Can a Teenager Get a Car Loan? Your Comprehensive Guide to Driving Off Responsibly

Can a Teenager Get a Car Loan? Your Comprehensive Guide to Driving Off Responsibly Carloan.Guidemechanic.com

The dream of owning your first car is a powerful one for many teenagers. It represents freedom, independence, and a significant step into adulthood. But as exciting as the thought of hitting the open road might be, a crucial question often arises: Can a teenager get a car loan?

The short answer is: it’s complicated, but often possible. While direct car loans for minors are rare due to legal constraints, there are clear pathways to vehicle ownership for young adults who demonstrate responsibility and have the right support system. This in-depth guide will unravel the complexities, explore the options, and provide you with expert insights to navigate the journey of financing a car as a teenager.

Can a Teenager Get a Car Loan? Your Comprehensive Guide to Driving Off Responsibly

We’ll cover everything from legal requirements and the power of a co-signer to building credit and understanding the full financial commitment. Our goal is to equip you with the knowledge to make smart, informed decisions, ensuring your first car is a step towards financial empowerment, not a burden.

The Reality Check: Legal Age and Loan Eligibility

Before diving into strategies, it’s essential to understand the fundamental legal hurdle: the age of majority. In most parts of the United States and many other countries, you must be at least 18 years old to legally enter into a contract, including a car loan agreement.

This isn’t a rule set by lenders, but by law. A minor, someone under 18, generally lacks the legal capacity to sign a binding contract. This protects young individuals from making financial commitments they might not fully understand or be able to honor. Consequently, lenders are highly reluctant, if not entirely unwilling, to issue a loan directly to a minor.

Even if a lender were to approve a loan for a minor, the contract could later be deemed voidable by the minor, leaving the lender without legal recourse. This risk is simply too high for financial institutions. Therefore, while the desire for a car might be strong at 16 or 17, the legal framework typically requires an adult’s involvement.

The Game Changer: The Power of a Co-Signer

If you’re under 18 or even a young adult with limited credit history, a co-signer is almost always the key to unlocking a car loan. This is where the dream of car ownership often becomes a reality for teenagers.

A co-signer is an individual, typically a parent, guardian, or another financially responsible adult, who agrees to share legal responsibility for the loan. By co-signing, they pledge to repay the loan if the primary borrower (the teenager) fails to do so. This significantly reduces the risk for the lender.

Based on my experience, a reliable co-signer is not just helpful; they are often indispensable for a teenager seeking a car loan. Their strong credit history and stable income provide the lender with the assurance needed to approve the application. It essentially bridges the gap between a teenager’s lack of financial history and the lender’s requirements.

Who Can Be a Co-Signer?

Ideally, a co-signer should have an excellent credit score, a stable employment history, and sufficient income to comfortably cover the loan payments if necessary. They are literally putting their own financial standing on the line for you.

Pro tips from us: Choose a co-signer who genuinely understands the commitment and is willing to support you. Open and honest communication about responsibilities is crucial from the very beginning.

Understanding the Co-Signer’s Responsibility

It’s vital for both the teenager and the co-signer to fully grasp the implications. If the teenager misses payments, the co-signer’s credit score will be negatively impacted, just as if it were their own debt. In the event of default, the lender will pursue the co-signer for the full amount owed.

Common mistakes to avoid are underestimating the co-signer’s liability or failing to discuss worst-case scenarios. A car loan with a co-signer is a shared financial commitment, and it requires trust and mutual understanding.

What Lenders Look For (Even with a Co-Signer)

While a co-signer dramatically improves a teenager’s chances, lenders still assess several factors to determine loan eligibility and interest rates. These factors reflect the overall risk of lending money.

Understanding these criteria can help you prepare and present the strongest possible application. It’s about demonstrating financial maturity and responsibility, even at a young age.

Credit Score

For most teenagers, a traditional credit score is non-existent or very limited. This is perfectly normal, as credit is built over time through responsible borrowing. Lenders, therefore, primarily rely on the co-signer’s credit score when evaluating the application.

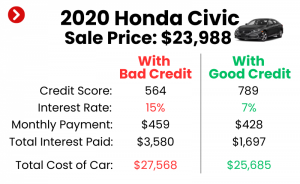

A co-signer with a strong credit history (generally FICO scores above 700) will lead to better loan terms, including lower interest rates. This is why selecting a co-signer with good credit is so important.

