Can a 600 Credit Score Get a Car Loan? Your Comprehensive Guide to Driving Away with Confidence

Can a 600 Credit Score Get a Car Loan? Your Comprehensive Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Driving a reliable car is a necessity for many, offering freedom and convenience. But what if your credit score hovers around 600, placing you in the "subprime" category? This often sparks anxiety and leads to a crucial question: Can a 600 credit score get a car loan?

Based on my extensive experience in the financial and automotive sectors, the resounding answer is yes, it is absolutely possible. However, it’s not always a straightforward path, and understanding the nuances is key. This in-depth guide will equip you with the knowledge, strategies, and confidence to navigate the lending landscape and secure the car loan you need, even with a 600 credit score.

Can a 600 Credit Score Get a Car Loan? Your Comprehensive Guide to Driving Away with Confidence

We’ll dive deep into what lenders look for, how to improve your chances, where to find the best financing options, and critical advice to avoid common pitfalls. Our ultimate goal is to empower you to make informed decisions and drive away in your new vehicle with a smart, sustainable loan.

Understanding Your 600 Credit Score: What It Means for Lenders

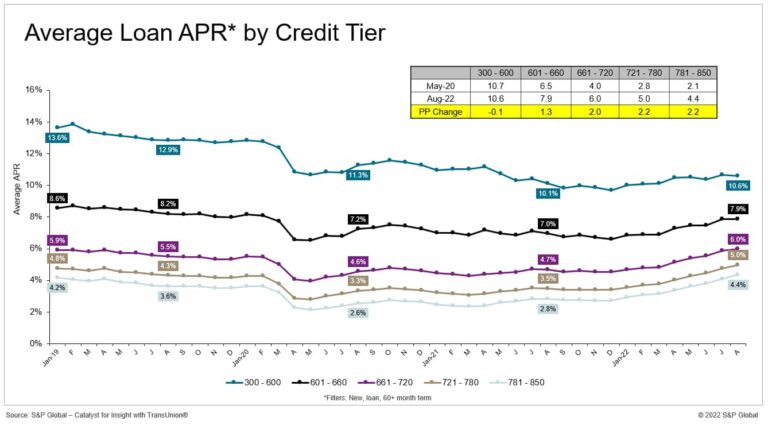

Before we explore the "how," let’s clarify what a 600 credit score signifies in the eyes of a lender. Credit scores, such as FICO or VantageScore, range from 300 to 850. A score of 600 typically falls into the "Fair" or "Subprime" category.

This classification indicates a moderate level of risk to lenders. While it’s not considered "bad credit," it suggests that you might have a history of missed payments, high credit utilization, or a limited credit history. Lenders use this score to assess the likelihood of you repaying your loan on time.

For a 600 score, lenders will generally perceive a higher risk compared to someone with excellent credit. This perception often translates into less favorable loan terms, primarily higher interest rates. They’re not saying "no" outright, but they are proceeding with caution.

The Reality: Yes, You Can Get a Car Loan, But With Caveats

So, can a 600 credit score get a car loan? Absolutely. Many lenders specialize in working with borrowers in the subprime credit range. The critical distinction, however, lies in the terms of the loan you’ll likely receive.

You should prepare for interest rates that are higher than what someone with a 700+ credit score would qualify for. This is the lender’s way of mitigating the increased risk they’re taking on. Higher interest rates mean you’ll pay more over the life of the loan.

However, a 600 credit score doesn’t automatically condemn you to predatory rates. With the right strategy and preparation, you can secure a manageable loan. The key is to demonstrate your ability to repay and reduce the lender’s perceived risk in other ways.

Beyond the Score: Factors Lenders Consider

While your credit score is a significant factor, it’s not the only piece of the puzzle. Lenders look at a holistic view of your financial situation. Understanding these other factors allows you to strengthen your application, even with a 600 score.

