Can a Cosigner Help You Get a Car Loan? Your Ultimate Guide to Driving Away with Confidence

Can a Cosigner Help You Get a Car Loan? Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Getting approved for a car loan can feel like navigating a complex maze, especially if your credit history isn’t sparkling. Many hopeful car buyers face hurdles like a low credit score, no credit history, or a high debt-to-income ratio. It’s a common scenario that can leave you wondering if your dream car will forever remain out of reach.

But what if there was a way to boost your application, increase your chances of approval, and even secure better loan terms? This is where the power of a cosigner often comes into play. A cosigner can be a game-changer, but it’s a decision that carries significant implications for everyone involved.

Can a Cosigner Help You Get a Car Loan? Your Ultimate Guide to Driving Away with Confidence

In this comprehensive guide, we’ll dive deep into whether a cosigner can truly help you get a car loan. We’ll explore the benefits, risks, and everything you need to know to make an informed decision. Our goal is to equip you with expert knowledge, helping you navigate the process with clarity and confidence.

The Core Question: Can a Cosigner Truly Help You Get a Car Loan? (And Why)

The short answer is a resounding yes, a cosigner can significantly help you get a car loan. However, understanding why and how they help is crucial to appreciating their role. A cosigner essentially adds their financial strength and creditworthiness to your loan application.

Lenders are inherently risk-averse. When you apply for a loan, they assess your likelihood of repayment based on various factors, including your credit score, income, employment stability, and existing debts. If any of these factors are weak, the lender perceives a higher risk.

How a Cosigner Bolsters Your Application

A cosigner acts as a guarantor, promising the lender that they will take full responsibility for the loan if you, the primary borrower, fail to make payments. This dual responsibility significantly reduces the lender’s perceived risk. It’s like having a safety net for the bank.

For individuals with limited credit history, a low credit score, or a high debt-to-income ratio, a cosigner can bridge this gap. They provide the confidence a lender needs to extend credit, turning a potential rejection into an approval. This support can open doors to better loan terms than you might secure on your own.

Scenarios Where a Cosigner is Most Beneficial

Based on my experience, a cosigner is particularly impactful in a few key situations:

- No Credit History: This is common for young adults or new immigrants. Without a credit history, lenders have no data to assess your repayment behavior, making you a high-risk applicant. A cosigner with established credit provides that missing link.

- Bad or Poor Credit Score: If past financial missteps have impacted your credit, a cosigner’s excellent credit score can counterbalance your weaker one. This improves your overall application profile.

- High Debt-to-Income (DTI) Ratio: Even with good credit, if a significant portion of your income is already allocated to existing debts, lenders might hesitate. A cosigner with a low DTI can help demonstrate greater collective financial capacity.

- Unstable Employment/Low Income: Lenders prefer consistent income. If your employment history is short or your income is modest, a cosigner with a stable job and solid income can strengthen your application.

Understanding the Cosigner’s Role and Responsibilities

While the benefits for the primary borrower are clear, it’s vital to fully grasp the cosigner’s role and the significant responsibilities they undertake. This isn’t just a formality; it’s a serious financial commitment.

What Exactly Does a Cosigner Do?

When someone cosigns a car loan, they aren’t just vouching for you; they are essentially signing a legally binding agreement to repay the loan if you cannot. They become equally responsible for the debt, just as if they were the primary borrower. This means their name appears on the loan agreement alongside yours.

They do not typically have ownership rights to the car, unless they are also listed on the vehicle’s title. Their primary role is purely financial: to guarantee the debt. This distinction is important to understand.

Legal Implications for the Cosigner

The legal implications for a cosigner are profound. If the primary borrower defaults on payments, the lender has the right to pursue the cosigner for the full amount of the outstanding debt, including any late fees and collection costs. This isn’t a "last resort" measure; lenders can often go after the cosigner as soon as a payment is missed.

This means the cosigner’s assets, like their savings or even their own car, could be at risk if the loan goes unpaid. They are on the hook for every penny, just as if they had taken out the loan themselves.

Impact on the Cosigner’s Credit

A cosigned loan will appear on both the primary borrower’s and the cosigner’s credit reports. As long as payments are made on time, this can positively impact both credit scores. However, if payments are missed or the loan defaults, it will negatively affect both credit scores.

