Can I Add Someone To My Car Loan? The Ultimate Guide to Joint Car Loans, Co-Signing, and Refinancing

Can I Add Someone To My Car Loan? The Ultimate Guide to Joint Car Loans, Co-Signing, and Refinancing Carloan.Guidemechanic.com

Navigating the world of car financing can often feel like a complex journey. You’ve secured your dream car, or perhaps you’re looking to improve your existing loan terms, and a crucial question arises: Can I add someone to my car loan? This isn’t just a simple yes or no answer; it’s a decision with significant financial and legal implications for all parties involved.

As an expert blogger and professional SEO content writer, I’ve delved deep into countless financial scenarios. Based on my experience, understanding the nuances of adding a co-borrower or co-signer to an existing car loan is paramount. This comprehensive guide will equip you with the knowledge needed to make an informed decision, ensuring you understand the process, benefits, risks, and alternatives. We’ll explore everything from improving your approval chances to the long-term impact on credit scores and relationships.

Can I Add Someone To My Car Loan? The Ultimate Guide to Joint Car Loans, Co-Signing, and Refinancing

The Core Question: Can You Add Someone To Your Car Loan?

The direct answer to "Can I add someone to my car loan?" is yes, but it’s rarely a straightforward process and almost always involves a new loan agreement. You typically cannot just "add" someone to an already established car loan as if you’re adding a name to a utility bill. Loan agreements are legally binding contracts between the lender and the original borrower(s).

Lenders are risk-averse, and changing the terms of a loan, especially by adding a new party, alters their risk assessment significantly. This usually necessitates a complete re-evaluation, which most often leads to refinancing the existing loan with the new individual included. This process is crucial to understand, as it redefines the financial landscape for everyone involved.

Why Would You Even Consider Adding Someone to Your Car Loan?

People explore the option of adding someone to their car loan for various compelling reasons, primarily centered around financial improvement and shared responsibility. Understanding these motivations is the first step in determining if this path is right for your situation.

Improving Approval Chances

One of the most common reasons for adding another person is to bolster your loan application. If your credit score is less than ideal, or your income alone doesn’t quite meet a lender’s requirements, bringing in a financially stronger individual can significantly increase your chances of approval. Their good credit history and stable income act as a safety net for the lender.

This strategy is particularly effective for younger borrowers or those rebuilding their credit. It opens doors to loans that might otherwise be out of reach, helping them get on the road when they might not qualify alone.

Securing Better Interest Rates

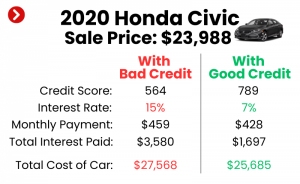

A higher credit score and a stronger overall financial profile typically translate into lower interest rates. If the person you’re adding has excellent credit, their presence on the loan can help you qualify for a much more favorable annual percentage rate (APR). Over the life of a car loan, even a percentage point or two can save you hundreds, if not thousands, of dollars.

Lower interest rates directly reduce your monthly payments and the total cost of the loan. This financial relief can make a significant difference in your budget and long-term savings.

Sharing Financial Responsibility

For couples, family members, or close partners, sharing the financial burden of a car loan can be a practical solution. When two incomes contribute to the monthly payments, it eases the strain on individual budgets and provides a buffer against unexpected financial challenges.

This shared responsibility can also foster a sense of joint ownership and accountability, which is particularly beneficial if both parties regularly use the vehicle. It’s about combining resources to manage a significant asset more effectively.

Building Credit for the New Person

Adding someone to a car loan can be an excellent opportunity for the new party to build or improve their credit history, especially if they are a co-borrower. Making timely payments on a substantial installment loan like a car loan demonstrates financial responsibility and can positively impact their credit score over time.

This can be a strategic move for young adults or those with limited credit history to establish a strong financial foundation. However, it’s a double-edged sword: missed payments will negatively affect both individuals’ credit.

Co-borrower vs. Co-signer: Understanding the Critical Distinction

Before you proceed, it’s absolutely vital to understand the difference between a co-borrower and a co-signer. While both involve adding someone to your car loan in a capacity that impacts responsibility, their legal rights and obligations differ significantly. Common mistakes to avoid are confusing these two roles, as it can lead to serious misunderstandings down the line.

What is a Co-borrower?

A co-borrower (sometimes called a joint applicant) is someone who applies for the loan with you from the outset. They are considered an equal party to the loan, sharing both the benefits and responsibilities.

- Ownership: A co-borrower typically has ownership rights to the vehicle. Their name will appear on the car’s title, signifying joint ownership.

