Can I Buy Two Cars With One Loan? Navigating the Complexities of Multiple Vehicle Financing

Can I Buy Two Cars With One Loan? Navigating the Complexities of Multiple Vehicle Financing Carloan.Guidemechanic.com

The allure of owning two cars can be strong, whether it’s for a growing family, a daily commuter alongside a weekend toy, or simply the convenience of having an extra vehicle. Many people naturally wonder: "Can I buy two cars with one loan?" It’s a question that delves deep into the mechanics of auto financing, credit, and risk assessment.

As an expert in auto finance and a seasoned blogger, I’ve seen firsthand the misconceptions surrounding this topic. While the idea of simplifying your financial life with a single payment for multiple assets is appealing, the reality of auto lending is often more nuanced. This comprehensive guide will explore the possibilities, highlight the challenges, and equip you with the knowledge to make informed decisions when considering financing multiple vehicles.

Can I Buy Two Cars With One Loan? Navigating the Complexities of Multiple Vehicle Financing

The Short Answer: Is It Possible? (And Why It’s Tricky)

Let’s cut straight to the chase: it is highly unlikely that you can secure a traditional, secured auto loan for two cars under a single loan agreement. Most conventional auto lenders operate on a one-loan-per-vehicle basis. Each car has a unique Vehicle Identification Number (VIN), and each auto loan is secured by that specific VIN as collateral.

This fundamental principle dictates how lenders assess risk and manage their assets. If you default on a single auto loan, the lender knows exactly which asset to repossess to recover their losses. When you introduce a second vehicle into the equation under the same secured loan, the complexity for the lender escalates significantly.

Why Lenders Prefer One Loan, One Car: The Lender’s Perspective

Understanding the lender’s viewpoint helps clarify why this rule is so pervasive. Their primary goal is to minimize risk and ensure the loan can be repaid or recovered if necessary.

Clear Collateral and Valuation

Each car represents a distinct asset with its own market value. When a loan is secured by a single vehicle, the lender has a clear understanding of the collateral’s worth. If they were to bundle two cars into one loan, they would need to accurately assess the combined value, which can fluctuate differently for each vehicle.

Furthermore, if a borrower defaults, the process of repossessing and selling two separate vehicles tied to a single loan agreement becomes administratively cumbersome. Lenders prefer straightforward processes to protect their investment.

Risk Assessment and Management

From a risk management standpoint, a single secured loan for two disparate assets is complex. What if one car is totaled but the other is fine? How does the insurance payout affect the overall loan balance and remaining collateral? These are questions that traditional auto loan structures are not designed to handle efficiently.

Based on my experience, lenders typically shy away from scenarios that introduce ambiguity in collateral and recovery procedures. They prefer to mitigate risk by keeping things simple: one loan, one VIN.

Regulatory and Legal Frameworks

The legal and regulatory frameworks surrounding auto loans are often built around the concept of a single vehicle securing a single debt. Creating a "two-car loan" would require new legal agreements and potentially different regulatory oversight, which most lenders are unwilling to pursue given the existing, well-established auto financing model.

Understanding Your Options: When One Loan Might Work (Indirectly)

While a traditional secured auto loan for two cars is generally not an option, there are indirect methods or alternative loan types that could potentially allow you to finance two vehicles with what effectively feels like a single loan from your perspective. However, these come with their own set of considerations and risks.

1. The Unsecured Personal Loan

An unsecured personal loan is perhaps the closest you’ll get to a "one loan for two cars" scenario. With this type of loan, you receive a lump sum of money directly into your bank account. You are then free to use these funds for any purpose, including purchasing two vehicles.

How it works: You apply for a personal loan for the combined amount needed for both cars. If approved, the money is yours to spend. You then pay cash for both vehicles.

Pros: Flexibility in use of funds, no collateral required (meaning your cars aren’t directly seized if you default on this loan).

Cons: Interest rates are typically much higher than secured auto loans because there’s no collateral for the lender to fall back on. Loan terms are often shorter, leading to higher monthly payments. Approval amounts might be lower, and your credit score needs to be excellent to qualify for a substantial sum at a reasonable rate.

2. Home Equity Loan or Line of Credit (HELOC)

If you own a home with substantial equity, a home equity loan or HELOC could be an option. These loans use your home as collateral, allowing you to borrow against its value.

