Amdm Car Loans and Leases: Your Ultimate Guide to Navigating Auto Financing with Confidence

Amdm Car Loans and Leases: Your Ultimate Guide to Navigating Auto Financing with Confidence Carloan.Guidemechanic.com

The journey to owning or leasing a new vehicle is often filled with excitement, but it can quickly become overwhelming when faced with the complexities of auto financing. Understanding the nuances of car loans and leases is crucial, whether you’re dealing with a specific entity like "Amdm" or any other financial provider. Many consumers feel lost amidst jargon, varying rates, and tricky terms.

This comprehensive guide is designed to provide you with all the "Amdm Car Loans And Leases Answers" you need. We’ll demystify the process, empower you with knowledge, and equip you to make informed decisions that align with your financial goals. By the end of this article, you’ll feel confident navigating any auto financing scenario, ensuring you get the best deal possible.

Amdm Car Loans and Leases: Your Ultimate Guide to Navigating Auto Financing with Confidence

Understanding the Fundamentals: Car Loans vs. Car Leases

Before diving into the specifics of "Amdm Car Loans And Leases," it’s essential to grasp the fundamental differences between buying a car with a loan and leasing one. Each option comes with distinct advantages and disadvantages that cater to different lifestyles and financial situations. Choosing the right path is the first critical step in your auto financing journey.

The Auto Loan Explained: Owning Your Ride

When you take out an auto loan, you are essentially borrowing money to purchase the vehicle outright. You become the owner of the car once the transaction is complete, though the lender holds a lien on the title until the loan is fully repaid. This path offers a sense of permanence and complete control over your vehicle.

Pros of an Auto Loan:

- Ownership and Equity: You eventually own the car, building equity over time. This means you can sell it later and potentially recoup some of your initial investment.

- No Mileage Restrictions: Drive as much as you want without worrying about penalties for exceeding predetermined limits. This is perfect for those with long commutes or a love for road trips.

- Customization Freedom: You are free to modify your vehicle with aftermarket parts, tint windows, or make any personal upgrades without lease restrictions.

- Long-Term Value: Once the loan is paid off, you have a valuable asset that continues to serve your transportation needs without monthly payments.

Cons of an Auto Loan:

- Higher Monthly Payments: Generally, loan payments are higher than lease payments for a comparable vehicle, especially in the initial years. This is because you’re paying off the full purchase price.

- Depreciation: Cars lose value rapidly, especially in the first few years. You bear the full brunt of this depreciation, which can be significant.

- Maintenance Costs: Once the manufacturer’s warranty expires, all maintenance and repair costs become your responsibility. These can add up unexpectedly.

- Selling Hassle: When you want a new car, you’ll need to go through the process of selling or trading in your current vehicle, which can be time-consuming.

Key Terms to Understand for Loans:

- Principal: The actual amount of money you borrow to purchase the car.

- Interest: The cost of borrowing the principal, expressed as a percentage.

- APR (Annual Percentage Rate): This is the true annual cost of your loan, including interest and certain fees. A lower APR means lower overall borrowing costs.

- Loan Term: The duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). Longer terms often mean lower monthly payments but more interest paid overall.

The Auto Lease Demystified: Driving Without Ownership

Leasing a car is more akin to a long-term rental agreement. You pay to use the vehicle for a set period and mileage, but you never actually own it. At the end of the lease term, you return the car to the dealership, or you may have the option to purchase it. This option is popular for those who enjoy driving new cars frequently.

Pros of an Auto Lease:

- Lower Monthly Payments: Lease payments are typically significantly lower than loan payments for the same vehicle because you’re only paying for the depreciation of the car during your lease term, plus interest.

- New Car Every Few Years: Leasing allows you to drive a brand-new vehicle with the latest features and technology every two to four years.

- Warranty Coverage: Most lease terms align with the manufacturer’s warranty period, meaning you’re usually covered for major repairs throughout your lease.

- Tax Advantages for Businesses: For business owners, lease payments can sometimes be tax-deductible.

