APR vs. Interest Rate Car Loan: The Ultimate Guide to Saving Thousands on Your Next Vehicle

APR vs. Interest Rate Car Loan: The Ultimate Guide to Saving Thousands on Your Next Vehicle Carloan.Guidemechanic.com

The thrill of buying a new car is undeniable. The sleek design, the new car smell, the promise of open roads – it’s an exciting prospect. But for many, this excitement is quickly overshadowed by the daunting process of securing a car loan. You’re presented with numbers, percentages, and terms that can feel like a foreign language. Among the most crucial, yet often misunderstood, are the APR vs. Interest Rate Car Loan.

Many car buyers mistakenly focus solely on the interest rate, believing it represents the entire cost of borrowing. This common oversight can, unfortunately, lead to paying hundreds, even thousands, more than necessary over the life of the loan. As an expert blogger and professional SEO content writer with years of experience navigating the complexities of automotive financing, I’m here to tell you that understanding the difference between APR and the simple interest rate is not just important – it’s essential for your financial well-being.

APR vs. Interest Rate Car Loan: The Ultimate Guide to Saving Thousands on Your Next Vehicle

This comprehensive guide will demystify these critical terms, empowering you to make informed decisions and ultimately save a significant amount of money. We’ll dive deep into what each term means, why APR is the true indicator of your loan’s cost, and how you can leverage this knowledge to secure the best possible deal on your next vehicle. Let’s unlock the secrets to smarter car financing together.

The Basics: What is a Car Loan Interest Rate?

Let’s begin with the concept that most people are familiar with: the interest rate. At its core, the interest rate is the cost you pay to borrow money from a lender, expressed as a percentage of the principal loan amount. Think of it as the price tag for using someone else’s money.

When you take out a car loan, the lender charges you interest on the outstanding balance. This interest is typically calculated on a simple interest basis for auto loans. This means the interest is only charged on the principal amount that you still owe. As you make your monthly payments, a portion goes towards the principal, and a portion goes towards the interest. Over time, as your principal balance decreases, the amount of interest you pay each month also gradually reduces.

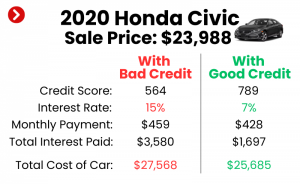

Based on my experience, many people mistakenly believe the interest rate is the only cost associated with borrowing. While it’s a significant component, it’s just one piece of a larger financial puzzle. Factors like your credit score, the loan term, and current market conditions all play a substantial role in determining the interest rate you’re offered. A higher credit score generally signals less risk to lenders, often resulting in a lower interest rate, which can translate to considerable savings.

Decoding the True Cost: What is APR (Annual Percentage Rate)?

Now, let’s introduce the term that truly reveals the total annual cost of borrowing: the Annual Percentage Rate (APR). While the interest rate reflects just the cost of borrowing the principal, the APR provides a more holistic view. It encompasses not only the interest rate but also most of the additional fees and charges associated with obtaining the loan.

The APR is essentially the "all-in" cost of your loan, expressed as a single, annualized percentage. It’s a standardized way for lenders to present the true cost of credit, allowing consumers to compare different loan offers more accurately. By law, lenders are required to disclose the APR, making it a crucial tool for transparent financial decision-making.

So, why is APR different from the simple interest rate? It’s because the APR bundles various costs that an interest rate alone does not. Understanding these components is key to fully grasping your loan’s actual expense.

Key Components That Make Up Your Car Loan APR:

When you see an APR, it’s a combination of several elements. Let’s break down what typically goes into this comprehensive rate:

-

The Interest Rate Itself: This is, of course, the primary component. It’s the base charge for borrowing the money, as we discussed earlier. Without the interest rate, there wouldn’t be a loan.

-

Origination Fees: These are charges for processing a new loan application. Lenders impose them to cover the administrative costs of setting up your loan. Origination fees can sometimes be a flat fee or a percentage of the total loan amount. They add directly to the overall cost of your loan, thus increasing the APR.

-

Documentation Fees (Doc Fees): Often seen at dealerships, these fees cover the cost of preparing and processing all the paperwork associated with your vehicle purchase and loan. While some states regulate these fees, in others, they can be a significant addition. When included in the financing, they inflate your APR.

-

Application Fees: Though less common for standard auto loans, some lenders might charge a small fee simply for submitting your loan application. If present, this fee will also contribute to the APR.

-

Underwriting Fees: These charges cover the lender’s cost of assessing your creditworthiness and determining the risk associated with lending to you. Similar to origination fees, they are part of the administrative burden passed on to the borrower.

-

Broker Fees: If you’re using a loan broker to find financing, they might charge a fee for their services. If this fee is rolled into the loan amount, it will also be factored into the APR.

Pro tips from us: Always ask for a full breakdown of all fees included in the APR. A reputable lender should be transparent about every charge. Some fees, like late payment fees or early payoff penalties, are generally not included in the APR because they are conditional charges. However, it’s vital to read the fine print for these as well, as they can significantly impact your total cost if you incur them.

APR vs. Interest Rate Car Loan: Why APR is Your True North

Now that we’ve defined both terms, let’s emphasize why understanding the difference between APR vs. Interest Rate Car Loan is paramount. The simple truth is: APR is the definitive measure of the total cost of your loan. While the interest rate is what most people initially focus on, it can be misleading when comparing loan offers.

Imagine you’re comparing two car loan offers:

- Loan A: Offers an interest rate of 5.0% but includes $500 in various fees.

- Loan B: Offers an interest rate of 5.5% but has no additional fees.

If you only looked at the interest rate, Loan A would seem like the better deal. However, when you factor in the fees, Loan A’s APR might actually be 6.2%, while Loan B’s APR remains 5.5%. In this scenario, Loan B, despite having a higher initial interest rate, is the cheaper option because its overall cost, as reflected by the APR, is lower. This is precisely why solely comparing interest rates is a common mistake that many car buyers make. It’s where many individuals get tripped up and end up paying more than necessary.

Lenders are legally obligated to disclose the APR for transparency. This legal requirement is designed to protect consumers by providing a standardized metric for comparing credit products. By focusing on the APR, you’re looking at the complete financial picture, not just a segment of it. This allows for a genuine "apples-to-apples" comparison between different lenders and different loan products, ensuring you can identify the most cost-effective option available to you.

Factors That Significantly Influence Your Car Loan APR

Your car loan APR isn’t a fixed number; it’s a dynamic figure influenced by a multitude of factors. Understanding these elements can help you take steps to secure a lower rate and ultimately save money.

-

Your Credit Score: Without a doubt, your credit score is the single biggest determinant of the APR you’ll be offered. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (generally 700+) indicates a lower risk, which translates to more favorable terms, including a lower interest rate and, consequently, a lower APR. Conversely, a lower score suggests higher risk, leading to a higher APR.

Pro tip: Before you even start car shopping, check your credit report and score. If there are errors, dispute them. If your score is low, consider taking steps to improve it. Even a small increase can make a big difference in your APR. For more detailed guidance on boosting your credit, you might find our article on "How to Improve Your Credit Score" incredibly helpful.

-

The Loan Term: The length of your loan repayment period also significantly impacts your APR. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower APRs. This is because the lender is taking on less risk over a shorter period. While shorter terms mean higher monthly payments, they usually result in less total interest paid and a lower overall cost. Longer terms (e.g., 60, 72, or even 84 months) often come with higher APRs because the lender’s risk exposure increases over an extended period.

-

Your Down Payment: Making a substantial down payment reduces the amount of money you need to borrow. This lowers the lender’s risk and can often lead to a lower APR. A larger down payment also means you’ll have more equity in the vehicle from the start, which is an attractive prospect for lenders. Aim for at least 10-20% of the car’s value if possible.

-

Lender Type: Different types of lenders offer varying APRs. Banks, credit unions, and dealership financing all have their own advantages and disadvantages. Credit unions, being member-owned, often offer some of the most competitive APRs. Banks provide a broad range of options, while dealership financing can be convenient but may sometimes include markups. Shopping around between these different lender types is crucial.

-

Vehicle Type and Age: The type of car you’re buying can also affect your APR. Newer, more reliable vehicles often qualify for lower rates because they hold their value better and are considered less risky collateral. Older or high-mileage cars might be seen as higher risk due to potential mechanical issues and depreciation, which can result in a higher APR.

-

Market Conditions: Broader economic factors and the Federal Reserve’s interest rate policies can influence the prevailing APRs across the entire lending market. When the Fed raises its benchmark rate, car loan APRs generally tend to rise, and vice versa. While you can’t control market conditions, being aware of them helps set realistic expectations.

Practical Application: How to Use APR to Compare Car Loan Offers

Understanding the theoretical difference between APR vs. Interest Rate Car Loan is one thing, but applying that knowledge effectively is where you truly save money. Here’s how to put APR to work when comparing car loan offers:

-

Get Pre-Approved from Multiple Lenders: This is arguably the most powerful step you can take. Before you even set foot in a dealership, apply for pre-approval from several different financial institutions – banks, credit unions, and online lenders. Each pre-approval will give you a concrete loan offer, including a specific APR. Having these offers in hand gives you a baseline for comparison and a strong negotiating tool.

-

Focus Solely on the APR for Comparison: When you receive these pre-approval offers, ignore the simple interest rate for a moment and go straight to the APR. This is the number that tells you the real, total cost of each loan. Compare the APRs side-by-side to determine which lender is offering you the best deal. Even a seemingly small difference in APR can translate into hundreds or thousands of dollars saved over the life of the loan.

-

Don’t Just Look at Monthly Payments: While your monthly budget is crucial, don’t let a low monthly payment seduce you without scrutinizing the underlying APR and loan term. A lower payment might simply mean a longer loan term, which often results in a higher total cost due to increased interest and a higher overall APR. Always evaluate the monthly payment in conjunction with the APR and the total amount you will pay back.

-

Leverage Your Pre-Approvals at the Dealership: Once you have your best pre-approved APR, you can use it to your advantage at the dealership. When the dealer offers financing, present them with your lowest pre-approved APR. They may be able to beat it, or at least match it, to earn your business. This strategy gives you significant negotiation power. Based on my experience helping countless individuals, having multiple pre-approved offers is your strongest negotiating tool, transforming you from a passive borrower into an empowered consumer.

-

Understand the Total Amount Paid: Beyond just the APR, always ask for the total amount you will pay back over the life of the loan. This number includes the principal plus all interest and fees. It’s the ultimate bottom line and provides the clearest picture of your financial commitment. For more strategies on navigating the dealership, our guide on "Negotiating Car Prices Like a Pro" offers invaluable insights.

Beyond APR: Other Crucial Considerations and Pro Tips

While APR is your north star for comparing loan costs, there are other vital aspects of car financing that informed buyers should consider. Overlooking these can still lead to unexpected expenses or financial strain.

-

Consider the Total Cost of Ownership: The loan payment is just one piece of the puzzle. Remember to factor in other ongoing costs associated with car ownership: insurance premiums, fuel, maintenance, repairs, and registration fees. A car with a low APR might still be expensive if its insurance is high or it requires premium fuel. Ensure the entire package fits comfortably within your budget, not just the monthly loan payment.

-

Read the Fine Print, Every Single Word: This cannot be stressed enough. Before signing any loan agreement, meticulously read every clause. Look for details regarding prepayment penalties (fees for paying off your loan early), late payment fees, default clauses, and any other hidden charges. Understanding these terms can prevent unpleasant surprises down the road.

-

Avoid Dealer Markups (When Possible): While dealers offer a convenient one-stop shop, they often mark up the interest rate or APR provided by their lending partners to generate additional profit. This is perfectly legal. Your pre-approval from an outside lender acts as a safeguard, ensuring you’re getting a competitive rate and not falling victim to an inflated APR. Pro tips from us: Always negotiate the car price before discussing financing. Separate these two critical parts of the car-buying process.

-

The Power of Refinancing: If you’ve already secured a car loan and your credit score has significantly improved, or if market rates have dropped, you might be a candidate for refinancing. Refinancing means taking out a new loan to pay off your old one, ideally at a lower APR. This can significantly reduce your monthly payments or the total amount of interest you’ll pay over time. It’s a smart move to periodically check if you qualify for a better rate.

-

Budgeting for More Than Just the Payment: Beyond the loan payment, create a comprehensive budget that includes all car-related expenses. Unexpected repairs can happen, and having an emergency fund specifically for your vehicle can prevent you from falling into debt or missing loan payments. A little financial foresight goes a long way.

-

Seek External Guidance: For additional unbiased information on auto loans and consumer rights, consider consulting trusted external sources. The Consumer Financial Protection Bureau (CFPB) offers excellent resources and guides to help you navigate auto financing responsibly. You can find valuable information on their website: https://www.consumerfinance.gov/consumer-tools/auto-loans/

Conclusion: Your Path to Smarter Car Financing

Navigating the world of car loans doesn’t have to be intimidating. By understanding the crucial distinction between APR vs. Interest Rate Car Loan, you empower yourself to make truly informed financial decisions. Remember, the interest rate is merely a component, while the Annual Percentage Rate (APR) is your comprehensive guide to the true cost of borrowing. It’s the metric that encapsulates the interest rate along with most of the associated fees, providing a transparent, apples-to-apples comparison between different loan offers.

We’ve explored how factors like your credit score, loan term, and down payment heavily influence your APR, and how proactive steps like getting pre-approved from multiple lenders can give you significant negotiation leverage. By focusing on the APR, diligently reading the fine print, and considering the total cost of ownership, you move beyond being a passive borrower to becoming an astute consumer.

Armed with this knowledge, you’re not just buying a car; you’re making a smart financial decision that can save you thousands of dollars over the life of your vehicle loan. Take control, do your research, and drive away with confidence, knowing you’ve secured the best possible deal. Your wallet will thank you.