1st Advantage Car Loan: The Ultimate Expert Guide to Approval, Rates, and Driving Your Dream Car

1st Advantage Car Loan: The Ultimate Expert Guide to Approval, Rates, and Driving Your Dream Car Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex highway, full of twists, turns, and unexpected detours. For many prospective car owners, finding a trusted lender that offers competitive rates and a straightforward process is paramount. If you’ve been researching your options, you’ve likely come across 1st Advantage Car Loan, a name that often pops up when people search for reliable auto financing.

As an expert blogger and professional SEO content writer, I’ve spent years delving into the intricacies of personal finance and auto lending. Based on my extensive experience, understanding the nuances of a lender like 1st Advantage is crucial before making a commitment. This comprehensive guide will dissect everything you need to know about 1st Advantage Car Loan, from eligibility and application tips to understanding rates and terms. Our goal is to empower you with the knowledge to make an informed decision and confidently drive away in your dream car.

1st Advantage Car Loan: The Ultimate Expert Guide to Approval, Rates, and Driving Your Dream Car

What Exactly is 1st Advantage Car Loan? Understanding the Lender

When you’re looking for a car loan, you’re not just looking for money; you’re looking for a financial partner. 1st Advantage Car Loan typically refers to auto financing solutions offered by 1st Advantage Federal Credit Union. This institution, like many credit unions, operates differently from traditional banks. They are member-owned, meaning their primary focus is on providing value and excellent service to their members, rather than maximizing profits for shareholders.

This fundamental difference often translates into several benefits for borrowers. Credit unions are known for potentially offering more favorable interest rates, lower fees, and a more personalized customer service experience. For anyone seeking an auto loan, understanding this operational model is the first step in appreciating what 1st Advantage brings to the table. They aim to be a genuine "advantage" for their members’ financial well-being.

Why Consider 1st Advantage for Your Next Auto Loan?

Choosing a car loan provider isn’t a decision to take lightly. There are countless options available, but 1st Advantage Car Loan stands out for several compelling reasons. Their member-centric approach often translates into tangible benefits that can save you money and simplify your borrowing experience.

Here are some key advantages that make them a strong contender in the auto financing landscape:

- Competitive Interest Rates: One of the most significant draws of credit unions like 1st Advantage is their ability to offer lower interest rates compared to many traditional banks. Because they are non-profit and member-owned, they can pass on savings to their members. This can lead to substantial savings over the life of your loan.

- Flexible Loan Terms: Every borrower has unique financial circumstances. 1st Advantage typically offers a variety of loan terms, allowing you to choose a repayment schedule that best fits your budget. Whether you prefer a shorter term with higher monthly payments to save on interest or a longer term for lower monthly installments, they often have options.

- Personalized Service: Unlike large, impersonal banks, credit unions pride themselves on their community focus and personalized member service. You’re not just a number; you’re a member of their financial family. This often means more attentive support throughout the application process and beyond.

- Pre-Approval Options: Getting pre-approved for a car loan is a smart move, and 1st Advantage typically facilitates this. Pre-approval gives you a clear understanding of how much you can afford before you even step foot on a dealership lot. This strengthens your negotiation position and helps you stick to your budget.

- Refinancing Opportunities: Even if you already have a car loan with another lender, 1st Advantage might be able to help you save money. They often offer competitive refinancing options, allowing you to secure a lower interest rate or more favorable terms on an existing auto loan.

These benefits highlight why 1st Advantage Car Loan is a serious consideration for anyone looking to finance a vehicle. Their dedication to member satisfaction often translates into a smoother, more affordable car buying experience.

Types of Car Loans Offered by 1st Advantage

Just as there are many types of cars, there are also various types of auto loans designed to meet different needs. 1st Advantage Car Loan understands this diversity and typically offers a range of financing solutions. Understanding these options is key to finding the perfect fit for your situation.

Let’s explore the common types of car loans you can expect:

- New Car Loans: If you’re eyeing that brand-new model fresh off the assembly line, 1st Advantage provides financing specifically for new vehicles. These loans often come with attractive rates, reflecting the lower risk associated with financing a new car. You’ll typically get competitive terms to help you drive away in your latest acquisition.

