Can a 600 Credit Score Get a Car Loan? Your Expert Guide to Auto Loan Approval

Can a 600 Credit Score Get a Car Loan? Your Expert Guide to Auto Loan Approval Carloan.Guidemechanic.com

The dream of owning a reliable car is a common one, providing freedom and convenience in our daily lives. But what if your credit score hovers around the 600 mark? Many people find themselves asking, "Can a 600 credit score get a car loan?" It’s a valid and frequently asked question that often comes with a mix of hope and anxiety.

Navigating the world of auto financing can feel like a complex maze, especially when your credit isn’t perfect. A 600 credit score places you in what lenders typically categorize as "fair" or "subprime" territory. This doesn’t mean the door to car ownership is closed, but it does mean you’ll need a strategic approach and a clear understanding of what to expect.

Can a 600 Credit Score Get a Car Loan? Your Expert Guide to Auto Loan Approval

In this comprehensive guide, we’ll dive deep into the realities of securing a car loan with a 600 credit score. We’ll explore how lenders view your credit, what factors beyond your score truly matter, and most importantly, equip you with actionable strategies to boost your chances of approval and secure the best possible terms. Our goal is to empower you with the knowledge and confidence to drive away in your next vehicle, even with a less-than-perfect credit history.

Understanding Your 600 Credit Score: What It Means to Lenders

Before we answer the core question, let’s understand what a 600 credit score signifies in the eyes of potential lenders. Credit scores typically range from 300 to 850, and a 600 score falls squarely into the "fair" or "subprime" category. This isn’t considered "good" or "excellent," which usually starts around 670 and goes upwards.

From a lender’s perspective, a 600 credit score indicates a moderate to high level of risk. It suggests that you might have had some challenges managing credit in the past, such as late payments, high credit card balances, or a limited credit history. While not as high-risk as someone with a score in the 400s or 500s, it’s still a score that prompts lenders to exercise more caution.

Based on my experience working with numerous individuals seeking auto financing, lenders primarily use your credit score as a quick snapshot of your financial responsibility. A 600 score tells them that while you might be generally trying to manage your finances, there are areas where improvement is needed. This perception directly influences the interest rates and terms they are willing to offer.

The Short Answer: Yes, a 600 Credit Score Can Get a Car Loan – But With Caveats

So, to directly address the burning question: Yes, you absolutely can get a car loan with a 600 credit score. However, it’s crucial to understand that this approval often comes with specific conditions and expectations that differ significantly from those offered to borrowers with higher credit scores.

The primary caveat is that you will likely face higher interest rates compared to someone with a good or excellent credit score. Lenders compensate for the increased risk associated with a 600 score by charging more for the loan. This means your monthly payments will be higher, and the total cost of the car over the life of the loan will be considerably more.

Another important consideration is the loan terms themselves. Lenders might offer shorter or longer loan durations, or require a larger down payment to mitigate their risk. The key is to be prepared for these possibilities and to strategically position yourself to secure the most favorable terms available for your credit situation. It’s not just about getting approved; it’s about getting approved intelligently.

Key Factors Lenders Consider Beyond Your Credit Score

While your 600 credit score is a significant factor, it’s not the only piece of the puzzle. Lenders look at your overall financial picture to assess your ability and willingness to repay the loan. Understanding these additional factors can dramatically improve your chances of auto loan approval.

1. Your Debt-to-Income Ratio (DTI)

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders analyze. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For instance, if your total monthly debt payments (including rent/mortgage, credit card minimums, student loans, etc.) are $1,500 and your gross monthly income is $4,000, your DTI is 37.5%.

Lenders prefer to see a lower DTI, typically below 40-45%, as it indicates you have enough disposable income to comfortably manage new loan payments. A high DTI, even with a 600 credit score, can signal that you’re already stretched thin financially, making you a higher risk. Demonstrating a manageable DTI proves your capacity to take on additional debt.

2. Income Stability and Employment History

A steady and reliable source of income is paramount for auto loan approval. Lenders want to see proof that you have the consistent financial means to make your monthly payments. This often means providing pay stubs, tax returns, or bank statements to verify your income.

A long and stable employment history with the same employer or in the same industry is also highly valued. It suggests reliability and a reduced risk of job loss, which could impact your ability to repay the loan. If you’ve recently changed jobs, be prepared to explain the circumstances and demonstrate continuity in your earnings.

3. The Power of a Down Payment

Making a significant down payment is one of the most effective ways to strengthen your application for a car loan with a 600 credit score. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your financial commitment to the purchase.

Based on my experience, a down payment of at least 10-20% of the vehicle’s purchase price can make a substantial difference. Not only does it increase your approval odds, but it can also lead to more favorable interest rates and lower monthly payments. It shows the lender that you have skin in the game.

4. Vehicle Choice and Affordability

The type of vehicle you choose plays a direct role in your loan approval. Lenders are more likely to approve a loan for an affordable, reliable used car than for a brand-new luxury model, especially with a 600 credit score. The car’s value acts as collateral for the loan.