How it works: You apply for a home equity loan or HELOC for the amount needed for both vehicles. Once approved, you receive the funds (either a lump sum for a home equity loan or a revolving credit line for a HELOC) and use them to purchase your cars.

Pros: Often offers lower interest rates than personal loans due to being secured by your home. Longer repayment terms are common, leading to lower monthly payments.

Cons: This is a significant risk. Your home is on the line. If you default, you could lose your house. The application process can be lengthy and involves closing costs. Pro tips from us: Carefully weigh the potential loss of your home against the convenience of a lower interest rate.

3. Refinancing an Existing Car Loan with Cash-Out

This scenario only applies if you already own one car and want to buy a second. If you have significant equity in your current vehicle, you might be able to refinance your existing auto loan and take out extra cash.

How it works: You refinance your current car loan for a higher amount than you currently owe. The difference is given to you as cash, which you can then use as a down payment or full payment for your second car.

Pros: You end up with one loan payment for your first car (albeit a larger one) and cash for the second.

Cons: Your first car’s loan term might extend, and you’ll likely pay more interest over time. The amount of cash you can get is limited by your existing car’s equity and the lender’s loan-to-value limits. This only provides funds for the second car, not truly combines the financing of both.

4. Business Loan (If Cars are for Business Use)

If the two vehicles are intended strictly for business purposes (e.g., a small fleet for a startup, delivery vehicles), a business loan could be an avenue. Business loans have different underwriting criteria and can sometimes accommodate financing multiple assets under a single agreement, especially if the assets are revenue-generating.

How it works: You apply for a business loan, clearly outlining the purpose of purchasing two vehicles for your company operations. The loan is tied to your business’s financial health and projections.

Pros: Tailored for business needs, potentially allowing for tax deductions.

Cons: Requires a registered business, a solid business plan, and often a personal guarantee from the business owner. Interest rates and terms vary widely.

The More Realistic Scenario: Two Loans for Two Cars

For the vast majority of individuals looking to finance two vehicles, the most common, straightforward, and often financially prudent approach is to secure two separate auto loans, one for each car.

Individual Secured Auto Loans

This is the standard model for car financing. Each vehicle you purchase will have its own dedicated loan.

How it works: You apply for a loan for Car A, and then apply for a separate loan for Car B. Each loan will be secured by its respective vehicle.

Pros:

- Clear Collateral: Each loan is directly tied to one VIN, simplifying the process for both you and the lender.

- Potentially Better Rates: Secured auto loans generally offer lower interest rates compared to unsecured personal loans because the lender has collateral.

- Easier Management: While you have two payments, each loan’s terms, interest rate, and remaining balance are distinct, which can make individual management clearer.

- Flexibility: You can choose different lenders for each car to get the best terms, or even buy one car new and one used, each with tailored financing.

Cons:

- Two Monthly Payments: You’ll have two separate loan payments to manage each month.

- Two Application Processes: You’ll go through the application and approval process twice.

- Credit Impact: Each loan application results in a hard inquiry on your credit report, and managing two loans successfully will impact your credit history.

Joint Application for Two Separate Loans

If you’re purchasing two cars with a partner, you can apply jointly for each of the two separate auto loans. This can sometimes strengthen your application by combining incomes and credit histories.

Key Factors Lenders Consider When You Apply for Any Car Loan (Especially for Multiple)

Whether you’re applying for one loan or two, lenders assess several critical factors to determine your eligibility and the interest rate you’ll receive. When you’re attempting to finance multiple vehicles, these factors become even more scrutinized.

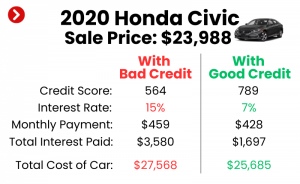

1. Credit Score

Your credit score is paramount. It’s a snapshot of your creditworthiness and your history of managing debt. A higher credit score (generally 700+) indicates lower risk to lenders, often resulting in better interest rates and more favorable terms.

