Beyond RoadLoans: Discovering the Best Car Loan Alternatives for Your Next Vehicle Purchase

Beyond RoadLoans: Discovering the Best Car Loan Alternatives for Your Next Vehicle Purchase Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex maze. Many people start their journey by exploring well-known online lenders like RoadLoans, appreciative of their streamlined pre-approval process and broad appeal to various credit profiles. RoadLoans has certainly carved a niche by simplifying what can often be an intimidating experience.

However, the world of auto financing is vast, offering a multitude of options that might better suit your unique financial situation and vehicle needs. Understanding these alternatives is crucial for making an informed decision, potentially saving you thousands of dollars over the life of your loan. This comprehensive guide will take you deep into the landscape of car loans like RoadLoans, exploring their strengths, weaknesses, and how to find the perfect fit for you.

Beyond RoadLoans: Discovering the Best Car Loan Alternatives for Your Next Vehicle Purchase

What Makes RoadLoans a Popular Choice?

Before we dive into alternatives, it’s helpful to understand why RoadLoans became a go-to for many car buyers. Their primary appeal lies in their online-centric approach. You can apply for pre-approval from the comfort of your home, often receiving a decision in minutes.

This convenience extends to their wide network of dealerships, allowing you to shop with a pre-approved offer in hand. RoadLoans is also known for considering applicants across a spectrum of credit scores, making them accessible to a broader audience than some traditional lenders. This blend of ease, speed, and inclusivity has made them a benchmark for online auto financing.

Key Factors to Consider When Choosing a Car Loan Lender

When you’re comparing car loans, it’s not just about finding the lowest monthly payment. A truly smart decision involves looking at several critical factors that impact your overall cost and experience. Based on my experience in the auto finance industry, overlooking any of these can lead to unexpected expenses or a less-than-ideal borrowing situation.

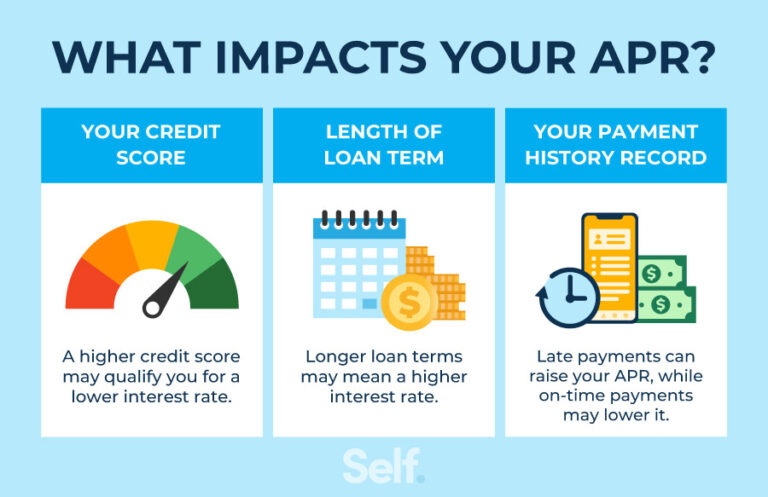

Understanding Interest Rates (APR)

The Annual Percentage Rate (APR) is arguably the most important number you’ll encounter. It represents the true cost of borrowing, encompassing not just the interest rate but also any lender fees rolled into the loan. A lower APR directly translates to less money paid over the loan’s term.

Always compare APRs, not just advertised interest rates. Even a difference of one or two percentage points can significantly impact your total repayment, especially on a larger loan amount. Your credit score, the loan term, and the vehicle’s age will all play a role in determining the APR you’re offered.

Loan Terms: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term means lower monthly payments, it also means you’ll pay more in interest over the life of the loan. This is a common trade-off that many borrowers face.

Pro tip from us: While lower monthly payments are appealing, try to choose the shortest loan term you can comfortably afford. This strategy minimizes the total interest paid and helps you build equity in your vehicle faster. Conversely, overly long terms can lead to negative equity, where you owe more than the car is worth.

Fees and Charges: Read the Fine Print

Beyond the interest rate, some lenders charge various fees that can add to your loan’s cost. These might include origination fees, application fees, or prepayment penalties. While many reputable lenders offer loans without these extra charges, it’s vital to be aware of them.

Always ask for a detailed breakdown of all potential fees before finalizing your loan agreement. Common mistakes to avoid are signing without thoroughly reviewing the full disclosure statement. Understanding every line item ensures there are no unwelcome surprises later on.

The Power of the Pre-Approval Process

A pre-approval is more than just a preliminary check; it’s a powerful tool in your car-buying arsenal. It involves a lender reviewing your credit and financial information to determine how much they are willing to lend you, at what interest rate, and under what terms. This process gives you a concrete offer before you even step onto a dealership lot.

