Anyone Approved Car Loan: Your Ultimate Guide to Getting Financed, No Matter Your Credit History

Anyone Approved Car Loan: Your Ultimate Guide to Getting Financed, No Matter Your Credit History Carloan.Guidemechanic.com

The dream of owning a car is a common aspiration for many. It represents freedom, independence, and convenience, opening up new possibilities for work, family, and leisure. However, for a significant portion of the population, the path to car ownership is often complicated by financing challenges. You might have faced credit difficulties in the past, have no credit history at all, or perhaps your financial situation doesn’t fit the traditional lender’s mold. This is where the concept of an "Anyone Approved Car Loan" enters the conversation, offering a glimmer of hope.

But what exactly does "Anyone Approved Car Loan" mean, and is it too good to be true? This comprehensive guide will demystify the process, explain the realities behind the promise, and provide you with actionable steps to secure the financing you need. Our ultimate goal is to empower you with the knowledge and strategies to drive away in your desired vehicle, regardless of your past financial hurdles. Let’s embark on this journey together to understand how you can achieve car loan approval.

Anyone Approved Car Loan: Your Ultimate Guide to Getting Financed, No Matter Your Credit History

Understanding "Anyone Approved Car Loan": The Reality Behind the Promise

When you hear the phrase "Anyone Approved Car Loan," it’s easy to imagine a magical solution where every application is automatically accepted. In reality, while no legitimate lender can guarantee approval without any conditions, this term typically refers to a broad spectrum of financing options specifically designed for individuals with diverse or challenging credit profiles. It signifies a high likelihood of approval, even if your credit history is less than perfect.

Based on my experience, many people misunderstand this phrase, thinking it means a free pass. Instead, it points to lenders, dealerships, and programs that specialize in what’s known as "subprime auto lending" or "bad credit car loans." These financial institutions are willing to take on higher risks by lending to borrowers who might not qualify for conventional loans. They assess applications using a more holistic approach, often looking beyond just your credit score to your current financial stability and ability to repay.

This means that while the terms might differ from a prime loan – perhaps a slightly higher interest rate or a larger down payment requirement – the doors to car ownership are still open. It’s about finding the right lender who understands your unique situation and is equipped to offer a viable solution.

Who Needs an "Anyone Approved" Loan? Identifying Your Situation

The need for an "Anyone Approved Car Loan" often arises from various financial circumstances that make traditional lending difficult. Understanding where you stand is the first crucial step in finding the right financing solution.

Bad Credit History

This is perhaps the most common reason people seek these specialized loans. A history of late payments, defaults on previous loans, collections, repossessions, or even bankruptcy can severely impact your credit score. Traditional lenders often see these as red flags, indicating a higher risk of default. However, many "Anyone Approved" lenders are specifically set up to evaluate applicants with these past challenges.

They understand that life happens and that a past mistake doesn’t necessarily define your current ability to manage finances. They focus on demonstrating a commitment to improving your financial situation and a stable income to support loan repayments.

No Credit History

It’s a classic paradox: you need credit to get credit. Young adults just starting their financial journey, new immigrants to a country, or individuals who have always used cash and avoided credit products often find themselves in this "credit invisible" category. Without a credit history, lenders have no data to assess your repayment behavior, making them hesitant to approve loans.

Pro tips from us: If you’re in this situation, these specialized lenders can be a lifeline. They might consider alternative data points, such as rental payment history, utility bill payments, or even proof of consistent employment, to establish your creditworthiness.

Low Income or Unconventional Employment

While a stable income is always a factor, some individuals with lower incomes or unconventional employment (e.g., self-employed, gig workers, seasonal employees) might struggle to meet the strict income thresholds or employment stability requirements of traditional lenders. "Anyone Approved" programs often have more flexible income verification processes and may consider a broader range of income sources.

The key here is demonstrating a reliable and consistent income stream, even if it’s not a standard W-2 salary. Lenders want assurance that you can consistently make your monthly car payments.

Unique Financial Situations

Life is full of unique circumstances. Perhaps you’ve recently gone through a divorce, experienced a medical emergency that impacted your finances, or are dealing with other temporary setbacks. These situations, while often beyond your control, can affect your credit or financial stability. Specialized lenders are often more willing to listen to your story and consider the broader context of your financial life, rather than just a number on a credit report.

Honestly assessing your financial standing and being transparent with potential lenders about your specific situation will significantly improve your chances of securing an "Anyone Approved Car Loan."

Key Factors Lenders Consider (Even for "Anyone Approved" Loans)

Even when seeking an "Anyone Approved Car Loan," lenders will still conduct a thorough evaluation of your financial situation. The difference lies in how they weigh these factors and their willingness to be more flexible. Common mistakes to avoid are thinking a lender won’t look at these crucial elements just because they offer "anyone approved" options.

