BMW Used Car Loan Rates: Your Ultimate Guide to Securing the Best Deal

BMW Used Car Loan Rates: Your Ultimate Guide to Securing the Best Deal Carloan.Guidemechanic.com

The allure of a BMW is undeniable. From the iconic kidney grille to the precision engineering, owning a "Bimmer" represents a blend of luxury, performance, and status. While a brand-new BMW might be out of reach for some, a pre-owned model offers an incredible opportunity to experience this automotive excellence without the steep depreciation hit. However, navigating the world of BMW used car loan rates can feel like another complex engine to master.

This comprehensive guide is designed to demystify the financing process for a used BMW. We’ll dive deep into everything you need to know, from understanding what influences your loan rate to uncovering strategies for securing the most favorable terms. Our goal is to empower you with the knowledge to make informed decisions, ensuring your journey into BMW ownership is as smooth and exhilarating as the drive itself.

BMW Used Car Loan Rates: Your Ultimate Guide to Securing the Best Deal

Why a Used BMW is a Smart Investment

Choosing a used BMW isn’t just about saving money upfront; it’s a savvy financial move that offers significant benefits. New cars depreciate rapidly the moment they’re driven off the lot, losing a substantial portion of their value in the first few years. Opting for a pre-owned model allows you to bypass this initial, steepest depreciation curve.

You gain access to premium features, advanced technology, and superior driving dynamics that would be significantly more expensive in a new vehicle. A well-maintained, pre-owned BMW can offer exceptional value, delivering a luxury experience at a fraction of the original cost. This intelligent approach allows you to enjoy the prestige and performance of a BMW while making a sound financial decision.

Understanding BMW Used Car Loan Rates: The Core Concept

At its heart, a used car loan is a sum of money borrowed to purchase a vehicle, which you then repay with interest over a set period. The interest rate is essentially the cost of borrowing that money, expressed as an Annual Percentage Rate (APR). This APR is a crucial figure because it encompasses not just the interest rate but also any additional fees associated with the loan, providing a more complete picture of your borrowing cost.

Your BMW used car loan rate directly impacts your monthly payments and the total amount you’ll pay over the life of the loan. A lower APR means lower monthly payments and less money spent on interest overall. Understanding how these rates are determined is the first step toward securing a competitive deal.

Lenders assess various factors to determine the risk associated with lending you money. This risk assessment directly translates into the interest rate they offer. The higher the perceived risk, the higher your interest rate will likely be.

Key Factors Influencing Your BMW Used Car Loan Rate

Several critical elements come into play when lenders calculate your potential BMW used car loan rate. Each factor contributes to their overall assessment of your creditworthiness and the perceived risk of the loan. Let’s break down these influential components.

1. Your Credit Score: The Ultimate Indicator

Your credit score is arguably the single most important factor determining your interest rate. It’s a three-digit number that summarizes your financial history, indicating how reliably you’ve managed debt in the past. Lenders use this score to quickly gauge your risk as a borrower.

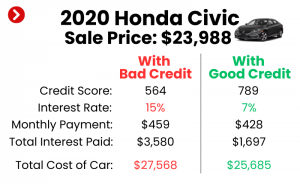

- Excellent Credit (780+): Borrowers with excellent credit scores typically qualify for the lowest available BMW used car loan rates. They are considered low-risk, demonstrating a strong history of on-time payments and responsible credit management.

- Good Credit (670-779): Most consumers fall into this category. You’ll still qualify for competitive rates, though they might be slightly higher than those for excellent credit. Showing consistent financial responsibility is key here.

- Fair Credit (580-669): With fair credit, rates will be higher as lenders perceive a greater risk. It’s still possible to get approved, but improving your score before applying can save you significant money.

- Poor Credit (Below 580): Securing a loan with poor credit can be challenging, and the rates will be substantially higher. Lenders might require a larger down payment, a co-signer, or a shorter loan term to mitigate their risk.

Based on my experience as a financial advisor, consistently paying bills on time, keeping credit utilization low, and avoiding new debt can significantly boost your score. A strong credit history not only opens doors to better loan options but also reinforces your financial reputation.

2. The Loan Term: Length Matters

The loan term refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This choice has a direct impact on both your monthly payment and the total interest paid.

