Amdm Car Loans and Leases: Your Ultimate Guide to Driving Away with Confidence

Amdm Car Loans and Leases: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Driving a new or used vehicle is more than just a convenience; for many, it’s a necessity, a passion, or a symbol of freedom. However, the path to vehicle ownership or long-term usage can often seem complex, especially when it comes to financing. This is where understanding your options, particularly with providers like Amdm Car Loans And Leases, becomes crucial.

This comprehensive guide is designed to demystify the world of automotive financing, offering an in-depth look at both car loans and leases through the lens of Amdm’s offerings. Our goal is to equip you with the knowledge and confidence to make an informed decision that perfectly aligns with your financial situation and lifestyle. Let’s embark on this journey to secure your next ride with Amdm!

Amdm Car Loans and Leases: Your Ultimate Guide to Driving Away with Confidence

Understanding Amdm Car Loans: Your Path to Ownership

An Amdm Car Loan represents a direct route to vehicle ownership. When you opt for a car loan, you are essentially borrowing a specific amount of money from a financial institution, like Amdm, to purchase a vehicle outright. This borrowed sum, plus interest, is then repaid over a predetermined period, typically ranging from 24 to 84 months.

The fundamental appeal of an Amdm car loan lies in the fact that, once the loan is fully repaid, the vehicle becomes entirely yours. This means you build equity with each payment and have complete freedom over your car’s usage, modifications, and eventual resale. It’s a commitment to ownership, offering stability and long-term value.

What is an Amdm Car Loan?

An Amdm Car Loan is a financial product designed to help individuals acquire a vehicle by providing the necessary funds upfront. Amdm, as a financing provider, aims to offer competitive interest rates and flexible repayment terms, making vehicle ownership accessible to a wide range of customers. They act as your partner in converting your dream car into a tangible asset.

The loan agreement outlines the principal amount borrowed, the annual percentage rate (APR), the repayment schedule, and any associated fees. Understanding these terms thoroughly before signing is paramount to ensuring a comfortable and manageable financial commitment.

The Amdm Loan Application Process

Securing an Amdm car loan typically involves a straightforward, yet thorough, application process designed to assess your financial eligibility. Based on my experience, a smooth application process is key to a stress-free car buying journey, and Amdm strives to make this as efficient as possible.

The first step usually involves completing an online or in-person application form, providing personal and financial details. This includes information about your employment, income, and residential history. Be prepared to furnish documentation to support these claims, such as pay stubs, bank statements, and proof of residence.

Next, Amdm will conduct a credit check to evaluate your creditworthiness. Your credit score plays a significant role in determining your eligibility and the interest rate you’ll be offered. A higher credit score generally translates to more favorable loan terms. Once your application and credit are reviewed, Amdm will provide you with a decision, often accompanied by specific loan offers tailored to your profile.

Key Factors Influencing Your Amdm Loan

Several critical factors will directly impact the terms and overall cost of your Amdm car loan. Being aware of these elements allows you to better prepare and potentially secure more advantageous financing. Understanding these influences is a cornerstone of smart financial planning.

1. Your Credit Score: This three-digit number is arguably the most influential factor. A strong credit history and high credit score (typically above 670) signal to lenders like Amdm that you are a reliable borrower, often resulting in lower interest rates and more flexible terms. Conversely, a lower score may lead to higher interest rates to offset the perceived risk.

2. Down Payment: The amount of money you pay upfront for the vehicle directly reduces the amount you need to borrow. A larger down payment can significantly lower your monthly payments, decrease the total interest paid over the life of the loan, and potentially help you qualify for a better interest rate from Amdm. It demonstrates a stronger financial commitment.

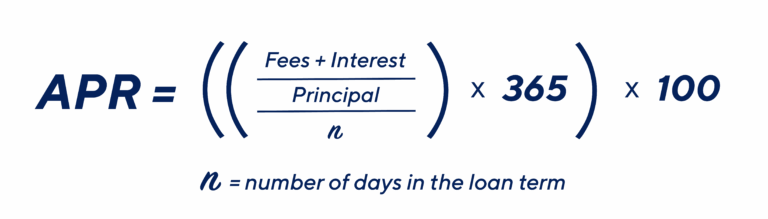

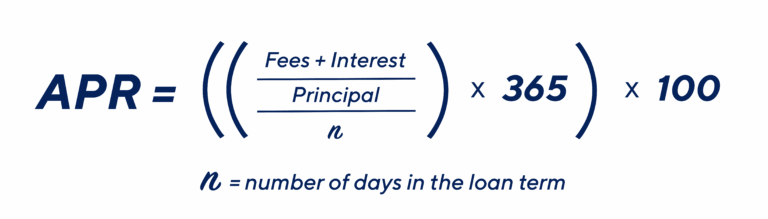

3. Interest Rate (APR): The interest rate, expressed as an Annual Percentage Rate (APR), is the cost of borrowing money. Amdm determines your interest rate based on your credit score, the loan term, the vehicle’s age and type, and prevailing market conditions. Even a seemingly small difference in APR can save you hundreds or thousands of dollars over the loan term.

4. Loan Term: This refers to the duration over which you agree to repay the loan, typically measured in months. Shorter loan terms mean higher monthly payments but less interest paid overall. Longer terms offer lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll pay more in interest over time. Carefully consider the balance between affordability and total cost.

Pros and Cons of Amdm Car Loans

Making an informed decision about an Amdm car loan requires a clear understanding of its benefits and drawbacks. Weighing these points against your personal circumstances is essential.

Pros of Amdm Car Loans:

- Ownership and Equity: The most significant advantage is that you own the car once the loan is paid off. You build equity with each payment, and the vehicle becomes a personal asset.

- Freedom and Flexibility: As the owner, you have complete control. There are no mileage restrictions, no penalties for customization, and you can sell or trade in the vehicle at any time.

- Long-Term Value: If you tend to keep your vehicles for many years, a loan can be more cost-effective in the long run compared to continually leasing new cars.

- Refinancing Opportunities: Should your credit score improve or interest rates drop, you might be able to refinance your Amdm loan for more favorable terms, reducing your monthly payments or total interest.

Cons of Amdm Car Loans:

- Higher Monthly Payments: Generally, loan payments are higher than lease payments for a comparable vehicle, as you’re financing the entire purchase price.

- Depreciation: Vehicles begin to depreciate the moment they are driven off the lot. As an owner, you bear the full brunt of this depreciation, which can be substantial in the early years.

- Maintenance Costs: Once the manufacturer’s warranty expires, you are fully responsible for all repair and maintenance costs, which can add up significantly as the car ages.

- Sales Tax and Fees: You typically pay sales tax on the full purchase price of the vehicle upfront or rolled into the loan, along with various registration and titling fees.

Navigating Amdm Car Leases: Flexibility and Fresh Rides

For those who prefer the idea of driving a new vehicle every few years without the long-term commitment of ownership, an Amdm Car Lease presents an attractive alternative. A lease is essentially a long-term rental agreement where you pay to use a vehicle for a specified period and mileage, rather than owning it.

With an Amdm car lease, you only pay for the depreciation of the vehicle during the time you drive it, plus interest (often called a "money factor") and fees. This model often results in lower monthly payments compared to a traditional car loan for a similar vehicle. It’s ideal for individuals who enjoy driving the latest models and appreciate the predictability of being under warranty.

What is an Amdm Car Lease?

An Amdm Car Lease allows you to drive a brand-new vehicle for a set period, typically 24 to 48 months, in exchange for regular monthly payments. At the end of the lease term, you have several options: return the vehicle, purchase it, or lease a new one. Amdm structures its lease agreements to offer flexibility and competitive terms, catering to different lifestyles.

Unlike a loan, you don’t build equity with a lease. Instead, you are paying for the privilege of using the vehicle. This means you avoid the burden of selling a used car and can consistently drive vehicles equipped with the latest technology and safety features.

The Amdm Lease Application Process

The application process for an Amdm car lease is quite similar to that of a loan, focusing on your financial stability and creditworthiness. Lenders want to ensure you can meet the monthly payment obligations for the duration of the lease term.

You’ll need to complete an application form, providing personal, employment, and income details. Amdm will perform a credit check, as your credit score is a crucial determinant of your eligibility and the money factor (interest rate equivalent) you’ll receive. A strong credit profile is key to securing the best lease terms and lower monthly payments. After approval, you’ll review and sign the lease agreement, which meticulously details all terms and conditions.

Key Elements of an Amdm Lease Agreement

Understanding the specific components of your Amdm lease agreement is vital to avoid surprises and ensure it aligns with your driving habits. Pro tips from us: always understand the fine print regarding mileage and wear and tear, as these can significantly impact your end-of-lease costs.

1. Lease Term: This is the duration of your lease agreement, commonly 24, 36, or 48 months. A shorter term means higher monthly payments but allows you to switch to a new car more frequently. Longer terms reduce monthly payments but extend your commitment.

2. Mileage Limit: Leases come with an annual mileage cap (e.g., 10,000, 12,000, or 15,000 miles per year). Exceeding this limit results in excess mileage fees, which can range from $0.15 to $0.25 or more per mile. It’s crucial to accurately estimate your driving habits to choose an appropriate mileage allowance.

3. Residual Value: This is Amdm’s projected wholesale value of the vehicle at the end of the lease term. Your monthly payments are calculated based on the difference between the capitalized cost (the car’s agreed-upon price) and the residual value, plus the money factor and taxes. A higher residual value means lower monthly payments.

4. Wear and Tear: Lease agreements define what constitutes "normal wear and tear." Anything beyond this, such as significant dents, scratches, damaged upholstery, or bald tires, can result in excess wear and tear charges at lease end. It’s wise to review these guidelines thoroughly and maintain the vehicle meticulously.

Pros and Cons of Amdm Car Leases

Just like loans, Amdm car leases come with their own set of advantages and disadvantages. Evaluating these points will help you determine if leasing is the right choice for your lifestyle and financial goals.

Pros of Amdm Car Leases:

- Lower Monthly Payments: Lease payments are typically significantly lower than loan payments for a comparable vehicle because you’re only paying for the depreciation during the lease term, not the entire purchase price.

- Drive New Cars More Often: Leasing allows you to upgrade to a brand-new vehicle with the latest features and safety technology every few years, avoiding the hassle of selling your old car.

- Warranty Coverage: Most lease terms align with the manufacturer’s bumper-to-bumper warranty, meaning you’re generally covered for unexpected repairs throughout your lease.

- Tax Advantages for Businesses: For some businesses, lease payments may be tax-deductible, offering a financial benefit not typically available with vehicle ownership.

Cons of Amdm Car Leases:

- No Ownership or Equity: You never own the vehicle and therefore don’t build any equity. The money you pay essentially goes towards renting the car.

- Mileage Restrictions: Exceeding the agreed-upon mileage limit can lead to costly penalties at the end of the lease, making it unsuitable for high-mileage drivers.

- Wear and Tear Charges: You are responsible for maintaining the vehicle in good condition. Excessive wear and tear beyond normal limits can result in additional fees upon return.

- Early Termination Penalties: Breaking a lease early can be very expensive, often requiring you to pay the remaining payments and additional fees, making it less flexible than a loan.

- No Customization: Modifying a leased vehicle is usually prohibited, as you must return it in its original condition.

Amdm Car Loans vs. Leases: Which One is Right for You?

The decision between an Amdm car loan and a lease is a highly personal one, dependent on your individual financial situation, driving habits, and long-term goals. There’s no single "better" option; rather, it’s about finding the best fit for you. Common mistakes to avoid are not evaluating your long-term needs and focusing solely on the monthly payment without considering the total cost and flexibility.

Let’s break down the key considerations to help you make an informed choice:

- Ownership Preference: Do you desire to own your vehicle outright and build equity, or are you comfortable with always having a new car without the burden of ownership? If ownership is a priority, an Amdm loan is your choice.

- Budget Considerations: Are lower monthly payments your primary concern, even if it means no ownership? Leases generally offer more affordable monthly costs. If you can afford higher payments for eventual ownership, a loan might be better.

- Driving Habits: How many miles do you typically drive in a year? If you drive significantly more than 12,000-15,000 miles annually, a lease’s mileage restrictions and potential penalties make a loan a more practical option.

- Vehicle Longevity: Do you prefer to drive a new car every few years, enjoying the latest technology and safety features, or do you tend to keep your vehicles for five years or more? Leasing suits the former, while a loan is better for the latter.

- Financial Goals: Are you looking to minimize upfront costs and monthly expenses, or are you focused on building assets and avoiding continuous car payments in the long run? Loans contribute to asset building, while leases offer consistent, predictable expenses.

For a deeper dive into vehicle choices that might influence your financing decision, you might find our detailed comparison of incredibly helpful in weighing your options.

Maximizing Your Amdm Financing Experience

Regardless of whether you choose an Amdm car loan or a lease, there are proactive steps you can take to optimize your financing experience. Preparation and strategic negotiation can lead to significant savings and a more satisfying outcome.

Preparing for Your Application

Before you even step foot into a dealership or submit an application, a little preparation can go a long way. This groundwork helps you approach the financing process from a position of strength.

- Check Your Credit Score: Obtain a copy of your credit report and score from all three major credit bureaus (Experian, Equifax, TransUnion). Correct any inaccuracies and understand where you stand, as this will heavily influence your rates.

- Determine Your Budget: Don’t just think about the monthly payment. Factor in insurance, fuel, maintenance, and registration fees. Know your absolute maximum affordable monthly payment and total vehicle price before you start shopping. For more budgeting tips, check out our guide on .

- Research Vehicles: Know what car you want and its fair market value. This prevents you from overpaying and gives you a benchmark for loan or lease calculations.

- Gather Documents: Have essential documents ready, such as proof of income (pay stubs, tax returns), proof of residence (utility bills), identification, and any trade-in vehicle information.

Negotiation Strategies

Negotiating for a car loan or lease goes beyond just the vehicle price. Smart negotiation can lead to better financing terms with Amdm.

- For Loans: Focus on the overall vehicle price first, then negotiate the interest rate. Don’t just focus on the monthly payment, as a longer loan term can make a higher total cost seem more affordable. Consider getting pre-approved for a loan from another lender to use as leverage.

- For Leases: Negotiate the "capitalized cost" (the agreed-upon price of the car) as if you were buying it. A lower cap cost means lower monthly payments. Also, understand and try to negotiate the "money factor" (interest rate) and ask about the residual value.

Understanding Amdm’s Special Offers and Promotions

Amdm, like many financial institutions, often runs special promotions, particularly on specific models or during certain times of the year. These can include lower interest rates on loans, reduced money factors on leases, or attractive cash-back incentives.

Always inquire about any current offers when you’re considering financing with Amdm. These promotions can significantly reduce your overall cost, but ensure you understand the eligibility requirements and terms associated with them. Sometimes, choosing a slightly different model or trim level might unlock substantial savings.

End-of-Term Options (Loans and Leases)

Knowing what happens at the end of your financing term is just as important as understanding the beginning.

- For Loans: Once your Amdm car loan is fully paid off, you receive the title to your vehicle, and it is entirely yours. You then have the freedom to keep it, sell it privately, or trade it in for your next vehicle.

- For Leases: At the end of an Amdm lease, you typically have three main options:

- Return the car: Hand over the keys, pay any excess mileage or wear and tear charges, and walk away.

- Buy out the lease: Purchase the vehicle for its residual value, often plus a purchase option fee. This is a good option if you love the car and the buyout price is favorable.

- Lease a new car: Turn in your old lease and sign a new lease agreement for a different vehicle, continuing the cycle of driving new cars.

Expert Advice and Final Thoughts

Navigating the landscape of Amdm Car Loans And Leases can feel daunting, but with the right information, it becomes an empowering process. Based on our years of experience in automotive financing, the most successful outcomes stem from thorough research, clear understanding of terms, and honest self-assessment of one’s financial situation.

Whether you prioritize ownership and long-term equity with an Amdm car loan, or the flexibility and constant newness of an Amdm car lease, the key is to make a decision that aligns with your personal and financial goals. Don’t rush the process, and always ask questions until you feel completely confident.

Amdm aims to provide accessible and transparent financing solutions. By leveraging the insights shared in this guide, you are well-equipped to engage with Amdm, explore their offerings, and secure the financing that puts you in the driver’s seat of your desired vehicle. Take the time to compare, calculate, and consider all angles. Your journey to a new vehicle experience with Amdm starts with an informed choice.

For more general financial guidance on car buying, consider exploring resources from trusted external sources like Investopedia, which provides comprehensive explanations of various financial concepts related to auto loans and leases.

Start your journey with Amdm today, armed with knowledge and ready to make a confident decision for your next vehicle.