Allstate Car Loans

Allstate Car Loans Carloan.Guidemechanic.com

Navigating the Road to Your Next Vehicle: A Comprehensive Guide to Allstate Car Loans and Smart Auto Financing

Allstate Car Loans

The journey to owning a new or pre-owned vehicle is often exciting, filled with dreams of open roads and new adventures. But before you hit the accelerator, there’s a crucial pit stop: securing the right financing. Many consumers naturally wonder about their trusted insurance provider’s role in this process, leading to questions like, "Does Allstate offer car loans?" or "How can Allstate help me finance my vehicle?"

This isn’t just a simple query; it’s a doorway into understanding the intricate relationship between auto insurance, financial services, and the broader car loan market. As an expert who has spent years dissecting consumer finance and auto trends, I’ve observed firsthand the confusion and opportunities that arise when these worlds intersect. My mission with this pillar article is to cut through the noise, provide clarity, and equip you with the knowledge to make the smartest financial decisions for your next car purchase.

We’ll explore the nuances of Allstate car loans, clarify Allstate’s actual role in vehicle financing, and then dive into a robust guide for securing the best auto loan for your needs. From understanding interest rates to navigating the application process and leveraging your existing insurance relationship, this article is designed to be your ultimate co-pilot on the road to a successful car purchase. Get ready to transform uncertainty into confidence as we unlock the secrets to smart auto financing.

Demystifying Allstate’s Involvement in Car Loans: Protection First, Partnership Second

When you hear "Allstate," the immediate thought is usually protection. For decades, Allstate has been a household name synonymous with insurance, safeguarding homes, lives, and, most notably for car owners, vehicles. This core identity as an insurer is crucial to understanding their position in the car loan landscape.

Allstate’s Primary Mission: Protection, Not Lending

At its heart, Allstate is an insurance giant. Their primary business model revolves around assessing risk and providing financial protection against unforeseen events. This means their expertise and services are focused on offering policies like comprehensive, collision, liability, and other forms of auto insurance. Directly issuing traditional car loans, where they act as the principal lender, falls outside their core operational framework.

Based on my experience tracking major financial institutions, it’s common for large corporations to specialize. Allstate has perfected the art of insurance, building robust systems and a vast network to serve policyholders. Diverting significant resources to become a direct auto lender would require a completely different operational structure, regulatory compliance, and market strategy – a path they generally haven’t pursued in the traditional sense.

Strategic Partnerships and Referral Networks

While Allstate itself doesn’t typically provide direct car loans, this doesn’t mean they operate in a vacuum regarding your car purchase. Large financial entities often form strategic alliances. Allstate may, through various programs or affiliates, connect their customers with preferred lending partners or provide advice through their financial advisors. These partnerships are designed to offer a more holistic service experience to their existing policyholders.

For instance, an Allstate financial professional might guide you through budgeting for a car purchase or offer insights into the types of loans available. They could also refer you to trusted banks or credit unions with whom they have established relationships. It’s important to clarify that such referrals are about facilitating your search, not Allstate itself extending the credit. This distinction is vital for setting realistic expectations.

The Intertwined World of Insurance and Financing: Where Allstate Truly Shines

Where Allstate truly becomes indispensable in your car financing journey is after you’ve secured your loan. Every financed vehicle requires insurance – often comprehensive and collision coverage – to protect the lender’s investment. This is where Allstate’s expertise directly benefits you.

Once you have a loan, your car becomes an asset that needs safeguarding. Allstate steps in to provide that crucial protection, ensuring that in the event of an accident, theft, or damage, both you and the lender are covered. This is the natural synergy: you get the loan from a lender, and Allstate protects the asset that secures that loan. Understanding this relationship helps you appreciate the full spectrum of services Allstate can offer in relation to your car ownership.

Navigating the Car Loan Landscape: A Borrower’s Blueprint

Even without Allstate being a direct lender, their presence as your insurer or a potential advisor makes understanding the car loan landscape paramount. Your goal is to secure the most favorable terms possible, and that requires a strategic approach.

The Power of Pre-Approval: Your Secret Weapon

One of the most impactful steps you can take is to get pre-approved for a car loan before you step foot in a dealership. Based on my experience, this single action shifts the power dynamic significantly in your favor. When you walk into a dealership with a pre-approval in hand, you’re no longer just a shopper; you’re a buyer with established financing.

Pre-approval provides you with a clear understanding of how much you can borrow, at what interest rate, and what your estimated monthly payments will be. This knowledge empowers you to negotiate the car’s price based on its actual value, rather than being swayed by monthly payment figures dictated by the dealer’s financing options. It also streamlines the buying process, saving you time and stress at the dealership.

Understanding Loan Types: Tailoring Your Financing

Not all car loans are created equal. The type of loan you seek will depend on the vehicle you’re purchasing and your financial goals.

- New Car Loans: Typically offer the lowest interest rates due to the vehicle’s high value and lower depreciation risk for the lender. Terms can range from 36 to 72 months, sometimes even longer.

- Used Car Loans: Rates are usually slightly higher than new car loans, reflecting the increased risk associated with an older vehicle. Lenders often have age and mileage restrictions for used car financing.

- Refinancing Loans: This involves replacing an existing car loan with a new one, often to secure a lower interest rate, reduce monthly payments, or change the loan term. This is an excellent option if your credit score has improved since your initial purchase or if market rates have dropped.

Key Factors Influencing Your Loan: The Pillars of Approval

Lenders evaluate several critical factors when considering your loan application. Understanding these can help you prepare and present yourself as a low-risk borrower.

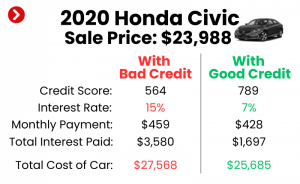

- Credit Score: Your credit score is arguably the most significant determinant of your interest rate. A higher score (generally 700+) indicates a history of responsible borrowing and will unlock the most competitive rates. Lenders use this score to gauge your creditworthiness.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have sufficient income to manage additional debt. A high DTI can signal financial strain.

- Down Payment: A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. It also demonstrates your financial commitment to the purchase.

- Loan Term: This is the length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but result in more interest accumulating over time. It’s a balance between affordability and total cost.

The Application Process: From Documents to Driving Away

Once you’ve identified potential lenders and understand the types of loans available, the application process itself becomes the next hurdle. While specific requirements vary, a general framework applies to most auto loan applications.

Gathering Your Documents: Preparation is Key

Before you even begin filling out forms, compile all necessary documentation. This proactive step can significantly expedite the process.

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2 forms, tax returns (if self-employed). Lenders need to verify your ability to repay the loan.

- Proof of Residence: Utility bills, lease agreements, or mortgage statements showing your current address.

- Credit History: While lenders will pull your credit report, it’s wise to review your own beforehand for any discrepancies.

- Vehicle Information: If you’ve already picked a car, have its VIN, make, model, and mileage ready. This is especially true for used cars.

Filling Out the Application: Precision Matters

Accuracy is paramount when completing your loan application. Any discrepancies or errors could lead to delays or even rejection.

- Be Honest and Thorough: Provide accurate information about your financial situation. Lenders will verify the details, and misrepresentations can have serious consequences.

- Understand Every Field: If you’re unsure about a question, ask for clarification. Don’t guess.

- Review Before Submitting: Double-check all entries for typos or mistakes before hitting that submit button.

Understanding the Offer: Beyond the Monthly Payment

Once approved, you’ll receive a loan offer. This is where many borrowers make a common mistake: focusing solely on the monthly payment. Pro tips from us emphasize looking at the complete picture.

- Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and any fees. A lower APR is always better.

- Total Loan Cost: Calculate the total amount you will pay over the life of the loan, including principal and all interest. This gives you a clear financial perspective.

- Loan Term: Reconfirm the length of the loan and how it aligns with your long-term financial strategy.

- Prepayment Penalties: Check if there are any penalties for paying off your loan early. Ideally, you want a loan without such restrictions, allowing you flexibility.

Maximizing Your Allstate (Insurance) Benefits with Your Car Loan

Here’s where being an Allstate customer, or considering becoming one, truly aligns with your car loan. While they don’t directly lend, their insurance products are integral to financed vehicles.

Bundling Opportunities: Smart Savings

Allstate, like many insurers, often provides discounts for bundling multiple policies. If you already have home insurance or life insurance with Allstate, adding your auto policy could unlock significant savings.

- The "Good Hands" Discount: Inquire about multi-policy discounts. These savings can effectively offset part of your monthly car payment, making your overall car ownership more affordable.

- Loyalty Rewards: Long-term customers may also qualify for additional loyalty benefits or preferred rates, further enhancing your financial position.

GAP Insurance: Essential Protection for Financed Vehicles

This is one of the most critical insurance products for anyone with a car loan, especially for new vehicles that depreciate quickly.

- What it Is: Guaranteed Asset Protection (GAP) insurance covers the "gap" between what you owe on your car loan and your car’s actual cash value (ACV) if it’s totaled or stolen.

- Why It Matters: If your car is totaled, your standard auto insurance policy will only pay out the ACV. If you owe more than that on your loan, you’re responsible for the difference. GAP insurance steps in to cover that remaining balance, preventing you from being upside down on a car you no longer own.

- Allstate’s Role: Allstate offers GAP insurance as an add-on to many of its auto policies, providing peace of mind and crucial financial protection against an unforeseen loss.

Roadside Assistance: An Often-Overlooked Benefit

Many Allstate auto policies include roadside assistance, a practical benefit that can save you money and stress.

- Coverage: This typically includes services like towing, jump-starts, flat tire changes, fuel delivery, and lockout services.

- Value Proposition: For a financed vehicle, being stranded on the side of the road can be particularly stressful. Allstate’s roadside assistance ensures you’re never alone, and it avoids out-of-pocket expenses for unexpected breakdowns. This means less financial strain and more confidence in your drive.

Pro Tips for Securing the Best Car Loan: My Expert Recommendations

Drawing from my extensive experience in consumer finance, these actionable tips can significantly improve your chances of securing the most advantageous car loan terms.

- Shop Around Extensively: Never settle for the first loan offer, especially from a dealership. Dealers often mark up interest rates to increase their profit. Instead, apply with multiple lenders – banks, credit unions, and online lenders – within a short timeframe (usually 14-45 days, depending on the credit scoring model) to minimize the impact on your credit score. This allows you to compare offers side-by-side and choose the absolute best rate and terms.

- Improve Your Credit Score Before Applying: This is a golden rule. Even a slight increase in your score can translate to significant savings over the life of the loan.

- Pay Bills On Time: Payment history is the biggest factor in your score.

- Reduce Existing Debt: Lowering your credit utilization ratio can boost your score.

- Check for Errors: Review your credit report regularly for inaccuracies that could be dragging your score down.

- Internal Link Idea: For more in-depth strategies, check out our guide on "Boosting Your Credit Score: A Comprehensive Checklist."

- Negotiate Like a Pro: Don’t just negotiate the car’s price; negotiate the loan terms as well. With a pre-approval in hand, you have leverage. You can ask the dealer to beat your pre-approved rate, or at least match it. Remember, everything is negotiable, from the sales price to the financing terms and trade-in value.

- Read the Fine Print, Every Single Word: This cannot be stressed enough. Common mistakes to avoid include skimming the loan agreement. Pay close attention to:

- Prepayment Penalties: As mentioned, ensure you can pay off your loan early without extra fees.

- Hidden Fees: Look for origination fees, documentation fees, or any other charges that inflate the total cost.

- Late Payment Penalties: Understand the consequences of missed or late payments.

- Automatic Payment Discounts: Some lenders offer a slight interest rate reduction for setting up automatic payments.

Common Mistakes to Avoid When Getting a Car Loan

Even the most informed borrowers can sometimes fall prey to common pitfalls. Being aware of these can save you thousands of dollars and a lot of stress.