- Shorter Loan Terms: Opting for a shorter term (e.g., 36 or 48 months) usually results in higher monthly payments. However, you’ll pay significantly less interest over the life of the loan. Lenders also view shorter terms as less risky, which can sometimes lead to a slightly lower interest rate.

- Longer Loan Terms: Longer terms (e.g., 60 or 72 months) reduce your monthly payments, making the car more "affordable" on a month-to-month basis. The trade-off is that you’ll pay considerably more in total interest, and the car might be older and require more maintenance before the loan is fully paid off.

Common mistakes to avoid are extending the loan term too much just to lower the monthly payment. While it might seem appealing initially, you could end up "upside down" on your loan (owing more than the car is worth) and pay a hefty sum in interest.

3. Your Down Payment: Showing Commitment

A down payment is the initial amount of money you pay towards the purchase of the vehicle. It reduces the total amount you need to borrow, which directly impacts your loan.

- Lower Loan Amount: A larger down payment means you’re borrowing less money, which translates to lower monthly payments and less interest paid overall.

- Reduced Risk for Lender: Lenders view a substantial down payment favorably. It demonstrates your financial commitment and reduces their risk, as you have immediate equity in the vehicle. This can often result in a lower BMW used car loan rate.

- Avoiding Negative Equity: A good down payment helps prevent you from owing more than the car is worth (negative equity), especially with a depreciating asset like a car.

Pro tips from us: Aim for at least a 10-20% down payment on a used car if possible. This not only lowers your financial burden but also positions you for better loan terms.

4. Vehicle Age and Mileage: Perceived Risk

The age and mileage of the used BMW you’re considering also play a role in financing. Lenders assess these factors to determine the vehicle’s reliability and resale value.

- Newer Used Models (Lower Mileage): Generally, newer used BMWs with lower mileage are seen as less risky. They are expected to be more reliable and hold their value better, often qualifying for more favorable interest rates.

- Older Used Models (Higher Mileage): Older vehicles with high mileage are perceived as higher risk due to potential maintenance issues and lower resale value. Lenders might offer higher rates or shorter loan terms for these vehicles. Some lenders may even have restrictions on financing very old or high-mileage cars.

This isn’t to say you can’t finance an older BMW; it just means you might need to be prepared for different loan terms.

5. The Interest Rate Environment: Market Conditions

Broader economic factors, particularly the prevailing interest rate environment set by central banks (like the Federal Reserve in the U.S.), influence all lending rates. When the Fed raises its benchmark rates, auto loan rates generally tend to increase across the board. Conversely, a period of lower interest rates can make borrowing more affordable.

While you have no control over market conditions, being aware of them can help you understand why rates might be higher or lower than they were historically. Timing your purchase, if possible, can sometimes work in your favor.

6. Lender Type: Diverse Options

The type of lender you choose can also impact your BMW used car loan rates and the overall financing experience. Different institutions have different risk appetites, fee structures, and customer service models. We’ll explore these options in detail later.

Where to Find the Best BMW Used Car Loan Rates

Finding the best financing deal for your used BMW requires a bit of research and comparison shopping. Don’t settle for the first offer you receive. Exploring various lender types can uncover significantly better rates and terms.

1. BMW Financial Services

For many BMW enthusiasts, BMW Financial Services (BMW FS) is the first stop. They specialize in financing BMW vehicles and often have specific programs for their Certified Pre-Owned (CPO) inventory.

- Pros:

- Specialized Knowledge: They understand BMWs inside and out.

- CPO Incentives: Often offer competitive rates or special promotions for BMW CPO vehicles. This is because CPO vehicles undergo rigorous inspections and come with extended warranties, reducing lender risk.

- Convenience: Can often handle financing directly at the dealership, streamlining the purchase process.

- Cons:

- Limited Scope: Primarily focused on BMW vehicles, so if you’re comparing other brands, you’ll need other lenders.

- Rates May Not Always Be the Lowest: While competitive for CPO, their rates for non-CPO used BMWs might not always beat external lenders, especially if you have excellent credit.

2. Banks and Credit Unions

Traditional banks and local credit unions are excellent places to shop for BMW used car loan rates. They offer a wide range of auto loan products and are often very competitive, especially for borrowers with good credit.

- Banks: Large national banks often have established auto lending divisions. They can offer competitive rates and the convenience of managing all your finances under one roof.

