Accelerate Your Financial Freedom: The Ultimate Guide to Paying Down Your Car Loan Faster

Accelerate Your Financial Freedom: The Ultimate Guide to Paying Down Your Car Loan Faster Carloan.Guidemechanic.com

For many, a car is an essential part of daily life, offering convenience and independence. However, the monthly car loan payment can often feel like a heavy anchor, tethering your finances for years. Imagine a world where that payment is gone, freeing up hundreds of dollars each month for savings, investments, or simply more breathing room.

This isn’t just a pipe dream; it’s an achievable goal. As an expert blogger and someone deeply invested in financial well-being, I’ve seen firsthand the transformative power of proactive debt management. This comprehensive guide will equip you with proven strategies to pay down your car loan faster, saving you a significant amount on interest and accelerating your journey to financial freedom. Let’s unlock the secrets to early auto loan payoff and reclaim your financial power!

Accelerate Your Financial Freedom: The Ultimate Guide to Paying Down Your Car Loan Faster

Why Paying Down Your Car Loan Faster Is a Smart Move

Before we dive into the "how," let’s solidify the "why." Understanding the profound benefits of an early car loan payoff can be a powerful motivator. It’s not just about getting rid of a bill; it’s about optimizing your financial life.

Save a Significant Amount on Interest

Every car loan comes with an interest rate, which is essentially the cost of borrowing money. The longer you take to repay your loan, the more interest accrues over time. By accelerating your payments, you reduce the principal balance more quickly, meaning less interest has the chance to accumulate. This translates into real money saved – money that stays in your pocket, not the lender’s.

Consider a typical car loan. Even a seemingly small interest rate can add up to thousands of dollars over a five or six-year term. Paying off your loan even a year or two early can shave a substantial amount off the total cost of your vehicle. It’s one of the most direct ways to boost your personal savings.

Achieve Financial Freedom Sooner

Debt, of any kind, can be a burden. Eliminating your car loan payment means one less fixed expense draining your monthly budget. This newfound flexibility allows you to redirect those funds towards other crucial financial goals, whether it’s building an emergency fund, saving for a down payment on a home, or investing for retirement.

Think about the mental weight lifted when you know your car is truly yours, free and clear. This peace of mind is invaluable. It opens doors to more opportunities and reduces financial stress, allowing you to focus on what truly matters.

Reduce Overall Debt Burden and Improve Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a key metric lenders use to assess your financial health. A lower DTI ratio indicates that you have more income available to cover your debts, making you a more attractive borrower for future loans, like a mortgage. Paying off your car loan significantly reduces your overall debt burden, thereby improving this crucial ratio.

This improved financial standing can also make it easier to secure other lines of credit at more favorable terms down the road. It’s a foundational step towards building a stronger financial profile and enhancing your creditworthiness.

Free Up Monthly Cash Flow

Imagine having an extra $300, $400, or even $500 available in your budget every single month. What could you do with that money? This is the immediate and tangible benefit of an early car loan payoff. That cash flow can be used to tackle other higher-interest debts, boost your savings, or simply provide more disposable income for your lifestyle.

Based on my experience, the psychological boost of freeing up monthly cash flow is immense. It creates a sense of empowerment and control over your finances, which can motivate you to pursue even greater financial achievements. It’s a powerful catalyst for positive financial change.

Understanding Your Car Loan: The Foundation of Early Payoff

Before you can effectively strategize to pay down your car loan faster, you need a clear understanding of how your specific loan works. This knowledge is your roadmap to smart repayment.

Key Components: Principal, Interest Rate, and Loan Term

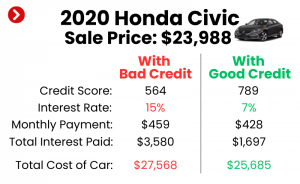

Every car loan is comprised of a few fundamental elements. The principal is the actual amount of money you borrowed to purchase the vehicle. The interest rate is the percentage charged by the lender for that borrowed money, and it’s a critical factor in how much you’ll ultimately pay. Finally, the loan term is the duration over which you’ve agreed to repay the loan, typically measured in months (e.g., 60 months, 72 months).

Understanding how these three components interact is crucial. A higher interest rate means more of your payment goes towards interest, especially in the early stages of the loan. A longer loan term, while offering lower monthly payments, almost always results in paying significantly more in total interest over the life of the loan.