- Responsibility: They are equally responsible for the loan payments. If one party fails to pay, the other is legally obligated to cover the full amount.

- Credit Impact: The loan activity (payments, balance) will appear on both co-borrowers’ credit reports, affecting both their scores equally.

- Access: Both parties generally have access to and use of the vehicle, though specific arrangements can be made between them.

Adding a co-borrower is like entering a financial partnership. Both individuals are on the hook for the entire debt, and both share in the asset.

What is a Co-signer?

A co-signer, on the other hand, acts as a guarantor for the loan. They agree to be legally responsible for the debt if the primary borrower defaults, but they usually do not have ownership rights to the vehicle itself.

- Ownership: A co-signer’s name typically does not appear on the car’s title. The primary borrower maintains sole ownership of the vehicle.

- Responsibility: The co-signer is secondarily responsible. They are not expected to make payments unless the primary borrower fails to do so. However, if the primary borrower defaults, the lender will pursue the co-signer for the full outstanding balance.

- Credit Impact: The loan will appear on the co-signer’s credit report, impacting their credit score based on payment history. Any late or missed payments by the primary borrower will negatively affect the co-signer’s credit.

- Access: A co-signer generally has no legal right to use or possess the vehicle.

Pro tips from us: Always clarify with your lender whether you are seeking a co-borrower or a co-signer. The distinction is not merely semantic; it has profound legal and financial consequences.

The Process: How to Add Someone to Your Car Loan (If Possible)

As established, simply "adding" someone to an existing car loan is rarely an option. The most common and viable method involves securing a new loan. This can primarily be achieved through refinancing.

Option 1: Refinancing Your Car Loan with a New Co-borrower/Co-signer

Refinancing is the process of paying off your existing car loan with a new loan, often with different terms (interest rate, payment amount, loan duration) and, in this case, a new party included. This is by far the most common and generally the only way to officially add someone to your car loan.

Understanding the Refinancing Process:

- Assess Your Current Loan: Gather all details about your existing loan: current balance, interest rate, remaining term, and payment history.

- Evaluate Both Parties’ Financials: The lender will consider the credit scores, income, and debt-to-income ratio of both you and the person you wish to add. Ensure both parties have a strong financial standing to qualify for the best rates.

- Shop Around for Lenders: Don’t just stick with your current lender. Explore options from various banks, credit unions, and online lenders. Each might offer different rates and terms based on your combined financial profile.

- Submit a Joint Application: Both individuals will need to complete a new loan application, providing all necessary financial documentation (proof of income, identification, etc.).

- Receive Loan Offers: Compare the offers you receive. Pay close attention to the interest rate, monthly payment, and total cost over the loan’s life.

- Close the New Loan: Once approved and you accept an offer, the new loan will be used to pay off your old loan. The new title will be issued reflecting the new ownership structure (if it’s a co-borrower situation), and both parties will be legally bound to the new agreement.

Option 2: Loan Modification (Less Common and Lender-Specific)

While extremely rare for adding a new party, a loan modification typically involves changing the terms of an existing loan with the original borrowers. In very specific, often hardship-related circumstances, a lender might consider modifying a loan to add a co-signer, but this is highly unusual and not a standard practice for car loans.

- Challenges: Lenders are unlikely to take on additional risk by simply adding a party to an existing contract without a full re-evaluation and a new loan. They prefer the security of a new, fully underwritten loan.

- When it might happen: If a primary borrower is facing imminent default and a co-signer is added as a last resort to prevent repossession, a lender might consider it. However, this is an exception rather than a rule.

Option 3: Selling the Car and Applying for a New Loan (Drastic Measure)

If refinancing isn’t an option or is too complex, a more drastic measure is to sell the current car, pay off the existing loan, and then apply for an entirely new car loan for a new (or even the same) vehicle with the new person as a co-borrower or co-signer. This is essentially starting fresh but comes with the hassle of selling a vehicle and potentially dealing with depreciation.

What Lenders Look For When Adding Someone to a Car Loan

When you apply for a new loan (via refinancing) with an additional party, lenders will scrutinize both individuals’ financial health. Their primary goal is to assess the combined risk.