- Used Car Loans: Buying a used car is a fantastic way to save money and still get a reliable vehicle. 1st Advantage offers loans tailored for pre-owned cars, trucks, and SUVs. While rates might differ slightly from new car loans due to factors like vehicle age and mileage, they strive to keep them competitive.

- Auto Loan Refinancing: Already have a car loan but feel like you’re paying too much interest? Refinancing your auto loan with 1st Advantage could be a game-changer. This option allows you to replace your current loan with a new one, potentially at a lower interest rate or with different terms. It’s an excellent way to reduce your monthly payments or the total interest paid over time.

- Pre-Approval Loans: This isn’t a loan type in itself, but a crucial step in the car buying process. 1st Advantage typically offers a pre-approval service, allowing you to get approved for a specific loan amount before you start shopping. This gives you significant leverage at the dealership and helps you set a realistic budget.

Each of these options is designed to cater to different stages of your car ownership journey. Whether you’re buying new, used, or looking to improve an existing loan, 1st Advantage Car Loan aims to provide a suitable financial product.

Navigating Eligibility Requirements for a 1st Advantage Car Loan

Before you even start filling out an application, it’s wise to understand the general eligibility criteria for a 1st Advantage Car Loan. While specific requirements can vary slightly, most lenders, including credit unions, look for a few key indicators of financial responsibility. Meeting these criteria will significantly increase your chances of approval.

Here’s a breakdown of what 1st Advantage will typically assess:

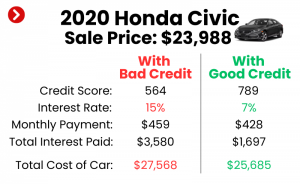

- Credit Score and History: Your credit score is perhaps the most critical factor. Lenders use it to gauge your creditworthiness and your likelihood of repaying the loan. A higher credit score (generally 670 and above) indicates a lower risk, often qualifying you for the best interest rates.

- Pro Tip from Us: Before applying, obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it for any errors and dispute them immediately. A clean credit report is your best asset. For more insights into managing your credit, check out our guide on Understanding Your Credit Score for Auto Loans (simulated internal link).

- Income and Employment Stability: Lenders want to ensure you have a steady income stream to make your monthly payments. They will typically ask for proof of income, such as pay stubs, W-2 forms, or tax returns. Stable employment over a period of time (e.g., 1-2 years) is also a positive indicator.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio (ideally below 36%) suggests you have enough disposable income to comfortably take on a new car loan without being overextended.

- Membership with 1st Advantage: As a credit union, 1st Advantage typically requires you to be a member to access their services, including car loans. Membership usually involves opening a savings account with a small deposit. Check their specific membership eligibility, which often includes living or working in certain areas, or being affiliated with specific organizations.

- Vehicle Information (for specific loans): While not a personal eligibility requirement, the vehicle itself plays a role, especially for used car loans. Factors like the vehicle’s age, mileage, and make/model can influence approval and loan terms. Lenders often have limits on the age or mileage of vehicles they will finance.

Understanding these requirements helps you prepare effectively. Addressing any potential weaknesses in your application beforehand can significantly improve your chances of securing a 1st Advantage Car Loan.

The Application Process: A Step-by-Step Guide to Your 1st Advantage Car Loan

Applying for a car loan doesn’t have to be daunting. With 1st Advantage Car Loan, the process is designed to be as straightforward as possible, especially for members. Based on my experience, a well-prepared applicant can navigate these steps with ease.

Here’s a typical step-by-step breakdown of how to apply for an auto loan with 1st Advantage:

- Become a Member (if not already): Since 1st Advantage is a credit union, the first step is usually to establish membership. This typically involves meeting their eligibility criteria (e.g., residency, employment, or association with specific groups) and opening a savings account with a minimal deposit.

- Gather Your Documents: Preparation is key. Before you start the application, collect all necessary paperwork. This commonly includes:

- Proof of identity (driver’s license, state ID)

- Proof of residency (utility bill, lease agreement)

- Proof of income (pay stubs, W-2s, tax returns)

- Social Security Number

- Vehicle information (if you’ve already chosen a car, including VIN, make, model, year, and selling price)

- Apply for Pre-Approval (Recommended): This is a highly recommended step. Applying for pre-approval online or in person allows 1st Advantage to assess your financial situation and determine how much you qualify for. This provides you with a maximum loan amount and an estimated interest rate, giving you buying power before you even visit a dealership.