Cons of an Auto Lease:

- No Ownership or Equity: You don’t own the car and build no equity. Your payments don’t contribute to an asset you can later sell.

- Mileage Restrictions: Leases come with strict annual mileage limits (e.g., 10,000, 12,000, or 15,000 miles). Exceeding these limits results in hefty per-mile penalties.

- Wear and Tear Charges: At the end of the lease, you can be charged for excessive wear and tear beyond what’s considered "normal." This can include minor dents, scratches, or interior damage.

- Early Termination Fees: Getting out of a lease early can be extremely expensive, often costing thousands of dollars in penalties.

Key Terms to Understand for Leases:

- Residual Value: This is the estimated value of the car at the end of the lease term. It’s a crucial factor in determining your monthly payment; a higher residual value generally means lower payments.

- Money Factor: Similar to an interest rate for a loan, the money factor represents the financing charge on a lease. It’s usually a very small decimal (e.g., 0.00250), which you can multiply by 2400 to get an approximate APR.

- Capitalized Cost (Cap Cost): This is essentially the selling price of the car that the lease is based on. Negotiating a lower cap cost is one of the most effective ways to reduce your monthly lease payment.

- Cap Cost Reduction: This is similar to a down payment on a loan. It’s an upfront payment that reduces the capitalized cost, thereby lowering your monthly lease payments.

Preparing for Your Amdm Car Loan or Lease Application

Thorough preparation is the bedrock of a successful and financially sound auto financing experience. Jumping into a dealership without understanding your financial standing or what you truly need can lead to costly mistakes. Based on my experience, taking these preparatory steps will put you in a strong negotiating position for "Amdm Car Loans And Leases" or any other provider.

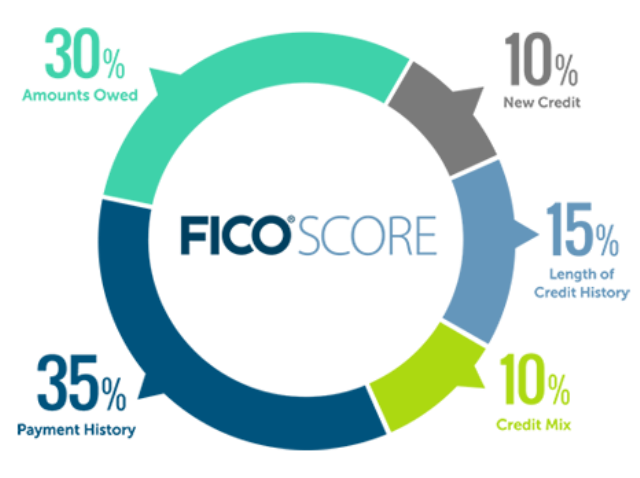

Know Your Credit Score: The Gateway to Better Rates

Your credit score is arguably the most influential factor in determining the interest rate (APR) you’ll be offered on a loan or the money factor on a lease. Lenders use it to assess your creditworthiness and the risk associated with lending you money. A higher score typically translates to lower financing costs.

Pro tips from us: Check your credit score and report well in advance of visiting a dealership. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, Transunion) once a year at AnnualCreditReport.com. Review it for any errors or inaccuracies that could be negatively impacting your score. Correcting these can significantly improve your standing. If your score isn’t ideal, consider taking steps to improve it, such as paying down existing debts or disputing incorrect entries, before applying for financing.

Budgeting Wisely: What Can You Truly Afford?

Many people make the mistake of focusing solely on the monthly payment when budgeting for a car. However, the true cost of vehicle ownership extends far beyond that single number. Ignoring these additional expenses can quickly lead to financial strain.

Common mistakes to avoid are: forgetting about insurance premiums, fuel costs, regular maintenance (oil changes, tire rotations), unexpected repairs, and registration fees. A good rule of thumb is the "20/4/10 rule": aim for a 20% down payment, finance the car for no more than four years, and keep your total monthly vehicle expenses (payment, insurance, fuel) under 10% of your gross monthly income. This holistic approach ensures your car doesn’t become a financial burden.

Down Payments and Trade-Ins: Reducing Your Overall Cost

Making a down payment or utilizing a trade-in can significantly impact the total cost of your car loan or lease. Both strategies reduce the amount you need to finance, leading to lower monthly payments and less interest paid over the life of the loan.

A substantial down payment, typically 10-20% of the vehicle’s price, immediately reduces your principal. This means you’ll pay interest on a smaller sum, saving you money in the long run. For leases, a cap cost reduction (the lease equivalent of a down payment) lowers your monthly payments. When considering a trade-in, always get multiple appraisals – one from the dealership, and others from independent sources like Kelley Blue Book or Carvana. This ensures you know the true market value of your vehicle and can negotiate effectively.

Navigating the Amdm Application and Approval Process

Once you’ve done your homework, it’s time to engage with the financing process. Whether you’re applying for "Amdm Car Loans And Leases" or another lender, understanding what to expect and what to scrutinize in the offers is critical. This stage is where your preparation truly pays off.

Required Documentation: What You’ll Need

Lenders require specific documents to verify your identity, income, and ability to repay the loan or lease. Having these readily available will streamline your application process.

Typically, you’ll need:

- A valid driver’s license.

- Proof of income (recent pay stubs, tax returns, or bank statements).

- Proof of residency (utility bill, lease agreement).

- Proof of auto insurance (you’ll need to have this in place before driving off the lot).

- Social Security Number for a credit check.

- Trade-in title or registration (if applicable).

Gathering these documents beforehand saves time and shows the dealer you are a serious and organized buyer.

Understanding Your Offer: APR, Loan Term, and Other Key Figures

When a lender presents you with a financing offer, it’s easy to get fixated on the monthly payment. However, it’s vital to look beyond this single figure and understand the underlying components of the offer. This is where many common mistakes are made.

Common mistakes to avoid are: agreeing to a long loan term (e.g., 72 or 84 months) just to achieve a lower monthly payment. While it reduces your immediate financial outlay, it significantly increases the total interest you pay over the life of the loan and prolongs the period you owe money on a depreciating asset. Always compare the APR (for loans) or money factor (for leases) offered by the dealership with any pre-approvals you may have secured from your bank or credit union. A lower APR or money factor can save you hundreds, if not thousands, over the term.

Lease Specifics: Money Factor, Residual Value, and Cap Cost

For leases, the "Amdm Car Loans And Leases" offer will hinge on three primary numbers: the capitalized cost, the money factor, and the residual value. These figures directly determine your monthly payment.

The capitalized cost is essentially the negotiated selling price of the car. It’s the most negotiable element of a lease. The money factor is the financing charge, similar to an interest rate. The residual value is the estimated value of the car at the end of the lease, determined by the lender. Your monthly payment is largely calculated by taking the difference between the capitalized cost and the residual value (the depreciation portion), adding the money factor, and then factoring in taxes and fees. A lower cap cost and money factor, combined with a higher residual value, will result in the lowest monthly lease payment.

Smart Negotiation Strategies for Amdm Car Deals

Negotiation is an art form, and when it comes to "Amdm Car Loans And Leases," it can save you a substantial amount of money. Approaching the negotiation process strategically, armed with knowledge, will give you a significant advantage. Remember, every element of the deal is potentially negotiable.

Separate the Price from the Financing

This is a golden rule in car buying. Dealerships often try to bundle the vehicle price and financing terms into one discussion, making it harder for you to track individual costs. Always negotiate the actual purchase price of the vehicle first, as if you were paying cash. Once you’ve agreed on a price, then shift your focus to the financing options.

Pro tips from us: Having a firm, pre-negotiated price for the car allows you to compare financing offers more clearly. It prevents the dealer from inflating the car’s price while offering a seemingly attractive APR, or vice-versa. Keep these two aspects distinct for maximum clarity and control.

