Can I Get 2 Car Loans? Navigating the Road to Multiple Vehicle Financing

Can I Get 2 Car Loans? Navigating the Road to Multiple Vehicle Financing Carloan.Guidemechanic.com

Have you ever found yourself wondering, "Can I get 2 car loans?" Perhaps your family is growing, you’ve started a side hustle that requires a separate vehicle, or you simply need a reliable second car for daily commutes. It’s a common question that many individuals and families face, and the short answer is: yes, it’s often possible, but it comes with a significant layer of complexity and crucial considerations.

Financing two vehicles simultaneously isn’t as straightforward as securing a single loan. Lenders will scrutinize your financial health much more intensely, looking for signs that you can comfortably manage the added debt without overextending yourself. This comprehensive guide will delve deep into everything you need to know about securing a second car loan, from eligibility factors and application strategies to the potential risks and smart alternatives. Our goal is to equip you with the knowledge to make an informed decision, ensuring you drive away with confidence, not regret.

Can I Get 2 Car Loans? Navigating the Road to Multiple Vehicle Financing

The Short Answer: Yes, But It’s Complicated

The simple truth is that having two car loans is not inherently prohibited. Lenders are primarily concerned with your ability to repay the debt. If your financial profile demonstrates sufficient income, a strong credit history, and a manageable debt load, they may be willing to approve you for a second vehicle.

However, this isn’t a given. It requires a robust financial standing and a clear understanding of what lenders look for. Think of it as passing a more rigorous financial stress test. While one car loan might be a manageable weight, adding a second one significantly increases your monthly financial obligations and, consequently, the perceived risk for lenders.

Key Factors Lenders Evaluate for a Second Car Loan

When you apply for any loan, lenders assess your risk profile. For a second car loan, this assessment becomes even more critical. They want assurance that you won’t default on either loan. Let’s break down the pivotal factors that will determine your eligibility.

Your Credit Score: The Ultimate Financial Report Card

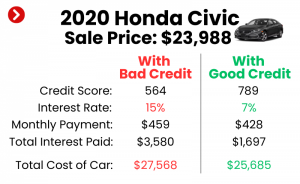

Your credit score is arguably the most influential factor in any loan application, and it plays an even more significant role when seeking a second car loan. This three-digit number provides lenders with a snapshot of your past borrowing behavior and your reliability as a borrower. A higher score signals less risk.

Based on my experience in the lending industry, a credit score of 700 or above is generally considered "good" and significantly improves your chances of approval for a second car loan. Scores in the excellent range (760+) will often unlock the most favorable interest rates and terms. Conversely, a fair or poor credit score will make securing a second loan much more challenging, and if approved, the interest rates will likely be substantially higher. Lenders see a lower score combined with existing debt as a red flag for potential overextension.

Debt-to-Income (DTI) Ratio: Your Financial Balancing Act

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders use to determine how much of your gross monthly income is consumed by debt payments. It’s calculated by dividing your total monthly debt payments (including your existing car loan, mortgage, credit cards, student loans, and the proposed new car loan) by your gross monthly income. This ratio provides a clear picture of your capacity to take on additional financial obligations.

Lenders typically prefer a DTI ratio of 36% or less, though some might go up to 43% for well-qualified borrowers. If your current DTI is already high, adding a second car loan could push it beyond an acceptable threshold, making approval very difficult. Pro tips from us: before even considering a second car loan, calculate your current DTI. If it’s approaching or exceeding 30%, focus on reducing existing debt first to improve your standing. A lower DTI demonstrates to lenders that you have ample disposable income to cover new payments.

Income Stability and Verification: A Steady Stream of Funds

Lenders need to be confident that you have a consistent and reliable source of income to make all your loan payments. They will meticulously verify your income through pay stubs, tax returns, and employment verification. Stability is key here; a long history with the same employer or a stable self-employment track record is highly favorable.