1. Your Income and Employment Stability

Lenders want to see a consistent and reliable source of income. This reassures them that you have the financial capacity to make your monthly car payments. They’ll typically ask for proof of income, such as pay stubs, W-2s, or tax returns.

Long-term employment with the same company is a huge plus. It signals stability and a reduced risk of job loss, which directly impacts your ability to repay. A steady job history, even across different employers, is also beneficial.

2. Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric. It compares your total monthly debt payments (including the prospective car loan) to your gross monthly income. For example, if your total monthly debt payments are $1,500 and your gross monthly income is $4,000, your DTI is 37.5%.

Lenders generally prefer a DTI ratio below 43%, though some may go higher for subprime loans. A lower DTI indicates that you have enough disposable income to comfortably manage new debt. A high DTI can be a red flag, even with a decent income.

3. The Size of Your Down Payment

This is perhaps one of the most powerful tools you have to improve your chances with a 600 credit score. A substantial down payment significantly reduces the lender’s risk. It means you’re borrowing less money, and you have immediate equity in the vehicle.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price, if possible. Not only does it make you a more attractive borrower, but it also lowers your monthly payments and the total interest you’ll pay over the loan term. It shows commitment.

4. The Vehicle You Choose

The type of car you want to finance also plays a role. Lenders are more comfortable financing a reasonably priced vehicle that aligns with your income and budget. Trying to finance an expensive luxury car with a 600 credit score is a much harder sell.

New cars often have lower interest rates through manufacturer incentives, but their higher price point might make them less suitable for a subprime borrower. Used cars can be a good option, but ensure they are not too old or have excessive mileage, as lenders may see older vehicles as higher risk.

5. Payment History on Previous Auto Loans (If Any)

If you’ve had an auto loan before, your payment history on that specific loan is incredibly valuable. Making all your payments on time, even if you had a 600 score then, demonstrates your reliability as an auto borrower. This can sometimes outweigh other negative aspects of your credit report.

Conversely, a history of missed car payments will make securing a new auto loan much more challenging. Lenders will see this as a direct indicator of future risk.

6. Having a Co-signer

A co-signer with good credit can dramatically improve your chances of approval and help you secure better loan terms. A co-signer legally agrees to be responsible for the loan if you fail to make payments. This reduces the risk for the lender.

However, choosing a co-signer is a serious decision. It impacts their credit score and financial well-being. Ensure both parties understand the full implications before proceeding. It’s often best reserved for close family members who understand the commitment.

Strategies to Improve Your Chances of Approval

Don’t just hope for the best; actively work to present yourself as the best possible candidate. Here are actionable strategies:

1. Save for a Larger Down Payment

As mentioned, a substantial down payment is your secret weapon. It reduces the amount you need to borrow, which lowers the lender’s risk and your monthly payments. This also decreases the total interest paid over the life of the loan.

Consider setting a savings goal for your down payment. Even an extra few hundred dollars can make a difference in your loan terms and approval odds. This demonstrates financial responsibility and commitment.

2. Get Pre-Approved Before You Shop

Applying for pre-approval from multiple lenders is a smart move. It gives you a clear idea of what loan amount and interest rate you can expect before you step onto a dealership lot. This puts you in a stronger negotiating position.

Pre-approvals are usually "soft inquiries" on your credit, meaning they won’t negatively impact your score. It also helps you set a realistic budget for your car purchase.

3. Consider a Co-signer (If Feasible)

If you have a trusted friend or family member with good credit who is willing to co-sign, this can be a game-changer. Their strong credit profile can offset your 600 score, potentially securing you a lower interest rate and better terms.

Remember, a co-signer shares equal responsibility for the loan. If you miss payments, it will negatively affect both your credit scores. Ensure clear communication and a solid plan for repayment.

4. Choose the Right Vehicle for Your Budget

Be realistic about what you can afford. Focus on reliable, practical vehicles that fit within your budget rather than stretching for a car that will strain your finances. A lower car price means a smaller loan amount, which is easier to get approved for and manage.