For multiple loans, lenders will look at your score for each application. A strong score can help you get approved for two loans without issue, provided other factors are also strong. Common mistakes to avoid are applying for new credit cards or other loans just before applying for car loans, as this can temporarily lower your score.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio is the percentage of your gross monthly income that goes towards debt payments. Lenders use this to assess your ability to take on additional debt. A DTI ratio below 36% is generally considered excellent, though many lenders will approve applicants with a DTI up to 43-50%.

When you apply for a second car loan, your existing debt (including the first car loan, mortgage, student loans, credit cards) will be factored in. The second loan’s payment will significantly increase your DTI, potentially pushing it above a lender’s comfort threshold.

3. Income Stability

Lenders want assurance that you have a steady, reliable source of income to make your monthly payments. This usually means a consistent employment history, verified through pay stubs, W-2s, or tax returns for self-employed individuals.

Having a stable job for several years demonstrates your financial reliability, which is particularly important when taking on the financial burden of two car payments.

4. Down Payment

A substantial down payment for each vehicle is incredibly beneficial. It reduces the amount you need to borrow, thereby lowering your monthly payments and interest paid over the life of the loan. It also shows the lender you have "skin in the game" and are less likely to default.

For two cars, making a good down payment on each vehicle can significantly improve your chances of approval and secure better rates, as it lowers the loan-to-value (LTV) ratio for each car.

5. Loan-to-Value (LTV) Ratio

The LTV ratio compares the loan amount to the car’s market value. A lower LTV (meaning you’re borrowing less relative to the car’s value, usually due to a larger down payment) is always preferred by lenders.

A high LTV, especially on two separate loans, might signal higher risk. Aim for an LTV of 80% or less for each car if possible, meaning a 20% or greater down payment.

Navigating the Application Process for Multiple Vehicles

Successfully financing two cars requires careful planning and a strategic approach.

1. Preparation is Key

Before you even start looking at cars, gather all your financial documents: pay stubs, bank statements, tax returns, and details of existing debts. Knowing your financial standing upfront will save you time and potential disappointment.

2. Shop Around for Lenders

Don’t just go with the first lender you find. Different banks, credit unions, and online lenders offer varying rates and terms. Shop around for each loan independently. A credit union might offer a better rate for one car, while an online lender might be more competitive for the other.

Based on my experience, applying for multiple loans within a short period (typically 14-45 days, depending on the credit scoring model) will usually be counted as a single hard inquiry on your credit report for rate shopping purposes. This allows you to compare offers without significantly damaging your credit score.

3. Be Transparent with Lenders

When discussing your financing needs, be upfront about your intention to purchase two vehicles. While you’ll be applying for separate loans, disclosing your overall financial strategy can help lenders understand your situation and advise you appropriately.

4. Create a Realistic Budget

Before committing to two car payments, meticulously create a budget that includes all potential expenses. Factor in not just the loan payments, but also increased insurance, fuel, maintenance, and registration costs for both vehicles. A clear budget will help you determine what you can truly afford.

Financial Implications and Long-Term Considerations

Buying two cars, whether with one "effective" loan or two separate ones, has significant financial implications that extend beyond the monthly payments.

Increased Monthly Payments

This is the most obvious impact. Two car loans mean two distinct payments, which collectively represent a substantial recurring expense. Ensure your budget can comfortably absorb this without straining your finances.

Insurance Costs

Two vehicles mean two insurance policies. Your overall insurance premium will likely double or even more, depending on the vehicles, your driving record, and your location. Factor this into your monthly budget from the start.

Maintenance and Fuel

The cost of maintaining and fueling two vehicles can quickly add up. Regular servicing, unexpected repairs, and fuel consumption for two cars will be a continuous expense. Don’t underestimate these ongoing operational costs.

Depreciation

Vehicles are depreciating assets. When you buy two, you’re essentially doubling the rate at which your assets are losing value. This is a long-term financial consideration that impacts your overall net worth.

Impact on Credit

Managing two car loans successfully can actually be beneficial for your credit score over time, demonstrating responsible debt management. However, missing payments on either loan can have a devastating impact, potentially lowering your score significantly and making future credit difficult to obtain.

Alternatives to Buying Two Cars at Once (If Financing Is Too Strenuous)

If the prospect of financing two cars simultaneously seems too daunting or financially risky, consider these alternatives:

1. Leasing One, Buying One

You could lease one vehicle (often a new one with lower monthly payments than purchasing) and buy the other (perhaps a reliable used car). This can reduce the overall immediate financial burden and keep monthly outlays more manageable.