Income and Employment Stability

Your ability to make consistent loan payments is paramount. Lenders want to see proof of stable income, typically through pay stubs, bank statements, or tax returns if you’re self-employed. They assess not just the amount, but also the consistency of your earnings. A steady job history, even if it’s relatively short, demonstrates reliability.

If your employment is new, some lenders might require additional verification or a slightly larger down payment. The longer you’ve been with your current employer, the better it looks to lenders.

Debt-to-Income Ratio (DTI)

Your DTI is a critical indicator of your financial health. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A high DTI indicates that a large portion of your income is already committed to other debts, leaving less disposable income for a new car payment.

Lenders offering "Anyone Approved" loans might have slightly higher acceptable DTI thresholds than prime lenders. However, a lower DTI will always make you a more attractive borrower, as it signals a greater capacity to handle additional debt responsibly.

Down Payment

Making a down payment is one of the most effective ways to improve your chances of approval, especially with a challenging credit history. A down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment to the purchase and your ability to save.

Pro tips from us: Even a modest down payment can make a significant difference. It demonstrates financial responsibility and reduces the loan-to-value (LTV) ratio, making the loan more secure for the lender.

Collateral (The Car Itself)

In an auto loan, the vehicle you’re purchasing serves as collateral. If you default on the loan, the lender can repossess the car to recover their losses. Therefore, the value and type of car you choose can influence your approval. Lenders prefer vehicles that hold their value well and are easily resold.

When you have less-than-perfect credit, opting for a moderately priced, reliable used car rather than a brand-new luxury vehicle can increase your approval odds. The car’s value directly impacts the lender’s risk exposure.

Co-signer

If you’re struggling to qualify on your own, a co-signer can be a valuable asset. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments. This provides an added layer of security for the lender, significantly improving your chances of approval and potentially securing better loan terms.

However, remember that a co-signer takes on a serious financial commitment. Ensure they understand the implications and that you are confident in your ability to make all payments on time.

The Path to Approval: Steps to Take Before Applying

Preparing thoroughly before you even submit an application can significantly enhance your prospects for an "Anyone Approved Car Loan." This proactive approach demonstrates responsibility and can help you secure better terms.

Check Your Credit Report and Score

Knowledge is power. Before approaching any lender, obtain copies of your credit report from all three major credit bureaus (Experian, Equifax, and TransUnion). You are entitled to a free report from each annually via AnnualCreditReport.com. Review them meticulously for any errors or inaccuracies. Disputing and correcting errors can potentially boost your credit score.

Understanding your credit score (even if it’s low) gives you a realistic picture of your standing and helps you anticipate the types of offers you might receive. An external link to a trusted source like the Consumer Financial Protection Bureau (CFPB) can provide more details on how to access and understand your credit reports.

Determine Your Budget

It’s crucial to understand what you can truly afford, not just for the car’s purchase price, but for the total cost of ownership. This includes:

- Monthly loan payment: What fits comfortably within your income and existing expenses?

- Car insurance: Rates can be higher for newer cars or for drivers with a less-than-perfect record.

- Fuel costs: Consider your daily commute and current gas prices.

- Maintenance and repairs: All cars require upkeep; older cars might need more.

- Registration and taxes: These are annual or one-time costs.

Pro tips from us: Create a realistic budget that accounts for all these factors. Overestimating your affordability can lead to financial strain down the road. For more details on managing your budget effectively, check out our comprehensive guide on .

Save for a Down Payment

As discussed, a down payment is incredibly beneficial. Start saving as much as you can. Even a small percentage (e.g., 5-10% of the car’s value) can make a difference. A larger down payment not only reduces your loan amount and monthly payments but also mitigates risk for the lender, making them more inclined to approve your application.

It also means you’ll pay less in interest over the life of the loan, saving you money in the long run.

Gather Necessary Documents

Having all your paperwork in order beforehand streamlines the application process and shows you are serious and organized. Typically, you’ll need:

- Proof of identity: Driver’s license or state ID.

- Proof of residency: Utility bill or lease agreement.

- Proof of income: Recent pay stubs (last 2-3 months), bank statements, or tax returns (if self-employed).

- Proof of insurance: You’ll need this before driving the car off the lot.

- References: Sometimes required, especially for "Buy Here, Pay Here" dealerships.

Pre-qualification vs. Pre-approval

Understanding the difference between these two can save you time and protect your credit score.

- Pre-qualification: This is a soft inquiry that doesn’t affect your credit score. It gives you an estimate of how much you might qualify for, based on basic financial information. It’s a good starting point for budgeting.

