Can I Get a Car Loan on SSI? Your Ultimate Guide to Driving Away with Confidence

Can I Get a Car Loan on SSI? Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

For many individuals receiving Supplemental Security Income (SSI), the thought of securing a car loan can feel like an uphill battle. The need for reliable transportation is often crucial for appointments, groceries, and maintaining independence, yet the perception of a fixed income can deter potential lenders. You might be wondering, "Can I really get a car loan on SSI?"

The answer, definitively, is yes. While it presents unique challenges, obtaining a car loan while on SSI is absolutely achievable with the right knowledge, preparation, and strategy. As expert bloggers and professional SEO content writers, we’re here to guide you through every step of this journey. This comprehensive article will not only explain how but also provide invaluable insights, drawing from our experience to help you navigate the process successfully and confidently.

Can I Get a Car Loan on SSI? Your Ultimate Guide to Driving Away with Confidence

Understanding SSI and Its Role in Car Loan Applications

Before diving into the specifics of car loans, let’s clarify what SSI entails. Supplemental Security Income (SSI) is a federal program that provides monthly payments to adults and children with disabilities or blindness who have limited income and resources. It’s designed to meet basic needs, offering a crucial safety net for many.

From a lender’s perspective, SSI is considered a form of verifiable, stable income. This is a critical point often misunderstood. While it might be a fixed amount, its reliability can be an advantage. The challenge often lies in the amount of income and how it relates to the cost of a loan, rather than the source itself.

Lenders primarily assess risk. They want assurance that you can consistently make your monthly payments. Your SSI income, combined with other financial factors, will be the basis for this assessment. Understanding this foundational principle is your first step towards securing a car loan.

Key Factors Lenders Evaluate When You Apply for a Car Loan

When you apply for any loan, lenders look at several key indicators to gauge your financial health and ability to repay. For SSI recipients, these factors become even more crucial. Based on my experience in financial guidance, focusing on these areas will significantly strengthen your application.

Your Credit Score: A Financial Report Card

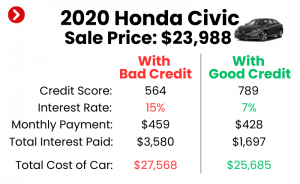

Your credit score is a three-digit number that summarizes your creditworthiness. It’s derived from your credit history, including how reliably you’ve paid past debts, the types of credit you’ve had, and how much credit you currently use. A higher score indicates lower risk to lenders.

For many SSI recipients, building or maintaining a strong credit history can be challenging. However, it’s not impossible, and even a modest score can open doors. Lenders use this score to determine not only whether to approve your loan but also the interest rate they’ll offer.

Pro tips from us: Start by checking your credit score and report from all three major bureaus (Experian, Equifax, and TransUnion). You are entitled to a free report from each annually via AnnualCreditReport.com. Review it for errors and understand your current standing.

Debt-to-Income (DTI) Ratio: Your Financial Balance

Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage monthly payments and take on additional debt. A lower DTI indicates you have more disposable income available to cover new loan payments.

For instance, if your SSI provides $1,000 per month, and you have $300 in other debt payments (like credit cards or personal loans), your DTI is 30%. Lenders generally prefer a DTI below 40%, though this can vary. For those on SSI, keeping this ratio as low as possible is paramount.

To calculate your DTI, sum all your monthly debt payments and divide that by your gross monthly income. Reducing existing debts before applying for a car loan can significantly improve this ratio and your chances of approval. This demonstrates financial responsibility and capacity.

The Power of a Down Payment

A down payment is a sum of money you pay upfront for the car, reducing the amount you need to borrow. This is a powerful tool, especially when applying for a car loan on SSI. A substantial down payment signals to lenders that you are serious about the purchase and have some financial stability.

From a lender’s perspective, a larger down payment reduces their risk. If you default on the loan, they have less to recover. For you, it means a smaller loan amount, lower monthly payments, and potentially a better interest rate. It also helps to avoid being "upside down" on your loan, where you owe more than the car is worth.

Saving for a down payment can take time, but it’s an investment that pays off. Even a few hundred dollars can make a difference, but aiming for 10-20% of the car’s value is ideal. Consider setting aside a portion of your SSI or any other income each month specifically for this purpose.

The Advantage of a Co-signer

If your credit score or DTI ratio isn’t as strong as you’d like, a co-signer can significantly boost your application. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you cannot make the payments. This provides an additional layer of security for the lender.

Choosing a co-signer requires careful consideration. It should be someone you trust implicitly, like a family member or close friend, who understands the commitment. Their credit score will be factored into the loan application, often leading to better terms and a higher likelihood of approval.

Common mistakes to avoid are choosing a co-signer who isn’t financially stable or failing to discuss the implications of co-signing thoroughly. Both parties are legally bound, so clear communication and mutual understanding are essential.

Your Vehicle Choice: Realistic Expectations

The type of car you choose plays a significant role in your loan approval and overall financial burden. While it’s tempting to eye a brand-new, fully loaded vehicle, a more modest, reliable used car is often the most practical choice for SSI recipients. Lenders are more likely to approve a loan for an affordable vehicle.