Choosing a car that is well within your budget and has a strong resale value makes the loan less risky for the lender. Avoid stretching your budget for a car you can barely afford, as this will only exacerbate your financial strain and could lead to missed payments down the road.

5. Having a Cosigner

Bringing a creditworthy cosigner onto your loan application can significantly improve your chances of approval and potentially secure a lower interest rate. A cosigner, typically someone with excellent credit, agrees to be equally responsible for the loan if you default.

This added layer of security dramatically reduces the risk for the lender, as they have another party to pursue for payment if you fail to meet your obligations. However, be mindful that cosigning is a serious commitment, and it can impact the cosigner’s credit if you miss payments. Always discuss the implications thoroughly before pursuing this option.

6. Specifics of Your Credit History

While your 600 score gives a general idea, lenders will look at the details. Is your score 600 because of a few old, minor blemishes that are fading? Or is it due to recent late payments, collections, or even a past bankruptcy? The recency and severity of negative marks are important.

A 600 score with a few old, minor issues is viewed differently than a 600 score with recent major delinquencies. Lenders want to see an improving trend, or at least a history that suggests stability, even if it has some past bumps.

Strategies to Boost Your Chances of Approval (and Get Better Terms)

Securing a car loan with a 600 credit score isn’t just about applying and hoping for the best. It requires a proactive and strategic approach. Here are our pro tips for maximizing your approval odds and getting the most favorable terms possible.

1. Save for a Larger Down Payment

As mentioned, a substantial down payment is your best friend when applying for a car loan with a fair credit score. Aim for at least 10-20% of the car’s purchase price, if not more. This reduces the amount you need to borrow, lowers your monthly payments, and signals financial responsibility to lenders.

Think of it this way: the less money a lender has to risk, the more comfortable they’ll be approving your application. A larger down payment can also help you avoid being "upside down" on your loan, where you owe more than the car is worth, a common mistake to avoid.

2. Improve Your Credit Score Before Applying

If you’re not in a rush, taking some time to improve your credit score can pay huge dividends. Even a small increase of 20-30 points can move you into a different risk category for lenders, potentially unlocking lower interest rates.

Pro tips from us: Focus on these key areas. Pay all your bills on time, every time, especially credit card and loan payments. Reduce your credit card balances to keep your credit utilization below 30% (ideally 10% or less). You might also consider checking your credit report for errors and disputing any inaccuracies. For a more detailed guide, check out our article on .

3. Get Pre-Approved from Multiple Lenders

Don’t wait until you’re at the dealership to think about financing. Start by getting pre-approved from several different lenders, including banks, credit unions, and online auto lenders. Pre-approval involves a "soft inquiry" on your credit, which doesn’t harm your score, and gives you a realistic idea of what loan amount and interest rate you qualify for.

Having multiple pre-approvals in hand gives you significant negotiating power at the dealership. You’ll know what a competitive offer looks like and won’t be pressured into taking the dealer’s first financing option, which may not be the best.

4. Consider a Creditworthy Cosigner

If you have a trusted family member or friend with excellent credit who is willing to cosign for you, this can be a game-changer. A cosigner can help you secure approval and significantly lower your interest rate, saving you hundreds or even thousands of dollars over the life of the loan.

However, remember the gravity of this decision. The cosigner is equally responsible for the debt. If you miss payments, their credit score will be negatively impacted, and they could be pursued for the debt. Ensure open communication and a clear understanding of the responsibilities involved.

5. Shop Around for the Best Offers

Never settle for the first loan offer you receive. Different lenders have varying criteria and risk assessments, especially for borrowers with fair credit. Compare interest rates, loan terms, and any associated fees from at least 3-5 different sources.

Look beyond just the monthly payment. A longer loan term might offer a lower monthly payment, but you’ll pay significantly more in interest over time. Focus on the total cost of the loan and choose the option that best fits your budget and long-term financial goals.

6. Choose the Right Vehicle for Your Budget

When you have a 600 credit score, it’s wise to be pragmatic about your car choice. Focus on reliable, affordable used cars rather than new vehicles or luxury models. A less expensive car means a smaller loan amount, which is easier to get approved for and reduces your overall financial burden.

Common mistakes to avoid are getting emotionally attached to an expensive vehicle that pushes your budget to its limit. Prioritize practicality and affordability. Remember, this car is a tool to get you from point A to point B and, importantly, an opportunity to rebuild your credit.

7. Gather All Necessary Documents in Advance

Be prepared when you apply for a loan. Having all your required documents ready will streamline the application process and show lenders you are organized and serious. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Bank account information

- Social Security Number

What to Expect: Interest Rates and Loan Terms with a 600 Credit Score

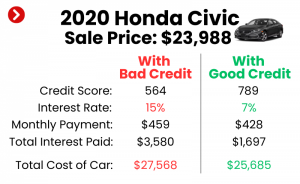

When you get a car loan with a 600 credit score, managing your expectations regarding interest rates is crucial. You will almost certainly face higher rates than borrowers with excellent credit. This is the reality of subprime auto lending.