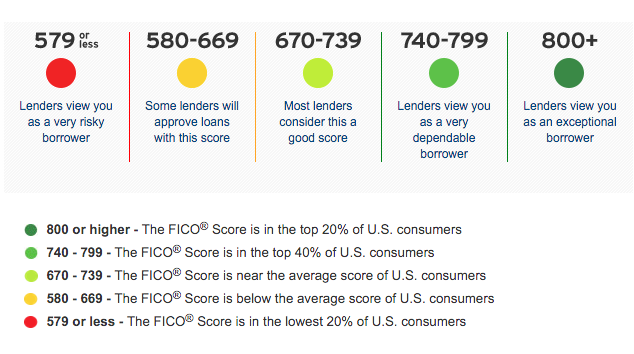

- Credit Scores: The credit scores of both the primary borrower and the person being added are paramount. A higher combined average or the presence of an excellent score will significantly improve approval chances and interest rates.

- Debt-to-Income (DTI) Ratio: Lenders calculate the percentage of your gross monthly income that goes towards debt payments. A lower DTI ratio for both parties indicates more disposable income and a lower risk of default.

- Income Stability: Lenders want to see consistent, verifiable income from both individuals. Steady employment history demonstrates the ability to make regular payments.

- Loan-to-Value (LTV) Ratio: For refinancing, the LTV compares the amount you want to borrow to the car’s current market value. If you owe significantly more than the car is worth (upside down), it can make refinancing more challenging.

- Relationship Between Parties: While not a direct financial factor, the relationship (e.g., married couple, parent-child) can sometimes be a soft factor, particularly for co-signing arrangements.

The Pros and Cons of Adding Someone to Your Car Loan: A Detailed Analysis

Making this decision requires a thorough understanding of both the potential upsides and downsides. It’s not just about getting the loan; it’s about the long-term implications for your finances and relationships.

The Pros:

- Improved Approval Odds: As discussed, a stronger combined financial profile makes you a more attractive borrower to lenders, increasing the likelihood of loan approval.

- Lower Interest Rates and Monthly Payments: With better credit and income, you can often qualify for a lower APR, which translates to reduced monthly payments and significant savings over the loan’s term.

- Shared Responsibility: For co-borrowers, the financial burden is explicitly shared, potentially making payments more manageable for both parties.

- Credit Building Opportunity: If the new person has limited credit history, being added to a car loan and making consistent, on-time payments can be an excellent way for them to establish or improve their credit score.

The Cons:

- Impact on Both Credit Scores: This is a critical point. The loan will appear on both individuals’ credit reports. If payments are missed or late, both credit scores will suffer. Even perfect payments can slightly impact credit utilization for both.

- Joint Liability (A Major Risk): Whether a co-borrower or co-signer, both parties are legally responsible for the entire loan amount. If one person stops paying, the lender will pursue the other for the full balance. This can lead to unexpected financial strain and potential legal action.

- Potential Strain on Relationships: Financial agreements, especially those with significant debt, can test even the strongest relationships. Disagreements over payments, car usage, or maintenance can lead to tension and resentment.

- Complex Process and Potential Costs: Refinancing involves paperwork, credit checks, and potentially new fees (e.g., title transfer fees, application fees). It’s not a simple administrative change.

- Difficulty in Removing Someone Later: Just as it’s hard to add someone, it’s often even harder to remove them without refinancing again or selling the vehicle. This can become a major issue if relationships sour or one party wants to move on.

Common Mistakes to Avoid When Considering Adding Someone

Based on my experience, many people rush into this decision without fully understanding the ramifications. Avoiding these common pitfalls can save you a lot of headache and financial trouble.

- Not Fully Understanding Legal Implications: Many assume a co-signer just "helps out" with credit, not realizing they are 100% responsible for the entire debt if the primary borrower defaults. Always read the fine print and understand your legal obligations.

- Underestimating Relationship Strain: Money issues are a leading cause of conflict in relationships. Don’t assume your relationship is immune to the pressures of shared debt. Open and honest communication is vital from the start.

- Not Checking Both Parties’ Credit Scores and Reports: Before applying, both individuals should pull their credit reports to identify any errors or issues. A hidden problem on one report could jeopardize the entire application or lead to higher rates.

- Ignoring Refinancing Costs and Fees: While refinancing can save money, there might be upfront costs. Factor these into your calculations to ensure the long-term savings outweigh the immediate expenses.

- Assuming It’s a Simple Process: It’s not a quick fix. It requires paperwork, credit checks, lender approval, and a new legal agreement. Treat it with the seriousness it deserves.

Pro Tips for a Smooth Process

To navigate this journey successfully, here are some expert tips to guide you.

- Open Communication is Key: Before even approaching a lender, sit down with the person you plan to add. Discuss expectations regarding payments, car usage, and what happens if financial difficulties arise. Get everything out in the open.

