Bank Loan For A Used Car: Your Ultimate Guide to Approval and Smart Financing

Bank Loan For A Used Car: Your Ultimate Guide to Approval and Smart Financing Carloan.Guidemechanic.com

The dream of owning a car is a common one, and for many, a pre-owned vehicle offers an intelligent, budget-friendly path to achieving it. Used cars provide incredible value, sidestepping the rapid depreciation of new vehicles while still offering reliable transportation. However, finding the perfect used car is only half the journey; the other crucial part is figuring out how to finance it.

This is where a bank loan for a used car comes into play. Securing the right financing can make all the difference, transforming a potential financial burden into an affordable, manageable monthly payment. Navigating the world of auto loans, especially for second-hand vehicles, can seem daunting, but with the right knowledge, it’s a straightforward process.

Bank Loan For A Used Car: Your Ultimate Guide to Approval and Smart Financing

In this comprehensive guide, we’ll demystify everything you need to know about getting a bank loan for a used car. From understanding eligibility to navigating the application process, comparing interest rates, and avoiding common pitfalls, we’ll equip you with the insights to secure the best possible financing and drive away in your chosen vehicle with confidence.

Why Opt for a Used Car (and How Financing Helps)

Choosing a used car is often a financially savvy decision. New cars lose a significant portion of their value the moment they’re driven off the lot, a phenomenon known as depreciation. Used cars have already undergone this initial depreciation, meaning you get more car for your money.

Beyond cost savings, the used car market offers an incredible variety of makes, models, and features that might be out of reach if bought new. A second-hand car loan from a bank makes these options accessible, breaking down a large upfront cost into manageable installments. It’s about smart spending and leveraging financial tools to your advantage.

Understanding Bank Loans for Used Cars: The Basics of Second-Hand Car Financing

A bank loan for a used car, also known as an auto loan for pre-owned vehicles, is essentially money borrowed from a financial institution to purchase a vehicle that has had a previous owner. Unlike personal loans, these are typically secured loans, meaning the car itself acts as collateral. This security often translates to lower interest rates compared to unsecured personal loans.

When you secure a used car loan, you agree to repay the principal amount (the money borrowed) plus interest over a predetermined period, known as the loan term. Your monthly payment will consist of a portion of the principal and the accrued interest. Understanding these basic components is the first step towards successful used car financing.

Eligibility Criteria: Securing Your Used Car Loan Approval

Before you even start browsing vehicles, it’s crucial to understand what lenders look for. Meeting the eligibility criteria significantly increases your chances of securing a used car loan approval with favorable terms.

1. Your Credit Score: The Cornerstone of Loan Approval

Your credit score is arguably the most important factor lenders consider. It’s a three-digit number that reflects your creditworthiness, essentially telling lenders how reliably you’ve managed debt in the past. A higher score indicates a lower risk.

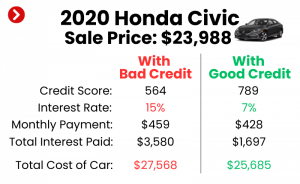

- What’s a good score? Generally, a FICO score of 670 and above is considered "good," with scores in the 700s and 800s being "very good" or "excellent." The better your score, the lower the interest rate you’re likely to qualify for, saving you potentially thousands over the life of the loan.

- Pro tips from us: Before applying, check your credit score and report. You can get free copies from annualcreditreport.com. If you find errors, dispute them immediately. If your score is low, take steps to improve it, such as paying down existing debts or making all payments on time. could provide more in-depth advice here.

- Common mistakes to avoid: Applying for a loan without knowing your credit score is a common oversight. This can lead to unexpected rejections or being offered rates that are far from competitive. It’s always better to be prepared.

2. Income Stability: Lenders Want Assurance

Lenders need to be confident you can make your monthly payments consistently. This means demonstrating a stable income source. They will typically ask for proof of employment, such as recent pay stubs, W-2 forms, or tax returns if you’re self-employed.

- Debt-to-Income Ratio (DTI): Beyond your gross income, lenders also scrutinize your debt-to-income ratio (DTI). This is the percentage of your gross monthly income that goes towards debt payments. A lower DTI (ideally below 40%) indicates you have more disposable income to cover new loan payments, making you a less risky borrower.

