Can I Pay Off A Car Loan Early? Unlocking Financial Freedom & Making Smart Decisions

Can I Pay Off A Car Loan Early? Unlocking Financial Freedom & Making Smart Decisions Carloan.Guidemechanic.com

The open road, the wind in your hair, and the distinct scent of a new car – it’s a dream many of us pursue. But with that dream often comes a monthly car loan payment, a recurring obligation that can feel like a financial anchor. Have you ever found yourself wondering, "Can I pay off a car loan early?" The short answer is almost always yes, and it’s a question that opens the door to significant financial benefits and a powerful sense of freedom.

In this super comprehensive guide, we’re not just scratching the surface. We’re diving deep into every facet of early car loan repayment, from the compelling reasons why you should consider it to the practical strategies for making it happen, and even the potential pitfalls to watch out for. Our ultimate goal is to equip you with the knowledge and confidence to make an informed decision that aligns perfectly with your financial aspirations. Let’s embark on this journey toward auto loan liberation together.

Can I Pay Off A Car Loan Early? Unlocking Financial Freedom & Making Smart Decisions

The Allure of Early Car Loan Payoff: Why Even Consider It?

The prospect of shedding a monthly debt payment is inherently appealing, but beyond the psychological relief, there are tangible financial advantages to paying off your car loan ahead of schedule. Understanding these benefits is the first step in deciding if this strategy is right for you. Based on my experience as a financial blogger and content writer, the desire for debt freedom is a powerful motivator.

1. Saving Substantial Money on Interest

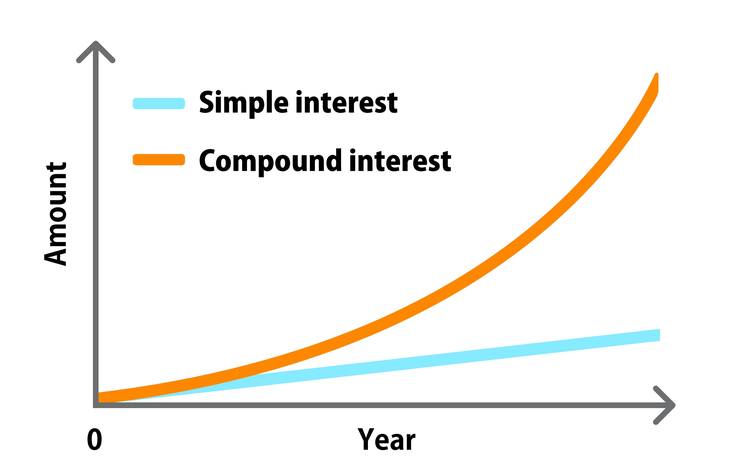

This is arguably the most compelling reason to accelerate your car loan payments. When you take out an auto loan, you agree to pay back the principal amount borrowed, plus interest, over a set period. Interest is essentially the cost of borrowing money, and it’s typically calculated based on your remaining principal balance.

By paying off your loan early, you reduce the amount of time the lender has to charge you interest. Each extra payment you make directly reduces your principal balance, which in turn means less interest accrues on that smaller balance in subsequent months. Over the life of a multi-year loan, these savings can add up to hundreds, or even thousands, of dollars. Imagine what you could do with that extra cash!

2. Achieving Debt-Free Living Faster

There’s an undeniable psychological and financial liberation that comes with being debt-free. Imagine a world where one less monthly bill demands your attention and a significant portion of your income. Paying off your car loan early is a concrete step towards achieving this state of financial independence.

This accelerated journey to debt freedom can have a ripple effect across your entire financial life. It frees up mental bandwidth and reduces stress, allowing you to focus on other critical financial goals without the weight of car payments looming over you. It’s a cornerstone of building a robust and secure financial future.

3. Improving Your Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) is a crucial metric that lenders use to assess your ability to manage monthly payments and repay future debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates that you have more income available to cover new debts.

When you eliminate your car loan, you effectively remove a significant monthly debt obligation from your DTI calculation. This improvement can make you a more attractive borrower for other large loans, such as a mortgage, and potentially qualify you for better interest rates down the line. It’s a strategic move for long-term financial planning.

4. Boosting Your Monthly Cash Flow

Once your car loan is fully paid off, that monthly payment amount is no longer obligated to the lender. This immediately translates into a boost in your disposable income or, more accurately, your available cash flow. This newfound financial breathing room is incredibly valuable.

You can then consciously redirect this freed-up money towards other important financial objectives. Perhaps you want to accelerate your retirement savings, build up your emergency fund, invest in your child’s education, or even save up for a down payment on a house. The possibilities are expansive and entirely within your control.

5. Reducing Financial Risk and Vulnerability

Life is unpredictable, and unexpected expenses or job losses can throw even the most carefully planned budgets into disarray. Carrying less debt inherently reduces your financial risk and makes you more resilient to these unforeseen circumstances. With fewer fixed obligations, you have greater flexibility to navigate tough times.

Eliminating your car payment provides a crucial safety net. Should an emergency arise, you won’t have the added pressure of ensuring that car payment is made, allowing you to focus your resources where they are most critically needed. It’s a proactive step towards building financial security.

The Practicalities: How to Pay Off Your Car Loan Early (Strategies)

So, you’re convinced that paying off your car loan early is a smart move. But how exactly do you go about it? There are several effective strategies you can employ, ranging from small, consistent efforts to larger, impactful actions. Pro tips from us emphasize being intentional with every extra payment.

1. Making Extra Principal Payments

This is one of the most straightforward and effective methods. Instead of just making your regular monthly payment, you add an additional amount to it. The crucial step here is to explicitly instruct your lender that this extra money should be applied directly to the principal balance, not simply held as a future payment or applied to interest.

Even a small additional sum, like an extra $50 or $100 each month, can significantly reduce your loan term and overall interest paid. Over several years, these consistent extra contributions compound their effect, saving you substantial money and time. Always double-check your loan statements to ensure the extra payments were correctly applied.

2. Making Bi-Weekly Payments

This strategy involves splitting your monthly car payment in half and paying that amount every two weeks instead of making one full payment each month. Since there are 52 weeks in a year, this means you’ll make 26 half-payments, which equates to 13 full monthly payments annually instead of the standard 12.

That "extra" full payment each year directly goes towards reducing your principal, accelerating your payoff timeline without feeling like a massive financial stretch each month. Many lenders offer this option directly, or you can manually set it up by dividing your payment and making two transfers each month.

3. Making a Lump Sum Payment

If you receive an unexpected financial windfall, such as a work bonus, a tax refund, an inheritance, or even proceeds from selling something valuable, a lump sum payment can dramatically shorten your loan term. This strategy offers an immediate and significant reduction in your principal balance.

When making a lump sum payment, just like with extra principal payments, ensure you clearly communicate to your lender that the entire amount should be applied directly to the principal. This maximizes the impact of your payment by reducing the base on which future interest is calculated from day one.

4. Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan. This strategy is particularly effective if you can secure a new loan with a lower interest rate or a shorter loan term, or ideally, both. A lower interest rate means more of your payment goes towards principal, and a shorter term naturally accelerates the payoff.

Before refinancing, compare rates from multiple lenders and carefully calculate the total cost. Common mistakes to avoid are refinancing to a longer term just to get a lower monthly payment, as this often means paying more interest over the life of the loan. For a deeper dive, check out our article on Understanding Car Loan Refinancing: Is It Right For You? (Internal Link Placeholder).

5. Applying Debt Repayment Methods (Snowball or Avalanche)

If you have multiple debts, you might consider applying established debt repayment strategies like the "debt snowball" or "debt avalanche" to your car loan.

- Debt Snowball: You pay off your smallest debt first, regardless of interest rate, while making minimum payments on others. Once that debt is gone, you roll its payment into the next smallest debt, gaining psychological momentum.

- Debt Avalanche: You prioritize paying off the debt with the highest interest rate first, saving you the most money on interest, while making minimum payments on others. This is mathematically the most efficient method.

Deciding which method suits you best depends on whether you’re motivated more by quick wins (snowball) or maximum interest savings (avalanche). Both can be powerful tools to eliminate your car loan faster.

Potential Pitfalls and Considerations: Is There a Downside?

While paying off a car loan early offers numerous advantages, it’s not a universally perfect solution for everyone. There are crucial factors to consider and potential downsides that could make it less ideal depending on your individual financial situation. Always approach such decisions with careful analysis.

1. Prepayment Penalties

The most significant potential pitfall to investigate is whether your loan agreement includes a prepayment penalty. This is a fee charged by some lenders if you pay off your loan ahead of schedule. While less common with auto loans compared to mortgages, they do exist, particularly with certain types of lenders or specific loan terms.

Prepayment penalties usually come in two forms: a fixed fee or a percentage of the remaining balance. Before making any extra payments, meticulously review your original loan documents or contact your lender directly to confirm if such a clause exists. Based on my experience, most modern auto loans, especially from major banks, do not have prepayment penalties, but verifying is always essential.

2. Opportunity Cost

Every dollar you spend or allocate to one purpose is a dollar that cannot be used for another. This concept is known as opportunity cost. When you direct extra funds towards your car loan, you’re essentially choosing that over other potential uses for that money.

Consider your other financial priorities. Do you have high-interest credit card debt (typically 18-25% APR)? If so, paying off that debt first will almost always save you more money than accelerating a car loan with a lower interest rate (e.g., 3-7% APR). Similarly, if you have robust investment opportunities with a high expected return, that money might generate more wealth there. Pro tip: Always ensure your emergency fund is robust before aggressively paying down lower-interest debt. For more on this, you can read about Opportunity Cost on Investopedia. (External Link Placeholder).

3. Impact on Credit Score (Minor and Temporary)

While paying off debt is generally good for your credit score in the long run, closing an account can sometimes cause a minor, temporary dip. This is because your credit score considers factors like your average age of credit accounts and your credit mix. When an account closes, it can slightly reduce the average age of your accounts.

However, the positive impact of reducing your overall debt burden and improving your debt-to-income ratio far outweighs any negligible, short-term negative effect. The benefits of being debt-free and having more financial flexibility will ultimately contribute to a healthier credit profile over time.

4. Draining Your Emergency Fund

Aggressively paying down debt is commendable, but not at the expense of your financial safety net. Draining your emergency fund – a dedicated savings account holding 3-6 months’ worth of living expenses – to pay off your car loan early is a common mistake to avoid.

Without an adequate emergency fund, you become vulnerable to unexpected financial shocks. Should you lose your job or face a medical emergency, you might be forced to take on new, potentially high-interest debt to cover essential expenses. Always ensure your emergency fund is fully funded before directing significant extra money to debt repayment. Our article, Building a Robust Emergency Fund: Your Financial Safety Net, offers excellent guidance (Internal Link Placeholder).

The "When": Deciding if Early Payoff is Right for You (Decision Framework)

Deciding when to pay off your car loan early isn’t a one-size-fits-all answer. It requires a thoughtful assessment of your personal financial landscape, your current goals, and your risk tolerance. Here’s a framework to help you navigate this important decision.

1. Assess Your Current Financial Situation

Before making any aggressive moves, take a holistic look at your finances. Do you have a fully funded emergency fund (typically 3-6 months of living expenses)? Are you carrying any high-interest debt, such as credit card balances, personal loans, or even student loans with higher interest rates than your car loan?

If the answer to either of those questions is "no" or "yes" respectively, addressing those issues should likely take precedence. Building your emergency fund provides security, and eliminating high-interest debt saves you more money in the long run due to its higher cost.

2. Review Your Loan Agreement Meticulously

This step is non-negotiable. Pull out your original car loan contract and scrutinize it for any mention of prepayment penalties. Understand your exact interest rate, the remaining principal balance, and how much time is left on your loan term.

Knowing these specifics will allow you to calculate how much interest you stand to save and whether any penalties would negate those savings. If you can’t find the information, contact your lender directly for clarification.

3. Compare Your Car Loan Interest Rate with Other Opportunities

What is the interest rate on your car loan? If it’s relatively low (e.g., 3-5%), the financial incentive to pay it off early might be less compelling compared to other uses for your money. If your interest rate is higher (e.g., 7% or more), the savings become much more significant.

Consider if that extra money could generate a higher return elsewhere. For example, if your car loan is at 4% and you have investment opportunities yielding a consistent 7-8% (e.g., a diversified stock market index fund in a long-term retirement account), you might choose to invest rather than pay off the car loan. This is a personal decision based on your risk tolerance and financial goals.

4. Consider Your Personal Financial Philosophy

Beyond the numbers, your personal philosophy towards debt plays a significant role. Some individuals are inherently debt-averse and prioritize the psychological peace of mind that comes with being completely debt-free. For these individuals, paying off a car loan early might be a priority even if the purely mathematical savings aren’t the absolute highest.

Others are more comfortable with debt, especially if it’s "good debt" (like a low-interest mortgage or car loan) that frees up capital for higher-return investments. There’s no right or wrong answer here; it’s about what helps you sleep best at night and aligns with your overall financial values.

