Best Place For Car Loan With Good Credit: Your Ultimate Guide to Unlocking Top Rates

Best Place For Car Loan With Good Credit: Your Ultimate Guide to Unlocking Top Rates Carloan.Guidemechanic.com

Securing a car loan when you have good credit isn’t just about getting approved; it’s about unlocking the absolute best terms, the lowest interest rates, and the most favorable repayment options. Your excellent credit score is a powerful asset, signaling to lenders that you are a reliable borrower, and it should be leveraged to its fullest potential.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate the car loan landscape. We’ll explore the various avenues available, from traditional banks to innovative online lenders, and equip you with the insights to make an informed decision. Our goal is to help you find not just a car loan, but the best car loan for your specific needs, ensuring you save money and drive away with confidence.

Best Place For Car Loan With Good Credit: Your Ultimate Guide to Unlocking Top Rates

Understanding Your Good Credit Advantage

Before diving into where to find your car loan, let’s solidify what "good credit" truly means in the automotive lending world and why it’s such a significant advantage.

What Constitutes "Good Credit" for a Car Loan?

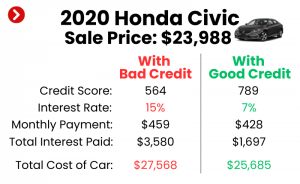

Generally, a good credit score for a car loan falls into the FICO score range of 670-739. However, many lenders consider scores above 700, and especially those above 740 (often termed "excellent credit"), to be ideal. The higher your score, the less risk you represent to a lender.

This low-risk profile translates directly into tangible benefits for you. Lenders compete more aggressively for borrowers with strong credit, which ultimately puts you in a powerful negotiating position. They are willing to offer more attractive terms to secure your business.

Why Good Credit is Your Superpower

Your strong credit history tells lenders that you pay your bills on time, manage debt responsibly, and are unlikely to default. This perception of reliability is invaluable. It directly influences the interest rate you’ll be offered, which is arguably the most critical factor in the overall cost of your car loan.

A lower interest rate means you pay less money over the life of the loan. Even a seemingly small difference of one or two percentage points can translate into hundreds, or even thousands, of dollars saved. Based on my experience in the financial sector, leveraging good credit is the single most effective way to minimize your car ownership costs beyond the vehicle’s purchase price.

Exploring Your Options: Where to Find Car Loans with Good Credit

When you possess good credit, the world of auto lending opens up significantly. You’re not limited to just one or two options; rather, you have a diverse range of lenders vying for your business. Understanding the unique advantages and potential drawbacks of each can help you pinpoint the best fit.

1. Traditional Banks

Large national banks and regional banks have long been a go-to source for car loans. They offer a sense of stability and often provide competitive rates for borrowers with good credit. Many consumers appreciate the familiarity and established infrastructure of these institutions.

Advantages of Banks for Good Credit Borrowers

Banks typically have robust online platforms for application and management, alongside physical branches for in-person assistance. For those with excellent credit, they are often able to secure some of the lowest advertised rates. They also offer a wide array of loan products, sometimes including flexible repayment schedules.

From a professional standpoint, if you already have a banking relationship – perhaps a checking account, savings account, or mortgage – with a particular institution, they might offer you even more favorable terms as a valued customer. This is often referred to as a "relationship discount."

Potential Considerations

While banks are strong contenders, their approval processes can sometimes be more stringent or take a bit longer than some online alternatives. Their focus is often on traditional lending models, which might mean less flexibility for unique financial situations. It’s always wise to compare their offers with other lender types to ensure you’re truly getting the best deal.

Pro tip from us: Don’t just assume your current bank will offer the best rate. Always shop around, even if you have a long-standing relationship. Loyalty is great, but saving money is better.

2. Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. This fundamental difference often translates into better rates and more personalized service compared to traditional banks. For individuals with good credit, credit unions are frequently among the best places to secure an auto loan.

Why Credit Unions Often Excel for Good Credit

Because they are member-owned, credit unions prioritize their members’ financial well-being. This often means they can offer lower interest rates on loans, including car loans, and fewer fees than for-profit banks. They tend to have a more community-focused approach and are often willing to work more closely with borrowers.

Based on my experience, credit unions are consistently at the top of the list when it comes to offering highly competitive APRs for well-qualified applicants. Their approval criteria can sometimes be slightly more flexible, or they might consider your overall financial picture more holistically.