If you’re self-employed, prepare to provide more extensive documentation, such as two years of tax returns and profit and loss statements. Lenders want to see a clear pattern of consistent earnings. Any perceived instability in your income can be a major hurdle, regardless of how high your current income might be.

Payment History on Existing Loans: Your Track Record Speaks Volumes

Your payment history on your existing car loan, as well as any other loans and credit accounts, is a direct indicator of your financial responsibility. Lenders will examine this history with a fine-tooth comb. A flawless record of on-time payments on your first car loan and all other debts is paramount.

Any late payments, defaults, or collections will severely damage your chances of getting approved for a second loan. It suggests that you might struggle to manage multiple financial commitments. A strong payment history reassures lenders that you are a reliable borrower who honors their financial obligations.

Down Payment: Showing Your Commitment

While not always mandatory for a first car loan, making a substantial down payment on your second vehicle can significantly boost your approval odds. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment and ability to save.

A down payment of 10-20% is generally recommended. Not only does it make your application more attractive, but it also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early in the financing term. This financial prudence is highly regarded by lenders.

Vehicle Value and Depreciation: The Collateral’s Worth

Lenders view the car itself as collateral for the loan. They will assess the vehicle’s value, age, and potential for depreciation. Financing an older, high-mileage vehicle with a rapid depreciation rate might be more challenging than financing a newer, more reliable model. The reason is simple: if you default, the lender needs to be able to recover their losses by selling the vehicle.

A car that holds its value well offers better security for the lender. Be prepared for a thorough evaluation of the second vehicle you intend to purchase. This is less about your personal financial standing and more about the asset you are using to secure the loan.

Common Scenarios for Needing a Second Car Loan

Understanding why you might need a second car loan can help you articulate your situation to a lender and assess your own needs. There are several common scenarios that lead individuals to consider this option.

One frequent reason is growing family needs. As families expand or children become licensed drivers, a single vehicle often proves insufficient. A second car provides essential mobility for everyone.

Another scenario involves business or work-related requirements. Many professionals, freelancers, or small business owners find that a dedicated vehicle for work purposes is necessary, separating it from personal use for accounting or practical reasons.

Sometimes, people need to replace an aging primary vehicle but aren’t ready to part with their existing one, perhaps due to sentimental value or for a specific use case like hauling. They might keep the older car while financing a newer, more reliable daily driver.

Finally, some individuals might pursue a second loan for a hobby vehicle, classic car, or recreational vehicle. While this is often seen as more discretionary, if your finances are robust, it can still be a viable option. In all these cases, the financial justification and stability remain the core concern for lenders.

The Application Process for a Second Car Loan

Securing a second car loan follows a similar path to your first, but with an amplified focus on due diligence. Understanding the process can help you navigate it more smoothly.

Preparation is Key: Gather Your Documents

Before you even approach a lender, ensure you have all necessary documentation in order. This typically includes:

- Proof of income (pay stubs, W-2s, tax returns for the last two years).

- Proof of residence (utility bills, lease agreement).

- Identification (driver’s license, social security card).

- Information on your existing car loan (account number, current balance, monthly payment).

- Details about the second vehicle you intend to purchase (make, model, VIN, estimated price).

Having these documents readily available demonstrates your seriousness and preparedness, streamlining the application process significantly. It shows lenders you are organized and ready to provide transparency.

Shopping Around for Lenders: Don’t Settle for the First Offer

Just as with your first car loan, it’s crucial to shop around and compare offers from multiple lenders. Don’t assume your current lender will offer the best terms for your second loan. Banks, credit unions, and online lenders each have different lending criteria and rates. Credit unions, in particular, often offer competitive rates to their members.

To learn more about comparing lenders effectively, check out our guide on . Comparing offers allows you to find the most favorable interest rates, repayment terms, and overall loan conditions, potentially saving you a substantial amount of money over the life of the loan.