2. Buying One Used, One New

Rather than financing two new cars, consider buying one new vehicle and a reliable, pre-owned car for the second. The used car will likely have a lower purchase price and, consequently, a smaller loan amount and monthly payment.

3. Phased Purchase

If you don’t urgently need both cars at the exact same time, consider buying one now and saving up for the second. This allows you to build up a substantial down payment for the second vehicle, or even purchase it outright with cash, thereby reducing your debt burden.

4. Consider Car Sharing or Public Transport

For households that only occasionally need a second car, explore car-sharing services, ride-sharing, or utilizing public transportation. This can be a significantly more cost-effective solution than owning and maintaining a second vehicle.

Pro Tips for a Smooth Multiple Car Purchase

Based on my experience helping countless individuals with their auto financing needs, here are some pro tips to make your multiple car purchase as smooth as possible:

- Improve Your Credit Score: Before applying for any loans, take steps to boost your credit score. Pay down existing debts, check your credit report for errors, and make all payments on time. A higher score means better rates. You can find more tips on improving your credit score in our article: .

- Save a Substantial Down Payment: Aim for at least 20% down on each vehicle. This reduces your loan amount, improves your LTV, and makes you a more attractive borrower.

- Consolidate Other Debts First: If you have high-interest credit card debt or other consumer loans, consider paying them down or consolidating them before applying for car loans. This lowers your DTI and frees up cash flow.

- Know Your Budget Inside Out: Don’t just estimate. Create a detailed budget that accounts for every expense associated with both vehicles, including insurance, maintenance, and fuel, beyond just the loan payments.

- Don’t Stretch Yourself Too Thin: It’s tempting to get the cars you truly want, but financial strain can quickly turn excitement into stress. Be realistic about what you can comfortably afford long-term.

- Consider a Co-signer (If Necessary): If your credit score or DTI ratio is borderline for one or both loans, a financially strong co-signer could help you secure approval and potentially better terms. Understand the implications, as the co-signer is equally responsible for the debt.

Common Pitfalls to Avoid

Navigating a multiple car purchase can be complex. Be aware of these common mistakes:

- Ignoring Your DTI Ratio: Many applicants focus solely on their credit score. Overlooking your DTI can lead to rejection, even with good credit, especially when adding significant new debt.

- Not Factoring in All Associated Costs: Beyond the loan, insurance, registration, maintenance, and fuel can easily add hundreds of dollars per month per car. A failure to budget for these can lead to financial distress.

- Applying with Too Many Lenders at Once: While rate shopping within a short window is fine, applying indiscriminately to dozens of lenders can negatively impact your credit score, making you appear desperate for credit.

- Falling for High-Interest "Bad Credit" Loans: If your credit isn’t stellar, you might be offered loans with exorbitant interest rates. Unless absolutely necessary, explore alternatives or work on improving your credit before taking on such expensive debt.

- Overlooking the Long-Term Commitment: Car loans typically last 5-7 years. Committing to two loans means a significant portion of your income will be tied up for a long time. Ensure this aligns with your future financial goals.

Conclusion

The question "Can I buy two cars with one loan?" is largely met with a "no" in the traditional sense of secured auto financing. Lenders prefer to secure each auto loan with a single, identifiable vehicle. While alternative financing methods like unsecured personal loans or home equity loans can provide the funds to purchase two cars with a single payment, these options introduce different risks and often come with higher interest rates or collateral demands.

For most people, the most realistic and often financially sound approach is to secure two separate, individual auto loans, one for each vehicle. This allows for clear collateral, potentially better interest rates, and distinct management of each debt. Regardless of your chosen path, thorough preparation, understanding your financial health (especially your credit score and DTI ratio), and meticulous budgeting are paramount.

The journey to owning two cars can be exciting and rewarding. By understanding the intricacies of financing and making informed decisions, you can ensure that this convenience doesn’t become a financial burden. Always prioritize your long-term financial stability and choose the path that best suits your unique circumstances. For further insights into managing your finances and understanding debt, consider exploring resources from trusted institutions like the Consumer Financial Protection Bureau.