Membership Requirements and Other Points

The main hurdle with credit unions is the membership requirement. You usually need to meet specific criteria, such as living in a certain geographic area, working for a particular employer, or being affiliated with a specific organization. However, many credit unions have broad eligibility, making it easier to join than you might think.

It’s worth investigating local and national credit unions to see if you qualify. The small effort required to join can often lead to significant savings on your car loan. Don’t overlook these hidden gems in the lending world.

3. Online Lenders and Lending Marketplaces

The rise of online lenders has revolutionized the auto loan market, offering unparalleled convenience and speed. For those with good credit, these platforms can be an excellent source for competitive rates and a streamlined application process.

The Convenience and Competition of Online Lending

Online lenders operate with lower overhead costs than brick-and-mortar institutions, allowing them to pass those savings on to consumers in the form of lower interest rates. They often boast quick pre-approval processes, sometimes delivering a decision within minutes. This speed is invaluable when you’re ready to purchase a vehicle.

Lending marketplaces, in particular, allow you to submit one application and receive multiple offers from various lenders. This fosters intense competition for your business, driving down rates for well-qualified borrowers. From my professional vantage point, online lenders have revolutionized how quickly and efficiently consumers can compare car loan offers.

Key Players and What to Look For

Companies like LightStream (a division of Truist Bank), Capital One Auto Finance (also offers direct online applications), and lending marketplaces such as LendingTree or RateGenius are popular choices. When considering online lenders, look for transparency in their rates, clear terms, and strong customer reviews.

While the process is often fully digital, ensure they have reliable customer support should you need assistance. Always confirm that any pre-approval offers are based on a "soft" credit inquiry, which won’t impact your credit score, before committing to a full application.

4. Dealership Financing

Many car dealerships offer financing options directly through their finance and insurance (F&I) departments. They act as intermediaries, connecting you with a network of lenders, including captive finance companies (e.g., Toyota Financial Services, Ford Credit) and other banks or credit unions.

The Appeal of One-Stop Shopping

The primary advantage of dealership financing is convenience. You can select your car and arrange financing all in one place, simplifying the purchasing process. Dealerships also often have access to special manufacturer incentives, such as 0% APR promotions or cash-back offers, particularly on new vehicles. For borrowers with excellent credit, these special offers can be incredibly attractive.

These captive finance companies often provide highly competitive rates, especially for new car purchases, aiming to move inventory. It’s a convenient solution that many buyers appreciate.

Common Mistakes to Avoid with Dealership Financing

While convenient, relying solely on dealership financing without exploring outside options is a common mistake. Dealers may mark up interest rates to profit from the financing, meaning you might not get the absolute best rate available to you. Their primary goal is to sell cars, and financing is a tool to achieve that.

Always arrive at the dealership with at least one pre-approved loan offer from an external lender (bank, credit union, or online lender). This gives you leverage to negotiate, ensuring the dealership’s offer is truly competitive. If their rate is higher, you have a strong alternative ready.

Key Factors to Consider When Choosing a Lender

With good credit, you have choices. To make the best choice, you need to look beyond just the advertised interest rate and consider the full scope of the loan offer.

Interest Rates (APR)

The Annual Percentage Rate (APR) is the single most important factor, as it represents the total cost of borrowing, including interest and certain fees. For good credit borrowers, aiming for the lowest APR possible is paramount. A difference of even 0.5% can save you hundreds over the loan term.

Always compare APRs, not just monthly payments. A lower monthly payment might simply mean a longer loan term, which ultimately costs you more in total interest.

Loan Terms

The loan term, or length of the loan (e.g., 36, 48, 60, 72 months), directly impacts your monthly payment and the total interest paid. Shorter terms mean higher monthly payments but significantly less total interest. Longer terms offer lower monthly payments but increase the overall cost of the loan.

With good credit, you might qualify for attractive rates on shorter terms, making them more affordable. Our insights suggest that balancing a comfortable monthly payment with the lowest total interest paid is key.

Fees and Charges

Some lenders charge origination fees, application fees, or prepayment penalties. While these are less common for auto loans, especially for good credit borrowers, it’s crucial to read the fine print. Ensure there are no hidden costs that could inflate the actual cost of your loan.

Transparent lenders will clearly outline all fees upfront. If a lender is vague about fees, consider it a red flag.

Customer Service and Reputation

A lender’s reputation for customer service can be incredibly valuable, especially if you encounter any issues during the loan term. Look for lenders with positive reviews regarding their responsiveness, clarity, and fairness. While online lenders offer convenience, ensure they have accessible customer support channels.

A well-regarded lender provides peace of mind, knowing you’re working with a reputable institution.

