Can I Get A Car Loan With Fair Credit? Your Comprehensive Guide to Driving Away Confidently

Can I Get A Car Loan With Fair Credit? Your Comprehensive Guide to Driving Away Confidently Carloan.Guidemechanic.com

Securing a car loan can feel like navigating a complex maze, especially when your credit score isn’t in the "excellent" category. Many prospective car buyers wonder, "Can I get a car loan with fair credit?" The answer, unequivocally, is yes, it is absolutely possible. While having a pristine credit history certainly makes the process smoother and often cheaper, a fair credit score is far from a deal-breaker.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to successfully obtain a car loan, even with fair credit. We’ll delve deep into what fair credit means for auto lenders, how to prepare your application, and crucial steps to take to secure the best possible terms. Our goal is to provide you with actionable advice, based on years of experience in the automotive and financial sectors, helping you drive away with confidence.

Can I Get A Car Loan With Fair Credit? Your Comprehensive Guide to Driving Away Confidently

Understanding "Fair Credit" in the Auto Loan World

Before we dive into the "how," let’s clarify what "fair credit" actually entails and how lenders perceive it. Your credit score is a numerical representation of your creditworthiness, a snapshot of your financial reliability. It’s a key factor lenders use to assess the risk of lending you money.

What Defines Fair Credit?

Credit scores typically fall into several ranges, with the most common scoring models being FICO and VantageScore. While the exact numbers can vary slightly, "fair credit" generally falls within these ranges:

- FICO Score: 580-669

- VantageScore: 601-660

If your score lands within these brackets, you’re considered to have fair credit. This means you likely have some credit history, but perhaps a few late payments, a relatively short credit history, or a higher credit utilization ratio.

How Lenders View Fair Credit

Lenders categorize applicants based on their credit scores because it helps them predict the likelihood of repayment. An applicant with excellent credit (740+) is seen as very low risk, while someone with poor credit (below 580) is considered high risk.

Fair credit applicants fall into a middle ground. Lenders recognize that you have some experience managing debt, but they also see potential indicators of increased risk. This perception directly impacts the loan terms you might be offered.

The Impact on Interest Rates and Terms

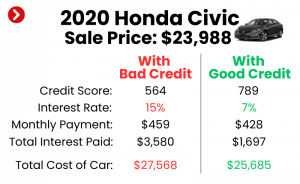

One of the most significant consequences of having fair credit when seeking an auto loan is the interest rate you’ll likely receive. Because lenders perceive a higher risk with fair credit, they often charge higher interest rates to compensate for that risk. This means you’ll pay more over the life of the loan compared to someone with a good or excellent credit score.

Additionally, fair credit can influence other loan terms, such as the loan duration or the maximum loan amount you qualify for. Lenders might be more conservative, offering shorter terms or requiring a larger down payment. Understanding this reality upfront helps you set realistic expectations and prepare effectively.

The Realities of Getting a Car Loan with Fair Credit

It’s important to approach the car loan process with a clear understanding of what to expect. While getting an auto loan with fair credit is achievable, it often requires a more strategic approach than if you had top-tier credit.

It’s Not Impossible, But It Requires Strategy

Many people mistakenly believe that a fair credit score immediately disqualifies them from car financing. This simply isn’t true. Lenders are in the business of lending money, and they understand that credit profiles vary widely. Your job is to present yourself as the most reliable borrower possible within your credit tier.

This means focusing on aspects of your financial profile that can offset your credit score, such as income stability, a down payment, or a co-signer. A proactive and well-prepared approach significantly increases your chances of approval and helps secure more favorable terms.

Expectations Regarding Interest Rates

As mentioned, higher interest rates are a common reality for fair credit car loan applicants. While someone with excellent credit might qualify for rates as low as 3-5%, fair credit applicants might see rates ranging from 7% to 15% or even higher, depending on various factors.

It’s crucial not to be discouraged by these numbers, but to be aware of them. Focus on securing the best rate available to you given your current credit standing. Remember, these rates aren’t set in stone forever; you might have options to refinance later as your credit improves.

Loan Terms: Shorter vs. Longer

The length of your loan term (e.g., 36, 48, 60, 72 months) also plays a significant role. With fair credit, lenders might prefer shorter loan terms, as this reduces their risk exposure over time. A shorter term means higher monthly payments but less interest paid overall.

