Beyond the Score: An In-Depth Look at How Bad Credit Car Loans Work for You

Beyond the Score: An In-Depth Look at How Bad Credit Car Loans Work for You Carloan.Guidemechanic.com

Navigating the world of auto financing can feel like a complex maze, especially when your credit score isn’t where you’d like it to be. Many people believe that a low credit score automatically disqualifies them from car ownership, but this simply isn’t true. While it presents unique challenges, obtaining a car loan with bad credit is absolutely possible.

This comprehensive guide will demystify the process, explaining exactly how bad credit car loans work. We’ll delve into the mechanics, outline the different types of lenders, and provide actionable strategies to help you secure financing and drive away in your next vehicle. Our goal is to equip you with the knowledge and confidence to make informed decisions, transforming what might seem like a roadblock into a manageable journey.

Beyond the Score: An In-Depth Look at How Bad Credit Car Loans Work for You

Understanding Bad Credit and Its Impact on Car Loans

Before diving into the specifics of how bad credit car loans work, it’s essential to understand what "bad credit" signifies in the eyes of a lender. Your credit score is a numerical representation of your creditworthiness, derived from your payment history, amounts owed, length of credit history, new credit, and credit mix. FICO scores, for instance, typically range from 300 to 850.

Generally, a FICO score below 620 is considered "subprime" or "bad credit." Lenders use this score to assess the risk of lending money to you. A lower score suggests a higher likelihood of default, meaning you might not repay the loan as agreed. This perceived risk is the primary reason why bad credit impacts car loan opportunities.

When a lender sees a low credit score, they interpret it as a signal of past financial difficulties. This doesn’t necessarily mean you’re a bad person or incapable of managing money, but it does raise a red flag from a purely financial perspective. Because of this elevated risk, lenders offering bad credit car loans often adjust their terms to protect their investment.

The Core Mechanics: How Do Bad Credit Car Loans Work?

The fundamental principle behind how bad credit car loans work is risk mitigation for the lender. Since borrowers with lower credit scores are seen as higher risk, lenders adjust various aspects of the loan to compensate. Understanding these adjustments is key to successfully navigating the process.

Higher Interest Rates

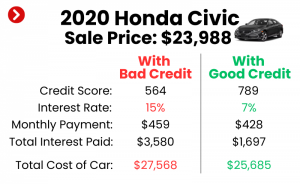

Perhaps the most significant difference you’ll encounter with a bad credit car loan is a higher interest rate, also known as the Annual Percentage Rate (APR). This is the lender’s primary way of compensating for the increased risk they’re taking. A higher APR means you’ll pay more over the life of the loan for the privilege of borrowing the money.

For example, while a borrower with excellent credit might qualify for an APR of 3-5%, someone with bad credit could face rates upwards of 15-25% or even higher. This difference can add thousands of dollars to the total cost of your vehicle. It’s crucial to factor this into your budget and understand the long-term financial implications.

Larger Down Payments

Lenders frequently require a larger down payment for bad credit car loans. A substantial down payment serves multiple purposes. Firstly, it reduces the amount of money you need to borrow, thereby lowering the lender’s exposure to risk.

Secondly, a larger down payment demonstrates your commitment to the purchase and your ability to save money. This signals financial responsibility, which can be reassuring to a lender. Based on my experience, aiming for at least 10-20% of the car’s purchase price as a down payment can significantly improve your chances of approval and potentially secure a slightly better rate.

Stricter Loan Terms

The terms of a bad credit car loan can also be more restrictive. While borrowers with excellent credit might have a wider range of loan durations (e.g., 36, 48, 60, or even 72 months), those with bad credit might find their options limited. Lenders might push for shorter loan terms, which result in higher monthly payments but reduce the overall interest paid.

Conversely, some lenders might offer longer terms to make monthly payments seem more affordable. However, this often means you’ll pay significantly more in interest over the loan’s lifetime. It’s a delicate balance, and understanding the total cost of the loan, not just the monthly payment, is vital.

Secured vs. Unsecured Loans

Car loans are almost always "secured" loans. This means the car itself acts as collateral for the loan. If you fail to make your payments, the lender has the legal right to repossess the vehicle to recoup their losses.