- Pre-approval: This involves a hard credit inquiry, which might slightly ding your credit score. However, it gives you a firm offer of a loan amount and interest rate, empowering you to shop for a car with confidence, knowing exactly what you can afford. It’s like having cash in hand at the dealership.

Where to Find "Anyone Approved" Car Loans

The landscape for car financing is vast, and for those seeking "Anyone Approved" options, several avenues specialize in catering to diverse credit situations. It’s about knowing where to look and understanding the pros and cons of each.

Dealership Financing (Buy Here, Pay Here)

"Buy Here, Pay Here" (BHPH) dealerships are perhaps the most direct route for individuals with very challenging credit. These dealerships act as both the seller and the lender, handling the entire financing process in-house. They often approve loans that traditional banks would reject, focusing more on your current income and ability to make payments.

Pros: High approval rates, convenient one-stop shop, quick approval.

Cons: Often higher interest rates, limited car selection (usually older, higher-mileage vehicles), and sometimes shorter loan terms. Based on my observations, many find success exploring these diverse avenues, but it’s crucial to compare terms.

Subprime Lenders

These are financial institutions that specialize in lending to borrowers with low credit scores. They are distinct from prime lenders (who cater to excellent credit) and near-prime lenders. Subprime lenders have risk models specifically designed to assess and mitigate the higher risk associated with bad credit applicants.

You can find subprime lenders through online marketplaces, direct applications, or often referred by traditional dealerships that don’t offer in-house financing but work with a network of specialized lenders.

Credit Unions

Credit unions are non-profit financial cooperatives that are member-owned. They often have more flexible lending criteria than large commercial banks and may be more willing to work with members who have a less-than-perfect credit history. Their rates can also be very competitive, as they pass profits back to their members.

If you are a member of a credit union, or eligible to join one, it’s definitely worth exploring their auto loan options. They tend to prioritize relationship banking and individual circumstances.

Online Loan Marketplaces and Brokers

The digital age has brought forth numerous online platforms that act as intermediaries, connecting borrowers with a network of lenders. You fill out one application, and the marketplace sends it to multiple lenders (including subprime ones) who might be willing to offer you a loan.

This approach saves time, allows for easy comparison of offers, and can broaden your access to lenders you might not have found otherwise. Be sure to use reputable platforms that protect your personal information.

Navigating the Application Process & Understanding Loan Terms

Once you’ve identified potential lenders, the next step is the application process itself and, crucially, understanding the terms of any loan offer you receive. This is where attention to detail and asking the right questions become vital.

The Application Form

Be prepared to provide detailed financial information. Honesty and accuracy are paramount. Any discrepancies or misrepresentations can lead to denial or, worse, legal issues down the line. Ensure all required documents are readily available to expedite the process.

The lender will use this information to assess your risk profile and determine the loan amount, interest rate, and terms they are willing to offer.

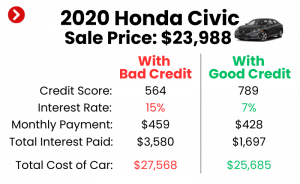

Understanding Interest Rates (APR)

The Annual Percentage Rate (APR) is the total cost of borrowing, expressed as a yearly percentage. It includes the interest rate plus any fees associated with the loan. For "Anyone Approved" loans, expect the APR to be higher than what someone with excellent credit would receive. This higher rate compensates the lender for the increased risk.

Pro tips from us: Always compare the APR, not just the advertised interest rate, as it gives you the most accurate picture of the loan’s total cost. A fixed APR means your payments remain consistent, while a variable APR can fluctuate.

Loan Term

The loan term is the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter terms: Result in higher monthly payments but less total interest paid over the life of the loan. This means you own the car sooner and save money.

- Longer terms: Result in lower monthly payments, making the loan more affordable on a month-to-month basis. However, you’ll pay significantly more in total interest and the car will depreciate faster than you pay off the loan, potentially leading to negative equity.

Choose a loan term that balances affordability with the total cost and your long-term financial goals.

Fees and Charges

Beyond interest, be aware of any additional fees. These can include:

- Origination fees: A charge for processing the loan.

- Documentation fees: For handling paperwork.

- Late payment penalties: Fees incurred if you miss a payment deadline.

- Prepayment penalties: Less common with auto loans, but check if there’s a fee for paying off your loan early.

Always ask for a complete breakdown of all fees and charges before signing any agreement.

Read the Fine Print

This cannot be stressed enough. Before you sign any loan agreement, read every single clause carefully. If you don’t understand something, ask for clarification. Don’t feel pressured to sign on the spot. Take your time, and if possible, have a trusted advisor review the terms with you. Common mistakes to avoid are rushing through the document or assuming certain terms.

