Amex Car Loan: Unpacking Your Auto Financing Options with American Express

Amex Car Loan: Unpacking Your Auto Financing Options with American Express Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is often filled with excitement, anticipation, and a fair share of financial considerations. Many consumers, particularly those who already enjoy the premium benefits and robust financial services of American Express, naturally wonder: "Can I get an Amex car loan?" It’s a question that frequently surfaces, given Amex’s strong presence in personal finance.

In this super comprehensive guide, we’re going to dive deep into the reality of Amex and auto financing. We’ll clarify common misconceptions, explore how your American Express membership can indirectly support your car buying goals, and crucially, guide you through the most effective pathways to secure a vehicle loan. Our goal is to equip you with the knowledge to make informed decisions, ensuring your car purchase is both financially sound and stress-free.

Amex Car Loan: Unpacking Your Auto Financing Options with American Express

The Direct Answer: Does American Express Offer Traditional Car Loans?

Let’s address the elephant in the room right away. For the vast majority of consumers and in most markets, American Express does not offer traditional, direct car loans in the same way a bank, credit union, or dealership might. This is a common misconception, and it’s important to set the record straight from the outset.

American Express primarily specializes in credit cards, charge cards, and a variety of travel, lifestyle, and business financial services. Their core business model revolves around these products, which cater to a broad spectrum of financial needs, but direct auto financing isn’t typically among them. When you search for "Amex car loan," you’re likely looking for a specific product that doesn’t exist within their standard offerings.

This doesn’t mean your Amex relationship is irrelevant to your car buying journey. Far from it! While they may not provide the direct loan, your status as an American Express cardholder and your financial discipline with their products can significantly enhance your ability to secure excellent financing elsewhere. We’ll explore these indirect benefits in detail.

How American Express Can Indirectly Support Your Car Purchase

Even without a direct "Amex car loan" product, your relationship with American Express can still be a powerful asset when you’re looking to finance a vehicle. It’s all about leveraging the benefits and tools available to you as a cardholder.

1. Leveraging Membership Rewards Points for Related Expenses

One of the most appealing aspects of many American Express cards is the Membership Rewards program. While you can’t typically pay for a car loan directly with points, you can certainly use them to offset other significant car-related costs.

Based on my experience, smart cardholders use their points strategically. You could redeem points for statement credits, effectively reducing your overall expenditures. Alternatively, points can be used for gift cards to gas stations, auto parts stores, or even for travel that might free up cash for your down payment. This indirect approach can significantly lighten the financial load associated with a new vehicle.

2. Accessing Personal Loans Through Amex (If Available)

While not a car loan, some American Express cardholders may be eligible for personal loans offered directly by Amex. These are typically unsecured loans, meaning they don’t require collateral like a car title.

If you qualify, a personal loan from Amex could potentially be used to fund a car purchase, especially for used vehicles or if you prefer an unsecured loan. However, it’s crucial to compare the interest rates and terms of a personal loan against traditional secured auto loans, which often have lower rates due to the collateral involved. Always weigh your options carefully before committing.

3. Building Strong Credit with Amex for Better Loan Rates

Perhaps one of the most significant, yet often overlooked, ways American Express helps with car financing is by enabling you to build and maintain an excellent credit score. Responsible use of your Amex card – paying your bills on time and keeping your credit utilization low – contributes positively to your credit profile.

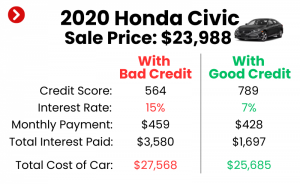

A robust credit score is the golden ticket to securing the best possible interest rates on any car loan, regardless of the lender. Lenders view borrowers with high scores as lower risk, translating into substantial savings over the life of your loan. This indirect benefit is absolutely invaluable.

4. Financial Tools & Resources for Better Planning

American Express offers various financial management tools and insights to its cardholders. These resources, while not directly providing a car loan, can help you better understand your spending, manage your budget, and track your financial health.

Having a clear picture of your finances is crucial before taking on a significant debt like a car loan. These tools can help you determine how much car you can truly afford, allowing you to approach other lenders with a solid financial plan.

Exploring Your Real Auto Financing Pathways

Since Amex typically doesn’t offer direct car loans, it’s essential to understand the primary avenues available for vehicle financing. Knowing your options empowers you to shop smart and secure the best terms.

1. Traditional Banks & Credit Unions

Traditional Banks: These are often the first stop for many car buyers. Banks like Chase, Bank of America, Wells Fargo, or your local community bank offer a range of auto loan products. They can provide competitive rates, especially if you have an existing relationship with them (e.g., checking or savings accounts).

Credit Unions: Often overlooked, credit unions can be excellent sources for auto loans. They are member-owned, non-profit financial institutions, which often translates to lower interest rates and more flexible terms compared to traditional banks. Joining a credit union is usually straightforward, often requiring a small deposit or meeting specific community criteria. Pro tips from us: Always check with a local credit union; their rates can sometimes be unbeatable.

2. Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders. This option provides convenience, as you can often complete the entire purchase and financing process in one location. Dealerships might also offer special promotional rates or incentives, particularly on new vehicles.

However, common mistakes to avoid are not comparing dealership offers with outside lenders. While convenient, the initial offer might not always be the best. It’s wise to arrive at the dealership with a pre-approved loan offer from another institution to use as a bargaining chip.

3. Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream (a division of Truist), or LendingClub provide quick pre-approvals and competitive rates.

The advantage of online lenders is the ease of comparing multiple offers from the comfort of your home. You can often get pre-approved in minutes, giving you a clear picture of what you can afford before you even step onto a dealership lot. This transparency is a huge benefit.

4. Secured vs. Unsecured Loans

When considering auto financing, it’s important to understand the difference between secured and unsecured loans.

- Secured Loans: The vast majority of traditional auto loans are secured. This means the car itself serves as collateral for the loan. If you default on payments, the lender has the right to repossess the vehicle. Because there’s collateral, secured loans typically come with lower interest rates.

- Unsecured Loans: Personal loans, like those potentially offered by Amex, are generally unsecured. There’s no collateral tied to the loan. This makes them riskier for the lender, and as a result, unsecured loans usually have higher interest rates. While you can use an unsecured personal loan for a car, it’s often more expensive than a dedicated auto loan.

Preparing for a Successful Car Loan Application

Securing the best auto loan isn’t just about finding the right lender; it’s also about preparing yourself as a borrower. Your financial readiness significantly impacts the terms you’ll receive.

1. Understanding Your Credit Score

Your credit score is arguably the most critical factor in securing a car loan. Lenders use it to assess your creditworthiness and determine your interest rate. A higher score (generally 700+) qualifies you for the most favorable rates.

As mentioned, responsible use of your American Express card, with timely payments and low credit utilization, is an excellent way to build and maintain a strong credit score. Before applying for any loan, obtain a free copy of your credit report from AnnualCreditReport.com and check for any errors.

2. Calculating Your Debt-to-Income Ratio (DTI)

Lenders also scrutinize your debt-to-income (DTI) ratio. This metric compares your total monthly debt payments to your gross monthly income. A low DTI indicates you have sufficient income to manage additional debt.

A DTI of 36% or less is generally considered favorable, though some lenders may approve higher ratios. Knowing your DTI beforehand allows you to understand how lenders will perceive your financial capacity to take on a car loan.

3. The Power of a Down Payment

Making a substantial down payment on a car offers several significant advantages. It reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan.

A larger down payment also builds immediate equity in the vehicle, protecting you from becoming "upside down" (owing more than the car is worth). While Amex points can’t directly fund a down payment, redeeming them for statement credits or other expenses can free up cash that you can then allocate to your down payment fund.

4. Budgeting Beyond the Monthly Payment

Many buyers focus solely on the monthly car payment. However, a responsible car purchase involves budgeting for more than just the loan. Consider the full cost of car ownership:

- Insurance: Premiums vary widely based on the vehicle, your driving record, and location.

- Fuel: Especially relevant with fluctuating gas prices.

- Maintenance & Repairs: All cars require regular servicing.

- Registration & Taxes: Annual costs that add up.

Pro tips from us: Get insurance quotes before you buy the car. A powerful sports car might have a low monthly payment but exorbitant insurance costs.

5. Pre-Approval: Your Secret Weapon

One of the smartest moves you can make is to get pre-approved for a car loan before you even visit a dealership. Pre-approval gives you a clear understanding of the maximum loan amount you qualify for and the interest rate you can expect.

Armed with a pre-approval letter, you walk into the dealership as a cash buyer. This shifts the negotiation focus from the monthly payment to the actual price of the car, giving you significant leverage. It also helps you resist pressure to take less favorable dealership financing.

The Smart Car Buying Process: From Research to Driveway

With your financing preparation complete, it’s time to navigate the actual car buying process. Approaching this systematically will save you time, money, and stress.

1. Thorough Vehicle Research

Before setting foot in a dealership, spend time researching vehicles that meet your needs, budget, and lifestyle. Consider factors like reliability, safety ratings, fuel efficiency, resale value, and ownership costs.

Don’t just look at aesthetics; delve into consumer reviews, expert analyses, and long-term reliability reports. Websites like Consumer Reports, Edmunds, and Kelley Blue Book are invaluable resources.

2. Test Drives & Inspections: Don’t Skip These Steps

Never buy a car without a thorough test drive. Pay attention to how the car handles, accelerates, brakes, and how comfortable it feels. Test it on different types of roads, including highways and city streets.

For used cars, a pre-purchase inspection by an independent, trusted mechanic is non-negotiable. This small investment can save you thousands of dollars in hidden repair costs down the line. Common mistakes to avoid are trusting the dealer’s inspection alone.