- Credit Unions: These member-owned institutions are known for offering some of the most competitive interest rates and personalized service. Because they are non-profit, they often pass savings on to their members. If you’re eligible to join a credit union (based on employment, geographic location, or association), it’s definitely worth checking their rates.

Pro tips from us: Always seek pre-approval from at least two banks or credit unions before you even step foot in a dealership. This gives you a strong negotiating tool and a clear understanding of what a competitive rate looks like for your financial profile.

3. Online Lenders

The digital age has brought a new wave of online-only lenders specializing in auto financing. These platforms offer convenience, speed, and often highly competitive rates due to their lower overhead costs.

- Pros:

- Quick Applications: Many offer fast online applications and instant pre-approvals.

- Competitive Rates: Can often undercut traditional lenders, especially for well-qualified buyers.

- Wide Comparison: Many online platforms allow you to compare offers from multiple lenders simultaneously.

- Cons:

- Less Personal Interaction: If you prefer face-to-face service, this might not be for you.

- Varying Reputations: It’s crucial to research the lender’s reputation before committing.

4. Dealership Financing (Beyond BMW FS)

While BMW dealerships offer BMW FS, they also often work with a network of other banks and financial institutions. This means they can present you with multiple financing options.

- Pros:

- Convenience: One-stop shopping; you can test drive, negotiate, and finance all in one place.

- Potential Incentives: Dealerships sometimes offer special promotional rates or manufacturer incentives, especially on certain models or during specific sales events.

- Cons:

- Markup: Dealerships might mark up the interest rate they receive from a lender to generate profit. This is why having your own pre-approval is so crucial.

- Limited Options: They may only work with a select few lenders, potentially missing out on a better rate elsewhere.

Based on my experience, never rely solely on dealership financing. Always walk in with at least one pre-approval in hand to ensure you’re getting a fair deal. This leverage can save you thousands over the loan term.

The BMW Certified Pre-Owned (CPO) Advantage

When discussing BMW used car loan rates, the topic of Certified Pre-Owned (CPO) vehicles often comes up. A BMW CPO car isn’t just a "used car"; it’s a meticulously inspected, low-mileage BMW that meets stringent factory standards.

- Rigorous Inspection: CPO BMWs undergo a comprehensive multi-point inspection by factory-trained technicians.

- Extended Warranty: They come with an extended warranty from BMW, providing peace of mind beyond the original factory warranty.

- Roadside Assistance: Many CPO programs include roadside assistance.

Because CPO vehicles are considered lower risk by lenders (due to their thorough inspection, reconditioning, and warranty coverage), they often qualify for more attractive financing rates. BMW Financial Services, in particular, frequently offers special, lower APRs for CPO vehicles compared to non-CPO used BMWs. This can make the slightly higher initial cost of a CPO vehicle worthwhile in the long run, especially when factoring in potential savings on maintenance and financing.

Strategies to Secure a Lower BMW Used Car Loan Rate

Armed with knowledge about what influences rates and where to find loans, let’s focus on actionable strategies to put you in the best possible position to secure the lowest BMW used car loan rate.

1. Improve Your Credit Score

This is foundational. Even small improvements to your credit score can translate into significant savings on interest.

- Check Your Credit Report: Obtain your free credit reports from Experian, Equifax, and TransUnion. Review them for errors and dispute any inaccuracies immediately.

- Pay Bills On Time: Payment history is the biggest factor in your score. Set up automatic payments to avoid missing due dates.

- Reduce Debt: Lowering your credit card balances reduces your credit utilization ratio, which positively impacts your score.

- Avoid New Credit: Don’t open new credit accounts or apply for multiple loans in the months leading up to your car purchase, as this can temporarily ding your score.

For more details on improving your credit score, check out our guide on .

2. Save for a Larger Down Payment

As discussed, a larger down payment reduces the amount you need to borrow and signals financial responsibility to lenders. Aim for at least 10-20% of the vehicle’s purchase price. This not only lowers your monthly payment but can also help you secure a better interest rate.

3. Choose a Shorter Loan Term (If Affordable)

If your budget allows for higher monthly payments, opt for a shorter loan term. You’ll pay off the car faster, significantly reduce the total interest paid, and potentially qualify for a slightly lower APR. Always balance affordability with the total cost of the loan.

4. Consider a Co-signer

If you have fair or poor credit, or if you’re a young borrower with limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a much lower rate. A co-signer shares responsibility for the loan, so ensure they understand the commitment.