Be Prepared to Walk Away

Your willingness to walk away from a deal is your most powerful negotiating tool. Salespeople are trained to identify committed buyers, and if they sense you’re desperate, they’re less likely to offer their best price. If the deal isn’t right, or you feel pressured, politely decline and leave.

Often, walking away prompts the dealership to present a better offer. It demonstrates that you are serious about getting a fair deal and won’t be swayed by high-pressure tactics. Remember, there are always other dealerships and other cars available.

Get Pre-Approved First

Before you even step foot into a dealership, secure a pre-approval for an auto loan from your bank, credit union, or an online lender. This step provides you with a significant advantage, giving you an "anchor" interest rate and loan amount.

When discussing "Amdm Car Loans And Leases" or any other dealer financing, you can use your pre-approval as leverage. If the dealer can’t beat or match your pre-approved rate, you already have a solid alternative. It turns the tables, making the dealership compete for your business, rather than you being at their mercy. Shop around for the best rates; don’t just take the first offer.

Post-Approval: Managing Your Amdm Car Loan or Lease

Securing your "Amdm Car Loans And Leases" agreement is a major step, but the journey doesn’t end there. Understanding your contract and knowing your options for managing it throughout its term is crucial for long-term financial health. Active management can save you money and headaches.

Understanding Your Loan/Lease Agreement

Once you’ve signed on the dotted line, you’re bound by the terms of the contract. It’s imperative to read every clause carefully, no matter how tedious it seems, before you sign. This includes reviewing all figures, terms, and conditions.

Common mistakes to avoid are: skipping the fine print. Pay close attention to clauses regarding prepayment penalties (for loans), early termination fees (for leases), mileage overage charges, and wear and tear policies. Knowing these details upfront prevents unwelcome surprises down the road. If anything is unclear, ask for clarification until you fully understand.

Early Payoff vs. Refinancing Your Loan

For car loans, you have options if your financial situation changes. An early payoff can be a smart move if you come into extra cash. Paying off your loan ahead of schedule saves you money on interest, as interest accrues daily on the outstanding balance. However, check if your loan agreement has any prepayment penalties, though these are less common with modern auto loans.

Refinancing your loan is another excellent option if interest rates have dropped, your credit score has improved significantly, or you want to change your loan term. Refinancing can lead to lower monthly payments, a reduced overall interest cost, or a shorter loan term, depending on your goals. Based on my experience, many people overlook refinancing and end up paying more than necessary.

End-of-Lease Options: What Happens Next?

As your lease approaches its end, you’ll have several choices regarding your "Amdm Car Loans And Leases" agreement. Understanding these options beforehand allows you to plan effectively.

Your options typically include:

- Buying the car: You can purchase the vehicle at the predetermined residual value stated in your lease agreement. This is a good option if you love the car and its buyout price is fair.

- Returning the car: You simply return the vehicle to the dealership. Be prepared for potential charges for excess mileage or damage beyond normal wear and tear.

- Extending the lease: Some lenders allow short-term extensions, which can be useful if you’re waiting for a new model or need more time to decide.

- Leasing a new vehicle: You can lease another car, often rolling over any equity (if the car’s market value is higher than its residual) or charges (like over-mileage) into the new lease.

Pro tips from us: Schedule a pre-inspection of your leased vehicle a few months before the return date. This allows you to address any potential wear and tear issues or mileage overages proactively, which can often be cheaper than paying dealership penalties.

Common Pitfalls and How to Avoid Them

Even with the best intentions, consumers can fall prey to common mistakes in auto financing. Being aware of these pitfalls is a crucial part of securing advantageous "Amdm Car Loans And Leases" and protecting your financial well-being. Knowledge is truly your best defense.

Not Reading the Fine Print

As mentioned earlier, the contract is the ultimate source of truth. Failure to meticulously read and understand every line can lead to unexpected costs, restrictive clauses, or unfavorable terms. Don’t assume anything; if it’s not in writing, it doesn’t exist.