The Amortization Schedule

Your car loan operates on an amortization schedule. This fancy term simply means that over the life of your loan, your payments are structured so that a larger portion goes towards interest in the beginning, and a larger portion goes towards the principal balance as you get closer to the end. This is why early extra payments are so powerful – they directly attack the principal when it makes the biggest difference.

Pro tips from us: Ask your lender for your amortization schedule or find an online calculator. Seeing how much interest you’re paying in the early months can be a huge motivator to accelerate your payments. It vividly illustrates where your money is going.

Prepayment Penalties: A Crucial Consideration

Before making any extra payments, it is absolutely vital to check your loan agreement for any prepayment penalties. Some lenders charge a fee if you pay off your loan early, designed to recoup the interest they would have otherwise earned. While less common with auto loans than with mortgages, they do exist.

Common mistakes to avoid are diving into an aggressive payoff plan without first confirming there are no penalties. If your loan does have a prepayment penalty, you’ll need to calculate whether the interest saved by paying early outweighs the cost of the penalty. In many cases, even with a penalty, paying early can still save you money, but it’s essential to do the math.

Proven Strategies to Pay Down Your Car Loan Faster

Now, let’s get into the actionable strategies. These are the methods that, based on my experience, have consistently helped individuals accelerate their car loan repayment and achieve financial peace of mind.

1. Make Extra Payments Whenever Possible

This is perhaps the most straightforward and effective strategy. Any amount you pay over your minimum monthly payment goes directly towards reducing your principal balance, assuming your lender applies it correctly (more on this later).

-

Lump Sum Payments: Did you receive a tax refund, an annual bonus, a work commission, or even a thoughtful monetary gift? Instead of spending it, consider applying a portion or all of it as an extra payment on your car loan. A single lump sum payment can significantly reduce your principal and shorten your loan term. This is a game-changer for many.

-

Rounding Up Payments: If your monthly payment is, say, $347, consider rounding it up to $350 or even $375. While seemingly small, these consistent extra amounts add up rapidly over time. It’s an easy way to make additional payments without feeling a huge pinch in your budget.

-

One Extra Payment Per Year: This strategy is simple yet powerful. Divide your regular monthly payment by 12 and add that amount to each of your 12 monthly payments. Alternatively, you can simply make an entire extra payment once a year. By doing so, you’ll effectively make 13 monthly payments instead of 12, significantly shaving off your loan term and interest.

Pro tips from us: Always specify to your lender that any extra payments should be applied directly to the principal balance, not towards future payments. This ensures your efforts are truly accelerating your payoff, not just building a credit for next month’s bill.

2. Switch to Bi-Weekly Payments

This is a clever trick that works wonders without requiring a massive overhaul of your budget. Instead of making one full payment once a month, you make half of your payment every two weeks.

How it works: There are 52 weeks in a year, which means 26 bi-weekly periods. If you make half a payment every two weeks, you’ll end up making 26 half-payments, which equates to 13 full monthly payments over the course of a year, rather than the standard 12. This "extra" payment each year has the same effect as the "one extra payment per year" strategy, but it often feels less burdensome because the payments are smaller and more frequent.

This method often aligns well with bi-weekly paychecks, making it easier to budget. Just ensure your lender can accommodate bi-weekly payments or set up an automated transfer from your bank.

3. Refinance Your Car Loan for Better Terms

Refinancing involves taking out a new loan to pay off your existing car loan. This can be a highly effective strategy if you can secure a lower interest rate or a shorter loan term.

-

When it Makes Sense: Refinancing is particularly beneficial if your credit score has improved since you first took out the loan, if current interest rates are lower than when you financed, or if you initially accepted a high-interest loan and now qualify for better terms. A lower interest rate means more of your payment goes towards principal, accelerating your payoff.

-

Process and Things to Watch Out For: Shop around for the best rates from multiple lenders – banks, credit unions, and online lenders. Be wary of refinancing for a longer loan term, even if it offers a lower monthly payment. While it might reduce your immediate outlay, it will almost certainly increase the total interest you pay over the life of the loan. The goal here is to pay down your car loan faster, not just reduce your monthly obligation.