- Submit Your Full Application: Once you’ve found the perfect car or decided to refinance, you’ll complete the full loan application. This involves providing detailed personal, financial, and vehicle information. You can usually do this online, over the phone, or by visiting a branch.

- Review and Approval: After submitting your application, 1st Advantage will review all your information, including pulling your credit report. They will then make a decision on your loan. If approved, you’ll receive an offer outlining the loan amount, interest rate, and terms.

- Sign and Fund: Carefully review all the loan documents. Once you understand and agree to the terms, you’ll sign the paperwork. After signing, the funds will be disbursed. If you’re buying from a dealership, the funds are often sent directly to them. For private sales or refinancing, the funds might be transferred to your account or the previous lender.

Following these steps meticulously will streamline your journey to securing a 1st Advantage Car Loan.

Expert Tips for a Successful 1st Advantage Car Loan Application

Getting approved for a car loan, especially one with favorable terms, often comes down to preparation and presenting yourself as a reliable borrower. Based on my experience working with countless individuals seeking financing, here are some pro tips to significantly boost your chances of approval for a 1st Advantage Car Loan.

- Boost Your Credit Score: This is arguably the most impactful step. Before applying, work on improving your credit. Pay down existing debts, especially credit card balances, and make all payments on time. Even a small increase in your score can lead to a better interest rate.

- Save for a Down Payment: While not always mandatory, a larger down payment signals to lenders that you are serious about your commitment and reduces their risk. It also means you’ll borrow less, resulting in lower monthly payments and less interest paid over the life of the loan.

- Establish a Budget and Stick to It: Understand how much car you can truly afford. Don’t just look at the monthly payment; consider insurance, maintenance, and fuel costs. A clear, realistic budget shows you’re a responsible borrower.

- Gather All Documents in Advance: Nothing slows down an application like missing paperwork. Have your identification, income verification, and any other required documents ready to go. This demonstrates your organization and commitment.

- Apply for Pre-Approval First: As mentioned, pre-approval is a powerful tool. It gives you a clear budget, simplifies negotiations at the dealership, and lets you know where you stand before you get emotionally attached to a specific vehicle.

- Be Honest and Transparent: Always provide accurate information on your application. Any misrepresentation can lead to delays, denial, or even legal issues. Transparency builds trust with your lender.

- Limit New Credit Applications: In the months leading up to your car loan application, try to avoid opening new credit cards or taking out other loans. Each new application can temporarily ding your credit score, making your auto loan approval harder.

- Maintain Stable Employment: Lenders prefer to see a consistent employment history. If you’ve recently changed jobs, ensure you can demonstrate a stable income and future prospects.

By implementing these pro tips, you’re not just applying for a 1st Advantage Car Loan; you’re strategically positioning yourself for the best possible outcome.

Common Mistakes to Avoid When Applying for an Auto Loan

While preparing for a successful application is crucial, it’s equally important to be aware of pitfalls that can derail your efforts. Based on common experiences I’ve observed, certain mistakes can lead to higher interest rates, denied applications, or even financial stress down the road. When pursuing a 1st Advantage Car Loan, steer clear of these common errors.

- Not Checking Your Credit Report Beforehand: This is a major oversight. Many applicants don’t review their credit report for inaccuracies or potential issues. A mistake on your report could unfairly lower your score and impact your loan terms. Always get your free annual report and dispute any errors.

- Applying to Too Many Lenders at Once: While it’s good to compare rates, submitting multiple applications in a short period can negatively affect your credit score. Each application typically results in a "hard inquiry," which can temporarily lower your score. Focus on a few reputable lenders, like 1st Advantage, after initial research.

- Focusing Only on the Monthly Payment: This is a classic dealer trick. While a low monthly payment sounds appealing, it often comes with a longer loan term, meaning you pay significantly more in interest over time. Always consider the total cost of the loan, including interest, not just the monthly installment.

- Not Understanding the Terms and Conditions: Many borrowers rush through loan documents without fully comprehending the fine print. Pay close attention to the interest rate (APR), loan term, any fees, prepayment penalties, and late payment clauses. Don’t be afraid to ask questions.