Consider certified pre-owned (CPO) vehicles. They offer many of the benefits of new cars (warranty, inspection) but at a lower price point, making them an excellent value proposition.

5. Shop Around for Lenders

Common mistakes to avoid are accepting the first loan offer you receive, especially at the dealership. Don’t limit yourself to just one option. Apply to several different types of lenders: credit unions, online lenders, and even multiple dealerships.

Each lender has different criteria and risk assessment models. What one lender might see as too risky, another might be willing to finance. Comparison shopping can save you thousands of dollars in interest over the life of the loan.

6. Proactively Improve Your Credit Score (Even Slightly)

While a significant credit score jump takes time, there are quick wins that can help. First, obtain your free credit reports from AnnualCreditReport.com and check for errors. Dispute any inaccuracies immediately.

Second, pay down any small outstanding debts, especially those with high interest rates. Reducing your credit utilization can provide a quick boost to your score. Finally, ensure all your current payments (credit cards, utilities, rent) are made on time. A few months of perfect payment history can positively impact your score.

Where to Find a Car Loan with a 600 Credit Score

Knowing where to look is half the battle. Here are the primary sources for auto loans when you have a 600 credit score:

1. Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders, including those who specialize in subprime loans. This can be convenient, as you can often complete the purchase and financing in one place.

Pros: Convenience, "one-stop shop," some dealers have special programs for challenged credit.

Cons: May not offer the best rates, can be high-pressure sales environment, limited lender options compared to shopping independently.

2. Credit Unions

Credit unions are often more forgiving than traditional banks, especially for members. They are non-profit organizations focused on their members’ financial well-being and may offer more flexible terms and lower interest rates to those with fair credit.

Pros: Potentially lower interest rates, more personalized service, willingness to work with members.

Cons: Requires membership (though often easy to join), may have stricter lending criteria than subprime specialists.

3. Online Lenders Specializing in Bad Credit

Many online lenders have emerged specifically to cater to borrowers with fair or bad credit. They often have streamlined application processes and can provide quick approval decisions. Examples include Capital One Auto Finance, LightStream, and many others you can find with a quick search.

Pros: Quick application and approval, access to multiple lenders, convenient from home.

Cons: Less personal interaction, may require extensive documentation, potentially higher rates than credit unions.

4. Traditional Banks (With a Catch)

If you have an existing banking relationship, it’s worth inquiring with your bank. While they typically prefer higher credit scores, an established relationship might give you a slight edge. However, they may not be as flexible as credit unions or subprime specialists.

Pros: Existing relationship might help, familiar institution.

Cons: Often have stricter credit score requirements, may not specialize in subprime loans.

Understanding Loan Terms and Interest Rates

When you have a 600 credit score, understanding the terms of your loan is paramount. The biggest factor will be the interest rate.

The Impact of High Interest Rates

A higher interest rate means you’ll pay significantly more money over the life of the loan. For example, a $20,000 loan at 6% over 60 months costs less in total interest than the same loan at 12%. The difference can be thousands of dollars.

Based on my experience, never just focus on the monthly payment. Always ask for the total cost of the loan, including all interest and fees. This gives you a true picture of what you’re committing to.

Loan Term Length

You’ll also need to consider the loan term (the number of months you have to repay the loan).

- Shorter terms (e.g., 36-48 months): Higher monthly payments but less total interest paid.

- Longer terms (e.g., 72-84 months): Lower monthly payments but significantly more total interest paid and a longer period during which your car could depreciate faster than you pay it off (being "upside down").

For a 600 credit score, lenders might push for longer terms to make monthly payments seem more affordable. Be cautious, as this can lead to paying much more in the long run. Try to strike a balance between affordability and minimizing interest.

APR vs. Interest Rate

The Annual Percentage Rate (APR) is often a more comprehensive measure than just the interest rate. APR includes the interest rate plus any additional fees associated with the loan, such as origination fees. Always compare APRs when evaluating loan offers to get the true cost of borrowing.