Income and Employment

Even with a co-signer, lenders prefer to see some indication that the teenager will contribute to or be solely responsible for the payments. Having a part-time job or any verifiable source of income demonstrates commitment and capacity to pay.

This shows responsibility and helps the lender assess the household’s ability to manage the new debt. A steady job, even if it’s entry-level, is a significant positive signal.

Debt-to-Income Ratio (DTI)

Lenders evaluate the DTI ratio, which compares your monthly debt payments to your gross monthly income. For a teenager, this will largely depend on the co-signer’s DTI. However, any existing debt the teenager might have (though unlikely) would also be considered.

A lower DTI ratio indicates that you or your co-signer have enough income left over to comfortably afford new debt. It’s a key metric for assessing repayment capacity.

Down Payment

Making a substantial down payment can significantly improve your chances of approval and lead to better loan terms. A larger down payment reduces the amount you need to borrow, thereby lowering the risk for the lender.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. This not only makes you a more attractive borrower but also reduces your monthly payments and the total interest paid over the life of the loan. Saving for a down payment is a tangible way for a teenager to demonstrate financial commitment.

Car Value and Type

The type and value of the car you wish to purchase also play a role. Lenders are often more comfortable financing newer, more reliable vehicles that hold their value well. Extremely old or high-mileage cars can be seen as higher risk due to potential maintenance issues.

This doesn’t mean you can’t get a loan for a used car, but the terms might be less favorable for a very old vehicle. Choose a car that is practical, affordable, and aligns with your financial capacity.

Building Your Financial Foundation: Steps for Teenagers

While a co-signer can open doors, proactively building your own financial foundation as a teenager is incredibly empowering. These steps will not only help you secure a car loan but also set you up for future financial success.

Financial literacy at a young age is a superpower, and these actions are concrete ways to start.

Getting a Job

One of the most impactful steps a teenager can take is getting a part-time job. Even a few hours a week demonstrate initiative, responsibility, and provides a source of income. This income can be used to save for a down payment, cover insurance, or contribute to loan payments.

Lenders view stable employment, regardless of the role, as a positive sign of your ability to manage financial obligations. It’s a tangible way to show your commitment.

Opening a Bank Account

If you don’t have one already, open a checking and savings account. This is a fundamental step in managing your money. A checking account allows for direct deposit of your paycheck and easier payment of bills.

A savings account is crucial for building your down payment fund and an emergency reserve. It teaches you the basics of financial organization.

Building Credit Responsibly

For a teenager, building a credit history can seem daunting, but it’s entirely achievable with responsible actions. This is a long-term play that pays dividends.

From a financial perspective, starting early to build credit is invaluable.

- Secured Credit Cards: These cards require a cash deposit, which becomes your credit limit. Using it responsibly (making small purchases and paying them off in full and on time) helps establish a positive payment history.

- Authorized User: A parent can add you as an authorized user on their well-managed credit card. This allows you to benefit from their good credit history, but only if they use it responsibly. Ensure clear rules are in place to prevent misuse.

- Small, Responsible Loans: Some credit unions offer "credit builder loans" designed to help individuals establish credit. You make payments into a savings account, and once paid off, the funds are released to you, along with a reporting of your payment history to credit bureaus.

Pro tips from us: Always pay your bills on time and in full. Avoid carrying a balance on credit cards, as interest can quickly accumulate.

Saving for a Down Payment

As mentioned, a down payment is a powerful tool. Start saving diligently from your job earnings, gifts, or any other income you receive. The more you put down, the less you borrow, and the more favorable your loan terms will likely be.

This demonstrates financial discipline and shows lenders you have "skin in the game." It also reduces your monthly payment, making the loan more manageable.

Budgeting

Learning to budget is perhaps the most crucial financial skill. Understand your income and meticulously track your expenses. This awareness allows you to make informed decisions about spending and saving.

Knowing where your money goes is the first step to controlling it. Use apps, spreadsheets, or even a simple notebook to manage your budget effectively.