Pre-Approval Process and Inquiries

Understanding the difference between a soft and hard credit inquiry is vital. A soft inquiry (often used for pre-approvals) does not affect your credit score. A hard inquiry (used for final loan applications) can slightly lower your score for a short period.

When shopping for multiple loan offers within a short window (typically 14-45 days, depending on the credit scoring model), multiple hard inquiries for the same type of loan are usually treated as a single inquiry. This allows you to shop around without significant credit score damage.

The Unbeatable Power of Pre-Approval

Pre-approval is not just a suggestion; it’s a strategic move that fundamentally shifts the car buying experience in your favor. For those with good credit, it’s an absolute must-do.

What is Car Loan Pre-Approval?

Pre-approval means a lender has reviewed your credit, income, and other financial details and has conditionally agreed to lend you a specific amount of money at a certain interest rate. This offer is typically valid for a set period, like 30 to 60 days. It gives you a clear understanding of your borrowing power before you even step onto a dealership lot.

You’ll receive a pre-approval letter stating the loan amount, interest rate, and terms. This letter is your golden ticket to confident car shopping.

How Pre-Approval Works for Good Credit Borrowers

When you apply for pre-approval, the lender performs a soft credit inquiry, which doesn’t harm your credit score. They’ll ask for basic financial information, such as your income, employment history, and debt-to-income ratio. With good credit, you’re likely to receive an attractive offer quickly.

This process allows you to gather multiple pre-approval offers from different lenders (banks, credit unions, online lenders) without impacting your credit score. You can then compare these offers side-by-side to find the absolute best rate and terms.

The Undeniable Benefits of Being Pre-Approved

Having a pre-approval in hand provides several critical advantages:

- Know Your Budget: You walk into the dealership knowing exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiation Power: You become a cash buyer in the eyes of the dealership. This means you can negotiate the car’s price based on its value, not on your financing needs. The dealership knows you have financing secured elsewhere, forcing them to match or beat your external offer.

- Focus on the Car: With financing sorted, you can concentrate solely on finding the right vehicle and negotiating the best purchase price, separating the car deal from the loan deal.

- Avoid Dealership Pressure: You won’t feel pressured into accepting high-interest financing from the dealership because you already have a better option.

Based on my years in the financial space, pre-approval is your secret weapon. It empowers you and puts you in control of the car-buying process.

Securing Your Ideal Car Loan: A Step-by-Step Guide

Even with good credit, a structured approach is essential to ensure you land the best possible car loan. Follow these steps to maximize your chances of success.

Step 1: Check Your Credit Score and Report

Before doing anything else, obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check your credit score. Websites like AnnualCreditReport.com allow you to get a free report annually. Look for any inaccuracies or errors that could be negatively impacting your score.

For a deeper dive into improving your credit score, be sure to read our comprehensive guide on . Resolving any discrepancies can potentially boost your score and qualify you for even better rates.

Step 2: Determine Your Budget

Beyond the loan itself, consider your overall budget for car ownership. This includes not just the monthly loan payment, but also insurance, fuel, maintenance, and potential repair costs. Don’t overextend yourself, even if you qualify for a large loan amount.

A common rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn’t exceed 10-15% of your take-home pay.

Step 3: Gather Necessary Documents

Prepare the documents lenders will typically request. This often includes:

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bills, lease agreement)

- Government-issued ID (driver’s license)

- Social Security Number

- Information about the vehicle you intend to purchase (if known)

Having these ready streamlines the application process and prevents delays.

Step 4: Shop Around and Get Multiple Pre-Approvals

This is perhaps the most crucial step for good credit borrowers. Apply for pre-approval with 3-5 different lenders:

- Your current bank or credit union.

- Other reputable credit unions in your area or those you qualify for.

- Established online lenders.

- Large national banks.

Remember, these pre-approvals typically involve soft credit inquiries, allowing you to compare offers without harming your score.

Step 5: Compare Offers Carefully

Don’t just look at the monthly payment. Scrutinize each pre-approval offer, focusing on:

- APR: The true cost of the loan.

- Loan Term: How long you’ll be paying.

- Total Interest Paid: Calculate this over the life of the loan.

- Fees: Any hidden costs.

- Prepayment Penalties: Ensure you can pay off the loan early without penalty.

Use a loan calculator to see how different APRs and terms affect the total cost.