3. Negotiating the Price: Separate the Car from the Loan

This is where your pre-approval comes in handy. Focus your negotiations solely on the purchase price of the vehicle, not the monthly payment. Dealerships often try to blend these, making it harder to discern the true cost.

Be prepared to walk away if you don’t get a fair price. Patience is a virtue in car negotiation. Remember, you’re buying a car, not a loan.

4. Understanding the Loan Agreement

Before signing any documents, meticulously read and understand every clause in your loan agreement. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees.

- Loan Term: The length of the loan (e.g., 60, 72, 84 months). Longer terms mean lower monthly payments but more interest paid overall.

- Total Amount Paid: Understand the sum of all payments over the loan’s life.

- Prepayment Penalties: Ensure there are no penalties for paying off the loan early.

- Additional Fees: Scrutinize any extra charges for documentation, processing, or extended warranties.

Pro tips from us: Never feel rushed to sign. If you have questions, ask for clarification. Take the document home to review if needed.

Common Pitfalls and Pro Tips for Auto Financing

Navigating the auto loan landscape can be tricky. Based on my experience, here are some common mistakes and essential tips to ensure a smooth, cost-effective process.

Common Mistakes to Avoid:

- Focusing Only on the Monthly Payment: This is the most prevalent pitfall. A lower monthly payment often means a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

- Ignoring Your Credit Score: Not knowing your credit score before applying can lead to accepting higher rates than you deserve.

- Skipping Pre-Approval: Without a pre-approval, you lose significant negotiation power at the dealership.

- Buying Unnecessary Add-ons: Resist pressure to purchase expensive extended warranties, paint protection, or fabric treatments that may offer little value.

- Not Shopping Around for Loans: Accepting the first loan offer, especially from a dealership, can cost you hundreds or even thousands of dollars in interest.

- Extending the Loan Term Too Long: While an 84-month loan might offer a low monthly payment, you’ll pay substantially more interest, and the car’s value will likely depreciate faster than you pay off the loan.

Pro Tips for Smart Borrowing:

- Shop Around for Loans First: Get quotes from at least three different lenders (banks, credit unions, online lenders) before visiting a dealership.

- Know Your Budget (and Stick to It!): Determine what you can truly afford, including all ownership costs, before you start shopping for a car.

- Make a Down Payment: Aim for at least 10-20% to reduce your loan amount and total interest.

- Keep Loan Terms Shorter: Opt for 60 months or less if your budget allows to minimize interest costs.

- Read the Fine Print: Understand all terms and conditions of your loan agreement before signing.

- Consider Refinancing: If you secure a loan with a high interest rate, you can always explore refinancing options later, especially if your credit score improves. This is a powerful strategy to save money down the line.

Amex Benefits That Do Relate to Car Ownership (Post-Purchase)

While American Express doesn’t offer direct car loans, your membership can still provide valuable benefits once you’ve purchased your vehicle, offering peace of mind and potentially saving you money.

- Purchase Protection: Many Amex cards offer purchase protection, which can cover eligible items against accidental damage or theft for a certain period after purchase. While it won’t cover the entire car, it might apply to a down payment made with your card or specific car accessories bought with it.

- Extended Warranty: Some premium Amex cards provide an extended warranty benefit. When you use your eligible card to purchase a car part or an eligible item for your car, this benefit can add an extra year (or more, depending on the card) of warranty coverage beyond the manufacturer’s original warranty.

- Roadside Assistance: Select American Express cards offer roadside assistance programs. This can be a lifesaver if you experience a flat tire, need a tow, or run out of gas, providing an extra layer of security when you’re on the road.

- Membership Rewards for Related Expenses: Continue to earn Membership Rewards points on everyday purchases like gas, car insurance premiums (if allowed by your insurer), car washes, and maintenance at eligible merchants. These points can then be redeemed for statement credits or other rewards, effectively subsidizing your car ownership costs.

Conclusion: Empowering Your Car Buying Journey

The idea of an "Amex car loan" is a common one, but as we’ve explored, American Express typically doesn’t offer direct auto financing products. However, this doesn’t diminish the value of your American Express relationship when it comes to purchasing a vehicle.

By leveraging your Amex card to build a strong credit score, utilizing Membership Rewards for related expenses, and taking advantage of potential personal loan offerings, you can significantly strengthen your position as a car buyer. Remember, the key to successful auto financing lies in thorough preparation, understanding your options from various lenders, and approaching the car buying process with confidence and knowledge.

Don’t let the absence of a direct "Amex car loan" deter you. Instead, use your American Express membership as a foundation for financial strength, enabling you to secure the best possible financing from the myriad of lenders available. With the insights from this guide, you’re well-equipped to navigate the auto financing landscape and drive away with a deal that truly benefits you.

Ready to find your perfect car and secure smart financing? Start by checking your credit score, budgeting diligently, and comparing offers from multiple lenders today!