Types of Car Loans and Where to Apply

Once you’re ready to explore financing, it’s helpful to know the different avenues available. Each has its pros and cons, and shopping around is always advisable.

Don’t settle for the first offer; competition among lenders can save you a significant amount.

Dealership Financing

Many car dealerships offer financing directly through their partnerships with various banks and financial institutions. This can be convenient, as you can often complete the purchase and financing in one place.

However, it’s essential to compare their rates with other lenders, as they might not always offer the most competitive terms. Be prepared to negotiate.

Banks and Credit Unions

Traditional banks and local credit unions are excellent places to seek a car loan. Credit unions, in particular, often offer competitive interest rates and personalized service, as they are member-owned.

Applying for pre-approval from a bank or credit union before visiting a dealership gives you leverage. You’ll know exactly how much you can afford and what interest rate you qualify for.

Online Lenders

A growing number of online lenders specialize in car loans. They often offer quick application processes and decisions. However, it’s crucial to research their reputation and terms thoroughly.

Always check for hidden fees and ensure you understand the entire loan agreement before committing. Read reviews and look for transparency.

Private Party Loans

If you’re buying a car from a private seller rather than a dealership, you’ll typically need a personal loan or a specialized private party auto loan. These can sometimes be harder to secure, especially for teenagers, and might have different terms than dealership-backed loans.

Be sure the car is thoroughly inspected by a trusted mechanic before committing to a private sale loan.

Pro tips from us: Always shop around for the best interest rates and loan terms. Get quotes from at least three different lenders before making a decision. This due diligence can save you hundreds, if not thousands, of dollars over the life of the loan.

The Application Process: What to Expect

Applying for a car loan, especially with a co-signer, involves several steps. Being prepared can make the process smoother and less stressful.

Knowledge of the process empowers you to approach it with confidence.

Gathering Documents

You and your co-signer will need to provide various documents. This typically includes:

- Government-issued identification (driver’s license or state ID)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bills, lease agreement)

- Social Security numbers

- Details about the car you intend to purchase (make, model, VIN)

Having these documents organized and ready will expedite the application.

Filling Out the Application

The application form will ask for personal and financial information for both the primary borrower and the co-signer. Be honest and accurate with all information provided. Any discrepancies could delay or jeopardize your approval.

Your co-signer will need to be present or provide their consent and information.

The Waiting Game and Understanding the Offer

Once you submit your application, lenders will review your information, pull credit reports (for the co-signer), and assess the risk. This process can take anywhere from a few hours to a few days.

If approved, you’ll receive a loan offer outlining the interest rate, loan term (length of the loan), and monthly payment amount. Carefully review every detail before signing.

Pro tips from us: Don’t hesitate to ask questions about anything you don’t understand in the loan agreement. It’s a legally binding document, and clarity is paramount.

Alternatives to a Traditional Car Loan for Teens

A traditional car loan isn’t the only path to car ownership for a teenager. Depending on your circumstances, other options might be more suitable or financially sound.

Exploring all avenues ensures you find the best fit for your situation.

Buying a Cheaper Used Car Outright

If possible, saving up enough money to buy an affordable used car with cash is often the most financially prudent choice. This avoids interest payments, monthly loan obligations, and the need for a co-signer.

While it might mean driving an older model, the freedom from debt is a significant advantage. It’s a powerful lesson in delayed gratification and financial independence.

Family Loan

Sometimes, parents or other family members might be willing to provide a personal loan. These arrangements can be more flexible, often with lower or no interest, and customized repayment schedules.

It’s crucial to treat a family loan with the same seriousness as a bank loan. Draw up a clear written agreement detailing the loan amount, repayment schedule, and any interest. This protects both parties and maintains good relationships.

Public Transportation or Ride-Sharing

In some areas, public transportation or ride-sharing services like Uber or Lyft can serve as viable alternatives, especially if car ownership isn’t an absolute necessity. Calculate the monthly cost of these options versus the total cost of car ownership (loan, insurance, fuel, maintenance).

Sometimes, it makes more financial sense to rely on these services until you are in a stronger financial position to buy a car.

Waiting and Saving More

Patience is a virtue, especially in financial matters. If a car loan feels like too much of a stretch right now, waiting a year or two, saving more, and building your credit can put you in a much better position.