Conversely, you might be tempted by longer loan terms (e.g., 72 or 84 months) because they offer lower monthly payments. While this can make a vehicle seem more affordable, it often results in paying significantly more in interest over the life of the loan and increases the risk of being "upside down" on your loan (owing more than the car is worth). Pro tips from us: Always consider the total cost of the loan, not just the monthly payment.

Essential Steps Before Applying for a Car Loan

Preparation is paramount when seeking an auto loan with fair credit. Taking these steps before you even set foot in a dealership or apply online can dramatically improve your outcomes.

1. Check Your Credit Score & Report

This is the foundational step. You cannot effectively plan without knowing your starting point.

- Why it’s crucial: Your credit report contains all the information lenders use to calculate your score. It lists your payment history, types of credit accounts, amounts owed, and length of credit history. Knowing this allows you to identify potential issues and understand how lenders see you.

- How to get it: You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months via AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring.

- Disputing errors: Common mistakes to avoid are not reviewing your report thoroughly. Look for any inaccuracies, such as incorrect late payments, accounts you don’t recognize, or incorrect personal information. Even small errors can negatively impact your score. If you find errors, dispute them immediately with the credit bureau. This process can take time, so start early.

2. Determine Your Budget

A car loan is a significant financial commitment. It’s vital to determine what you can truly afford, not just what a lender might approve you for.

- Affordability: Beyond the monthly car payment, factor in other costs like insurance, fuel, maintenance, and potential repairs. Based on my experience, many first-time buyers overlook these crucial expenses, leading to financial strain down the road.

- The 20/4/10 Rule: A common guideline suggests a 20% down payment, a loan term no longer than 4 years (48 months), and car expenses (payment + insurance) not exceeding 10% of your gross monthly income. While this might be challenging with fair credit, it’s a good benchmark to aim for.

3. Save for a Down Payment

A substantial down payment is one of your strongest allies when applying for a car loan with fair credit.

- Benefits of a larger down payment:

- Reduces loan amount: The less you borrow, the lower your monthly payments and the less interest you pay overall.

- Lowers lender risk: A significant down payment shows lenders you have "skin in the game" and are serious about repayment. This can make them more willing to approve your loan and offer better terms.

- Helps avoid negative equity: With a larger down payment, you’re less likely to owe more on the car than it’s worth, especially given how quickly new cars depreciate.

- Pro Tip: Aim for at least 10-20% of the car’s purchase price. Every dollar you put down improves your position.

4. Get Pre-Approved

This step is a game-changer for fair credit applicants. Getting pre-approved means a lender has conditionally agreed to lend you a certain amount of money at a specific interest rate before you even choose a car.

- Why pre-approval is powerful:

- Negotiating power: You walk into the dealership knowing exactly how much financing you qualify for and at what rate. This allows you to focus on negotiating the car’s price, not the financing. It puts you in the driver’s seat.

- Budget clarity: You know your borrowing limit, preventing you from falling in love with a car you can’t truly afford.

- Comparison shopping: You can compare offers from multiple lenders without impacting your credit score multiple times (as multiple inquiries within a short period for the same loan type are usually counted as one).

- How it differs from application: Pre-approval is a "soft inquiry" on your credit, which doesn’t affect your score. A full loan application involves a "hard inquiry," which can temporarily ding your score.

Strategies to Strengthen Your Application with Fair Credit

Even with fair credit, you have several levers you can pull to make your application more attractive to lenders. Employing these strategies can significantly improve your chances of approval and help you secure better loan terms.

The Power of a Down Payment

We’ve touched on this, but it bears repeating: a solid down payment is perhaps the single most effective way to bolster a fair credit application. It directly reduces the lender’s risk and signals your commitment. The more you can put down upfront, the less the lender needs to finance, making the loan less risky for them.

- Based on my experience, a 20% down payment can often move a fair credit applicant into a better interest rate tier, even if their score hasn’t dramatically changed. It shows financial discipline and reduces the loan-to-value (LTV) ratio, which lenders favor.

Consider a Co-signer

If your credit score is on the lower end of the "fair" spectrum, or if you have a limited credit history, a co-signer can be an invaluable asset.

- Who makes a good co-signer? An ideal co-signer has excellent credit, a stable income, and a strong financial history. This person could be a trusted family member or friend.

- Risks and benefits:

- Benefit: A co-signer essentially lends their good credit to your application, making you a much lower risk in the lender’s eyes. This often results in approval and significantly lower interest rates than you’d get on your own.

- Risk: The co-signer is equally responsible for the loan. If you miss payments, their credit score will be negatively affected, and they will be legally obligated to pay the debt. This is a serious commitment and should only be pursued with careful consideration and clear communication.

Choose the Right Vehicle

The type of car you choose also impacts your loan prospects and overall affordability.

- New vs. Used: While a brand-new car might be appealing, a reliable used car often makes more financial sense for fair credit applicants. Used cars generally have lower price tags, which means you’ll need to borrow less. They also depreciate slower than new cars.

- Depreciation and affordability: Research the depreciation rates of different makes and models. Some cars hold their value better, which is advantageous if you decide to sell or trade in later. Common mistakes to avoid are falling for an expensive, rapidly depreciating vehicle that stretches your budget too thin.

Shop Around for Lenders

This is a critical strategy that many consumers, especially those with fair credit, often overlook. Do not simply accept the first loan offer you receive, particularly if it comes from a dealership.

- Don’t just go to the dealership: Dealerships primarily want to sell cars, and while they offer financing, their rates might not be the most competitive for fair credit borrowers. They work with a network of lenders, but they might prioritize those that offer them a higher commission.

- Explore all options:

- Banks: Traditional banks often have competitive rates, especially if you’re already a customer.

- Credit Unions: These member-owned financial institutions are renowned for offering some of the best auto loan rates, often more leniently with fair credit applicants due to their community-focused mission.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, or Carvana Financing specialize in auto loans and can offer quick pre-approvals and competitive rates across a range of credit scores.

- Pro Tip: Apply for pre-approval with 3-5 different lenders within a 14-day window. Credit bureaus typically count these multiple inquiries as a single "hard inquiry," minimizing the impact on your credit score. This allows you to compare offers without penalty.

Focus on Reputable Lenders

While shopping around, ensure you’re dealing with legitimate and reputable financial institutions.

- Avoid predatory loans: Be wary of "buy here, pay here" dealerships or lenders that promise guaranteed approval regardless of credit score without clear terms. These often come with extremely high interest rates and unfavorable terms that can trap you in a cycle of debt.

- Read reviews: Check online reviews and ratings for any lender you’re considering. Ensure they are transparent about their fees and terms.

The Application Process: What to Expect

Once you’ve done your homework and found a car you like, it’s time to formally apply for the loan. Knowing what to expect can reduce stress and help you navigate the final steps effectively.

Required Documents

Lenders will need several documents to verify your identity, income, and financial stability. Be prepared to provide:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs (typically for the last 1-3 months), W-2 forms, or tax returns if you’re self-employed.

- Proof of Residence: Utility bill or lease agreement.

- Proof of Insurance: You’ll need to show you have adequate car insurance before driving off the lot.

- Vehicle Information: Details about the car you intend to purchase (VIN, make, model, year, mileage).

- Trade-in Information (if applicable): Title, registration, and any loan payoff information for your current vehicle.

Understanding Loan Offers: APR vs. Interest Rate

When comparing loan offers, pay close attention to the Annual Percentage Rate (APR), not just the interest rate.

- Interest Rate: This is the percentage charged on the principal amount of the loan.

- APR: This is the total cost of borrowing money over a year, expressed as a percentage. It includes the interest rate plus any additional fees, such as origination fees or closing costs.

- Pro Tip: Always compare APRs when evaluating loan offers, as it gives you a truer picture of the loan’s overall cost. A lower interest rate might look appealing, but a higher APR due to hidden fees can make it more expensive in the long run.

Negotiating Loan Terms

Even with fair credit, there might be some room for negotiation, especially if you have multiple pre-approval offers.

- Focus on the total price: Negotiate the price of the car first, separately from the financing. Once you agree on a price, then discuss the financing options.

- Consider shorter terms: If you can afford slightly higher monthly payments, a shorter loan term will save you a significant amount in interest over time.