Having a pre-approval allows you to shop like a cash buyer, focusing on the vehicle’s price rather than getting caught up in monthly payment negotiations. It also provides a benchmark, so you can compare any financing offered by the dealership against your independent pre-approved rate. This puts you in a much stronger negotiating position.

Credit Score Requirements: Knowing Where You Stand

Your credit score is a major determinant of the interest rate and loan terms you’ll qualify for. Lenders use credit scores to assess your creditworthiness and the likelihood of you repaying the loan. Generally, a higher credit score (typically 670 and above) will unlock the most favorable rates.

However, many lenders, including those similar to RoadLoans, cater to a range of credit profiles, from excellent to fair and even challenged credit. Understanding your own credit score and history before applying will help you target appropriate lenders and manage your expectations. For more insights into managing your credit, check out our article on .

Customer Service and Lender Reputation

While often overlooked, a lender’s reputation and quality of customer service are paramount. You want to work with a company that is transparent, responsive, and easy to communicate with if issues arise. Researching online reviews, customer testimonials, and Better Business Bureau ratings can provide valuable insights.

Based on my experience, a lender with strong customer support can make a significant difference, especially if you encounter unexpected financial challenges during your loan term. Look for lenders known for clear communication and helpfulness.

Top Alternatives to RoadLoans: A Deep Dive into Online Lenders

The market is rich with lenders offering car loans like RoadLoans, providing convenient online applications, competitive rates, and flexible terms. Here’s a look at some of the best categories and specific examples that stand out.

1. Direct Online Lenders

These lenders operate primarily online, offering a streamlined application process and often quick decisions, much like RoadLoans. They aim to provide competitive rates by minimizing overhead.

-

Capital One Auto Finance: A major player in the online auto loan space, Capital One offers pre-qualification that won’t impact your credit score, making it easy to see what you might qualify for. They work with a large network of dealerships, similar to RoadLoans, and cater to a wide range of credit scores. Their user-friendly online platform is a significant advantage.

-

LightStream (Truist Bank): For those with excellent credit, LightStream is often lauded for offering some of the lowest interest rates available. They provide unsecured auto loans, meaning the car itself isn’t collateral, which can offer greater flexibility. Their process is entirely online, fast, and highly efficient.

-

MyAutoLoan: This platform acts as a marketplace, connecting borrowers with multiple lenders. By filling out one application, you can receive up to four loan offers, allowing for easy comparison. MyAutoLoan is great for finding competitive rates and is known for catering to various credit scores, including those with less-than-perfect credit.

2. Credit Unions

Often overlooked, credit unions are non-profit financial institutions owned by their members. This structure frequently translates to lower interest rates and more personalized customer service compared to traditional banks or some online lenders.

To get a loan from a credit union, you typically need to become a member, which usually involves meeting specific eligibility criteria (e.g., living in a certain area, working for a particular employer, or joining an affiliated organization). The membership process is usually simple and worth the effort for the potential savings. Credit unions often have a more flexible approach to lending, especially for members with established relationships.

3. Traditional Banks

Major banks like Chase, Bank of America, and Wells Fargo also offer auto loans. While their online application processes may not be as rapid as some direct online lenders, they provide a sense of security and often have established relationships with local dealerships.

Banks can be a good option, especially if you already have an existing banking relationship, which might lead to preferential rates or easier application processes. They typically have stricter credit requirements than some online lenders but offer competitive rates for well-qualified borrowers.

4. Dealership Financing (Use with Caution)

While dealerships can arrange financing, it’s often wise to approach this option with a pre-approved loan already in hand. Dealerships work with various lenders and can sometimes offer attractive rates, especially if they have incentives from specific finance companies.

However, they might also mark up interest rates to increase their profit margin. Having an independent pre-approval allows you to compare their offer directly and ensure you’re getting the best deal. Pro tip: Never let a dealership be your only source for financing options.

The Pre-Approval Power Play: Your Secret Weapon

As mentioned earlier, getting pre-approved for a car loan before you start shopping is one of the smartest moves you can make. It transforms your buying experience from one of uncertainty to one of confidence and control. A pre-approval tells you precisely how much you can afford, at what interest rate, and for how long.

With a pre-approval letter in hand, you can negotiate the vehicle price without the distraction of financing details. The dealer knows you’re a serious buyer with your own funding, which puts you in a much stronger negotiating position. It also protects you from potentially being steered towards a more expensive vehicle or a higher interest rate than you qualify for.

Navigating Different Credit Scores: Loans for Everyone

Your credit score is a crucial factor, but it doesn’t dictate whether you get a loan, only the terms. Lenders like RoadLoans and its alternatives cater to a broad spectrum of credit profiles.