- Buying More Car Than You Can Afford: It’s easy to get carried away by an exciting new vehicle. However, overextending yourself financially can lead to payment struggles, affecting your credit and overall financial health. Stick to your budget, even if it means foregoing some optional features.

- Skipping the Pre-Approval Process: Not getting pre-approved means you go into a dealership blind. You lose significant negotiation power and might be pressured into less favorable financing options offered by the dealer.

- Forgetting About Additional Costs: A car’s price isn’t the only cost. Remember to factor in sales tax, registration fees, insurance, and ongoing maintenance. These can add hundreds or thousands to your annual vehicle expenses.

Avoiding these common mistakes will not only enhance your chances of securing a favorable 1st Advantage Car Loan but also contribute to a healthier financial future.

Understanding Interest Rates and Loan Terms

When you secure a 1st Advantage Car Loan, two of the most critical factors determining the total cost are the interest rate and the loan term. Grasping how these elements interact is fundamental to making a smart borrowing decision. Don’t just look at the monthly payment; dig deeper into the numbers.

The Interest Rate (APR)

The interest rate is essentially the cost of borrowing money, expressed as a percentage of the loan amount. However, you’ll often hear about the Annual Percentage Rate (APR). The APR is a more comprehensive measure, as it includes the interest rate plus any additional fees associated with the loan.

- Fixed vs. Variable Rates: Most auto loans, including those from 1st Advantage, are fixed-rate loans. This means your interest rate remains the same throughout the life of the loan, providing predictable monthly payments. Variable-rate loans, where the rate can change, are less common for auto financing but exist. Always confirm which type you’re getting.

- Impact on Total Cost: Even a small difference in APR can translate to significant savings or additional costs over the loan’s term. For example, a 0.5% lower APR on a $25,000 loan over five years can save you hundreds of dollars. This is why credit unions like 1st Advantage, known for competitive rates, can be a distinct advantage. Learn more about APR from the Consumer Financial Protection Bureau (CFPB) to fully understand its implications.

The Loan Term

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This choice has a direct impact on both your monthly payment and the total interest you’ll pay.

-

Shorter Terms: A shorter loan term means higher monthly payments but less interest paid overall. You’ll own your car outright sooner, and the total cost of the vehicle will be lower.

-

Longer Terms: A longer loan term results in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in interest over the life of the loan, and you’ll be making payments for a longer period, increasing the risk of negative equity (owing more than the car is worth).

-

Pro Tips from Us: While lower monthly payments from a longer term might seem appealing, always weigh it against the increased total cost. Try to choose the shortest loan term you can comfortably afford without straining your budget. A balanced approach ensures you’re not overpaying for your vehicle in the long run.

Refinancing Your Car Loan with 1st Advantage: A Smart Move?

Many people assume once they have a car loan, they’re stuck with it. However, that’s not always the case! Refinancing your auto loan with 1st Advantage Car Loan can be a smart financial move under certain circumstances. It’s essentially replacing your current car loan with a new one, ideally with more favorable terms.

When does it make sense to consider refinancing?

- Lower Interest Rates: If interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a lower APR. This can dramatically reduce your monthly payments and the total interest paid.

- Improved Credit Score: Perhaps when you initially financed your car, your credit wasn’t stellar. If you’ve diligently improved your credit history since then, 1st Advantage may offer you a much better rate now.

- Reduce Monthly Payments: If your financial situation has changed and you need to free up some cash flow, refinancing to a longer term (though be mindful of increased total interest) can lower your monthly payments.

- Shorten Your Loan Term: Conversely, if your income has increased, you might want to refinance to a shorter term. This will result in higher monthly payments but will save you a substantial amount in interest and help you pay off the car sooner.

- Remove a Co-signer: If you initially needed a co-signer to get approved, and your credit has since improved, refinancing can allow you to remove them from the loan.

The process for refinancing with 1st Advantage is similar to applying for a new loan. You’ll submit an application, they’ll review your credit and vehicle information, and if approved, you’ll sign new loan documents. It’s always worth exploring if refinancing can put more money back in your pocket.

Beyond the Loan: Customer Service and Support with 1st Advantage

Securing a 1st Advantage Car Loan is just the beginning of your financial relationship. A key differentiator for credit unions, including 1st Advantage, is their emphasis on member service and ongoing support. This aspect can significantly enhance your overall borrowing experience.

What can you expect after your loan is approved and funded?

- Accessible Support: Credit unions typically offer multiple channels for customer support, including in-person at branches, phone support, and online banking platforms. If you have questions about your payments, statements, or any other aspect of your loan, help is usually readily available.

- Online Account Management: Most modern financial institutions, including 1st Advantage, provide robust online banking portals and mobile apps. These tools allow you to view your loan balance, make payments, set up auto-pay, and access statements conveniently from your computer or smartphone.

- Financial Education Resources: As member-focused organizations, credit unions often provide resources to help members manage their finances better. This might include workshops, online articles, or one-on-one counseling. These resources can be invaluable for budgeting, credit improvement, and future financial planning.

- Relationship-Based Banking: Unlike transactional banking, 1st Advantage aims to build long-term relationships with its members. This means they are often more willing to work with you if you encounter financial difficulties, potentially offering solutions like payment deferrals or modified terms, rather than immediately resorting to punitive measures.

The continued support and personalized approach from 1st Advantage Car Loan contribute to a more positive and less stressful car ownership experience. This holistic approach to member well-being is a significant advantage over many traditional lenders.

Comparing 1st Advantage to Other Lenders: Doing Your Due Diligence

While this guide highlights the many benefits of a 1st Advantage Car Loan, it’s always wise to conduct your own comparison. No single lender is universally perfect for everyone, and what works best for one person might not be ideal for another. Based on my expertise, smart borrowers always do their due diligence.

Here’s how to effectively compare 1st Advantage with other potential lenders:

- Gather Quotes: Apply for pre-approval not just with 1st Advantage, but also with a few other reputable lenders. This could include other credit unions, online lenders, and traditional banks. Ensure you do this within a short window (typically 14-45 days, depending on the credit model) to minimize the impact on your credit score.

- Compare APRs, Not Just Interest Rates: Remember that APR includes fees, giving you a truer picture of the total borrowing cost.

- Evaluate Loan Terms: Look at the range of loan terms offered by each lender. Does 1st Advantage offer the flexibility you need?

- Assess Fees: Some lenders charge origination fees, application fees, or prepayment penalties. Always ask about all potential fees. Credit unions often have fewer fees than banks.

- Read Reviews and Testimonials: Look for what existing customers say about their experience with each lender, focusing on customer service, ease of application, and responsiveness.

- Consider Special Programs: Some lenders offer unique programs for specific situations, such as first-time buyers, students, or those with less-than-perfect credit. See if 1st Advantage or others have any relevant niche offerings.

- Check Membership Requirements: For credit unions like 1st Advantage, confirm you meet the membership criteria before getting too far into the process.

By systematically comparing these factors, you can confidently determine if a 1st Advantage Car Loan is indeed the best fit for your unique financial situation and car buying goals. Remember, the goal is to secure the most advantageous terms possible. If you’re considering a new vehicle, our article on The Ultimate Guide to Buying a New Car (simulated internal link) offers valuable advice to prepare you for the entire process.

Conclusion: Driving Forward with Confidence and 1st Advantage

Navigating the world of auto financing can be challenging, but with the right knowledge and a clear strategy, you can secure a loan that serves your best interests. This comprehensive guide has aimed to demystify the 1st Advantage Car Loan, presenting it as a strong contender for anyone seeking a reliable and member-focused auto financing solution.

From their competitive interest rates and flexible terms to their personalized customer service and straightforward application process, 1st Advantage Federal Credit Union consistently strives to provide a genuine advantage to its members. By understanding their offerings, preparing your application meticulously, and avoiding common pitfalls, you significantly increase your chances of securing favorable loan terms.

Remember, a car loan is a significant financial commitment. Take the time to evaluate all your options, leverage the insights shared in this guide, and don’t hesitate to ask questions. With 1st Advantage Car Loan, you have the potential to not only finance your dream car but also to do so with the confidence that you’ve made a smart, well-informed decision. Get ready to hit the road with peace of mind.