- Beware of add-ons: Dealerships often try to sell extended warranties, GAP insurance, or other add-ons. While some might be beneficial, they add to your loan amount and increase your monthly payment. Critically evaluate whether you truly need them. Common mistakes to avoid are allowing these add-ons to inflate your total loan cost unnecessarily.

Common Mistakes to Avoid During Application

- Applying for too many loans at once: While shopping around is good, excessive applications can hurt your credit score by generating too many hard inquiries. Stick to a focused period for comparison.

- Misrepresenting income or financial situation: Always be honest and transparent with lenders. Providing false information can lead to loan denial or even legal consequences.

- Not reading the fine print: Carefully review all loan documents before signing. Ensure you understand the interest rate, APR, loan term, payment schedule, and any penalties for late payments or early payoff. .

After Loan Approval: Building Better Credit for the Future

Getting a car loan with fair credit isn’t just about driving away with a new vehicle; it’s also a golden opportunity to improve your financial standing. By responsibly managing your auto loan, you can significantly boost your credit score, paving the way for better financial opportunities in the future.

Making Timely Payments

This is the most critical step. Your payment history accounts for the largest portion (35%) of your FICO score.

- Consistency is key: Make every payment on time, every month. Set up automatic payments from your bank account to avoid missing deadlines.

- Avoid late payments: Even one late payment can have a significant negative impact on your credit score, especially if it’s 30 days or more past due.

Avoiding New Debt

While you’re working on improving your credit, try to avoid taking on significant new debt.

- Keep credit utilization low: Don’t open new credit cards or take out personal loans unnecessarily. This shows lenders you are not overextending yourself. Your debt-to-income ratio (DTI) is another factor lenders consider. Keeping it low demonstrates good financial health.

Monitoring Your Credit

Continue to monitor your credit report regularly. This allows you to track your progress and quickly identify any new errors or suspicious activity. Many financial apps and credit card providers offer free credit monitoring services.

Refinancing Options Later

As your credit score improves (and it will, with responsible payment behavior), you might become eligible for better loan terms.

- Consider refinancing: After 6-12 months of on-time payments, your credit score could significantly improve. At this point, you might be able to refinance your car loan for a lower interest rate, saving you hundreds or even thousands of dollars over the remaining loan term. This is a smart financial move that many fair credit borrowers use to their advantage. .

Pro Tips & Common Mistakes to Avoid

Here are some final expert insights to help you navigate your fair credit car loan journey:

Pro Tips From Us:

- Don’t Settle for the First Offer: Always compare at least three to five loan offers, especially if you have fair credit. Competition among lenders benefits you.

- Understand the Total Cost: Focus on the total amount you’ll pay over the life of the loan (principal + interest), not just the monthly payment. A lower monthly payment over a longer term often means paying significantly more in interest.

- Boost Your Credit Score Pre-Application: If you have a little time, even a few months of diligent effort can push your fair credit score into the "good" range, opening doors to much better rates. Pay down credit card balances, ensure all bills are paid on time.

Common Mistakes to Avoid Are:

- Not Checking Your Credit Report: Going into the process blind is a recipe for disappointment. Always know your score and review your report for errors.

- Taking on a Loan You Can’t Afford: Just because you’re approved for a certain amount doesn’t mean you should borrow it. Stick to your budget, considering all car-related expenses.

- Focusing Only on Monthly Payments: This is a classic trap. Dealers often "pack" a loan with extras or extend the term to lower the monthly payment, but this drastically increases the total cost.

- Ignoring the Fine Print: Always read your loan contract thoroughly. If you don’t understand something, ask for clarification.

Conclusion

The question "Can I get a car loan with fair credit?" is met with a resounding yes, but it comes with the caveat that preparation, strategy, and diligence are your best allies. Having fair credit doesn’t close the door on car ownership; it simply means you need to be more informed and proactive in your approach.

By understanding your credit score, budgeting wisely, saving for a down payment, getting pre-approved, and diligently shopping for the best loan terms, you can absolutely secure a car loan that fits your financial situation. Furthermore, this journey can be a stepping stone to improving your credit score, opening up even better financial opportunities in the future. Drive away confidently by equipping yourself with the right knowledge and taking the smart steps outlined in this guide. Your dream car, even with fair credit, is well within reach.

External Resource: For more detailed information on managing your credit and understanding credit reports, you can visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/