-

Excellent/Good Credit (700+): If you have a strong credit history, you’re in the best position to secure the lowest interest rates and most favorable terms. Lenders will compete for your business, so comparing multiple offers is key. LightStream, for example, is excellent for those with top-tier credit.

-

Fair/Average Credit (600-699): Many online lenders, including Capital One Auto Finance and MyAutoLoan, are well-equipped to assist borrowers with fair credit. You might not get the absolute lowest rates, but you can still find competitive offers. Focusing on a solid down payment can also help improve your terms.

-

Challenged/Bad Credit (Below 600): Don’t despair if your credit isn’t perfect. While you’ll likely face higher interest rates, securing an auto loan is still possible. Lenders specializing in bad credit loans, or credit unions, might be more understanding. Strategies like a larger down payment, a co-signer with good credit, or choosing a less expensive vehicle can significantly improve your chances and terms. For more detailed advice on this, you might find our article helpful.

Understanding Loan Terms & Avoiding Common Pitfalls

Beyond the initial approval, it’s crucial to understand the nuances of your loan agreement to avoid future headaches.

APR vs. Interest Rate: Know the Difference

While often used interchangeably, the APR (Annual Percentage Rate) provides a more complete picture of your loan’s cost than the simple interest rate. The APR includes the interest rate plus any fees that the lender charges, amortized over the loan term. Always focus on comparing APRs when evaluating offers.

The "Hidden" Costs: What Else to Watch For

Beyond the principal and interest, be wary of additional products often bundled into car loans. These might include extended warranties, GAP insurance, or credit life insurance. While some of these might offer value, they significantly increase your loan amount and interest paid. Always question what is being added and whether it’s truly necessary.

Longer Loan Terms vs. Higher Monthly Payments

As discussed, longer loan terms mean lower monthly payments, which can be very tempting. However, this convenience comes at a cost: more interest paid over time and the risk of negative equity. Common mistakes to avoid are automatically opting for the longest term available just to get the lowest payment. Think long-term.

Common Mistakes to Avoid Are:

- Not getting pre-approved: You lose significant negotiating power.

- Focusing only on monthly payments: This can lead to longer terms and more interest.

- Ignoring your credit report: Always check for errors before applying for a loan.

- Accepting the first offer: Always shop around for multiple quotes.

- Skipping the fine print: Understand every clause, especially regarding fees and penalties.

Refinancing Your Car Loan: When and Why It Makes Sense

Even if you’ve already secured a car loan, the journey doesn’t have to end there. Refinancing your auto loan means taking out a new loan to pay off your existing one, often with a different lender. This can be a smart move if interest rates have dropped, your credit score has significantly improved since you got your original loan, or you want to change your loan term.

Refinancing can potentially lower your monthly payments, reduce the total interest paid, or shorten your loan term. It’s always worth exploring if your financial situation has improved or if market rates are more favorable. Many of the same online lenders we’ve discussed also offer competitive refinancing options.

Pro Tips for Securing the Best Car Loan

Based on my years of experience, here are some actionable tips to ensure you get the most favorable terms for your next car loan:

- Know Your Credit Score: Get a free copy of your credit report from AnnualCreditReport.com and review it for accuracy. Address any errors before applying.

- Save for a Down Payment: A larger down payment reduces the amount you need to borrow, which can lead to better interest rates and lower monthly payments.

- Shop Around: Apply for pre-approval with at least 3-4 different lenders (online lenders, credit unions, banks). This allows you to compare offers effectively.

- Negotiate Separately: Negotiate the car’s price and the loan terms independently. Don’t let the dealership combine these discussions.

- Consider a Co-signer: If your credit isn’t stellar, a co-signer with excellent credit can help you qualify for better rates.

- Understand Your Budget: Don’t just focus on the car payment. Factor in insurance, fuel, maintenance, and registration costs.

Conclusion: Empowering Your Auto Loan Journey

The quest for the perfect car loan, much like finding the ideal vehicle, requires diligence and an informed approach. While RoadLoans offers a convenient and accessible entry point for many, a world of excellent alternatives awaits. By understanding key factors like APR, loan terms, and the power of pre-approval, you empower yourself to make a decision that aligns with your financial goals.

Remember, the goal isn’t just to get approved, but to secure the best possible terms for your situation. Take the time to compare, negotiate, and understand every detail of your loan. With the insights provided in this guide, you are now well-equipped to navigate the auto loan landscape with confidence and drive away with a deal that makes financial sense for you. For further trusted information on consumer finance, consider exploring resources like the Consumer Financial Protection Bureau (CFPB) website.