5. Shop Around Aggressively for Pre-approvals

This is perhaps the most crucial step. Don’t rely on the first offer. Apply for pre-approval with at least three to five different lenders – banks, credit unions, and online lenders.

- Compare APRs: Focus on the Annual Percentage Rate (APR), not just the monthly payment.

- Understand Terms: Read the fine print regarding fees, prepayment penalties, and other conditions.

- Use Pre-approval as Leverage: Once you have a pre-approval in hand, you can use it to negotiate with the dealership’s finance department. If they can’t beat your pre-approved rate, you already have a fantastic alternative.

All credit inquiries made within a short period (typically 14-45 days, depending on the scoring model) for the same type of loan (like an auto loan) are usually treated as a single inquiry, minimizing the impact on your credit score.

6. Negotiate with the Dealer (If Using Their Financing)

If the dealership offers an attractive rate, you still have room to negotiate. They might be able to match or even beat your external pre-approval to earn your business. Be firm, polite, and always have your pre-approval as a backup.

Common Mistakes to Avoid When Financing a Used BMW

Even experienced buyers can fall into common traps when financing a vehicle. Being aware of these pitfalls can save you money and headaches.

- Not Checking Your Credit Score: Going into the financing process blind is a major error. Know your score and review your report beforehand.

- Only Getting One Loan Offer: This is akin to buying the first car you see. Always shop around for multiple pre-approvals to ensure you’re getting the best possible BMW used car loan rate.

- Focusing Solely on the Monthly Payment: While important, fixating only on the monthly payment can lead to extending the loan term excessively or accepting a higher interest rate, costing you more in the long run. Always look at the total cost of the loan.

- Extending the Loan Term Too Much: Long loan terms (72+ months) mean you’ll pay significantly more interest and risk being "upside down" on your loan for a longer period. Try to keep terms to 60 months or less if feasible.

- Ignoring Additional Fees: Be aware of any origination fees, documentation fees, or other charges that can inflate the total cost of your loan. Always ask for a full breakdown of all costs.

- Falling for High-Pressure Sales Tactics: Don’t let a salesperson rush you into a decision. Take your time, read all documents carefully, and don’t sign anything you don’t fully understand.

- Not Factoring in Insurance and Maintenance: A BMW, even a used one, can have higher insurance premiums and maintenance costs than a non-luxury vehicle. Ensure these are factored into your budget before committing to a loan.

Refinancing Your BMW Used Car Loan

What if you’ve already financed a used BMW and now realize you could get a better rate? Refinancing is a viable option that can save you money.

When It Makes Sense to Refinance:

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you might qualify for a lower interest rate.

- Lower Market Rates: If general auto loan rates have dropped since your purchase, refinancing could be beneficial.

- Original High Rate: If you had fair credit or didn’t shop around initially, you might be paying a higher rate than necessary.

- Change in Financial Situation: You might want to lower your monthly payments by extending the term (though this means more interest overall) or shorten the term to pay it off faster.

How to Refinance:

- Check Your Current Loan Details: Gather information on your existing loan balance, interest rate, and remaining term.

- Shop for New Rates: Apply for pre-approvals from various lenders, just as you did for your initial loan.

- Compare Offers: Look for a new loan that offers a significantly lower APR or better terms.

- Complete the Process: Once approved, the new lender will pay off your old loan, and you’ll begin making payments to the new lender.

Refinancing can be a powerful tool to reduce your financial burden and align your loan with your current financial standing. According to the Consumer Financial Protection Bureau, understanding your loan terms, including the APR, is crucial for making informed decisions about refinancing.

Conclusion: Drive Your Dream BMW with Confidence

Owning a used BMW is a fantastic way to experience luxury and performance without the premium price tag of a new model. However, securing favorable BMW used car loan rates is paramount to making this dream financially sustainable. By understanding the factors that influence your rate, actively shopping around with various lenders, and employing smart strategies, you empower yourself to get the best possible deal.

Remember to prioritize improving your credit, making a solid down payment, and always comparing multiple loan offers. Avoid common pitfalls by focusing on the total cost of the loan, not just the monthly payment. With this comprehensive knowledge, you’re now well-equipped to navigate the world of used BMW financing with confidence, ensuring your journey into BMW ownership is as rewarding as the drive itself. Happy hunting for your ultimate driving machine!