- Focusing Only on Monthly Payments: Dealers love to talk about low monthly payments because it distracts from the total cost. A lower monthly payment often means a longer loan term and significantly more interest paid over time. Always ask for the total cost of the loan.

- Ignoring the Total Cost of the Loan: This ties into the previous point. The interest rate multiplied by the loan term, plus the principal, gives you the true financial impact. A slightly higher monthly payment on a shorter term can be far more economical in the long run.

- Not Understanding Add-ons: When you’re in the finance office, you might be offered various add-ons like extended warranties, rustproofing, or fabric protection. While some can be valuable (like GAP insurance), many are overpriced or unnecessary. Understand each one, their cost, and whether you truly need them before signing.

- Applying for Too Many Loans at Once (Without Strategy): While shopping around is crucial, indiscriminately applying to many lenders over a long period can negatively impact your credit score due to multiple hard inquiries. Use the credit score "shopping window" effectively.

Refinancing Your Allstate-Insured Vehicle: When and How

Refinancing your car loan can be a powerful financial move, especially if your circumstances have changed since you first financed your vehicle. This is particularly relevant for those with an Allstate-insured car who might be looking to reduce their monthly outgoings.

When is Refinancing a Good Idea?

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you’re likely eligible for a lower interest rate.

- Lower Market Rates: Interest rates fluctuate. If current auto loan rates are lower than what you’re paying, refinancing can save you money.

- To Lower Monthly Payments: If you’re facing financial strain, extending your loan term through refinancing can reduce your monthly burden, though it might increase total interest paid.

- To Shorten Your Loan Term: Conversely, if your financial situation has improved, you might refinance to a shorter term to pay off the car faster and reduce total interest.

- To Remove a Co-signer: If a co-signer was needed initially, but your credit has strengthened, refinancing can release them from their obligation.

The Refinancing Process:

- Check Current Rates: Research current auto loan rates from various lenders.

- Gather Documents: Similar to an initial loan, you’ll need proof of income, identity, and your current loan details.

- Apply to Multiple Lenders: Shop around for the best refinancing offer.

- Review the New Loan Offer: Compare the new APR, monthly payment, and total cost to your existing loan.

- Finalize and Sign: If the new offer is better, complete the paperwork, and the new lender will pay off your old loan.

- External Link Idea: For a broader understanding of refinancing, consider exploring resources from the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. Their guides offer excellent, unbiased information on managing loans.

The Future of Car Financing and Allstate’s Evolving Role

The automotive and financial industries are in constant flux, driven by technological advancements and shifting consumer expectations. The future promises even more streamlined, personalized financing options.

- Digitalization and AI: Expect an even greater shift towards fully online applications, instant approvals, and AI-driven personalized loan offers based on your financial profile.

- Embedded Finance: We may see more "embedded" financing options directly integrated into the car-buying process, whether through manufacturer platforms or partnerships with insurance providers.

- Allstate’s Continued Relevance: As an insurer, Allstate will continue to be a vital part of car ownership. Their role might evolve to include even more sophisticated advisory services or integrated platforms that simplify the entire car ownership lifecycle, from financing to insuring and maintaining your vehicle. They could leverage their vast customer data to offer highly personalized insurance products that align seamlessly with your financing terms.

Your Journey to a Financed Vehicle, Supported by Smart Choices

Navigating the world of car loans can seem daunting, but armed with the right knowledge, it becomes a clear path. While Allstate car loans aren’t a direct lending product from the insurance giant, Allstate plays a pivotal role in protecting your financed asset and can be a valuable resource through its partnerships and financial advice.

Remember the key takeaways: pre-approval is your power, shopping around for rates is non-negotiable, understanding all loan terms is crucial, and leveraging your insurance provider for essential coverage like GAP insurance offers invaluable peace of mind. By adopting these strategies, you’re not just getting a car loan; you’re making a smart financial decision that supports your goals and protects your investment.

As you embark on your next vehicle purchase, remember that the "Good Hands" of Allstate are there to protect your ride, allowing you to focus on the open road ahead. Drive safely and finance wisely!