- Based on my experience: Lenders are looking for consistency. If your employment history is sporadic, or your income fluctuates wildly, it might raise red flags. Be ready to explain any gaps or inconsistencies in your employment history.

3. Age and Mileage of the Car: Lender Restrictions

Unlike new car loans, used car financing often comes with restrictions on the vehicle itself. Banks typically have limits on the maximum age and mileage a used car can have to be eligible for financing.

- For instance, some banks might only finance vehicles up to 7-10 years old, or with less than 100,000-120,000 miles. These limits are in place because older, higher-mileage vehicles are perceived as having a higher risk of mechanical failure, which could impact their value as collateral.

- Always check a lender’s specific vehicle requirements before falling in love with a car that might not qualify for a used car loan.

4. Your Age and Residency: Basic Requirements

As with any loan, you must be at least 18 years old (19 in some states) and a legal resident of the country where you’re applying. Lenders will require proof of identity and residency, such as a driver’s license and utility bills. These are standard verification steps to ensure you meet the basic legal requirements for borrowing.

The Used Car Loan Application Process: A Step-by-Step Guide to Pre-Owned Vehicle Financing

Securing an auto loan for pre-owned vehicles doesn’t have to be complicated. Following a structured approach can streamline the process and lead to a successful outcome.

Step 1: Get Your Finances in Order

Before you even look at cars or lenders, take an honest look at your financial situation.

- Check your credit score and report: As mentioned, this is paramount. Resolve any discrepancies and understand your standing.

- Gather income proof: Have recent pay stubs, W-2s, or tax returns ready.

- Determine your budget: This isn’t just about the car’s price. Factor in insurance, registration fees, potential maintenance, and fuel costs. Use a used car loan calculator to estimate monthly payments based on different loan amounts, interest rates, and terms. Being realistic here prevents future financial strain.

Step 2: Research Lenders and Compare Offers

Don’t just go with the first offer you receive. There’s a wide range of financial institutions that offer used car financing.

- Banks: Traditional banks are a common choice, often offering competitive rates for well-qualified borrowers.

- Credit Unions: These member-owned institutions are known for offering slightly lower interest rates and more flexible terms to their members.

- Online Lenders: Many online platforms specialize in auto loans and can provide quick approvals and competitive rates, often with a streamlined digital application process.

- Pro tips from us: Compare not just interest rates, but also loan terms, fees (origination fees, prepayment penalties), and customer service reviews. A slightly higher interest rate with excellent customer support or more flexible terms might be a better overall deal.

Step 3: Get Pre-Approved (Highly Recommended)

One of the smartest moves you can make is getting pre-approved for a loan before you start shopping for a car.

- Benefits: Pre-approval gives you a clear understanding of how much you can borrow and at what interest rate. This acts as a firm budget, saving you time by only looking at cars you can afford. It also gives you significant negotiating power with dealerships, as you walk in with your own financing already secured.

- How it works: Lenders will perform a "soft inquiry" on your credit report for pre-approval, which doesn’t affect your score. Once you decide to move forward, a "hard inquiry" will be made during the full application.

- Based on my experience: Walking into a dealership with a pre-approval letter from your bank is like having a secret weapon. Dealers know you’re a serious buyer and will often work harder to meet your price, or even beat your pre-approved rate.

Step 4: Find Your Car and Get It Inspected

With your financing pre-approved, you can now confidently shop for your used car.

- Importance of inspection: Never buy a used car without a thorough pre-purchase inspection (PPI) by an independent, trusted mechanic. Even if the seller or dealer offers their own inspection, getting an unbiased second opinion is crucial. This can uncover hidden issues that save you significant money and headaches down the line.

- Vehicle history reports: Invest in a CarFax or AutoCheck report. These provide vital information about the car’s past, including accident history, previous owners, service records, and title issues.

- Common mistakes to avoid: Getting emotionally attached to a car before confirming its condition or your ability to finance it. A proper inspection can prevent you from buying a lemon, which no loan can fix.

Step 5: Submit the Full Application

Once you’ve found the perfect car and it’s passed inspection, you’ll finalize your loan application with your chosen lender.

- You’ll provide all necessary documentation (ID, income proof, vehicle details) and the lender will perform a final credit check.

- The lender will then issue the funds, typically directly to the seller (dealership or private party), or sometimes to you in the form of a check to facilitate the purchase.

Key Factors Influencing Your Auto Loan For Pre-Owned Vehicles

Several critical elements will shape the terms and overall cost of your bank loan for a used car. Understanding these can help you secure a better deal.

1. Interest Rates: The Cost of Borrowing

The interest rate is the percentage charged by the lender for the money you borrow. It directly impacts your monthly payment and the total amount you’ll repay over the loan term.

- Factors affecting: Your credit score is the biggest determinant. Borrowers with excellent credit will qualify for the lowest rates. Other factors include the loan term (shorter terms often have slightly lower rates), the age and mileage of the car (older cars might have higher rates), and current market interest rates.

- How to get the best rate: Maintain a strong credit score, shop around with multiple lenders, and consider making a larger down payment. Even a difference of one percentage point can save you hundreds, if not thousands, over the life of the loan.

2. Loan Term: Balancing Payments and Total Cost

The loan term is the duration over which you agree to repay the loan, typically ranging from 24 to 72 months for used cars.

- Pros and cons of shorter terms: Shorter terms mean higher monthly payments but you pay less interest overall. You also own the car outright sooner.

- Pros and cons of longer terms: Longer terms result in lower monthly payments, which can make a car more affordable on a monthly basis. However, you’ll pay significantly more in total interest over the life of the loan. You also risk owing more on the car than it’s worth (being "upside down" or "underwater") as it continues to depreciate.

- Pro tips from us: Aim for the shortest term you can comfortably afford. While lower monthly payments from a longer term might be tempting, the increased total cost can be substantial.

3. Down Payment: A Smart Investment

A down payment is the initial amount of money you pay upfront towards the purchase of the car. It reduces the amount you need to borrow.

- Why it’s important: A substantial down payment reduces your loan amount, which in turn lowers your monthly payments and the total interest paid. It also signals to lenders that you’re a serious and responsible borrower, potentially leading to better interest rates.

- How much is enough? While there’s no strict rule, aiming for at least 10-20% of the car’s purchase price is a good target for a used car.

- Benefits of a larger down payment:

- Lower monthly payments.

- Less interest paid over time.

- Reduced risk of being upside down on your loan.

- Better loan terms and potentially easier approval.

4. Additional Fees: Don’t Overlook Them

Beyond interest, be aware of other fees that might be associated with your used car loan.

- Origination fees: A charge for processing the loan.

- Documentation fees: Fees charged by dealerships for preparing paperwork (often negotiable).

- Prepayment penalties: Some lenders charge a fee if you pay off your loan early. Always check for this, especially if you plan to make extra payments.

- Late payment fees: Charges incurred if you miss a payment deadline.

Documents Required for Your Used Car Loan Application

Being prepared with the right documents can speed up your used car loan application process. While requirements can vary slightly between lenders, here’s a general list:

- Personal Identification: Valid driver’s license or state-issued ID.

- Proof of Income: Recent pay stubs (1-3 months), W-2 forms (1-2 years), or tax returns (for self-employed individuals).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement with your current address.

- Social Security Number.

- Vehicle Information: Once you’ve chosen a car, you’ll need its VIN (Vehicle Identification Number), make, model, year, mileage, and purchase price.

- Proof of Insurance: You’ll need to show proof of comprehensive and collision insurance coverage before the loan can be finalized, as the car is the collateral.

Dealer Financing vs. Bank Loan for a Used Car: Making the Right Choice

When buying a used car, you typically have two main financing avenues: through the dealership or through an independent lender like a bank or credit union. Each has its pros and cons.

- Dealer Financing:

- Pros: Convenience (one-stop shop), sometimes offers special promotions or manufacturer incentives, especially for certified pre-owned vehicles. Can be helpful for those with less-than-perfect credit.

- Cons: Rates might not always be the most competitive (dealers often mark up interest rates), less transparency in some cases, limited lender options.

- Bank Loan (or Credit Union/Online Lender):

- Pros: Often offers more competitive interest rates, especially for borrowers with good credit. More transparency in terms. Getting pre-approved gives you stronger negotiating power at the dealership.

- Cons: Requires an extra step in the buying process, involves dealing with a separate entity.

- Based on my experience: While dealer financing can be convenient, it’s almost always a good idea to get a pre-approval from your bank or credit union first. This gives you a benchmark. If the dealer can beat your pre-approved rate, fantastic! But if not, you already have a solid alternative. Don’t be pressured into taking dealer financing without comparing.

Pro Tips for a Smooth Used Car Loan Approval Process

Getting approved for a bank loan for a used car can be a seamless experience if you follow these expert recommendations:

- Maintain a Strong Credit Score: This is your best asset. Pay bills on time, keep credit utilization low, and regularly monitor your credit report for errors.

- Save for a Substantial Down Payment: The more you put down, the less you borrow, leading to better terms and easier approval.

- Shop Around for Rates: Don’t settle for the first offer. Compare interest rates and terms from at least three different lenders (banks, credit unions, online lenders) within a short window (14-30 days) to minimize credit score impact.

- Get Pre-Approved: This step is invaluable. It sets your budget, streamlines the car-buying process, and gives you leverage in negotiations.

- Be Realistic About Your Budget: Factor in not just the monthly payment, but also insurance, fuel, maintenance, and potential repair costs. Don’t overextend yourself.

- Avoid New Credit Applications: In the months leading up to your loan application, avoid applying for new credit cards or other loans. This can temporarily lower your credit score and signal financial instability.

- Ensure the Used Car Meets Lender Requirements: Verify the car’s age, mileage, and condition align with your chosen lender’s policies before making an offer.

Common Mistakes to Avoid When Getting a Bank Loan For A Used Car

Even experienced buyers can make missteps. Here are some common mistakes to avoid:

- Not Checking Your Credit Score: Going in blind can lead to disappointment or higher rates. Always know your standing.

- Skipping Pre-Approval: This deprives you of negotiating power and can lead to emotional purchases outside your budget.

- Overlooking Hidden Fees: Always read the fine print. Ask about all fees associated with the loan and the car purchase.

- Focusing Only on Monthly Payments: While important, a low monthly payment often comes with a longer loan term and much higher total interest paid. Always consider the total cost of the loan.

- Not Inspecting the Car Thoroughly: A used car needs a professional inspection. A loan for a vehicle that constantly breaks down is a financial burden, not an asset. might be useful here.

- Borrowing More Than You Can Afford: It’s tempting to get a slightly more expensive car, but stick to your budget. Over-borrowing leads to financial stress and potential default.

After Approval: What Next?

Once your bank loan for a used car is approved and you’ve completed the purchase, your focus shifts to managing your new financial commitment.

- Finalizing the Purchase: Ensure all paperwork is correct, including the loan agreement, title transfer, and registration. Make sure you have adequate insurance coverage in place before driving off.

- Understanding Your Repayment Schedule: Know your exact monthly payment, due date, and how to make payments. Set up automatic payments if possible to avoid missing deadlines.

- Consider Refinancing: If interest rates drop significantly, or if your credit score improves substantially after taking out the loan, you might consider refinancing your used car loan. This could potentially lower your interest rate and monthly payments, saving you money over the remaining term. However, always calculate if the savings outweigh any refinancing fees.

Conclusion: Drive Away with Confidence

Securing a bank loan for a used car is a significant financial step, but it doesn’t have to be a complicated one. By understanding the eligibility criteria, meticulously navigating the application process, and being aware of the key factors that influence your loan, you can ensure a smooth and successful experience. Remember, knowledge is power, and being well-informed puts you in the driver’s seat of your financing journey.

With careful planning, thorough research, and smart decision-making, you can confidently secure the best auto loan for pre-owned vehicles, allowing you to enjoy your new-to-you car without financial stress. Start your research today, get pre-approved, and soon you’ll be hitting the road in your perfect used car, knowing you made a smart financial choice.