This allows you to potentially secure a loan independently, with better terms, and for a car that truly meets your needs without overextending yourself.

Financial Literacy for Young Drivers: Beyond the Loan

Securing a car loan is just the first step. True financial literacy for young drivers involves understanding the entire cost of car ownership. Many teenagers, and even some adults, underestimate these ongoing expenses.

Based on my years of observing young drivers, underestimating these ongoing costs is a common pitfall. Ignoring them can quickly turn the dream of car ownership into a financial nightmare.

Insurance Costs

Car insurance for teenagers, especially young male drivers, is notoriously expensive. Due to a lack of driving experience and higher statistical risk, premiums can be significantly higher than for older, more experienced drivers.

Always get insurance quotes before committing to a car purchase. This cost alone can be a major budget item. Factors like the car’s make, model, safety features, and even color can influence premiums.

Maintenance and Fuel

Cars require regular maintenance – oil changes, tire rotations, brake checks, and occasional repairs. These costs add up over time. Fuel is another significant ongoing expense that fluctuates with gas prices and driving habits.

Budget for these essential costs. Neglecting maintenance can lead to larger, more expensive repairs down the road.

Registration and Taxes

Depending on your location, you’ll face annual vehicle registration fees and potentially property taxes on your car. These are mandatory expenses that need to be factored into your budget.

Research your local requirements to understand these recurring costs.

Emergency Fund

Unexpected repairs are an inevitable part of car ownership. A blown tire, a dead battery, or an engine light can quickly drain your wallet if you’re unprepared.

Pro tips from us: Establish an emergency fund specifically for car-related issues. Aim to have at least a few hundred dollars set aside. This fund prevents you from going into debt for unexpected repairs.

Common Mistakes Teenagers and Parents Make

Navigating the world of car loans and car ownership can be tricky. Being aware of common pitfalls can help you avoid them.

Learning from others’ mistakes is a smart way to ensure your own success.

- Not Understanding the Co-Signer’s Responsibility: Both parties must fully grasp that the co-signer is equally liable for the loan. A default affects both credit scores.

- Taking on Too Much Debt: Getting approved for a large loan doesn’t mean it’s affordable. Ensure the monthly payments (loan + insurance + fuel + maintenance) fit comfortably within your budget.

- Ignoring Insurance Costs: This is a huge one. Many teens find their insurance premiums are almost as high as their car payment. Always get a quote before buying.

- Buying a Car That’s Too Expensive to Maintain: While a luxury car might be appealing, the maintenance and repair costs can be exorbitant. Opt for reliable, affordable-to-maintain vehicles.

- Not Reading the Fine Print: Always read the entire loan agreement carefully. Understand the interest rate, term, any fees, and the total cost of the loan. Don’t be afraid to ask questions.

- Ignoring Credit Building: Even with a co-signer, proactively building your own credit is crucial for future financial independence. Don’t miss this opportunity.

- Impulse Buying: Rushing into a car purchase without research, budgeting, and shopping around often leads to regret and financial strain. Take your time.

Conclusion: Driving Off Responsibly

The question, "Can a teenager get a car loan?" doesn’t have a simple yes or no answer. While direct loans for minors are legally challenging, the path to car ownership is certainly accessible through responsible planning, the support of a co-signer, and a commitment to financial literacy.

As we’ve explored, securing a car loan as a teenager involves more than just finding a lender. It’s about demonstrating maturity, building a financial foundation, understanding the full scope of car ownership costs, and making smart, informed decisions. From getting a job and saving for a down payment to responsibly building credit and carefully budgeting for ongoing expenses like insurance and maintenance, every step contributes to your long-term financial well-being.

Whether you choose the route of a co-signed loan, opt for a family loan, or save up to buy a car outright, remember that your first vehicle is more than just transportation; it’s a significant financial responsibility. Approach this milestone with diligence, transparency, and a commitment to sound financial practices. By doing so, you’ll not only achieve the freedom of the open road but also lay a strong foundation for a lifetime of financial success.

For more in-depth advice on managing your finances as a young adult, be sure to check out our article on . Understanding interest rates is also crucial; learn more by visiting . For general financial literacy, we recommend exploring resources from the Consumer Financial Protection Bureau at .