment into a financial strain. A good rule of thumb is that your total car-related expenses, including your car loan payment, should ideally not exceed 10-15% of your net monthly income.

Common mistakes to avoid are underestimating these additional costs and overextending yourself. Use online budget calculators to get a clear picture of what you can comfortably afford each month without jeopardizing other financial obligations. This strategic planning ensures that your new car brings joy, not financial stress.

3. Save for a Substantial Down Payment

A significant down payment is one of the most powerful tools you have to improve your car loan terms. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over time. Furthermore, a larger down payment demonstrates your financial commitment to lenders, often leading to better interest rates.

Based on my observations, many consumers try to get by with the smallest down payment possible, or even none at all. While zero-down car loan options exist, they typically come with higher interest rates and mean you’ll owe more than the car is worth from day one – a situation known as being "upside down" or "underwater." This can be problematic if you need to sell or trade in the car early.

Pro tips from us: Aim for at least 10% of the vehicle’s purchase price for a used car, and 20% for a new car. This not only puts you in a stronger negotiating position but also helps mitigate depreciation, which is particularly rapid in the first few years of a new car’s life. The more you put down, the less risk you carry, and the better your car loan approval chances.

4. Get Pre-Approved Before You Shop

One of the most empowering steps you can take in the car financing process is getting pre-approved for a loan. Pre-approval means a lender has reviewed your credit and financial information and agreed to lend you a specific amount at a particular interest rate, contingent on the final vehicle details. This essentially provides you with a concrete offer before you step onto a dealership lot.

The advantage of pre-approval is immense. It transforms you into a cash buyer in the eyes of the dealership. Instead of negotiating a price and financing simultaneously, you can focus solely on getting the best price for the vehicle, knowing your financing is already secured. This eliminates the pressure to accept potentially less favorable auto loan terms offered by the dealership’s finance department.

Common mistakes to avoid are letting the dealership handle all the financing without comparison shopping. Always arrive at the dealership with your pre-approval letter in hand. This gives you leverage and a benchmark against which to compare any offers from the dealer, ensuring you secure the most competitive car loan rates.

5. Shop Around for Multiple Lenders

Just as you wouldn’t buy the first car you see, you shouldn’t accept the first car loan offer you receive. Lenders vary significantly in their rates, fees, and terms. Shopping around allows you to compare multiple offers and find the one that best suits your financial situation. This is a critical step often overlooked in the rush to buy a car.

Based on my experience, consumers who compare offers from at least three different lenders typically secure better deals. Consider banks, credit unions, and online lenders, as each may have unique advantages. Credit unions, for example, are often known for offering highly competitive car loan rates due to their member-focused structure. Online lenders provide convenience and often quick approval processes.

Pro tips from us: When applying to multiple lenders within a short period (typically 14-45 days), credit bureaus usually count these inquiries as a single event. This is because they understand you’re rate shopping for a single loan, minimizing the impact on your credit score. Don’t be afraid to cast a wide net to find the optimal car loan for your needs.

6. Choose the Right Loan Term for Your Needs

The loan term, or the length of time you have to repay your car loan, is a crucial factor impacting both your monthly payment and the total cost of the loan. While a longer loan term (e.g., 72 or 84 months) might offer a lower monthly payment, it almost always means you’ll pay significantly more in interest over the life of the loan.

Conversely, a shorter loan term (e.g., 36 or 48 months) results in higher monthly payments but substantially less interest paid overall. It also means you’ll own your car free and clear much sooner. The decision hinges on balancing affordability with long-term cost-effectiveness.

Common mistakes to avoid are automatically opting for the longest term to achieve the lowest monthly payment without considering the total cost. Pro tips from us: Evaluate your budget carefully to see if you can comfortably afford a shorter term. If you find yourself needing a very long term just to make the payments, it might be a sign that you’re looking at a car outside your true budget. For more insights on budgeting, you might find our article on Smart Budgeting for Big Purchases helpful.

7. Understand the Interest Rate (APR) and Its Impact

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. However, when it comes to car loans, you should primarily focus on the Annual Percentage Rate (APR). The APR represents the total cost of your loan over a year, including not only the interest rate but also any additional fees or charges from the lender.

A seemingly small difference in APR can translate into hundreds or even thousands of dollars over the life of your auto loan. For example, a 0.5% difference on a $30,000 loan over 60 months can mean a significant amount saved. This is why comparing APRs from different lenders is so vital.

Based on my experience, some lenders might quote a low interest rate but then add various fees that push up the overall APR. Always ask for the complete APR when comparing offers. Ensure you’re comparing apples to apples across different loan proposals to truly identify the best car loan rates available to you.

8. Read the Fine Print: Terms and Conditions Are Key

Before signing any car loan agreement, it is absolutely imperative to read every single line of the contract. This document outlines all the terms and conditions of your loan, including interest rates, payment schedules, late payment penalties, prepayment penalties, and any other associated fees. Many people, in their eagerness to get their new car, rush through this critical step.

Common mistakes to avoid include assuming certain terms or overlooking clauses that could cost you money down the line. Look specifically for details on early payoff penalties; some loans charge a fee if you repay the loan before the scheduled term. Also, be aware of any clauses regarding default or repossession, and understand your rights and responsibilities.

Pro tips from us: Don’t hesitate to ask questions about anything you don’t understand. A reputable lender will be happy to clarify all aspects of the car financing agreement. If you feel pressured or rushed, take a step back. It’s your financial commitment, and you have the right to be fully informed. You can also consult resources like the Consumer Financial Protection Bureau (CFPB) for independent advice on understanding loan terms. Link to CFPB Car Buying Guide.

9. Consider a Co-Signer (If Necessary)

If you have a lower credit score or limited credit history, securing a car loan with favorable terms can be challenging. In such cases, considering a co-signer might be a viable option. A co-signer is someone with good credit who agrees to be equally responsible for the loan repayment if you default. Their strong credit profile can help you get approved or secure a lower interest rate.

While a co-signer can be a pathway to car loan approval, it’s a decision that shouldn’t be taken lightly. The co-signer’s credit score will be impacted by the loan, and they will be legally obligated to make payments if you fail to. This can strain personal relationships if things go wrong.

Pro tips from us: Only consider a co-signer if you are absolutely confident in your ability to make all payments on time. Have an open and honest conversation with the potential co-signer about the responsibilities and risks involved. This strategy should be a last resort, or a temporary bridge to building your own credit, rather than a permanent solution for car financing.

10. Know When to Refinance Your Car Loan

Securing your initial car loan is a major step, but the journey doesn’t necessarily end there. Life circumstances and market conditions can change, making it beneficial to consider refinancing your auto loan down the road. Refinancing involves taking out a new loan to pay off your existing one, ideally with more favorable terms.

You might consider refinancing if your credit score has significantly improved since you first took out the loan, if interest rates have dropped, or if you need to lower your monthly payments due to a change in financial circumstances. Refinancing can potentially reduce your interest rate, shorten or lengthen your loan term, or even remove a co-signer from the original loan.

Based on my experience, many people miss out on potential savings by not re-evaluating their car financing periodically. Pro tips from us: It’s worth reviewing your loan terms and current market rates every 12-18 months. Use online refinancing calculators to estimate your potential savings. This proactive approach ensures you’re always on the best possible vehicle loan terms. If you’re looking to manage your debt better, our guide on Effective Debt Management Strategies could offer further insights.

Drive Away with Confidence

Navigating the world of car loans can seem complex, but by arming yourself with these 10 expert strategies, you’re well on your way to making an informed and financially sound decision. From understanding your credit score to wisely choosing your loan term and even considering future refinancing, each step plays a vital role in securing the best possible car loan for your needs.

Remember, the goal isn’t just to get approved for a loan; it’s to secure terms that empower your financial well-being while you enjoy your new ride. Take your time, do your research, and don’t be afraid to ask questions. With a strategic approach, you’ll not only drive away in your dream car but do so with complete financial confidence. Start your car financing journey today, equipped with knowledge and ready to make smart choices.