4. Generate Extra Income Specifically for Debt Reduction

Sometimes, simply cutting expenses isn’t enough, or you’ve already trimmed your budget to the bone. In such cases, actively increasing your income can be a powerful lever to accelerate your car loan payoff.

-

Side Hustles: Explore opportunities for a side hustle. This could be anything from freelance writing or graphic design to driving for a ride-sharing service, pet sitting, or delivering food. Even a few hundred extra dollars a month can make a significant difference in your repayment schedule.

-

Selling Unused Items: Look around your home. Do you have electronics, clothing, furniture, or collectibles that you no longer use or need? Platforms like eBay, Facebook Marketplace, and local consignment shops can help you turn these items into cash. Every dollar earned can be directly applied to your car loan.

Based on my experience, earmarking this extra income specifically for your car loan creates a powerful mental link and keeps you motivated. It’s not just "extra money"; it’s "car loan freedom money."

5. Allocate Windfalls Wisely

Unexpected money often feels like a bonus, and it’s tempting to splurge. However, these windfalls present a golden opportunity to make a substantial dent in your car loan.

-

Tax Refunds: Many people view their tax refund as "found money." Instead of a shopping spree, consider applying a significant portion, or even all, of your refund directly to your car loan principal. This can shorten your loan term by months, if not a year or more.

-

Bonuses and Inheritances: If you receive a work bonus, a gift, or a small inheritance, resist the urge for immediate gratification. While treating yourself a little is fine, prioritize your financial health by using a large part of these funds to make a lump sum payment on your auto loan.

Common mistakes to avoid are letting these windfalls disappear into everyday spending without a plan. Be intentional about how you use this money to accelerate your debt payoff.

6. Cut Unnecessary Expenses and Reallocate Savings

This strategy involves a thorough review of your budget to find areas where you can trim spending and redirect those savings towards your car loan.

-

Budgeting Deep Dive: Take a close look at your monthly expenditures. Are there subscriptions you no longer use? Can you reduce your dining out frequency? Are there cheaper alternatives for your coffee habit or entertainment? Even small, consistent cuts can free up surprising amounts of cash.

-

Automate Savings: Once you identify areas to cut, automate the transfer of those saved funds directly to your car loan. This removes the temptation to spend the money elsewhere and ensures your efforts are consistent.

– for more in-depth strategies on how to create a budget that works for you. Remember, every dollar saved is a dollar that can work towards your debt freedom.

7. Consider a Shorter Loan Term (During Refinancing)

If you’re in a position to refinance your loan, actively pursue a shorter loan term. While this will likely result in higher monthly payments, it dramatically reduces the total interest you pay over the life of the loan.

For example, refinancing from a 72-month loan to a 48-month loan might increase your monthly payment, but the overall interest savings can be substantial. This strategy is best suited for those whose financial situation has improved and can comfortably handle the increased monthly obligation. It’s a direct route to an early auto loan payoff.

8. Debt Snowball or Avalanche Method (Broader Strategy)

While these are general debt payoff strategies, they can certainly be applied to your car loan within a larger debt management plan.

- Debt Snowball: You pay off your smallest debt first, regardless of interest rate, then roll that payment into the next smallest debt. The psychological wins of seeing debts disappear quickly can be highly motivating.

- Debt Avalanche: You prioritize paying off the debt with the highest interest rate first. This method saves you the most money on interest in the long run.

If your car loan has a high interest rate compared to other debts, the avalanche method would prioritize it. If it’s one of your smaller debts, the snowball method might help you gain momentum.

Common Mistakes to Avoid When Paying Off Your Car Loan Early

While the desire to pay down your car loan faster is commendable, certain pitfalls can derail your efforts or even cause financial harm. Being aware of these common mistakes can save you a lot of headache and money.

Ignoring Prepayment Penalties

As mentioned earlier, some loans come with fees for early payoff. Common mistakes to avoid are neglecting to check your loan agreement for these clauses. A prepayment penalty could potentially negate some or all of your interest savings. Always verify this detail with your lender before making substantial extra payments.

Not Specifying Extra Payments Go to Principal

This is a critical point. When you send in an extra payment, your lender might, by default, apply it to your next month’s payment or use it to pay down accrued interest first. While technically helpful, it doesn’t directly reduce the principal balance in the most effective way for early payoff.