This secured nature is one of the reasons lenders are more willing to offer financing to individuals with bad credit for car purchases compared to, say, unsecured personal loans. The collateral provides a safety net for the lender, reducing their overall risk.

Specialized Lenders and "Subprime" Financing

Not all lenders are equipped or willing to handle bad credit car loans. This niche market is primarily served by "subprime" lenders who specialize in working with borrowers who have less-than-perfect credit. These lenders have different risk assessment models and understand the unique challenges faced by this demographic.

You might also encounter "Buy Here, Pay Here" dealerships, which operate as both the seller and the lender. While they often offer easy approval, they typically come with significantly higher interest rates and less favorable terms. We’ll explore these options in more detail shortly.

Types of Lenders Offering Bad Credit Car Loans

Understanding where to look for financing is a crucial step in how bad credit car loans work. Different types of lenders cater to various credit profiles, each with its own advantages and disadvantages.

Dealership Financing (Captive & Independent)

Many car dealerships offer financing options directly on-site, acting as intermediaries between you and various lenders. This can be very convenient, allowing you to choose a car and secure financing all in one place. Dealerships often work with a network of banks, credit unions, and subprime lenders.

Some dealerships have "captive" finance companies (e.g., Ford Credit, Toyota Financial Services), while others work with independent finance companies. The advantage here is that the finance manager can often "shop" your application to multiple lenders, potentially finding you the best available rate for your credit situation. However, always be prepared to compare their offer with outside financing.

Online Lenders

The digital age has brought a wealth of online lenders specializing in bad credit auto loans. These platforms allow you to apply from the comfort of your home, often receiving pre-qualification decisions within minutes. Online lenders can be a great way to compare offers from multiple institutions without visiting various dealerships or banks.

Pro tips from us: Many online lenders use soft credit inquiries for pre-qualification, which don’t affect your credit score. This allows you to gauge your eligibility and potential rates before committing to a full application. Always verify the lender’s reputation and read reviews.

Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. They often offer more competitive interest rates and more flexible terms than traditional banks, even for borrowers with bad credit. Their member-centric approach means they might be more willing to work with you individually to find a solution.

To qualify for a credit union loan, you typically need to become a member, which usually involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer). If you qualify, exploring a credit union is often a smart move for any auto loan.

"Buy Here, Pay Here" Dealerships

"Buy Here, Pay Here" (BHPH) dealerships are unique because they are both the seller of the car and the lender. This means they finance the vehicle themselves, cutting out third-party banks or finance companies. They often advertise "guaranteed approval" or "no credit check" loans, making them appealing to individuals with very poor credit or no credit history.

While BHPH dealerships offer a last resort for many, they come with significant drawbacks. Interest rates are typically much higher, and the vehicle selection may be limited to older, higher-mileage cars. Furthermore, not all BHPH dealerships report payments to credit bureaus, which means making on-time payments might not help rebuild your credit score. Use these as a last resort only.

The Application Process for Bad Credit Car Loans

Understanding the application process is critical for anyone wondering how bad credit car loans work and how to get one approved. While the specifics can vary slightly between lenders, the core requirements and steps remain consistent.

Pre-qualification vs. Full Application

Many lenders offer a pre-qualification option. This involves submitting some basic financial information, often resulting in a soft credit pull that doesn’t impact your credit score. Pre-qualification gives you an idea of the loan amount you might be approved for and an estimated interest rate. It’s a fantastic tool for setting realistic expectations before you even start seriously shopping for a car.

A full application, on the other hand, requires more detailed personal and financial information and involves a hard credit inquiry. This hard inquiry will temporarily ding your credit score by a few points. However, if you’re shopping for a car loan within a short period (typically 14-45 days, depending on the scoring model), multiple hard inquiries for auto loans are usually grouped as a single inquiry, minimizing the impact on your score.

Required Documents

When applying for a bad credit car loan, be prepared to provide several documents. Lenders need to verify your identity, income, and residency to assess your ability to repay the loan. Common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-4), bank statements showing direct deposits, tax returns if self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Proof of Employment: Contact information for your employer, employment verification letters.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and price.

Having these documents organized and ready can significantly speed up the application process.

What Lenders Look For Beyond the Score

While your credit score is important, it’s not the only factor lenders consider when approving bad credit car loans. They also look at:

- Income Stability: Consistent employment and a reliable income source are crucial. Lenders want to see that you have the means to make your monthly payments.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover a new car payment.