Pro tips from us: A cosigned loan adds to the cosigner’s debt-to-income ratio. This could potentially impact their ability to secure new loans or lines of credit in the future, even if the primary borrower is making all payments diligently. Lenders see the cosigned loan as part of the cosigner’s financial obligations.

Benefits of Using a Cosigner for Your Car Loan

When used wisely, a cosigner can unlock several significant advantages, making your car ownership dreams a reality. These benefits extend beyond just getting approved.

1. Improved Approval Chances

This is perhaps the most obvious and immediate benefit. With a cosigner, especially one with excellent credit and a stable financial history, your loan application becomes far more attractive to lenders. Their financial strength offsets your weaknesses, making you a much lower risk.

This increased confidence from the lender can turn a "no" into a "yes," allowing you to purchase the vehicle you need. It’s particularly impactful for those who have been repeatedly denied loans due to their credit profile.

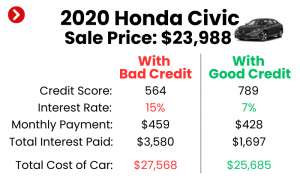

2. Potentially Lower Interest Rates

A higher perceived risk almost always translates to higher interest rates. Lenders charge more to compensate for the chance that you might default. By adding a financially strong cosigner, you significantly reduce that risk.

This reduction in risk often leads to more favorable loan terms, including a lower interest rate. Over the life of a car loan, even a small reduction in the interest rate can save you hundreds or even thousands of dollars. This makes your car more affordable in the long run.

3. Opportunity to Build Your Own Credit

One of the most valuable long-term benefits of a cosigned car loan is the opportunity it provides to build or rebuild your own credit history. As long as the payments are made on time, every month, this positive payment history will be reported to the credit bureaus under your name.

This responsible borrowing behavior is crucial for establishing a strong credit score. Over time, this improved credit can help you qualify for future loans, mortgages, or credit cards independently, without the need for a cosigner. It’s a stepping stone to financial independence.

The Risks and Downsides for Both Parties

While the benefits are compelling, it’s crucial to approach cosigning with eyes wide open to the potential risks. This isn’t a decision to be taken lightly, as it can have serious financial and relational consequences.

For the Primary Borrower (You)

- Reliance and Lost Independence: You become reliant on someone else’s good faith and credit. This can sometimes hinder your journey toward financial independence if you don’t use the opportunity to build your own credit.

- Relationship Strain: If you miss payments or default, the financial burden falls directly on your cosigner. This can severely damage your relationship, potentially beyond repair. Money matters are often the root cause of significant interpersonal conflict.

- Limited Flexibility: You might feel obligated to stay with the current loan terms or lender, even if better options arise, out of consideration for your cosigner.

For the Cosigner

- Full Financial Liability: This is the biggest risk. The cosigner is 100% responsible for the debt if the primary borrower defaults. This means the lender can pursue them for the full amount, potentially leading to lawsuits, wage garnishment, or liens on their assets.

- Credit Score Damage: Even a single missed payment by the primary borrower can negatively impact the cosigner’s credit score. A default could severely damage it, making it harder for the cosigner to obtain their own loans or credit in the future.

- Debt-to-Income Ratio Impact: The cosigned loan adds to the cosigner’s total debt load, even if they aren’t making payments. This can affect their eligibility for other loans (e.g., a mortgage) because lenders factor in all reported debts.

- Collection Calls and Stress: If the primary borrower falls behind, collection agencies will contact the cosigner, leading to significant stress and inconvenience.

- Repossession Risk: If the loan defaults and the car is repossessed, the cosigner could still be liable for any deficiency balance after the sale of the vehicle.

Common mistakes to avoid are: Not having a clear, written agreement between the primary borrower and the cosigner about payment responsibilities and communication. Many issues arise from misunderstandings, not malice.

Who Makes a Good Cosigner?

Choosing a cosigner is a critical decision that should be based on financial stability and mutual trust, not just emotional ties. Not just anyone can be an effective cosigner.