While exact rates vary wildly based on the lender, the current economic climate, the car’s age, and other factors, you can expect rates that are often in the high single digits or even double digits. For comparison, someone with excellent credit might qualify for rates below 5%, while you might see offers of 8-15% or higher.

The impact of these higher interest rates on your total loan cost is significant. For example, on a $20,000 loan over 60 months, an 8% interest rate would cost you roughly $4,300 in interest, while a 15% rate would cost nearly $8,600. That’s a substantial difference in the total amount you pay for the car.

Lenders might also offer longer loan terms (e.g., 72 or even 84 months) to make the monthly payments seem more affordable. While this can ease the immediate burden, it significantly increases the total interest paid over the life of the loan. Pro tips from us: always try to opt for the shortest loan term you can comfortably afford to minimize interest costs.

Common Mistakes to Avoid When Seeking a Car Loan with a 600 Credit Score

Navigating the car buying process with a fair credit score can be tricky. Being aware of common pitfalls can help you avoid costly errors.

- Applying Everywhere at Once: Resist the urge to submit multiple applications to every lender you find. Each "hard inquiry" on your credit report can temporarily lower your score. Instead, use pre-qualification (soft inquiries) and then limit full applications to a few select lenders within a short timeframe (usually 14-45 days), as FICO models often count these as a single inquiry for rate shopping.

- Not Getting Pre-Approved: As discussed, skipping pre-approval means you go into the dealership blind. You lose negotiating power and might end up with less favorable terms than you could have secured elsewhere.

- Settling for the First Offer: Just because you have a 600 credit score doesn’t mean you should accept the first loan offer. Always compare offers from multiple lenders to ensure you’re getting the most competitive rate available to you.

- Buying a Car You Can’t Truly Afford: It’s easy to get excited about a new car, but overextending your budget is a recipe for financial stress. Consider not just the monthly payment, but also insurance, maintenance, fuel, and registration costs. A car is an ongoing expense.

- Ignoring the Total Cost of the Loan: Focus on the overall interest paid and the total amount repaid, not just the monthly payment. A lower monthly payment over a longer term often means paying much more in the long run.

- Not Understanding the Loan Terms: Always read the fine print. Understand the interest rate, loan term, any prepayment penalties, and late payment fees. Don’t sign anything you don’t fully comprehend.

Pro Tips for Long-Term Success After Securing Your Car Loan

Getting approved for a car loan with a 600 credit score is a significant step, but it’s also an opportunity to improve your financial standing for the future.

1. Make Payments On Time, Every Time

This is arguably the most critical step. Consistently making your car loan payments on time is one of the most effective ways to rebuild and improve your credit score. Payment history is the largest factor in your FICO score. Each on-time payment demonstrates reliability to credit bureaus and future lenders.

Set up automatic payments or calendar reminders to ensure you never miss a due date. This diligent repayment will be recorded on your credit report, gradually transforming your 600 score into something much more favorable.

2. Consider Refinancing Later

Once you’ve made 6-12 months of on-time payments and your credit score has improved, you might be a strong candidate for refinancing your auto loan. Refinancing allows you to replace your current high-interest loan with a new one that ideally has a lower interest rate.

This can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan. It’s a smart financial move that rewards your improved credit behavior. Our article on can provide more insights into how refinancing works.

3. Budget for Car Ownership Beyond the Payment

Remember that the cost of owning a car extends far beyond the monthly loan payment. You’ll need to budget for auto insurance, fuel, routine maintenance (oil changes, tire rotations), and potential repairs.

Having an emergency fund specifically for car-related expenses can prevent you from falling behind on your loan payments if an unexpected repair bill arises. Being prepared for these costs ensures your car remains a reliable asset, not a financial burden. For more information on smart car buying and ownership, you can consult trusted external resources like the Federal Trade Commission’s guide on buying a car (www.consumer.ftc.gov/articles/0055-buying-car).

Conclusion: Your Road to Auto Loan Approval with a 600 Credit Score

The answer to "Can a 600 credit score get a car loan?" is a resounding yes, but it requires strategy, patience, and realistic expectations. While you might face higher interest rates and more stringent terms initially, it is absolutely possible to secure financing for the vehicle you need.

By understanding how lenders evaluate your financial profile, preparing a robust application with a strong down payment, exploring options like a cosigner, and diligently shopping for the best loan terms, you can significantly improve your chances of approval. More importantly, this process can serve as a vital stepping stone toward rebuilding your credit and achieving greater financial stability.

Don’t let a fair credit score deter you from pursuing your transportation needs. Arm yourself with knowledge, apply these expert strategies, and take control of your car buying journey. Your future self, with a higher credit score and a reliable vehicle, will thank you. Start your journey today – smart, informed, and ready to drive forward!