Can I Get A Car Loan At 17? Navigating the Road to Automotive Independence as a Minor

Can I Get A Car Loan At 17? Navigating the Road to Automotive Independence as a Minor Carloan.Guidemechanic.com

The dream of owning your first car is a powerful one, especially when you’re 17. The freedom of the open road, the independence of driving yourself, and the ability to work or explore without relying on others can feel incredibly liberating. However, as an aspiring young driver, you might quickly run into a significant roadblock when trying to secure financing: your age. The question, "Can I get a car loan at 17?" is a common one, and the short answer is usually "not directly."

This isn’t to say it’s impossible, but the path requires understanding legalities, financial realities, and strategic planning. As an expert blogger and professional SEO content writer, I’ve seen countless young individuals grapple with this exact challenge. This comprehensive guide will delve deep into why obtaining a car loan as a minor is complex, explore the viable solutions, and provide you with actionable insights to help you navigate this crucial step towards automotive independence. We’ll cover everything from legal requirements to smart financial moves, ensuring you’re well-equipped for the journey ahead.

Can I Get A Car Loan At 17? Navigating the Road to Automotive Independence as a Minor

The Legal Landscape: Why 17 is a Hurdle for Car Loans

The primary reason a 17-year-old typically cannot get a car loan independently boils down to a fundamental legal principle: contractual capacity. In most jurisdictions, individuals must be at least 18 years old to enter into a legally binding contract. This isn’t just a banking rule; it’s a protection enshrined in law.

When you take out a car loan, you are essentially signing a contract with a lender. This contract obligates you to repay a specific sum of money, with interest, over a set period. If a minor could freely enter such agreements, they could potentially be exploited or make financial decisions they aren’t fully prepared for. The law, therefore, considers minors to lack the full "capacity" to understand and uphold the terms of such significant financial agreements.

Based on my experience in the financial landscape, lenders are inherently risk-averse. Loaning money to someone who can legally void the contract at any time presents an unacceptable level of risk for them. If a 17-year-old were to default on a loan, the lender would have very limited legal recourse to recover their money, as the contract itself could be deemed unenforceable. This protection is designed to shield young people, but it also creates a significant barrier when you’re eager to finance a vehicle.

The "Impossible" Made Possible: Pathways for 17-Year-Olds

While direct, independent car loans are off the table for 17-year-olds, there are definitive, well-established pathways that can make car ownership and financing a reality. These solutions almost always involve the support of a financially mature adult. Understanding these options is your first step toward getting behind the wheel.

1. The Power of a Co-Signer: Your Strongest Ally

By far the most common and effective method for a 17-year-old to secure a car loan is through a co-signer. A co-signer is typically a parent, guardian, or another financially stable adult who agrees to share legal responsibility for the loan. Their involvement bridges the gap of your age and lack of credit history.

Who can be a co-signer? Generally, a co-signer needs to be at least 18 years old (or 21 in some states for certain types of loans) with a strong credit history and a stable income. This adult essentially promises the lender that if you, the primary borrower, fail to make payments, they will step in and fulfill that obligation. Their financial standing and creditworthiness are what lenders primarily evaluate when considering the loan application.

What does a co-signer do? A co-signer doesn’t just vouch for you; they become equally responsible for the debt. This means their credit score can be affected if payments are missed, and they are legally bound to repay the entire loan amount if you cannot. For the minor, this means increased chances of loan approval and often access to better interest rates, as the lender perceives less risk.

Pro tips from us: Choosing a co-signer should be a serious, mutual decision. Both parties need to understand the responsibilities and potential risks involved. Have open, honest conversations about financial expectations, payment schedules, and what happens if circumstances change. A co-signer is giving you a significant financial gift, and treating that responsibility with the utmost seriousness is paramount.

2. Joint Application: Shared Ownership and Responsibility

Similar to co-signing, a joint application involves two or more individuals applying for a loan together, with both names on the loan and potentially the car title. In this scenario, both applicants are considered primary borrowers, sharing equal rights and responsibilities for the loan and the vehicle. This differs slightly from a co-signer, who is usually secondary on the title and primarily responsible for payment only if the main borrower defaults.

A joint application might be an option if, for example, a parent intends to share the car’s use and expenses with their 17-year-old. Both parties’ incomes and credit histories would be considered, but crucially, the 17-year-old’s name on the loan would still likely require a parent or guardian to be the primary applicant due to age restrictions on contractual capacity. This option solidifies shared ownership and financial accountability from the outset.