Take your time, ask questions, and never sign a document you haven’t fully comprehended. Bring a trusted friend or family member to review it with you if you feel overwhelmed.

Overlooking Additional Fees and Charges

The sticker price or advertised monthly payment rarely tells the whole story. Dealerships may include various add-ons, fees, and charges that inflate the total cost of your "Amdm Car Loans And Leases" deal. These can include document fees, processing fees, extended warranties, GAP insurance (Guaranteed Asset Protection), and rustproofing.

While some fees are legitimate, others are negotiable or unnecessary. Always ask for an itemized list of all charges and question anything you don’t understand or believe is excessive. Only agree to add-ons that truly provide value to you.

Stretching Loan Terms Too Long

One of the most common mistakes is extending the loan term to achieve a lower monthly payment. While a 72 or 84-month loan might seem appealing initially, it has significant drawbacks. You’ll pay substantially more interest over the life of the loan.

Furthermore, you risk becoming "upside down" on your loan, meaning you owe more than the car is worth, especially as depreciation takes its toll. This makes it difficult to sell or trade in the car without incurring a loss. Based on my experience, keeping loan terms as short as comfortably possible (ideally 36-60 months) is usually the wisest financial decision.

Ignoring Your Credit Score

Your credit score is your financial superpower in the auto financing world. Ignoring it or not checking it before applying for "Amdm Car Loans And Leases" means you’re going into the process blind. A low score limits your options and results in higher interest rates.

Actively managing and improving your credit score is one of the most impactful things you can do to secure better financing terms. Pay bills on time, keep credit utilization low, and dispute any errors on your report.

Protecting Yourself: Amdm Car Loans And Leases Answers for Your Peace of Mind

Ultimately, the power to secure a fair and favorable "Amdm Car Loans And Leases" deal lies with you. Empowering yourself with information and knowing your rights are the best forms of protection against potential missteps or predatory practices.

The Importance of Independent Research

Never rely solely on the information provided by a single dealership or lender. Conduct your own independent research on vehicle pricing, market values (for trade-ins), interest rates, and lease terms. Websites like Edmunds, Kelley Blue Book, and Consumer Reports offer invaluable data.

Pro tips from us: Compare offers from multiple dealerships and lenders. This competitive shopping ensures you get the best deal available and gives you leverage in negotiations. The more informed you are, the less likely you are to be taken advantage of.

When to Seek Professional Advice

While this guide provides extensive information, there might be complex situations where professional advice is beneficial. If you have unique financial circumstances, a poor credit history, or are dealing with an unusual offer, consider consulting with a financial advisor or an independent auto broker.

Their expertise can help you navigate tricky situations, understand complex contracts, and ensure your best interests are protected. Sometimes, a small consultation fee can save you thousands in the long run.

Consumer Rights and Protections

As a consumer, you have rights that protect you during the car buying and financing process. The Federal Trade Commission (FTC) provides excellent resources and guidelines regarding auto sales and leasing. They emphasize transparency, fair advertising, and protecting consumers from deceptive practices.

Familiarize yourself with your rights and know who to contact if you suspect unfair or illegal practices. Organizations like the FTC and your state’s Attorney General’s office can provide assistance. External Link: Federal Trade Commission Car Buying Guide

Conclusion: Your Road to Confident Auto Financing

Navigating "Amdm Car Loans And Leases" or any auto financing can seem like a daunting task, but it doesn’t have to be. By understanding the core differences between loans and leases, preparing your finances, knowing what to look for in an offer, and employing smart negotiation tactics, you can approach the process with confidence and control.

Remember, knowledge is your most powerful tool. Take your time, ask questions, compare offers, and never feel pressured into a deal that doesn’t align with your financial well-being. With the comprehensive "Amdm Car Loans And Leases Answers" provided in this guide, you are now well-equipped to make intelligent decisions and drive away with a deal that truly suits you.

We hope this article has provided immense value and clarity. Feel free to share your experiences or questions in the comments below!