Bank of Stockton Car Loan: Your Ultimate Guide to Driving Away Happy

Bank of Stockton Car Loan: Your Ultimate Guide to Driving Away Happy Carloan.Guidemechanic.com

The open road beckons, the scent of a new car (or a "new-to-you" car) fills your imagination, and the promise of adventure awaits. For many, purchasing a vehicle is a significant milestone, a blend of excitement and practical necessity. However, transforming that dream into a reality often involves navigating the world of auto financing. This is where a trusted financial partner, like the Bank of Stockton, can make all the difference.

Securing the right car loan isn’t just about getting approved; it’s about finding terms that align with your financial goals and make your car ownership journey smooth and stress-free. In this comprehensive guide, we’ll dive deep into everything you need to know about obtaining a Bank of Stockton Car Loan, from understanding your options to mastering the application process and beyond. Our goal is to equip you with the knowledge to make an informed decision, ensuring you drive away not just with a new car, but with complete financial confidence.

Bank of Stockton Car Loan: Your Ultimate Guide to Driving Away Happy

Why Consider a Bank of Stockton Car Loan for Your Next Vehicle?

When it comes to financing a major purchase like a car, choosing the right lender is paramount. The Bank of Stockton, with its rich history and deep roots in the community, offers a distinctive approach to auto financing that sets it apart. They aren’t just a faceless institution; they are a local partner invested in your financial well-being.

One of the primary advantages of opting for a Bank of Stockton Car Loan is the personalized service you receive. Unlike larger national banks, where you might feel like just another number, Bank of Stockton prides itself on building relationships. This often translates into a more understanding and flexible approach to your unique financial situation.

Based on my experience, working with a local bank often means easier access to loan officers who can explain terms clearly and answer all your questions face-to-face. This level of personalized attention can be invaluable, especially if you’re new to car financing or have specific concerns you wish to address. Their commitment to the community often extends to offering competitive rates and terms designed to serve their local customers best.

Unpacking Your Bank of Stockton Car Loan Options

The journey to car ownership looks different for everyone, and Bank of Stockton understands this diversity. They offer a range of car loan options designed to cater to various needs, whether you’re eyeing a brand-new model or a reliable pre-owned vehicle. Understanding these options is the first step toward making an informed choice.

New Car Loans

For those who dream of driving a car straight off the dealership lot, a new car loan from Bank of Stockton can turn that aspiration into reality. These loans are typically for vehicles that have never been previously titled. New car loans often come with some of the most attractive interest rates and longer repayment terms, reflecting the lower risk associated with financing a brand-new asset.

The benefit of a new car loan extends beyond just the vehicle itself; it often means lower maintenance costs in the initial years and the peace of mind that comes with a manufacturer’s warranty. Bank of Stockton works to provide competitive financing solutions that make owning a new vehicle more accessible. They aim to structure payments that fit comfortably within your monthly budget.

Used Car Loans

Opting for a used car can be a smart financial decision, offering significant savings on depreciation and often lower insurance costs. Bank of Stockton provides robust used car loan options, recognizing the value and practicality of pre-owned vehicles. These loans are designed for cars that have had previous owners and typically come with specific criteria regarding the vehicle’s age and mileage.

While interest rates for used car loans might be slightly higher than for new cars, they remain highly competitive, especially for well-maintained, newer used models. It’s crucial to understand any age or mileage restrictions Bank of Stockton might have for used vehicle financing. Pro tips from us: always ensure the used car has a clean title and a thorough inspection before committing.

Refinancing Your Existing Car Loan

Perhaps you already have a car loan, but your financial situation has improved, or you’ve found better rates elsewhere. Refinancing your car loan with Bank of Stockton could be a strategic move to save money. Refinancing involves taking out a new loan to pay off your current one, ideally at a lower interest rate or with more favorable terms.

Common reasons to refinance include improving your credit score since you first obtained the loan, wanting to lower your monthly payments, or seeking to reduce the total interest paid over the life of the loan. Bank of Stockton’s refinancing options provide an opportunity to potentially free up cash flow or shorten your loan term. This could lead to significant long-term savings.

The Pre-Approval Advantage: Your Secret Weapon in Car Buying

Before you even set foot on a dealership lot, one of the most powerful steps you can take is to get pre-approved for a car loan. A Bank of Stockton Car Loan pre-approval is more than just a preliminary check; it’s a strategic tool that empowers you throughout the car buying process. It transforms you from a casual browser into a serious buyer with clear financial backing.

What exactly is pre-approval? It’s when a lender, like Bank of Stockton, reviews your financial information (credit score, income, debt) and tentatively agrees to lend you a specific amount of money, up to a certain limit, at an estimated interest rate. This commitment is valid for a set period, usually 30 to 60 days. It gives you a clear understanding of your borrowing power before you start shopping.

The benefits of pre-approval are numerous. Firstly, it provides you with a definitive budget. You’ll know exactly how much car you can afford, preventing you from falling in love with a vehicle outside your price range. Secondly, and perhaps most importantly, pre-approval gives you significant negotiation power at the dealership. You walk in knowing your financing is already secured, allowing you to focus purely on the car’s price.

Based on my experience, dealerships often try to roll financing into the negotiation, which can complicate things. With a pre-approval in hand, you can negotiate the vehicle’s price as if you were a cash buyer. This separation of car price from financing terms often leads to a better overall deal. Common mistakes to avoid are skipping pre-approval and letting the dealership handle all financing without prior knowledge of your options.

Navigating the Bank of Stockton Car Loan Application Process

Applying for a car loan might seem daunting, but with Bank of Stockton, the process is designed to be straightforward and transparent. Being prepared with the necessary documentation and understanding each step will ensure a smooth experience. Their goal is to make your path to car ownership as easy as possible.

Essential Documents You’ll Need

Gathering your documents beforehand is a pro tip that significantly speeds up the application process. Bank of Stockton, like any responsible lender, will require specific information to assess your creditworthiness and verify your identity. Having these ready will prevent delays.

Here’s a list of common documents you’ll likely need:

- Personal Identification: A valid government-issued ID, such as your driver’s license, and your Social Security number are essential for identity verification.

- Proof of Income: Lenders need to confirm you have the means to repay the loan. This typically includes recent pay stubs (usually the last two or three), W-2 forms, or tax returns if you are self-employed.

- Employment Verification: Your employment history helps lenders understand your stability. They might ask for employer contact information or a letter of employment.

- Residence Verification: Documents like utility bills, lease agreements, or mortgage statements confirm your address.

- Vehicle Information (if applicable): If you’ve already chosen a specific car, you’ll need details such as the make, model, year, VIN (Vehicle Identification Number), and purchase price.

Step-by-Step Application Guide

The Bank of Stockton offers convenient ways to apply for your car loan. You can usually choose between applying online, which provides flexibility, or visiting a local branch for a more personal touch.

- Initiate Your Application: Start by visiting the Bank of Stockton’s official website or stopping by your nearest branch. You’ll fill out a loan application form that requests personal, financial, and employment details.

- Submit Required Documents: Attach or provide all the necessary documents we outlined above. If applying online, you might be able to upload digital copies. In-branch applications allow for direct submission.

- Credit Check Authorization: You will authorize Bank of Stockton to perform a credit check. This allows them to access your credit report and score, which are crucial for determining your eligibility and interest rate.

- Review and Decision: Once your application and documents are submitted, a loan officer will review everything. They will assess your financial health, credit history, and the loan amount requested. This review process usually takes a few business days.

- Receive Your Offer: If approved, Bank of Stockton will present you with a loan offer detailing the approved amount, interest rate, repayment term, and monthly payment. You’ll have the opportunity to review these terms carefully.

- Finalize the Loan: Once you accept the terms, you’ll sign the necessary loan documents. The funds will then be disbursed, either directly to you (for private sales) or to the dealership.

Pro tips from us: Always be honest and accurate in your application. Any discrepancies can cause delays or even lead to rejection. Don’t hesitate to ask your loan officer questions if any part of the process is unclear.

Key Factors Influencing Your Bank of Stockton Car Loan Approval and Rates

Several critical factors come into play when Bank of Stockton evaluates your car loan application and determines your interest rate. Understanding these elements can help you prepare and potentially improve your chances of securing the best possible terms. It’s a holistic assessment of your financial health and the risk involved.

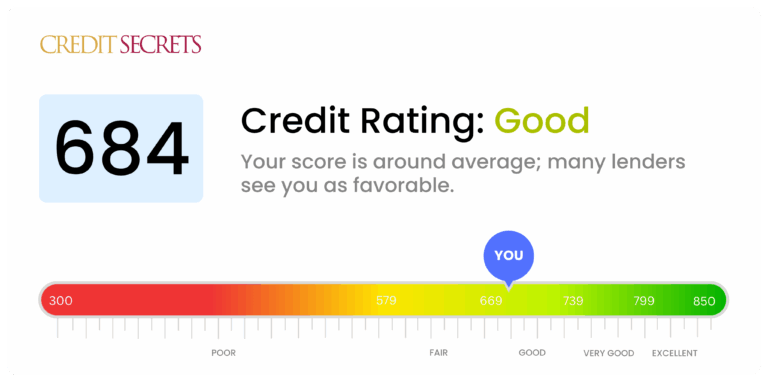

Your Credit Score

Your credit score is arguably the most influential factor. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score (generally 700+) indicates a lower risk to lenders, often resulting in lower interest rates and more favorable loan terms. Conversely, a lower score might lead to higher rates or require a co-signer.

Based on my experience, even a modest improvement in your credit score can translate into significant savings over the life of a car loan. It’s wise to check your credit report for inaccuracies before applying.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI ratio indicates you have more disposable income to cover your loan payments, making you a less risky borrower. Bank of Stockton will look for a healthy balance, ensuring you’re not overextending yourself financially.

Loan Term

The loan term refers to the length of time you have to repay the loan (e.g., 36, 48, 60, or 72 months). A shorter loan term generally means higher monthly payments but less interest paid over the life of the loan. A longer term results in lower monthly payments, which can be appealing for budgeting, but you’ll pay more in total interest. Choosing the right term involves balancing affordability with overall cost.

Down Payment

Making a significant down payment reduces the amount you need to borrow, which can lower your monthly payments and potentially lead to a better interest rate. A larger down payment also shows the lender your commitment to the purchase and reduces their risk. It’s a powerful way to demonstrate financial stability.

Vehicle Age and Type

The type and age of the vehicle you intend to purchase also play a role. Newer vehicles generally command lower interest rates due to their higher resale value and lower depreciation risk for the lender. Older or high-mileage vehicles might be considered higher risk, potentially leading to slightly higher rates. Bank of Stockton will assess the vehicle’s value to ensure it adequately secures the loan.

Optimizing Your Car Loan Experience with Bank of Stockton

Securing a Bank of Stockton Car Loan isn’t just about applying; it’s about strategizing to get the best possible deal. There are several proactive steps you can take to optimize your loan experience and ensure you drive away with terms that truly benefit you. This involves preparing your finances and understanding the nuances of the loan.

Improving Your Credit Score

If your credit score isn’t where you want it to be, take steps to improve it before applying. Pay your bills on time, reduce existing debt, and avoid opening new lines of credit. Even small improvements can make a difference in your interest rate. Accessing your credit report from reputable sources like Experian, Equifax, or TransUnion is a good starting point to identify areas for improvement.

Saving for a Down Payment

As discussed, a larger down payment is a significant advantage. Start saving early, even if it’s a small amount each month. Consider selling an old car or other unused assets to boost your down payment fund. This not only reduces your loan amount but also builds equity in your new vehicle faster.

Negotiating Vehicle Price Effectively

Armed with your Bank of Stockton pre-approval, you’re in a strong position to negotiate the car’s price. Focus on the total purchase price, not just the monthly payment. Be prepared to walk away if the deal isn’t right. Pro tips from us: research average selling prices for your desired vehicle beforehand using resources like Kelley Blue Book or Edmunds.

Understanding Loan Terms: APR vs. Interest Rate

It’s crucial to understand the difference between the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing money, expressed as a percentage. The APR includes the interest rate plus any additional fees charged by the lender, giving you the total cost of the loan over a year. Always compare APRs when looking at different loan offers, as it provides a more accurate picture of the true cost.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan or the APR. A low monthly payment might seem attractive but could indicate a longer loan term with significantly more interest paid over time. Always ask for the full breakdown of costs and terms.

Beyond the Loan: Additional Car Buying Tips

While securing your Bank of Stockton Car Loan is a major step, the car buying journey involves more than just financing. A holistic approach ensures you make a decision you’ll be happy with for years to come. Consider these additional tips to round out your purchasing strategy.

Researching Vehicles Thoroughly

Before you even think about loans, invest time in researching the cars that meet your needs and budget. Look at reliability ratings, safety features, fuel efficiency, and resale value. Test drive multiple vehicles to get a feel for what suits you best. This due diligence can prevent buyer’s remorse.

Budgeting for Insurance and Maintenance

Remember that the cost of car ownership extends beyond the monthly loan payment. Factor in insurance premiums, which can vary significantly based on the vehicle, your driving record, and your location. Also, set aside a budget for routine maintenance, unexpected repairs, and fuel. A comprehensive financial plan for your car ensures long-term affordability.

Considering Your Trade-In

If you plan to trade in your current vehicle, research its value beforehand. Online tools can give you a good estimate. This knowledge will help you negotiate fairly at the dealership. Be prepared to sell your car privately if the trade-in offer isn’t satisfactory, as this can sometimes yield a higher return.

For more in-depth guidance on managing your finances and making smart purchasing decisions, you might find our article on "Budgeting for Big Purchases" helpful. (Internal Link 1: Assuming a blog post exists on budgeting). Additionally, understanding the nuances of your credit can be a game-changer; explore our guide on "Mastering Your Credit Score for Better Loan Rates." (Internal Link 2: Assuming a blog post exists on credit scores). For general information on auto loan basics and consumer protection, the Consumer Financial Protection Bureau offers excellent resources: https://www.consumerfinance.gov/consumer-tools/auto-loans/ (External Link).

Conclusion: Your Road to Financial Confidence with a Bank of Stockton Car Loan

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, and having a reliable financial partner can make all the difference. A Bank of Stockton Car Loan offers more than just funds; it provides a pathway to car ownership built on local trust, personalized service, and competitive options. By understanding the various loan types, leveraging the power of pre-approval, and meticulously navigating the application process, you empower yourself to make the best financial decision.

Remember, a successful car purchase isn’t just about the vehicle itself, but also about the financial health it supports. With the insights provided in this guide, you are well-equipped to approach Bank of Stockton with confidence, secure favorable terms, and drive away happy. Take control of your car buying experience, and let Bank of Stockton help you get on the road to your next adventure.