Understanding your obligations and the lender’s rights is crucial to avoiding future misunderstandings or unexpected costs.

Rebuilding Your Credit with an "Anyone Approved" Loan

Securing an "Anyone Approved Car Loan" is not just about getting a vehicle; it’s also a powerful opportunity to rebuild or establish a positive credit history. This can pave the way for better financial opportunities in the future.

How Timely Payments Can Improve Your Score

Your payment history is the single most important factor in calculating your credit score. Making every car loan payment on time, every month, demonstrates financial responsibility to credit bureaus. As you consistently make on-time payments, lenders report this positive behavior, which then gets reflected in your credit report and subsequently boosts your credit score.

This is a gradual process, but it’s incredibly effective. Each on-time payment chips away at the negative impact of past credit issues or builds a new foundation if you had no credit.

Importance of Making Every Payment On Time

It’s not enough to make most payments on time. A single late payment can negate the positive impact of several on-time payments and can significantly lower your credit score. Set up reminders, consider automatic payments from your bank account, or mark your calendar to ensure you never miss a due date.

Consistency is key when it comes to credit building. Treat your car loan as a priority payment.

Refinancing Opportunities Down the Line

As your credit score improves through consistent, on-time payments, you may become eligible for better loan terms. After 6-12 months of responsible payments, consider exploring refinancing options. Refinancing involves taking out a new loan, usually with a lower interest rate, to pay off your existing car loan.

This can significantly reduce your monthly payments and the total amount of interest you’ll pay over the life of the loan, saving you hundreds or even thousands of dollars. Discover more strategies for improving your credit score and preparing for refinancing in our article: .

Common Mistakes to Avoid When Seeking Car Loan Approval

Navigating the world of "Anyone Approved Car Loans" requires vigilance. Avoiding common pitfalls can save you money, stress, and protect your credit score.

Applying to Too Many Lenders at Once

While it’s good to shop around, submitting multiple loan applications within a short period can trigger several "hard inquiries" on your credit report. Each hard inquiry can temporarily lower your credit score, making you appear riskier to lenders.

Pro tips from us: Focus on getting pre-qualified first (which uses a soft inquiry) with a few lenders. Once you have a clearer picture, narrow down your choices and proceed with full applications within a concentrated shopping period (typically 14-45 days), as credit bureaus often count multiple auto loan inquiries within this window as a single inquiry.

Ignoring the Total Cost of Ownership

As mentioned earlier, the price of the car and its monthly payment are only part of the equation. Many applicants focus solely on the monthly payment and overlook insurance, maintenance, fuel, and registration costs. Common mistakes we’ve seen countless times include people getting a loan they can afford but being unable to cover the ongoing expenses of the car, leading to financial distress.

Always budget for the complete picture to ensure your car ownership is sustainable.

Not Reading the Loan Agreement Carefully

This is a critical error. The loan agreement is a legally binding document. Failing to read and understand every clause, including terms about late payments, repossession, interest rate changes (if variable), and any hidden fees, can lead to unpleasant surprises.

If something seems unclear, don’t hesitate to ask for clarification. Reputable lenders will be transparent and willing to explain.

Settling for the First Offer

Even with challenging credit, it’s wise to compare offers from a few different lenders. The first offer you receive might not be the best one available to you. By comparing interest rates, fees, and loan terms, you can ensure you’re getting the most favorable deal possible for your situation.

Competition among lenders can work in your favor, so take the time to explore your options.

Being Dishonest on Your Application

Never, under any circumstances, provide false information on your loan application. This includes inflating your income, misrepresenting your employment, or concealing other debts. Lenders have sophisticated verification processes, and any dishonesty will likely be uncovered.

Providing false information can lead to immediate loan denial, legal consequences, or even criminal charges for fraud. Honesty and transparency build trust and lead to legitimate financing solutions.

Conclusion: Your Journey to Car Ownership Starts Now

The phrase "Anyone Approved Car Loan" isn’t a myth; it’s a testament to the diverse and evolving landscape of auto financing. While approval is never truly "guaranteed" without conditions, the reality is that options exist for nearly every credit situation, from pristine to challenging. By understanding your own financial standing, preparing diligently, knowing where to seek out specialized lenders, and meticulously reviewing loan terms, you significantly increase your chances of driving away in the vehicle you need.

Remember, this journey is also an opportunity for financial growth. A responsibly managed car loan can be a powerful tool for rebuilding or establishing a positive credit history, opening doors to better financial opportunities in the future. Don’t let past credit challenges or a lack of credit history deter you. With the right knowledge and a proactive approach, car ownership is within your reach. Start your journey today, empower yourself with information, and take the wheel towards your automotive independence.