- Get Everything in Writing (Beyond the Loan Agreement): Create a separate, informal agreement outlining your understanding of payment responsibilities, contingency plans, and any other expectations. While not legally binding in the same way as the loan, it serves as a valuable reference.

- Shop Around for Lenders Diligently: Don’t settle for the first offer. Different lenders have different criteria and rates. Compare at least three to five offers to ensure you’re getting the best possible terms for your combined financial profile.

- Understand the "Why": Be clear about why you are adding someone. Is it for a better rate, approval, or shared responsibility? This clarity will help you evaluate if the benefits truly outweigh the risks.

- Consider Alternatives First: Before committing to joint debt, explore other options. Can you improve your own credit score over time? Can you afford a less expensive car? Sometimes, a different approach is safer.

Alternatives to Adding Someone to Your Current Loan

If the complexities and risks of adding someone to your car loan seem daunting, or if it’s simply not feasible, there are other avenues to explore.

- Improve Your Own Credit Score: Focus on strategies like paying bills on time, reducing other debts, and correcting errors on your credit report. A higher credit score can help you refinance solo or qualify for better terms on future loans.

- Personal Loan: In some cases, you might be able to secure a personal loan to pay off a portion or all of your car loan. This would be solely in your name and would consolidate debt, but interest rates can sometimes be higher than car loans.

- Sell the Car and Buy a Cheaper One: If your current car loan is a significant burden, selling the vehicle and purchasing a more affordable one could be a viable solution. This reduces your overall debt and monthly payments.

- Temporary Financial Assistance (Without Being on the Loan): The other person could simply provide you with funds to help with payments, without formally being added to the loan. This reduces their liability and keeps the car loan solely in your name.

- Debt Management Plan: If you’re struggling financially, a non-profit credit counseling agency can help you develop a debt management plan that might include negotiating with your current lender for more favorable terms on your existing loan.

What If You Want to Remove Someone From Your Car Loan Later?

Removing someone from a car loan is typically as challenging as adding them, if not more so. It almost always requires a new financial transaction.

- Refinancing (Again): This is the most common method. The remaining party (or a new single borrower) would apply for a new loan in their name only, using it to pay off the existing joint loan. This requires the remaining borrower to qualify for the loan independently.

- Selling the Vehicle: If refinancing isn’t possible, selling the car is another way to sever the financial ties. The proceeds from the sale would be used to pay off the loan, and any remaining debt or equity would be settled between the parties.

- Lender Policies: It’s extremely rare for a lender to simply remove a name from an existing loan without a new underwriting process. They are unlikely to reduce their security (i.e., fewer people responsible for the debt) without a compelling reason and a re-evaluation of risk.

Legal and Financial Implications: A Deeper Dive

Understanding the profound legal and financial ramifications is critical before making this decision. This isn’t just about a car; it’s about significant debt and long-term financial health.

- Defaulting on the Loan: If payments are not made, the loan will go into default. This negatively impacts the credit scores of all parties on the loan.

- Repossession: In the event of default, the lender has the right to repossess the vehicle. This further damages credit scores and results in the loss of the asset. Both co-borrowers or the primary borrower and co-signer would still be liable for any deficiency balance after the sale of the repossessed car.

- Impact on Future Borrowing: Having a joint car loan, or being a co-signer, increases your reported debt. This can affect your debt-to-income ratio, potentially making it harder to qualify for other loans (like a mortgage or another car loan) in the future, even if payments are always on time.

- Estate Planning: In the unfortunate event of one party’s passing, the loan obligations do not disappear. The remaining party (or their estate) would still be responsible for the full debt. It’s crucial to consider these scenarios and discuss them with all involved.

For more information on the responsibilities associated with joint accounts and co-signing, you can refer to trusted resources like the Consumer Financial Protection Bureau (CFPB) at .

Conclusion: Weighing Your Options Carefully

The question, "Can I add someone to my car loan?" opens up a complex discussion about shared financial responsibility, credit, and personal relationships. While it is possible, primarily through refinancing, it is never a decision to be taken lightly. The potential benefits—such as improved approval chances, lower interest rates, and shared responsibility—are significant. However, they come hand-in-hand with substantial risks, including joint liability, potential strain on relationships, and the long-term impact on both individuals’ credit scores.

Based on my expertise, the most important takeaway is the necessity for thorough research, open communication, and a clear understanding of the legal and financial obligations for all parties. Carefully weigh the pros and cons, explore all alternatives, and if you decide to proceed, ensure you understand every detail of the new loan agreement. Your financial future, and potentially a valued relationship, depend on making an informed and responsible choice.