Pro tips from us: Always include a note with your payment (if mailing a check) or contact your lender directly (if paying online or via phone) to explicitly state that the extra funds should be applied solely to the principal balance. This ensures your efforts are maximally effective.

Sacrificing Your Emergency Fund

While aggressively paying off debt is a smart move, it should never come at the expense of your financial security. Depleting your emergency fund to pay off your car loan leaves you vulnerable to unexpected expenses like job loss, medical emergencies, or home repairs.

An adequate emergency fund (typically 3-6 months of living expenses) is your financial safety net. Prioritize building and maintaining this fund before dedicating every spare dollar to accelerated debt repayment. Financial stability comes before hyper-aggressive payoff.

Refinancing for a Longer Term (Even with Lower Rates)

The temptation to lower your monthly payment by extending your loan term is strong, especially if you qualify for a lower interest rate. However, this is a common mistake that often leads to paying more interest overall. While the monthly payments feel lighter, you’re stretching out the interest accrual over a longer period.

Remember, the goal is to pay down your car loan faster and save money, not just to reduce your monthly obligation. Only consider refinancing for a shorter term, even if it means a slightly higher monthly payment.

Overlooking Other High-Interest Debt

Your car loan might not be your highest-interest debt. If you also carry balances on credit cards, personal loans, or other debts with significantly higher interest rates, prioritizing those might be a more financially savvy move. The "debt avalanche" method dictates tackling the highest interest debt first to save the most money.

Evaluate your entire debt portfolio. While paying off your car loan is a great goal, ensure it aligns with your broader financial strategy for maximum impact.

The Psychological Benefits of Early Car Loan Payoff

Beyond the tangible financial savings, there’s a powerful psychological component to paying off your car loan early. These benefits often provide the motivation needed to stay disciplined and committed to your payoff plan.

Peace of Mind and Reduced Stress

Debt can be a constant source of stress and worry. The knowledge that you owe money, especially on a depreciating asset like a car, can weigh heavily on your mind. Eliminating that obligation brings a profound sense of relief and peace. You’ll no longer have that recurring payment looming over your head, allowing you to breathe easier and focus on other aspects of your life.

Motivation for Other Financial Goals

Achieving one significant financial goal, like paying off your car loan, creates momentum. It proves to yourself that you are capable of disciplined financial management and can achieve ambitious targets. This success often spills over, motivating you to tackle other debts, build substantial savings, or accelerate your investment journey. It’s a powerful positive feedback loop.

Creating Your Personalized Car Loan Payoff Plan

Ready to take control? Here’s a simple framework to build your own plan to pay down your car loan faster.

- Assess Your Current Situation: Gather all the details of your car loan: original principal, current principal balance, interest rate, remaining term, and minimum monthly payment. Understand your budget and identify how much extra you can realistically afford to pay each month without jeopardizing your emergency fund or other essential expenses.

- Choose Strategies That Fit: Based on your assessment, select one or more of the strategies outlined above. Can you make an extra payment each year? Is refinancing an option? Can you cut expenses or generate extra income? Start with what feels most achievable.

- Set Realistic Goals: Don’t try to pay off your loan in three months if you have five years left and limited extra income. Set a realistic target, such as paying it off six months or a year early. Break it down into smaller, manageable steps.

- Monitor Your Progress: Regularly check your loan balance and track how much interest you’re saving. Seeing your principal balance shrink and your estimated payoff date move closer can be incredibly motivating. Adjust your plan as your financial situation changes.

Link to External Source: Consumer Financial Protection Bureau – Auto Loan Basics – for more government-backed information on understanding auto loans.

Conclusion: Drive Towards Financial Freedom Today!

Paying down your car loan faster is more than just a financial maneuver; it’s a strategic move towards greater financial freedom and peace of mind. By understanding your loan, implementing smart strategies like making extra payments, refinancing, or generating additional income, and avoiding common pitfalls, you can significantly reduce the total cost of your vehicle and free up valuable cash flow.

The journey to an early auto loan payoff might require discipline and consistency, but the rewards are well worth the effort. Imagine the day you make that final payment and receive your lien release – a tangible symbol of your achievement. Start implementing these strategies today, and take a significant step towards accelerating your financial well-being. Your future self will thank you for driving towards debt-free living!