Bad Credit, Big Dreams: Your Ultimate Guide to Getting a Car Loan Approved

Bad Credit, Big Dreams: Your Ultimate Guide to Getting a Car Loan Approved Carloan.Guidemechanic.com

Having bad credit can feel like a heavy burden, especially when you need a car loan to get around. Many people find themselves in this challenging situation, perhaps due to past financial missteps, unexpected life events, or simply a lack of credit history. The good news? Getting a car loan with bad credit is absolutely possible. It might require a bit more effort and strategic planning, but with the right approach, you can drive away in a reliable vehicle and even start rebuilding your financial standing.

This comprehensive guide is designed to be your roadmap. We’ll demystify the process, explore your options, and provide actionable advice to significantly increase your chances of approval, even when your credit score isn’t perfect. Based on my experience in the automotive and finance industries, I know the common hurdles and the best ways to overcome them. Let’s dive in!

Bad Credit, Big Dreams: Your Ultimate Guide to Getting a Car Loan Approved

Demystifying Bad Credit & Car Loans: What You Need to Know

Before we explore solutions, it’s crucial to understand the landscape. What exactly constitutes "bad credit" in the eyes of an auto lender, and why does it make securing a loan more challenging?

What is "Bad Credit" for an Auto Loan?

Generally, a FICO credit score below 600-620 is considered "subprime" or "bad credit" by most lenders. This range signifies a higher risk level for them. Scores can dip for various reasons, including missed payments, defaults, bankruptcies, or even having too many credit accounts open.

However, it’s not just about the number. Lenders also look at your overall credit report, checking for recent payment history, the types of credit you’ve had, and how long your accounts have been open. A low score combined with a history of missed car payments, for instance, will be viewed differently than a low score due to limited credit history.

Why is Bad Credit a Hurdle for Car Loans?

Lenders assess risk. When you have bad credit, you’re seen as a higher risk borrower. This means they are less confident you’ll make your payments on time or repay the loan in full. To offset this perceived risk, lenders often respond in a few ways:

- Higher Interest Rates: This is the most common consequence. A higher interest rate compensates the lender for the increased risk they’re taking on.

- Stricter Loan Terms: You might be offered shorter loan terms (meaning higher monthly payments) or require a larger down payment.

- Difficulty Getting Approved: Some traditional lenders might simply deny your application if your credit score falls below their minimum threshold.

Don’t let this discourage you. Understanding these factors is the first step toward strategically addressing them.

Your Pre-Application Power-Up: Preparation is Key

One of the biggest mistakes people make when they have bad credit and need a car loan is rushing into the application process unprepared. Preparation is your secret weapon. It shows lenders you are serious, responsible, and a calculated risk.

1. Check Your Credit Score and Report – Know Your Battlefield

This is non-negotiable. You can’t fix a problem if you don’t understand its scope. Obtain your credit reports from all three major bureaus: Equifax, Experian, and TransUnion. You’re entitled to a free report from each once a year via AnnualCreditReport.com.

Pro tips from us: Carefully review every detail on each report. Look for inaccuracies, outdated information, or accounts you don’t recognize. Disputing errors can sometimes boost your score surprisingly quickly. Even a small bump can make a difference in loan terms.

2. Create a Realistic Budget – How Much Can You Really Afford?

Before even looking at cars, sit down and map out your finances. List all your monthly income and expenses. This will reveal your disposable income—the amount you can realistically allocate to a car payment, insurance, fuel, and maintenance.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of ownership. Remember, a lower monthly payment often means a longer loan term and more interest paid overall. Be honest with yourself about what you can comfortably afford.

3. Save for a Substantial Down Payment – Your Financial Anchor

A down payment is incredibly powerful when you have bad credit. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. More importantly, it signals to lenders that you have some skin in the game.

Based on my experience, a down payment of 10-20% of the car’s value is ideal. If you can manage more, even better. This shows financial stability and commitment, significantly improving your chances of approval and potentially securing a better interest rate.

4. Know Your Trade-In Value – Another Form of Down Payment

If you have an existing vehicle, research its trade-in value using reputable sites like Kelley Blue Book (KBB.com) or Edmunds.com. A trade-in acts just like a cash down payment, reducing the amount you need to finance. Be realistic about its condition and be prepared for the dealer’s appraisal.

5. Gather All Necessary Documents – Be Ready to Prove It

Lenders will want to verify your identity, income, and residency. Having these documents ready streamlines the application process:

- Proof of Income: Pay stubs (last 2-3 months), W-2s, tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, mortgage statement.

- Identification: Driver’s license, social security card.

- Bank Statements: Recent statements to show financial activity.

Being organized demonstrates responsibility, which can subtly influence a lender’s perception of you.

Navigating the Lender Landscape: Who Will Lend to You?

Not all lenders are created equal, especially when you have bad credit. Understanding the different types of institutions and their approaches will help you target your efforts effectively.

1. Subprime Auto Lenders – Specialists in Bad Credit Car Loans

These lenders specialize in working with borrowers who have less-than-perfect credit. They are more willing to take on higher-risk applicants, but often at a cost. You can expect higher interest rates and potentially stricter terms compared to traditional banks.

Many dealerships have relationships with multiple subprime lenders, making them a common starting point. While the rates might be higher, getting approved and making timely payments can be a crucial step toward rebuilding your credit.

2. Buy Here Pay Here (BHPH) Dealerships – The Last Resort?

BHPH dealerships finance loans in-house, meaning they are both the seller and the lender. They often approve anyone, regardless of credit. The trade-off? Extremely high interest rates, limited car selection, and often less transparent loan terms.

Pro tips from us: While they offer guaranteed approval, proceed with extreme caution. Scrutinize every detail of the contract, understand all fees, and ensure you can genuinely afford the payments. This option should generally be considered only if all other avenues have been exhausted.

3. Credit Unions – Community-Focused and Often More Forgiving

Credit unions are member-owned financial cooperatives, not-for-profit organizations. They often have more flexible lending criteria and may be more willing to work with members who have bad credit, especially if you have an established relationship with them. Their interest rates tend to be more competitive than subprime lenders or BHPH lots.

It’s worth becoming a member of a local credit union and inquiring about their auto loan options. You might find a surprisingly favorable deal.

4. Online Auto Loan Platforms – Convenience and Speed

Numerous online lenders specialize in bad credit car loans. These platforms can offer quick pre-approvals and allow you to compare offers from multiple lenders without visiting dealerships. They often have a streamlined application process.

Look for reputable online platforms that clearly disclose terms and are transparent about their fees. They can be a great way to gauge your options and get an initial sense of what rates you might qualify for.

5. Traditional Banks – A Long Shot, But Worth Trying (Sometimes)

While traditional banks like Chase, Bank of America, or Wells Fargo typically prefer borrowers with good to excellent credit, it doesn’t hurt to inquire, especially if you have a long-standing relationship with them. They might offer slightly better rates if you meet their (often higher) criteria.

However, be prepared for a potential denial. If your credit is significantly low, they might not be the best starting point.

Boosting Your Chances: Strategies for Approval and Better Terms

Even with bad credit, you have leverage. Employing these strategies can significantly improve your odds of approval and potentially secure more favorable loan terms.

1. The Power of a Down Payment (Revisited)

We mentioned this in preparation, but it’s worth reiterating its impact. A larger down payment reduces the loan amount, lowers the lender’s risk, and can lead to a better interest rate. If you can save up 20% or more, you’ll be in a much stronger negotiating position. This is often the single most effective way to offset bad credit.

2. The Advantage of a Co-signer

A co-signer is someone with good credit who agrees to take on responsibility for the loan if you default. This significantly reduces the lender’s risk, as they have a second, financially strong party to pursue for payments.

Common mistakes to avoid are asking someone to co-sign without fully explaining the risks to them. This person’s credit will be affected if you miss payments, so choose someone you trust implicitly and who understands the commitment. This can be a great option if you have a willing and financially stable family member or friend.

3. Realistic Car Choice – Don’t Overextend Yourself

When your credit is shaky, aiming for a brand new, high-end vehicle is generally not wise. Focus on reliable, affordable used cars. Lenders are more comfortable financing a less expensive vehicle because their risk is lower.

A more affordable car also means lower monthly payments, making it easier for you to consistently pay on time and rebuild your credit. Think practical first, dream car later.

4. Demonstrating Stability – Proof of a Reliable Borrower

Lenders want to see stability. This includes:

- Stable Employment: Having a steady job for at least six months to a year (or longer) shows consistent income.

- Stable Residency: Living at the same address for an extended period indicates reliability.

- Consistent Income: Proof that you can make the payments, even if your credit history has blemishes.

Highlight these aspects during your application. They can often outweigh some of the negative credit history.

5. Understanding Loan Terms: Beyond the Monthly Payment

When you do get offers, don’t just look at the monthly payment. Dive into the details:

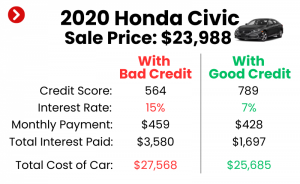

- Interest Rate (APR): This is the cost of borrowing money, expressed as a percentage. With bad credit, your APR will likely be higher. The Annual Percentage Rate (APR) includes the interest rate plus any additional fees, giving you a more accurate picture of the total cost.

- Loan Term: This is the length of the loan (e.g., 36, 48, 60, or 72 months). Longer terms mean lower monthly payments but more interest paid over the life of the loan.

- Total Cost of the Loan: Multiply your monthly payment by the number of months, then add any upfront fees or down payment. This reveals the true cost.

Pro tips from us: Always aim for the shortest loan term you can comfortably afford. This minimizes the total interest paid and helps you build equity in the car faster.

Common Pitfalls and Smart Solutions

Navigating the bad credit auto loan market can feel like walking through a minefield. Being aware of common traps can save you money and stress.

1. Avoiding Predatory Lenders and High-Pressure Sales

Some lenders and dealerships prey on desperate borrowers. If a deal sounds too good to be true, it probably is. Be wary of:

- Guaranteed Approval: While some places truly offer it (like BHPH), understand the associated costs.

- Ignoring Your Credit Score: A lender who doesn’t even ask about your credit might be hiding something.

- Unclear Terms: If they rush you through paperwork or refuse to explain clauses, walk away.

Take your time, read everything, and don’t be afraid to leave if you feel pressured.

2. The "Add-ons" Trap

Dealerships often try to sell you additional products like extended warranties, GAP insurance, paint protection, or VIN etching. While some might be beneficial (like GAP insurance if you’re upside down on your loan), they significantly increase the total amount you’re financing and your monthly payment.

Based on my experience, negotiate these items separately and decide if you truly need them. You can often purchase GAP insurance from your own auto insurer for less.

3. Don’t Just Focus on the Monthly Payment

As discussed, a low monthly payment can be deceiving if it’s stretched over 72 or 84 months with a high interest rate. This leads to paying significantly more in total interest.

Always ask for the total cost of the car, including all interest and fees. Use an online auto loan calculator to play with different scenarios (down payment, interest rate, loan term) to see their impact on the overall cost.

4. Multiple Hard Inquiries – Be Strategic

Every time a lender pulls your credit report for a loan application, it results in a "hard inquiry," which can temporarily ding your credit score. Applying to too many places at once can further lower your score.

Pro tips from us: To minimize impact, try to complete all your car loan applications within a 14-45 day window. Credit scoring models typically treat multiple inquiries for the same type of loan within this period as a single inquiry, recognizing you’re rate shopping.

The Application Journey: Step-by-Step

Once you’ve done your homework and found potential lenders, here’s what the application process generally looks like:

- Pre-qualification: Many lenders offer a "pre-qualification" process that involves a "soft pull" of your credit (which doesn’t affect your score). This gives you an idea of what you might qualify for without commitment.

- Formal Application: Once you’ve chosen a lender or two, you’ll complete a full application, which involves a "hard pull" of your credit.

- Provide Documentation: Submit all the documents you’ve gathered (proof of income, residency, ID, etc.).

- Review Offers: Carefully compare the interest rates, loan terms, and total costs from different lenders. Don’t be afraid to negotiate, even with bad credit.

- Finalize the Loan: Once you’ve chosen the best offer, sign the paperwork. Ensure you understand every clause before committing.

Beyond Approval: Rebuilding Your Credit

Getting a car loan with bad credit isn’t just about securing transportation; it’s a powerful opportunity to rebuild your credit.

Making Timely Payments – The Cornerstone of Credit Repair

This is paramount. Every on-time payment you make is reported to the credit bureaus, gradually improving your payment history—the most significant factor in your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

The Long-Term Benefits of Responsible Borrowing

As your credit score improves, you’ll open doors to better financial opportunities. Lower interest rates on future loans (mortgages, personal loans), better credit card offers, and even easier approval for rentals or utilities. A car loan, when managed responsibly, can be a springboard to a healthier financial future.

Conclusion: Your Road to a Brighter Financial Future

Needing a car loan with bad credit can feel daunting, but it is far from impossible. By understanding your credit situation, preparing meticulously, exploring all your lending options, and approaching the process strategically, you can secure the financing you need. Remember, this isn’t just about getting a car; it’s about taking control of your financial narrative and using this opportunity to rebuild your credit and secure a brighter financial future. Drive confidently, knowing you’ve made a smart, informed decision.

Ready to take the next step? Start by checking your credit report today, then begin budgeting for that crucial down payment. Your journey to a new car and improved credit begins now!

External Resource: For more information on understanding your credit reports and disputing errors, visit the Consumer Financial Protection Bureau at ConsumerFinance.gov.