Opting for a car that is well within your budget demonstrates financial prudence. It ensures your monthly payments are manageable, leaving room for other essential expenses and unexpected car maintenance. Prioritize reliability and fuel efficiency over luxury or excessive features.

Remember, the goal is to secure transportation, not to stretch your budget to its breaking point. A less expensive car reduces the principal loan amount, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Strategic Approaches to Securing a Car Loan on SSI

Beyond the basic financial factors, specific strategies can significantly improve your chances of approval. These approaches are particularly effective for individuals navigating the car loan landscape with SSI as their primary income.

Demonstrating Stable and Verifiable Income

While SSI is a fixed income, its regularity is a major asset. Lenders appreciate consistency. Your SSI award letter serves as official proof of income, which is highly credible. Don’t underestimate the power of this documentation.

In addition to your SSI, if you have any other verifiable income sources, no matter how small, include them in your application. This could be part-time work, other government benefits, or even regular contributions from a family member (though these might be viewed differently by lenders). The more income you can document, the stronger your application appears.

Pro tips from us: Prepare all your income documentation in advance. This includes your SSI award letter, bank statements showing regular deposits, and any pay stubs from other employment. Being organized shows responsibility and speeds up the application process.

Building Relationships with the Right Lenders

Not all lenders are created equal, especially when it comes to unique financial situations like receiving SSI. Some institutions are more accustomed to working with individuals on fixed incomes or those with less-than-perfect credit.

Credit Unions: Often, credit unions are an excellent starting point. They are member-owned and typically more flexible and understanding than large commercial banks. They tend to look at the whole financial picture of a borrower, rather than just strict credit scores. If you’re not already a member, consider joining one in your community.

Subprime Lenders: There are also lenders who specialize in subprime auto loans, catering to individuals with lower credit scores or unique income situations. While these loans often come with higher interest rates, they can be a viable option when traditional lenders decline. Always research these lenders thoroughly to ensure they are reputable.

Dealership Financing: Many dealerships offer in-house financing or work with a network of lenders. While convenient, always compare their offers with those from independent lenders. Sometimes, dealerships can secure loans for individuals with challenging credit, but it’s crucial to scrutinize the terms and interest rates.

The Power of Pre-Approval

Getting pre-approved for a car loan before you even step foot on a dealership lot is a highly recommended strategy. Pre-approval means a lender has reviewed your financial information and determined how much they are willing to lend you, at what interest rate.

The benefits are numerous:

- Clear Budget: You know exactly how much car you can afford, preventing you from falling in love with a vehicle outside your price range.

- Negotiating Power: You become a cash buyer in the eyes of the dealership. This allows you to focus on negotiating the car’s price, rather than being swayed by financing terms.

- Confidence: You approach the car-buying process with greater confidence, knowing your financing is already in place.

Based on my experience, pre-approval removes a significant amount of stress from car shopping. It empowers you to make a more informed decision and often leads to a better overall deal.

Considering Secured Loans

Most car loans are secured loans, meaning the car itself acts as collateral. If you fail to make payments, the lender can repossess the vehicle. This security reduces the lender’s risk, which can make them more willing to approve loans for individuals with lower credit scores or fixed incomes. This aspect is inherently built into auto financing, making it a more accessible loan type than, say, an unsecured personal loan for a similar amount.

The Car Loan Application Process: What to Prepare and Expect

Once you’ve done your homework and identified potential lenders, the next step is the application itself. Being prepared and knowing what to expect can make the process smoother and less stressful.

Essential Documents to Gather

Lenders will require several documents to verify your identity, income, and residency. Having these ready will streamline your application:

- Proof of Identity: Government-issued ID (driver’s license, state ID).

- Proof of Income: Your SSI award letter, bank statements showing direct deposits of SSI, and any pay stubs from other employment.

- Proof of Residency: Utility bills, lease agreement, or other official mail showing your current address.

- Bank Statements: Recent statements to show your financial activity and ability to manage funds.

- Social Security Number: For credit checks.

- References: Sometimes requested, especially if you have limited credit history.

Having these documents neatly organized in a folder will demonstrate your preparedness and professionalism to the lender.

Filling Out the Application Accurately and Honestly

When completing the loan application, absolute honesty is paramount. Provide accurate information about your income, debts, and personal details. Any discrepancies or misleading information can lead to your application being denied or even accusations of fraud.

If you have gaps in employment or a less-than-perfect credit history, be prepared to explain these situations concisely and honestly. Lenders appreciate transparency. If you’re unsure about any section, don’t hesitate to ask the loan officer for clarification.

Common mistakes to avoid are exaggerating your income or omitting details about existing debts. These will almost certainly be discovered during the verification process and will harm your credibility.

Navigating Multiple Applications (Carefully!)

It’s wise to shop around for the best interest rates and terms. However, applying to too many lenders in a short period can negatively impact your credit score. Each "hard inquiry" on your credit report can temporarily lower your score.

Pro tips from us: Group your applications within a 14-45 day window. Credit scoring models are designed to recognize that you’re shopping for a single loan, so multiple inquiries within this period will typically only count as one hard inquiry. This allows you to compare offers without undue damage to your credit.

Post-Approval: Managing Your Car Loan Responsibly

Congratulations, you’ve secured your car loan! This is a significant achievement, but the journey doesn’t end here. Responsible management of your loan is crucial for your financial well-being and for building a stronger credit history for the future.

Making Timely Payments

This is the most critical aspect of loan management. Every single payment made on time contributes positively to your credit history. Set up automatic payments from your bank account if possible, or mark your calendar with payment due dates. Missing payments can lead to late fees, damage your credit score, and eventually lead to repossession.

Budgeting for the Full Cost of Car Ownership

A car loan payment is just one piece of the puzzle. When budgeting, you must account for all associated costs of car ownership:

- Car Insurance: This is a legal requirement in most places and can be a significant monthly expense. Shop around for quotes.

- Fuel: Factor in your daily or weekly commuting needs.

- Maintenance: Cars require oil changes, tire rotations, and occasional repairs. Set aside a small amount each month for this "car fund."

- Registration and Taxes: Annual fees that need to be paid.

Pro tips from us: Create a detailed monthly budget that includes your car loan payment, insurance, fuel, and a small allocation for maintenance. This comprehensive approach will prevent financial surprises and ensure you can comfortably afford your new vehicle. For more detailed budgeting advice, consider exploring resources on "Budgeting for Car Ownership" (internal link placeholder).

Exploring Refinancing Options Down the Road

As you consistently make timely payments and potentially improve your credit score, you might become eligible for better loan terms in the future. Refinancing involves taking out a new loan to pay off your existing car loan, often with a lower interest rate or different payment schedule.

This can save you a substantial amount of money over the life of the loan. Typically, you’ll need to have made at least 6-12 months of on-time payments and seen an improvement in your credit profile to qualify for refinancing.

SSI Benefits and Car Ownership: A Quick Note

Many SSI recipients worry that owning a car might affect their benefits. Generally, one car used for transportation for you or a member of your household is considered an excluded resource by the Social Security Administration (SSA) and will not count against your resource limit. However, it’s always wise to confirm specific rules with the SSA or a qualified financial advisor, as regulations can sometimes have nuances.

Pro Tips from Us: Driving Towards Success

Based on our extensive experience helping individuals navigate financial challenges, here are some final pro tips to ensure your car loan journey on SSI is as smooth as possible:

- Don’t Settle for the First Offer: Always compare loan offers from multiple lenders. The difference in interest rates can save you hundreds, even thousands, of dollars over the life of the loan.

- Read the Fine Print: Before signing anything, thoroughly read and understand all terms and conditions of the loan agreement. Pay attention to the interest rate, loan term, any prepayment penalties, and late fees. Ask questions until everything is clear.

- Consider a Used Car: As mentioned, a reliable used car is often a more financially sensible choice. It depreciates slower than a new car and comes with a lower purchase price, making it easier to secure a loan and manage payments.

- Prioritize Reliability Over Luxury: Your primary goal is reliable transportation. Focus on vehicles known for their durability and low maintenance costs, rather than advanced features or luxury brands.

- Budget for All Car Expenses: This includes not just the loan payment, but also insurance, fuel, maintenance, and registration. A holistic budget prevents unexpected financial strain.

Common Mistakes to Avoid When Seeking a Car Loan on SSI

Even with the best intentions, some common pitfalls can derail your efforts. Being aware of these can help you steer clear:

- Not Checking Your Credit Report: Going into the application process blind to your credit history is a significant disadvantage. Always know where you stand.

- Applying Without a Clear Budget: Rushing into a loan without a solid understanding of what you can truly afford (including all car-related expenses) often leads to financial distress.

- Ignoring Additional Car Costs: Focusing solely on the monthly loan payment and forgetting about insurance, fuel, and maintenance is a recipe for financial trouble.

- Falling for Predatory Loans: Be wary of lenders promising guaranteed approval regardless of credit or income. These often come with extremely high interest rates and unfavorable terms designed to trap borrowers.

- Signing Without Understanding Terms: Never feel pressured to sign a document you haven’t fully read or understood. Take your time, ask questions, and seek clarification.

Conclusion: Your Road to Car Ownership Is Possible

Navigating the world of car loans while on Supplemental Security Income might seem daunting, but as we’ve explored, it is absolutely within reach. By understanding the factors lenders consider, strategically preparing your finances, and approaching the application process with knowledge and confidence, you can significantly increase your chances of approval.

Remember, your SSI income is a legitimate source of funds, and with a strong credit profile, a healthy debt-to-income ratio, a solid down payment, or the help of a co-signer, you can demonstrate your ability to responsibly manage a car loan. The key is preparation, transparency, and choosing the right vehicle and lender for your unique situation.

Don’t let perceived limitations deter you from achieving the independence that reliable transportation offers. Start by assessing your financial situation, gathering your documents, and building a strategy. Your journey to car ownership on SSI begins now, and with the insights shared here, you are well-equipped to drive away with confidence.