1. Excellent Credit Score

A good cosigner typically has a strong credit score, usually in the "good" to "excellent" range (700+). This is the primary factor lenders are looking for to offset your credit weaknesses. Their high score indicates a history of responsible borrowing and repayment.

Without a robust credit profile, the cosigner won’t provide the boost your application needs. Their credit history should ideally be long and clean, with no recent delinquencies or bankruptcies.

2. Stable Income and Employment

Lenders want to see that the cosigner has a reliable source of income and a stable employment history. This demonstrates their ability to make payments if the primary borrower cannot. A consistent job for several years is a strong indicator of financial stability.

Their income should also be sufficient to comfortably cover the car loan payments, in addition to their existing financial obligations. A high debt-to-income ratio for the cosigner can negate their good credit score.

3. Trust and Open Communication

This is perhaps the most overlooked, yet vital, characteristic. The relationship between the primary borrower and cosigner must be built on deep trust and open communication. Both parties need to understand the risks and responsibilities involved.

Based on my experience: It’s often best to cosign with a close family member who understands the gravity of the commitment and has a vested interest in your success. Someone you can openly discuss financial matters with, even uncomfortable ones, is essential.

4. Relationship Considerations

While a family member (parent, sibling) is a common choice, some people consider friends. However, borrowing money or involving friends in significant financial commitments can strain even the strongest friendships. Carefully consider the potential impact on your relationship if things go wrong.

A cosigner should also be someone who genuinely wants to help you succeed and is willing to accept the risks. They shouldn’t feel pressured into the role.

The Application Process with a Cosigner

Applying for a car loan with a cosigner is similar to a standard application, but with a few key differences. Being prepared can make the process much smoother.

1. Gathering Documents

Both you and your cosigner will need to provide a range of documents. This typically includes:

- Personal identification: Driver’s licenses or other government-issued IDs.

- Proof of income: Recent pay stubs, W-2 forms, or tax returns.

- Proof of residency: Utility bills or lease agreements.

- Social Security Numbers: Required for credit checks.

- Vehicle information: If you’ve already chosen a car (make, model, VIN).

Ensure all documents are current and readily available. Missing paperwork can cause delays.

2. Applying Together

Most lenders will require both the primary borrower and the cosigner to be present during the application process, either in person or virtually. Both parties will need to sign the loan agreement. This ensures that everyone fully understands and agrees to the terms and conditions.

The lender will pull both of your credit reports and assess your combined financial profile. They look at the overall picture of risk and repayment ability.

3. What Lenders Look For

When reviewing a cosigned application, lenders pay close attention to:

- The cosigner’s credit score: Is it strong enough to offset the primary borrower’s weaknesses?

- Combined debt-to-income ratio: Can the combined incomes comfortably cover the new car payment plus existing debts?

- Payment history of both individuals: While the cosigner’s is crucial, the primary borrower’s (even if limited) is still considered.

- Stability: Employment history, residency, and financial habits of both parties.

Pro Tips for a Smooth Application:

- Communicate openly: Discuss all aspects of the loan, including payment expectations, beforehand.

- Be honest: Provide accurate information on the application. Any discrepancies can lead to rejection.

- Understand the terms: Read the loan agreement carefully before signing. Ask questions about anything you don’t understand.

- Consider pre-approval: Getting pre-approved with your cosigner can give you a clear budget and strengthen your negotiating position at the dealership.

Alternatives to a Cosigner (If You Can’t Find One or Prefer Not To)

While a cosigner can be incredibly helpful, it’s not always the right path for everyone. Perhaps you can’t find a suitable cosigner, or you prefer to secure a loan independently. Fortunately, there are other strategies you can employ.

1. Saving for a Larger Down Payment

A substantial down payment immediately reduces the amount you need to borrow, which in turn lowers the lender’s risk. It shows the lender you have "skin in the game" and are serious about your financial commitment.

A larger down payment can also lead to lower monthly payments and potentially better interest rates, even if your credit isn’t perfect. This is often the most straightforward way to improve your loan prospects without external help.

2. Buying a Less Expensive Car

It might not be your dream car, but opting for a more affordable vehicle significantly reduces the loan amount. This lowers your monthly payment and makes the loan less risky for lenders.

A less expensive car can be a stepping stone. You can use it to build your credit over a few years, then trade up to your desired vehicle once your financial standing has improved. Sometimes, practical choices today lead to better opportunities tomorrow.

3. Improving Your Credit Score First

This is a long-term strategy, but it’s arguably the most empowering. Taking steps to improve your credit score before applying for a loan can open many doors. This includes:

- Paying all your bills on time, every time.

- Reducing existing debt, especially on credit cards.

- Disputing any errors on your credit report.

- Keeping old credit accounts open to maintain a long credit history.

You can check your credit report for free annually from Experian, Equifax, and TransUnion via AnnualCreditReport.com. This allows you to identify areas for improvement.

4. Exploring Secured Loans or Specific Bad Credit Lenders

Some lenders specialize in working with individuals who have less-than-perfect credit. These loans might come with higher interest rates or require collateral, but they can be an option. A secured car loan, for instance, uses the car itself as collateral. While riskier for you, it reduces the lender’s risk.

Be wary of predatory lenders with extremely high interest rates. Always compare offers and understand all terms before committing. For more insights on navigating car loans, you might find our article on Understanding Your Credit Score: A Car Buyer’s Guide helpful. (Internal Link Example)

Building Your Credit for Future Independence

Using a cosigner can be a fantastic short-term solution, but the ultimate goal should always be financial independence. A cosigned loan offers a unique opportunity to build a strong credit foundation that will serve you for years to come.

Why This is Important

Relying on a cosigner for every major purchase isn’t sustainable or ideal. Building your own robust credit profile empowers you to make financial decisions on your terms, securing better rates on mortgages, personal loans, and credit cards in the future. It’s about taking control of your financial destiny.

This journey to independence starts with understanding how credit works and actively managing your financial responsibilities. It’s an investment in your future self.

Steps to Take While on a Cosigned Loan (and Beyond)

- Make Payments On Time, Every Time: This is the golden rule of credit building. Even if your cosigner steps in, ensure your portion is paid. Consistent, on-time payments are the most significant factor in boosting your credit score.

- Monitor Your Credit Report: Regularly check your credit report for accuracy and to track your progress. You can get free credit reports annually from the three major bureaus.

- Keep Your Credit Utilization Low: If you have credit cards, try to keep your balances below 30% of your credit limit. This shows lenders you’re not over-reliant on credit.

- Consider a Secured Credit Card or Credit Builder Loan: Once you’ve managed the car loan for a while, these can be excellent tools to further diversify your credit history and accelerate your credit growth. A secured credit card requires a deposit, which becomes your credit limit, while a credit builder loan is designed specifically to help you establish a positive payment history.

- Communicate with Your Cosigner: Keep them informed about your payment status. If you anticipate a problem, discuss it with them before a payment is missed. Transparency builds trust.

Based on my experience as a financial blogger: Many individuals view a cosigned loan as a temporary solution and forget the long-term goal. Use this period to diligently improve your own financial habits. When the loan is eventually paid off, you’ll be in a much stronger position to stand on your own two financial feet. This could be your first significant step towards financial maturity. For more practical advice on managing finances, consider reading our article on Tips for First-Time Car Buyers: Navigating Your First Big Purchase. (Internal Link Example)

Conclusion: Driving Forward with Informed Decisions

So, can a cosigner help you get a car loan? Absolutely. For many, a cosigner is the key that unlocks the door to vehicle ownership, providing a crucial bridge over credit challenges and leading to more favorable loan terms. They offer their financial strength to give lenders the confidence needed to approve your application.

However, the decision to involve a cosigner is not to be taken lightly. It’s a significant financial commitment for both parties, laden with benefits but also substantial risks. Understanding the full scope of responsibilities, the potential impact on credit, and the legal implications is paramount. Open communication and mutual trust are the bedrock of any successful cosigning arrangement.

Whether you choose to pursue a car loan with a cosigner or opt for alternative strategies, remember that financial literacy is your most powerful tool. By understanding the process, mitigating risks, and proactively building your credit, you can drive away with confidence, knowing you’ve made an informed and responsible decision. Start your journey wisely, and pave your way to a stronger financial future.