Step 6: Negotiate with the Dealership (and Leverage Your Offers)

Once you have your pre-approval letter(s), you can confidently negotiate the price of the car. If the dealership offers financing, compare it directly to your pre-approved rate. If their offer is better, great! If not, you have your outside financing ready to go.

This negotiation leverage is a direct benefit of your good credit and diligent shopping.

Step 7: Read the Fine Print Before Signing

Never rush the signing process. Carefully review all loan documents. Ensure the interest rate, term, and fees match what you were offered and agreed upon. Ask questions about anything you don’t understand.

Once you sign, you’re committed. Taking a few extra minutes to review can prevent costly mistakes down the road.

Avoiding Pitfalls: Common Car Loan Mistakes to Steer Clear Of

Even with good credit, certain missteps can cost you money or lead to frustration. Being aware of these common mistakes can help you maintain your financial advantage.

Not Shopping Around for the Best Rate

This is the number one mistake we see. Many consumers simply accept the first loan offer they receive, whether from their bank or the dealership. As discussed, your good credit gives you leverage, but only if you use it. Failing to compare multiple offers means you could be leaving significant savings on the table.

Always assume there’s a better deal out there until you’ve actively looked for it.

Focusing Only on the Monthly Payment

While a low monthly payment is appealing, it can be a deceptive metric. Lenders can easily lower your monthly payment by simply extending the loan term, which drastically increases the total interest you pay over time. A 72-month loan will almost always have a lower monthly payment than a 48-month loan, but the 72-month loan will cost you more overall.

Always consider the total cost of the loan, not just the monthly installment.

Ignoring the Total Cost of the Loan

The total cost includes the principal amount borrowed plus all interest and fees. This is the true measure of how much you’re paying for your car loan. A seemingly small difference in APR can add up to hundreds or even thousands of dollars over a multi-year loan.

Our recommendation is to always calculate the total cost for each offer you receive. This holistic view helps you make the most financially sound decision.

Letting the Dealer Run Multiple Hard Inquiries Without Your Consent

Some less scrupulous dealerships might run your credit with numerous lenders without your explicit permission, resulting in multiple hard inquiries that could negatively impact your credit score. You have the right to know which lenders they are submitting your application to.

Always be clear that you want to limit inquiries, especially if you already have pre-approval. This is another reason why having your own financing ready is so powerful.

Skipping the Pre-Approval Step Entirely

As highlighted, pre-approval is your best friend. Going to a dealership without it is like going to a battle without armor. You lose negotiating power, you’re more susceptible to high-pressure sales tactics, and you’re less likely to secure the absolute best rate your good credit deserves.

Make pre-approval a non-negotiable part of your car buying process.

Maximizing Your Good Credit Beyond the Loan

Your excellent credit can influence more than just your loan rate. It can also open doors to other financial advantages when buying a car.

Down Payment Strategies

While good credit can get you a loan with zero down payment, making a significant down payment (e.g., 10-20% of the car’s value) is almost always a wise financial move. It reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid.

A larger down payment also reduces the risk of being "upside down" on your loan, where you owe more than the car is worth.

Leveraging Your Trade-In Value

If you have a trade-in, your good credit helps ensure you’re in a strong position to negotiate its value. Knowing you have solid financing options prevents a dealership from lowballing your trade-in in an attempt to make up for a low car price. Research your car’s trade-in value beforehand using reputable sources like Kelley Blue Book or Edmunds.

If you’re curious about the difference between new and used car loans, our article offers valuable insights.

Refinancing Options Later

Even with good credit, market rates can change, or your credit score might improve even further over time. Your good credit means you always have the option to refinance your car loan later if you find a significantly better rate. This flexibility ensures you’re never stuck with an unfavorable loan.

Keep an eye on interest rates, and if they drop, or your score jumps, exploring refinancing could save you even more.

Conclusion: Drive Away with Confidence and Savings

Having good credit is an immense asset when it comes to securing a car loan. It grants you access to the most competitive interest rates, flexible terms, and a wider array of lenders eager for your business. By understanding your options, leveraging the power of pre-approval, and diligently shopping around, you can transform the often-stressful car buying process into an empowering and financially savvy experience.

Don’t let your good credit go to waste. Take the time to research, compare offers, and negotiate wisely. Doing so will not only save you hundreds or even thousands of dollars over the life of your car loan but will also reinforce your strong financial standing. Drive away knowing you secured the best possible deal, all thanks to your excellent credit and smart decision-making.

Understanding your credit score is fundamental; a reliable source like can provide detailed insights into how scores are calculated and what they mean for your borrowing power. Start your journey today, and make your good credit work for you!