Beyond the Payment: What Happens After You Pay Off Your Car Loan Early?

Congratulations! You’ve made that final payment and are officially free of your car loan. But what happens next? There are a few important steps to ensure everything is properly finalized and to strategically manage your newly freed-up cash flow.

1. Getting Your Title and Lien Release

Once your loan is paid in full, your lender will release their lien on your vehicle. This means they no longer have a legal claim to your car. The process for receiving your clear title varies by state and lender. Some lenders will mail you a physical title directly, while others will send a lien release document that you then take to your local Department of Motor Vehicles (DMV) to obtain a new, clear title in your name.

It’s crucial to follow up and ensure you receive this documentation. Without a clear title, you won’t be able to sell your car or use it as collateral for another loan. Keep these documents in a safe place, such as a fireproof safe or a secure financial folder.

2. Notifying Your Insurance Company (Optional but Smart)

While not strictly necessary, it’s a good idea to inform your car insurance company that your loan has been paid off. Lenders often require specific types and levels of coverage (like comprehensive and collision) to protect their investment in the vehicle.

Once the car is fully yours, you have more flexibility to adjust your insurance coverage to suit your needs and budget. You might decide to reduce certain coverages, though always carefully weigh the risks involved. This could potentially lead to minor savings on your premiums.

3. Strategically Redirecting Your Cash Flow

This is where the real power of early payoff comes into play. You now have an extra monthly payment that was previously dedicated to your car loan. Don’t let this money simply disappear into your general spending! Pro tips from us: Be intentional about how you reallocate these funds.

Consider these options:

- Boost Your Emergency Fund: If it’s not fully funded, this is a prime opportunity to reach your goal.

- Tackle Other Debts: Direct the money towards other high-interest debts (credit cards, personal loans).

- Increase Savings: Put it towards a down payment on a house, a child’s education fund, or a vacation.

- Invest for the Future: Maximize contributions to your retirement accounts (401k, IRA) or open a brokerage account.

- Home Improvements or Other Goals: Fund projects that add value or fulfill long-held dreams.

The key is to consciously decide where this money will go, turning a former obligation into a powerful tool for achieving your next financial milestone.

Common Mistakes to Avoid When Paying Off a Car Loan Early

While the intention to pay off debt early is admirable, a few missteps can diminish the benefits or even cause unintended financial headaches. Here are some common mistakes to be aware of:

- Paying Extra Without Specifying "Principal Only": As mentioned, if you don’t explicitly instruct your lender to apply extra payments to the principal, they might just hold it as an advance payment or apply it to future interest, negating your efforts. Always specify!

- Ignoring Prepayment Penalties: Failing to check your loan agreement for prepayment penalties can lead to unexpected fees that might make early payoff less advantageous. Always confirm this first.

- Draining Your Emergency Fund: Never compromise your financial safety net to pay off a relatively low-interest car loan. Your emergency fund is paramount for unexpected life events.

- Refinancing to a Longer Term for Lower Payments: While a lower monthly payment sounds good, extending your loan term often means paying significantly more in total interest over the life of the new loan, even with a lower APR.

- Not Having a Plan for the Freed-Up Cash Flow: If you pay off your car loan early but then just let that extra money vanish into everyday spending, you’re missing a huge opportunity to accelerate other financial goals. Be intentional with your newfound funds.

- Not Celebrating Your Achievement! This isn’t a financial mistake, but it’s a missed opportunity for a morale boost! Paying off a major debt is a significant accomplishment – acknowledge it, celebrate it, and let it fuel your motivation for future financial wins.

Conclusion: Your Path to Auto Loan Freedom

So, can you pay off a car loan early? Absolutely, and for most people, it’s a financially savvy move that offers tangible benefits like significant interest savings, increased cash flow, and the profound peace of mind that comes with being debt-free. It’s a powerful step towards building a more secure and flexible financial future.

However, as we’ve explored, it’s not a decision to be made lightly. Carefully weigh the advantages against potential downsides like prepayment penalties and opportunity costs. Take the time to assess your unique financial situation, review your loan documents, and prioritize your broader financial goals, especially ensuring your emergency fund is robust and high-interest debts are addressed first.

By leveraging the strategies outlined in this guide and avoiding common pitfalls, you can confidently navigate the path to early car loan payoff. Embrace the opportunity to take control of your finances, make informed decisions, and accelerate your journey toward ultimate financial freedom. Now, what will you do with that extra cash each month? The choice, and the power, is all yours.