3. Emancipation: An Unlikely but Legal Path

Emancipation is a legal process where a minor is declared an adult by a court, granting them the same legal rights and responsibilities as someone 18 or older. An emancipated minor can enter into contracts, live independently, and manage their finances without parental consent. While this would technically allow a 17-year-old to get a car loan independently, it’s an extremely rare and complex path.

The process of emancipation typically requires demonstrating financial independence, living separately from parents, and proving that it’s in the minor’s best interest. It’s usually pursued in cases of severe family conflict or unique circumstances, not simply to obtain a car loan. For the vast majority of 17-year-olds, pursuing emancipation solely for a car loan is not a practical or recommended solution.

Preparing for Your First Car Loan (Even with a Co-Signer)

Even with a co-signer, you, as the 17-year-old, play a critical role in the success of your car loan application and your financial future. This is an excellent opportunity to build a strong foundation of financial literacy and responsibility. Lenders, and your co-signer, will appreciate your proactive approach.

1. Financial Literacy at 17: Understanding Your Money

This is where true independence begins. Before even thinking about a car loan, take the time to understand basic financial principles. This includes budgeting, understanding the difference between wants and needs, and tracking your income versus expenses.

Pro tips from us: Start by creating a simple budget. List all your income sources (part-time job, allowances) and all your regular expenses (phone bill, entertainment, savings). Seeing where your money goes is the first step to controlling it. Learning to manage money now will serve you well for the rest of your life.

2. Building a Financial Foundation: Small Steps, Big Impact

While you can’t build a robust credit history at 17, you can start laying the groundwork. This demonstrates responsibility to a potential co-signer and helps you prepare for when you turn 18.

- Secured Credit Cards (with parental guidance): Some banks offer secured credit cards where you put down a deposit equal to your credit limit. With a parent’s help and supervision, you can use this responsibly to make small purchases and pay them off in full each month, showing good payment habits.

- Authorized User on a Parent’s Card: If a parent adds you as an authorized user on their well-managed credit card, their positive payment history might reflect positively on your budding credit report. However, this is not guaranteed to build your own credit and should be approached with caution to avoid debt.

- Consistent Employment: Holding a steady part-time job, even if it’s just a few hours a week, shows responsibility and provides a verifiable income source. This looks good to lenders and proves your commitment to earning and contributing.

3. Researching Car Options: Beyond the Flashy Exterior

The excitement of getting a car can sometimes overshadow the practicalities. As a young driver, your focus should be on reliability, affordability, and safety. Flashy, high-performance cars come with significantly higher insurance premiums and maintenance costs, which can quickly become overwhelming.

Common mistakes to avoid are: falling in love with a car that’s beyond your means. Remember, the purchase price is just one part of car ownership. Research affordable, reliable used vehicles. Look for models known for their longevity and lower insurance rates. This practical approach will save you a lot of stress and money in the long run.

The Application Process: What to Expect

Once you’ve done your homework and found a willing co-signer, the actual application process for a car loan will involve several steps. Being prepared will make it smoother and more efficient.

- Gathering Documents: You and your co-signer will need to provide various documents. This typically includes government-issued IDs, proof of income (pay stubs, tax returns), proof of residence, and potentially bank statements. Having these ready will streamline the process.

- Visiting Dealerships/Lenders: Explore different financing options. You can apply for a loan directly through a dealership or pre-qualify with banks, credit unions, or online lenders. Pre-qualification can give you leverage when negotiating at the dealership.

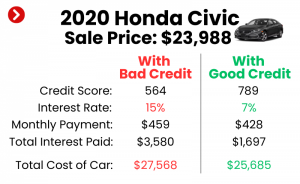

- Understanding Loan Terms: This is crucial. Don’t just look at the monthly payment. Pay close attention to the Annual Percentage Rate (APR), the loan term (how many months you have to pay it back), and the total amount you will pay over the life of the loan. A longer loan term might mean lower monthly payments but will almost always result in paying more in interest overall.

- Common mistakes to avoid during application are: rushing through paperwork, not asking questions about terms you don’t understand, and not comparing offers from multiple lenders. Always read the fine print carefully, especially regarding any fees or penalties.

Beyond the Loan: The True Cost of Car Ownership for Young Drivers

Securing the loan is a significant achievement, but it’s just the beginning. The true cost of car ownership extends far beyond the monthly payment, especially for young drivers. Ignoring these additional expenses is a common pitfall that can quickly lead to financial strain.

1. Insurance Nightmares (and how to mitigate them)

This is perhaps the biggest financial shock for most young drivers. Car insurance premiums for 17-year-olds are notoriously high. Why? Statistically, young, inexperienced drivers are involved in more accidents, making them a higher risk for insurance companies.

Pro tips from us: Don’t let this deter you, but be prepared. Research insurance costs before you buy the car. Tips for lowering costs include:

- Adding you to a parent’s policy: This is usually cheaper than a standalone policy.

- Good student discounts: Many insurers offer discounts for maintaining a high GPA.

- Defensive driving courses: Completing approved courses can sometimes lead to discounts.

- Choosing a safer, older car: Newer, more expensive, or high-performance cars will have significantly higher premiums.

- Consider higher deductibles: This lowers premiums but means you pay more out-of-pocket if you make a claim.

2. Maintenance & Fuel: Ongoing Expenses

Cars need regular maintenance to run safely and efficiently. This includes oil changes, tire rotations, brake checks, and more. Fuel costs can also add up quickly, especially if you have a long commute or drive frequently. Budgeting for these ongoing expenses is just as important as budgeting for your loan payment.

3. Unexpected Repairs: The Emergency Fund Importance

Even the most reliable car can break down. A flat tire, a dead battery, or a more serious mechanical issue can result in hundreds, if not thousands, of dollars in unexpected repair costs. Having an emergency fund specifically for car repairs is crucial. It prevents you from going into debt or having to rely on your co-signer for unexpected expenses.

Pro Tips from an Expert Blogger

Based on my experience observing financial journeys, the most successful young drivers are those who approach car ownership with a mindset of responsibility and long-term planning.

- Prioritize Financial Planning: Don’t just focus on getting the loan; focus on managing your finances responsibly after you get it. This period of shared responsibility with a co-signer is an invaluable training ground for future financial independence.

- The Long-Term Benefits of Starting Early: Successfully managing a car loan (with a co-signer) can be a fantastic way to begin building a positive credit history. When you turn 18, and especially when you’re older, this established history will be incredibly beneficial for future loans (like a mortgage) or credit card applications.

- Don’t Rush the Process: It’s tempting to want a car immediately, but patience and thorough preparation will lead to a better outcome. Rushing often leads to poor financial decisions, higher costs, and potential strain on relationships with co-signers.

- Consider Alternatives: If a loan seems too daunting, consider saving up for a reliable used car you can buy outright. This eliminates interest payments and the need for a co-signer, giving you complete financial control. Alternatively, discuss with your parents if they are willing to help you buy a car without a formal loan, perhaps with a structured repayment plan to them.

Common Mistakes to Avoid

Navigating your first major financial commitment requires vigilance. Here are common pitfalls 17-year-olds (and their co-signers) should actively avoid:

- Not Understanding the Full Cost: As discussed, the purchase price and loan payment are only part of the equation. Insurance, fuel, maintenance, and potential repairs add significantly to the monthly burden.

- Over-Borrowing: Don’t get a loan for more car than you genuinely need or can afford. It’s easy to get carried away at the dealership, but an expensive car means higher payments, higher insurance, and more depreciation.

- Ignoring Insurance Costs: This cannot be stressed enough. Get insurance quotes for specific vehicles before you commit to a purchase.

- Not Reading the Fine Print: Whether it’s the loan agreement or the insurance policy, always read every detail. If you don’t understand something, ask for clarification.

- Putting a Co-Signer at Undue Risk: Remember, your co-signer is putting their financial reputation on the line for you. Be transparent, communicate regularly, and prioritize making all payments on time to protect their credit. This responsibility also means not overextending them with a loan amount they aren’t comfortable with.

For more information on understanding consumer contracts and your rights, especially concerning minors, you can refer to trusted resources like the Consumer Financial Protection Bureau (CFPB) or similar government financial literacy sites.

Conclusion: Driving Towards Responsible Independence

While getting a car loan at 17 presents unique challenges due to legal age restrictions, it is absolutely achievable with the right strategy and support. The key lies in understanding the legal framework, leveraging the power of a co-signer, and committing to financial responsibility. This journey is not just about getting a car; it’s about taking your first significant steps towards financial independence, building good habits, and proving your capability to manage adult responsibilities.

By carefully planning, budgeting, and making informed decisions, you can navigate the road to car ownership successfully. Remember to openly communicate with your co-signer, understand all the costs involved, and view this experience as an invaluable lesson in financial literacy. The freedom of the open road awaits, but it’s best enjoyed when you’re driving with confidence and a solid financial plan. What are your biggest concerns about getting a car loan at 17? Share your thoughts in the comments below!