- Employment History: A stable work history (e.g., at least 6 months to a year at your current job) signals reliability.

- Residential Stability: How long you’ve lived at your current address can also be a factor, indicating stability.

Lenders use these additional data points to get a fuller picture of your financial responsibility, even if your credit score tells a less favorable story.

Common Mistakes to Avoid

Based on my experience, some common mistakes can hinder your bad credit car loan application:

- Applying Everywhere: Don’t submit full applications to numerous lenders haphazardly. Too many hard inquiries in a short period can further damage your credit score. Use pre-qualification first.

- Hiding Information: Be honest and transparent about your financial situation. Lenders will uncover discrepancies, which can lead to immediate denial.

- Focusing Only on Monthly Payment: While tempting, don’t let a low monthly payment blind you to high interest rates or extended loan terms that drastically increase the total cost.

- Not Shopping Around: Even with bad credit, comparing offers from different lenders can save you money. Never take the first offer presented.

Strategies to Improve Your Chances of Approval (and Get Better Terms)

Even with bad credit, you have options to strengthen your position and potentially secure more favorable loan terms. These strategies focus on reducing the lender’s risk and demonstrating your commitment.

Save for a Down Payment

As mentioned earlier, a significant down payment is one of the most effective ways to improve your chances. It reduces the loan amount, lowers your monthly payments, and signals financial discipline. Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. The more you put down, the less risk the lender takes on, and the more likely you are to get approved with better terms.

Find a Co-signer

A co-signer is someone with good credit who agrees to take legal responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk, as they have a second, more creditworthy individual to pursue if you default. This can be a game-changer for approval and interest rates.

However, choosing a co-signer is a serious decision. It impacts their credit score and financial well-being, so both parties must understand the full implications. Ensure you are absolutely committed to making every payment on time to protect your relationship and their credit.

Improve Your Credit Score First (If Possible)

If your need for a car isn’t immediate, dedicating time to improve your credit score can yield substantial long-term savings. Even a modest increase can move you into a different tier of interest rates. Focus on:

- Paying bills on time: Payment history is the most critical factor.

- Reducing outstanding debt: Especially on credit cards, lowering your credit utilization.

- Checking your credit report for errors: Disputing any inaccuracies can boost your score.

For more detailed strategies on credit improvement, you might find our article helpful.

Choose the Right Car

When you have bad credit, it’s not the time to splurge on a luxury vehicle. Lenders are more comfortable financing a reliable, affordable car that retains its value well. Opt for a pre-owned vehicle that is within your budget and meets your needs without adding unnecessary financial strain. A lower loan amount means lower risk for the lender.

Demonstrate Income Stability

Lenders want assurance that you can consistently make payments. Providing clear, verifiable proof of stable income and employment history is crucial. This means having recent pay stubs, bank statements, and consistent employment at your current job. If you’ve recently changed jobs, be prepared to explain the circumstances and demonstrate continuity of income.

Shop Around for Lenders

Even with bad credit, never settle for the first offer you receive. Apply for pre-qualification with several different types of lenders – online lenders, credit unions, and dealerships. Compare their interest rates, loan terms, and fees. This competitive shopping can uncover better deals and save you a significant amount of money over the life of the loan.

Managing Your Bad Credit Car Loan Responsibly

Getting approved for a bad credit car loan is a victory, but managing it responsibly is where the real long-term benefits lie. This is your opportunity to rebuild your credit and establish a stronger financial future.

Make Payments On Time, Every Time

This is the most critical aspect of responsible loan management. Every on-time payment reported to credit bureaus helps improve your payment history, which is the single most important factor in your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

A consistent record of timely payments will gradually, but surely, elevate your credit score. This opens doors to better financial products and lower interest rates in the future, including potential refinancing opportunities for your car loan.

Understand Your Loan Agreement

Before signing any documents, thoroughly read and understand your entire loan agreement. Pay close attention to:

- Annual Percentage Rate (APR): The true cost of borrowing, including interest and fees.

- Total Loan Amount: The principal plus all interest and fees over the loan term.

- Loan Term: The duration of the loan in months.

- Fees: Any origination fees, late payment fees, or prepayment penalties.

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early. Know if yours does.

If anything is unclear, ask questions until you fully grasp every clause. A well-informed borrower is a powerful borrower. For a deeper dive into auto loan specifics, you might find useful.

Beware of Predatory Lending

Unfortunately, the subprime lending market can sometimes attract less reputable lenders. Be cautious of offers that seem too good to be true, such as "guaranteed approval" with no income verification or extremely high-pressure sales tactics. Red flags include:

- Excessively high interest rates (well beyond the typical range for bad credit).

- Adding unnecessary products (like extended warranties or service contracts) without your explicit consent.

- Lack of transparency regarding fees or loan terms.

- Pushing you into a car you clearly can’t afford.

If something feels off, walk away. It’s better to wait and find a reputable lender than to fall victim to a predatory loan.

Refinancing Options

Once you’ve made consistent on-time payments for 6-12 months and your credit score has improved, you might be eligible to refinance your bad credit car loan. Refinancing involves taking out a new loan, often with a lower interest rate, to pay off your existing one. This can significantly reduce your monthly payments and the total amount of interest you pay over time.

Keep an eye on interest rates and your credit score. When they align favorably, explore refinancing options with different lenders, including credit unions, which often offer competitive rates.

The Power of Positive Reporting

One of the greatest benefits of a responsibly managed bad credit car loan is its positive impact on your credit report. When your payments are consistently reported as "on-time," it demonstrates your ability to handle credit responsibly. This helps to rebuild your credit history, leading to better opportunities in the future for all types of loans and credit products.

This entire process is a journey. Your bad credit car loan isn’t just a way to get a car; it’s a powerful tool for financial rehabilitation if used wisely.

Common Myths and Misconceptions about Bad Credit Car Loans

The topic of bad credit car loans is often surrounded by misinformation. Separating fact from fiction is crucial for anyone trying to understand how bad credit car loans work.

Myth: "Guaranteed Approval" Car Loans Mean Anyone Can Get One

Reality: While some lenders advertise "guaranteed approval," this is often misleading. What they mean is that they will approve someone for some kind of financing, but it might come with extremely high interest rates, unfavorable terms, or require a substantial down payment. There are always minimum qualifications, such as verifiable income or residency, that must be met. No legitimate lender can truly "guarantee" approval without any conditions.

Myth: "No Credit Check" Loans Are Always the Best Option for Bad Credit

Reality: "No credit check" loans, often offered by "Buy Here, Pay Here" dealerships, avoid pulling your credit report. While this might seem appealing, these loans typically come with significantly higher interest rates than even standard bad credit loans. Furthermore, these dealerships often don’t report your payments to credit bureaus. This means that even if you make all your payments on time, it won’t help you rebuild your credit score. They should generally be considered a last resort.

Myth: You’ll Always Get Ripped Off with Bad Credit

Reality: While it’s true that bad credit car loans come with higher interest rates and potentially stricter terms, it doesn’t mean you’ll automatically be "ripped off." By being informed, shopping around, understanding your budget, and negotiating, you can secure a fair deal given your credit situation. The key is to be an educated consumer and avoid predatory lenders. Empower yourself with knowledge, as we’ve aimed to do with this article.

Conclusion: Driving Towards Financial Recovery with Bad Credit Car Loans

Navigating the world of bad credit car loans can feel intimidating, but as we’ve explored, it’s a well-defined path with clear mechanisms and strategies for success. Understanding how bad credit car loans work is the first and most critical step towards securing reliable transportation and, perhaps more importantly, rebuilding your financial future.

While higher interest rates and stricter terms are part of the landscape, they are not insurmountable obstacles. By saving for a down payment, considering a co-signer, shopping diligently for lenders, and demonstrating income stability, you can significantly improve your chances of approval and secure more favorable terms. Remember, this journey isn’t just about getting a car; it’s about proving your creditworthiness and setting yourself on a path to financial recovery.

Once approved, managing your loan responsibly by making every payment on time will be your most powerful tool for credit score improvement. This consistency will open doors to better financial opportunities, including the possibility of refinancing your car loan down the line. Don’t let a past financial misstep define your future. With careful planning and responsible execution, a bad credit car loan can be a stepping stone to a brighter financial horizon and the reliable transportation you need. Start your journey today, armed with knowledge and confidence!

Further Reading: