Can I Apply For A Car Loan Online? Your Ultimate Guide to Seamless Digital Auto Financing

Can I Apply For A Car Loan Online? Your Ultimate Guide to Seamless Digital Auto Financing Carloan.Guidemechanic.com

The way we buy cars has evolved dramatically, and with it, the financing process. Gone are the days when securing a car loan meant endless trips to different banks and dealerships, juggling paperwork and enduring high-pressure sales tactics. Today, a powerful alternative has emerged, offering unparalleled convenience and efficiency: applying for a car loan online.

This comprehensive guide will not only answer the pivotal question, "Can I apply for a car loan online?" with a resounding "Yes!" but will also walk you through every step of the digital auto financing journey. We’ll explore the benefits, crucial preparations, the application process itself, and provide expert tips to ensure you secure the best possible deal from the comfort of your home. Get ready to navigate the modern landscape of car financing like a seasoned pro.

Can I Apply For A Car Loan Online? Your Ultimate Guide to Seamless Digital Auto Financing

The Dawn of Digital Auto Financing: Why Online is the New Standard

The internet has revolutionized nearly every aspect of our lives, and securing a car loan is no exception. For many years, the traditional route involved physically visiting lenders, filling out forms by hand, and waiting days for a decision. This cumbersome process often left car buyers feeling overwhelmed and disempowered.

Unlocking Unmatched Convenience

One of the most significant advantages of applying for a car loan online is the sheer convenience it offers. You can initiate and complete your online car loan application from anywhere, at any time—whether it’s late at night from your couch or during a lunch break at work. There’s no need to adhere to bank hours or commute through traffic. This flexibility empowers you to fit the financing process into your busy schedule seamlessly.

Speed and Efficiency at Your Fingertips

Traditional loan applications often involved a waiting game, sometimes taking days to hear back from lenders. With digital auto financing, the processing time is dramatically reduced. Many online lenders offer instant pre-approvals or quick decisions within hours, allowing you to move forward with your car purchase much faster. This accelerated timeline means you can get behind the wheel of your new vehicle sooner.

Empowered Comparison Shopping

Before the rise of online applications, comparing loan offers meant physically visiting multiple institutions, which was time-consuming and often intimidating. Now, with a few clicks, you can submit applications to several lenders simultaneously. This ease of comparison allows you to shop for the best interest rates, terms, and fees, ensuring you find a deal that truly suits your financial situation. Transparency in lending has never been more accessible.

Reduced Pressure, Clearer Decisions

Let’s face it: car dealerships can sometimes be high-pressure environments. Applying for your loan online before stepping onto a lot significantly reduces this stress. You can research, compare, and make informed decisions without feeling rushed or obligated. This allows you to focus purely on the vehicle purchase, knowing your financing is already in place.

Based on my experience, the shift to online applications has been revolutionary for car buyers. It transforms a historically daunting task into an accessible, transparent, and user-friendly process. Embracing online auto loan process means taking control of your car buying journey.

Yes, You Absolutely Can! Demystifying Online Car Loan Applications

To unequivocally answer the question: Yes, you absolutely can apply for a car loan online! This isn’t just a possibility; it’s rapidly becoming the preferred method for countless individuals seeking auto financing. The process involves leveraging secure online platforms provided by various financial institutions to submit your personal and financial information.

These platforms are designed to streamline the application, verification, and approval stages. You’ll typically fill out digital forms, upload necessary documents, and communicate with lenders electronically. This digital ecosystem encompasses a wide range of providers, from established banks and credit unions that have moved their services online to specialized online-only lenders and even financing portals directly linked to car dealerships. Each offers a unique set of terms and benefits, making it crucial to understand your options.

Before You Click ‘Apply’: Essential Preparations for Your Online Car Loan Journey

While applying online offers immense convenience, a little preparation goes a long way. Skipping these crucial preliminary steps can lead to unnecessary delays, rejections, or less favorable loan terms. Pro tips from us: Don’t skip this crucial preparatory phase. It’s the foundation of a successful online car loan application.

1. Know Your Credit Score Inside Out

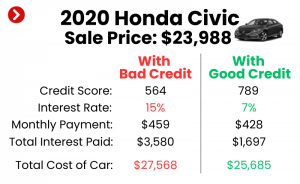

Your credit score is the single most influential factor in securing a car loan, especially online. Lenders use this three-digit number to assess your creditworthiness and determine the interest rate you’ll be offered. A higher score typically translates to lower interest rates and better terms.

Before applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your scores. Look for any errors or discrepancies that could negatively impact your rating and dispute them promptly. Understanding your credit standing allows you to set realistic expectations and potentially take steps to improve it if needed. Remember, a soft inquiry to check your score won’t impact it, unlike the hard inquiries lenders make during an actual application.

2. Master Your Budget and Down Payment Strategy

Before even thinking about a car, determine what you can realistically afford each month. Consider not just the loan payment, but also insurance, fuel, maintenance, and registration fees. Creating a detailed budget will prevent you from overextending yourself.

A significant down payment can dramatically improve your loan prospects. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan. Lenders also view a larger down payment as a sign of financial responsibility, often leading to better interest rates. Aim for at least 10-20% of the car’s purchase price if possible.

3. Gather Your Digital Document Arsenal

One of the most common delays in online applications is missing documentation. Lenders will require specific documents to verify your identity, income, and residence. Having these readily available in digital format (scanned copies or clear photos) will expedite the process.

Typically, you’ll need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (2-3 months), W-2s, tax returns (if self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Employment: Contact information for your employer.

- Banking Information: Account numbers for direct deposit or automatic payments.

- Vehicle Information: If you’ve already picked a car, details like VIN, make, model, and mileage.

Organizing these documents beforehand ensures a smooth submission process.

4. Research Reputable Online Lenders

The digital landscape is vast, with numerous online lenders vying for your business. Not all are created equal. Take the time to research different banks, credit unions, and dedicated online auto lenders. Look for institutions with positive customer reviews, transparent terms, and competitive rates. Websites like the Better Business Bureau or Trustpilot can offer insights into a lender’s reputation.

5. Embrace the Power of Pre-Approval

Obtaining pre-approval online is arguably the most strategic step you can take. A pre-approval is a conditional offer from a lender, indicating how much they are willing to lend you, at what interest rate, based on a preliminary review of your credit and finances.

This process involves a soft credit inquiry, which doesn’t harm your credit score. With a pre-approval in hand, you transform into a cash buyer at the dealership, giving you significant negotiation leverage. It also helps you stay within your budget and avoid falling for dealership financing that might not be in your best interest.

For a deeper dive into managing your financial health, you might find our article "Understanding Your Credit Score: A Comprehensive Guide" incredibly helpful.

Step-by-Step Guide: How to Apply For A Car Loan Online

Applying for a car loan online is generally straightforward, but knowing the sequence of steps can help you navigate the process confidently. Common mistakes to avoid are rushing this step or providing incomplete information.

Step 1: Choose Your Lenders Wisely

Based on your research and pre-approval efforts, select 2-3 online lenders to apply with. Applying to a handful within a short timeframe (typically 14-45 days, depending on the credit scoring model) will usually count as a single hard inquiry on your credit report, minimizing the impact. This allows you to compare actual offers without significant credit score damage.

Step 2: Fill Out the Online Application Form

Access the chosen lender’s website and locate their online car loan application. You’ll be prompted to provide detailed personal information, including your full name, address, contact details, date of birth, and Social Security Number. You’ll also need to input your employment history, income sources, and desired loan amount. Be accurate and thorough to avoid delays.

Step 3: Submit Required Documents Digitally

After completing the initial form, the lender will typically request you to upload the documents you gathered in your preparation phase. Most platforms offer secure upload portals where you can attach scanned copies or clear photos of your driver’s license, pay stubs, bank statements, and other supporting documentation. Ensure the files are legible and meet any specified format requirements.

Step 4: Await the Decision

Once your application and documents are submitted, the lender will review your information. Many online lenders boast quick car loan approval processes, sometimes providing an instant decision. For others, it might take a few hours or a couple of business days, especially if they need to verify details manually. You’ll usually receive notification via email or through the lender’s online portal.

Step 5: Review Loan Offers Carefully

If approved, you’ll receive one or more loan offers detailing the proposed interest rate (APR), loan term (e.g., 36, 48, 60 months), monthly payment, and any associated fees. This is a critical stage where you compare the offers you’ve received. Pay close attention to the Annual Percentage Rate (APR), as it represents the true cost of borrowing, including interest and some fees.

Step 6: Accept the Best Offer and Finalize

Once you’ve identified the best online car loans offer, you’ll formally accept it. This often involves an e-signature on the loan agreement. Read every line of the contract before signing. After acceptance, the lender will finalize the funding process. Depending on the lender, the funds might be directly deposited into your bank account, sent as a check, or wired directly to the dealership if you’ve already selected a vehicle. This typically happens within 1-3 business days.

Navigating the Nuances: Key Factors Lenders Consider Online

When you apply for a car loan online, lenders evaluate several key factors to assess your risk and determine your eligibility and interest rate. Understanding these elements can help you present the strongest possible application.

- Credit Score and History: As mentioned, this is paramount. Lenders look at your payment history, credit utilization, length of credit history, and types of credit accounts. A strong, consistent history of on-time payments is highly favorable.

- Debt-to-Income Ratio (DTI): Your DTI is a percentage that compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower. Most lenders prefer a DTI below 36%, though it can vary. For more on DTI, check out this informative article on Investopedia: What Is the Debt-to-Income (DTI) Ratio, and How Is It Calculated?

- Employment Stability and Income Level: Lenders want to see a stable employment history and sufficient income to comfortably cover the monthly car payments. They typically look for consistent employment for at least 1-2 years with a steady income source.

- Down Payment Amount: A larger down payment signifies a lower risk for the lender, as you have more equity in the vehicle from the start. It also reduces the loan-to-value (LTV) ratio, which is favorable.

- Vehicle Details (for Used Cars): If you’re financing a used car, the vehicle’s age, mileage, and condition can influence the loan terms. Lenders may have restrictions on financing very old or high-mileage vehicles due to depreciation and potential maintenance issues.

Pre-Approval vs. Full Application: Understanding the Difference

While often used interchangeably by some, there’s a distinct and important difference between a car loan pre-approval and a full application. Grasping this distinction is crucial for strategic car buying.

Pre-Approval: This is typically the first step. You provide basic financial information, and the lender performs a "soft inquiry" on your credit. This inquiry doesn’t affect your credit score. Based on this initial review, the lender gives you a conditional offer—an estimate of how much you can borrow and at what interest rate. A pre-approval essentially gives you a budget and buying power, allowing you to shop for cars with confidence. It’s a fantastic tool for negotiation at the dealership.

Full Application: This is the commitment phase. Once you’ve chosen a specific vehicle and are ready to finalize the purchase, you submit a full application. This involves providing all the detailed documentation (proof of income, residence, etc.) and allows the lender to perform a "hard inquiry" on your credit report. This hard inquiry can temporarily ding your credit score by a few points, but the impact is usually minimal if done within a short shopping window. The full application results in a final, binding loan offer.

The strategic advantage of pre-approval online is immense. It empowers you by separating the financing decision from the car-buying decision, giving you more control and reducing pressure.

Choosing the Best Online Car Loan: What to Look For

With multiple offers potentially on the table, how do you choose the best online car loans? It’s not just about the lowest monthly payment; a holistic view is essential.

- Interest Rates (APR): This is often the primary focus. A lower Annual Percentage Rate (APR) means you’ll pay less interest over the life of the loan. Even a seemingly small difference can save you hundreds or thousands of dollars.

- Loan Terms (Length): The loan term dictates how many months you have to repay the loan. Shorter terms (e.g., 36-48 months) mean higher monthly payments but less total interest paid. Longer terms (e.g., 72-84 months) result in lower monthly payments but significantly more interest over time. Choose a term that balances affordability with the total cost.

- Fees: Be vigilant about any hidden fees. These could include origination fees, application fees, or prepayment penalties if you decide to pay off your loan early. Reputable lenders are transparent about all costs.

- Lender Reputation and Customer Service: Research the lender’s reputation for customer service. Read reviews about their responsiveness, clarity of communication, and ease of managing the loan once approved. A good experience continues long after signing.

- Flexibility: Does the lender offer options like early payoff without penalties? Can you easily manage your account online? These small conveniences can make a big difference in your overall experience.

Common Mistakes to Avoid When Applying for a Car Loan Online

Based on years of observing car buyers, these are pitfalls we consistently see. Steering clear of these common errors will significantly improve your chances of securing a favorable auto financing online deal.

- Not Checking Your Credit Score First: Going into the application process blind is a recipe for disappointment. Always know your credit standing so you can target appropriate lenders and anticipate potential issues.

- Applying to Too Many Lenders Indiscriminately: While comparing offers is good, applying to dozens of lenders within a short period can lead to multiple hard inquiries, which can negatively impact your credit score. Stick to 2-3 reputable lenders after thorough research.

- Not Reading the Fine Print: It’s easy to skim through online agreements, but every clause matters. Understand the interest rate, terms, fees, prepayment penalties, and any other conditions before signing electronically.

- Underestimating Additional Costs: A car loan payment is only one part of car ownership. Don’t forget to budget for insurance, registration, taxes, fuel, and maintenance. These can significantly impact your overall financial comfort.

- Falling for "Guaranteed Approval" Scams: Be highly suspicious of any lender promising "guaranteed approval" regardless of credit history. These are often predatory lenders with exorbitant interest rates and hidden fees designed to trap vulnerable borrowers. Reputable lenders always conduct a credit assessment.

Is Your Online Application Secure? Addressing Privacy Concerns

In an age of increasing digital threats, it’s natural to wonder about the security of your sensitive financial information when you apply for a car loan online. Rest assured, reputable online lenders prioritize data security.

Always look for signs of a secure connection:

- HTTPS Protocol: The website address should begin with "https://" rather than "http://". The "s" indicates a secure connection.

- Padlock Icon: A padlock symbol should appear in your browser’s address bar, signifying that the connection is encrypted.

- Reputable Lender: Stick to well-known banks, credit unions, or online lenders with established reputations. They invest heavily in cybersecurity.

- Privacy Policy: Read the lender’s privacy policy to understand how they collect, use, and protect your personal data.

- Strong Passwords: Use unique, strong passwords for any online accounts you create with lenders.

Lenders use advanced encryption technologies (like SSL/TLS) to protect your data during transmission. While no system is 100% impervious, taking these precautions and choosing trusted providers significantly minimizes risks. For more general advice on safeguarding your digital footprint, consider reading "Protecting Your Personal Data Online: A Guide."

Conclusion: Embrace the Future of Car Financing

The answer to "Can I apply for a car loan online?" is a resounding and enthusiastic YES! The digital age has undeniably transformed the landscape of auto financing, making it more accessible, efficient, and transparent than ever before. From the convenience of applying anywhere, anytime, to the power of comparing multiple offers with ease, online car loan applications offer a superior experience for the modern car buyer.

By taking the time to prepare thoroughly, understanding the step-by-step process, and being aware of the factors lenders consider, you can navigate the world of digital auto financing with confidence. Avoid common pitfalls, prioritize security, and leverage the power of pre-approval to secure the best online car loans tailored to your needs.

The journey to your next vehicle doesn’t have to be stressful. By embracing the capabilities of the internet, you can secure your car loan smartly, efficiently, and on your terms. Start your online auto loan process today and drive away with confidence!