Understanding Loan Terms: Beyond the Monthly Payment

When reviewing loan offers, look beyond just the monthly payment. Pay close attention to the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing. Also, consider the loan duration. While a longer term might mean lower monthly payments, it also means you’ll pay more interest over time.

It’s vital to understand any prepayment penalties, which are fees charged if you pay off your loan early. Ensure the terms align with your financial goals and your ability to comfortably manage the payments without strain. Don’t rush this step; clarity here can prevent future financial headaches.

Applying and What to Expect: Soft vs. Hard Inquiries

When you apply for a car loan, lenders will typically perform a credit check. Initially, some lenders may conduct a "soft inquiry," which doesn’t affect your credit score. However, when you submit a formal application, a "hard inquiry" will be placed on your credit report. This can temporarily lower your score by a few points.

It’s important to know that multiple hard inquiries for the same type of loan within a short period (usually 14-45 days, depending on the credit scoring model) are often treated as a single inquiry. This means you can shop around for the best rates without unduly harming your credit score. Be transparent with lenders about your existing loan and your financial situation.

Strategies to Increase Your Chances of Approval

If you’re determined to get a second car loan, there are proactive steps you can take to strengthen your application and present yourself as a low-risk borrower.

Improve Your Credit Score

Even a small improvement in your credit score can make a difference. Before applying, focus on paying all your bills on time, reducing credit card balances, and checking your credit report for any errors. A higher score directly translates to better loan terms and a greater likelihood of approval.

Consistency in responsible credit management over several months can yield significant improvements. This isn’t a quick fix, but a sustained effort can dramatically enhance your financial profile.

Reduce Existing Debt

Lowering your existing debt, especially high-interest credit card debt, can significantly improve your DTI ratio. This demonstrates to lenders that you are not overleveraged and have more disposable income available for a new car payment. Prioritize paying down smaller debts or those with the highest interest rates.

Even if you can’t eliminate debts entirely, showing a concerted effort to reduce them can be viewed favorably. It reflects a proactive approach to managing your finances responsibly.

Increase Your Down Payment

As mentioned earlier, a larger down payment reduces the amount you need to borrow and signals your financial commitment. If possible, save up a substantial down payment for your second vehicle. This reduces the lender’s risk and can potentially lead to better loan terms.

Think of it as an investment in your own financial future. The more you put down upfront, the less you finance, which means less interest paid over time and a stronger financial position from the start.

Consider a Co-signer

If your credit isn’t perfect or your DTI is borderline, a co-signer with excellent credit and a stable income can significantly improve your chances of approval. A co-signer essentially guarantees the loan, taking on legal responsibility if you fail to make payments.

However, this comes with risks for the co-signer, as their credit will be affected if you default. Choose a co-signer carefully and ensure both parties fully understand the implications. This isn’t a decision to be taken lightly by either party.

Opt for a Less Expensive Second Vehicle

Choosing a more affordable second car can make a huge difference in your loan application. A lower purchase price means a smaller loan amount, which translates to lower monthly payments and a reduced impact on your DTI ratio. This makes you a less risky borrower in the eyes of lenders.

Sometimes, the ideal second car is one that meets your needs practically, rather than fulfilling a desire for luxury. Prioritize functionality and affordability to enhance your approval prospects.

Refinance Your First Loan (If Beneficial)

If you have an existing car loan with a high interest rate, refinancing it could potentially free up some monthly cash flow, making it easier to qualify for a second loan. A lower monthly payment on your first car can improve your DTI ratio and demonstrate better financial management.

If you’re considering refinancing, our article on offers detailed insights into whether it’s the right move for your situation. This strategy is about optimizing your current financial commitments to create room for new ones.

The Risks and Downsides of Taking on Two Car Loans

While getting a second car loan is possible, it’s crucial to understand the potential risks and downsides. This isn’t a decision to be made lightly, as it significantly increases your financial burden.

The most obvious risk is an increased financial burden. You’ll have two monthly car payments, two insurance premiums, and double the maintenance and fuel costs. This can quickly strain your budget, leaving less money for other necessities or savings.

This added financial pressure can also have a significant impact on other financial goals. Saving for a down payment on a house, contributing to retirement, or building an emergency fund might become much more challenging. Every dollar allocated to a second car loan is a dollar not going towards your long-term financial security.

There’s also the potential for negative equity on one or both vehicles. Cars depreciate rapidly, and if you owe more than your car is worth, selling it or trading it in becomes problematic. Having two cars in negative equity could trap you in a cycle of debt.

Common mistakes to avoid are underestimating the total cost of ownership for a second vehicle. People often forget to factor in the increased insurance premiums, registration fees, maintenance costs, and fuel expenses that come with an additional car. These "hidden" costs can quickly add up, turning an affordable monthly payment into a significant financial drain. Always budget for these additional expenses beyond the loan payment itself.

Alternatives to Getting a Second Car Loan

Before committing to a second car loan, explore alternatives that might better suit your needs and financial situation. Sometimes, a different approach can provide the flexibility you need without the added debt.

Public transportation can be a viable option in many urban areas, reducing the need for a second car entirely. It saves on fuel, insurance, and maintenance costs.

Ride-sharing services and carpooling offer convenient, on-demand transportation without the burden of ownership. For occasional use, this can be far more cost-effective than a second vehicle.

Consider selling your first car and buying one that fits all your needs. If your current car no longer serves your purpose, consolidating into a single, more suitable vehicle might be a smarter financial move. This simplifies your finances and reduces overall expenses.

Leasing a second vehicle, rather than buying, could be an option if you only need a car for a specific period or prefer lower monthly payments without the commitment of ownership. However, be aware of mileage restrictions and end-of-lease fees.

Finally, while not always recommended due to higher interest rates, a personal loan could be a very short-term alternative for a very inexpensive second car, but caution is advised due to less favorable terms compared to secured auto loans. Always weigh the pros and cons carefully.

Expert Insights and Final Considerations

Ultimately, the decision to pursue a second car loan boils down to a thorough and honest assessment of your financial health. Based on my experience, the key isn’t just whether you can get approved, but whether you should. Lenders assess risk; you need to assess affordability and long-term impact.

When does it make sense? If you have a stable, high income, excellent credit, a low DTI, and a clear, legitimate need for a second vehicle, then it can be a financially sound decision. This is especially true if the second car is essential for work or family logistics and fits comfortably within your budget without compromising other financial goals.

When doesn’t it make sense? If your budget is already tight, your credit score is struggling, or you’d be stretching your finances thin, then taking on a second car loan is likely a risky move. It could lead to financial stress, missed payments, and damage to your credit score, making future borrowing even harder.

Remember, responsible borrowing means ensuring you can comfortably afford all aspects of car ownership – not just the loan payment. This includes insurance, fuel, maintenance, and registration for both vehicles. For more detailed information on managing your debt-to-income ratio, you can refer to resources like the Consumer Financial Protection Bureau, which offers valuable guidance on financial wellness.

Conclusion: Drive Smart, Not Just Twice

Navigating the path to securing two car loans requires careful planning, diligent financial management, and a realistic outlook. While it’s certainly possible to finance two vehicles, the ultimate success and sustainability depend entirely on your individual financial circumstances. You must demonstrate to lenders, and more importantly, to yourself, that you have the robust income, excellent credit, and disciplined spending habits required to comfortably manage this significant financial commitment.

Before you apply, take the time to improve your credit, reduce existing debt, and build a substantial down payment. Explore all alternatives, and critically assess whether a second car loan aligns with your broader financial goals. By approaching this decision with prudence and a comprehensive understanding of all factors involved, you can make a choice that supports your lifestyle without jeopardizing your financial well-being. Drive smart, plan wisely, and ensure your journey on the road of multiple car ownership is a smooth and sustainable one.