Pro Tips for Navigating the Car Loan Process

1. Know Your Budget Before You Start

Before you even look at cars, determine how much you can truly afford for a monthly payment, insurance, fuel, and maintenance. Stick to this budget religiously. It will prevent you from getting emotionally attached to a car you can’t realistically afford.

2. Don’t Get Emotionally Attached Too Soon

It’s easy to fall in love with a car. However, getting emotionally invested before the financing is settled can lead to making impulsive decisions that are not in your best financial interest. Treat it as a business transaction first.

3. Read the Fine Print

This cannot be stressed enough. Understand every clause, every fee, and every term in your loan agreement. If something is unclear, ask for clarification. Don’t sign anything you don’t fully comprehend.

4. Be Prepared for Negotiation

Everything is negotiable – the car price, your trade-in value, and even some loan terms (within reason). Having multiple pre-approval offers gives you leverage. Don’t be afraid to walk away if the deal isn’t right for you.

5. Understand Add-ons

Dealerships often try to sell you add-ons like extended warranties, paint protection, or gap insurance. While some may be valuable, others are not. Understand what each one offers and whether it’s truly necessary for your situation. These can significantly increase your loan amount and total cost.

What to Do After Getting Approved

Securing the loan is a great first step, but your financial journey continues.

1. Make Payments On Time, Every Time

This is critical. Timely payments will help rebuild your credit score, making future borrowing easier and more affordable. Set up automatic payments if possible to avoid missing due dates.

2. Consider Refinancing in the Future

As your credit score improves (and it will if you make consistent on-time payments), you may qualify for a lower interest rate. After 12-18 months of good payment history, explore refinancing your car loan. This could save you a significant amount of money.

3. Continue Building Your Credit

Keep practicing good credit habits. Pay all your bills on time, keep credit card balances low, and regularly check your credit report. A stronger credit score opens doors to better financial opportunities in the future. For more tips on improving your credit, consider reading our article on .

Common Mistakes to Avoid

Navigating a car loan with a 600 credit score requires vigilance. Here are common mistakes to steer clear of:

- Accepting the First Offer: As discussed, comparison shopping is essential. The first offer is rarely the best.

- Not Checking Your Credit Report: Errors can unfairly lower your score. Always verify the information on your report.

- Buying More Car Than You Can Afford: Don’t let enthusiasm override financial prudence. Stick to your budget.

- Ignoring the Down Payment: A small or non-existent down payment makes your loan riskier and more expensive.

- Falling for Predatory Lending Practices: Be wary of "guaranteed approval" lenders who don’t care about your credit, as they often come with extremely high interest rates and unfavorable terms. Always verify a lender’s legitimacy and read reviews.

Conclusion: Drive Away with Confidence

The answer to "Can a 600 credit score get a car loan?" is a definitive yes, but with a strong emphasis on preparation, strategy, and diligence. While a 600 score places you in the subprime category, it doesn’t close the door to car ownership. Instead, it signals the need for a more thoughtful and proactive approach.

By understanding what lenders consider, saving for a down payment, shopping around for the best terms, and being meticulous with your loan agreement, you can secure a car loan that fits your budget and helps you rebuild your credit. Your 600 credit score is not a permanent label; it’s a starting point.

Take control of your financial journey. Arm yourself with knowledge, apply the strategies outlined here, and you’ll not only drive away in a reliable vehicle but also take a significant step towards a stronger financial future. Your journey to car ownership, even with a 600 credit score, is within reach.

Ready to take the next step? Share your experiences or questions in the comments below!

Disclaimer: This article provides general financial information and is not intended as professional financial advice. Always consult with a qualified financial advisor for personalized guidance.

External Link for Further Reading: For more detailed information on credit scores and what they mean, you can visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/

Internal Link Placeholder: