Can I Take Out a Car Loan at 18? Your Ultimate Guide to Driving Off the Lot with Confidence

Can I Take Out a Car Loan at 18? Your Ultimate Guide to Driving Off the Lot with Confidence Carloan.Guidemechanic.com

Turning 18 is a milestone packed with new freedoms and responsibilities. For many young adults, one of the most exciting prospects is the independence that comes with owning their first car. But as the dream of hitting the open road takes shape, a crucial question often arises: "Can I take out a car loan at 18?"

The short answer is yes, it’s absolutely possible. However, the path to securing an auto loan for an 18-year-old isn’t always a straightforward one. It requires careful planning, a solid understanding of financial principles, and strategic execution. This comprehensive guide will walk you through every aspect of obtaining a car loan as a young borrower, providing insights, expert tips, and actionable advice to help you navigate the process successfully. We’re here to turn that "can I?" into a confident "I can!"

Can I Take Out a Car Loan at 18? Your Ultimate Guide to Driving Off the Lot with Confidence

Understanding the Legal Landscape: Age and Loan Eligibility

The first hurdle to consider when asking, "Can I take out a car loan at 18?" is the legal age requirement. In most parts of the United States and many other countries, you must be at least 18 years old to legally enter into a contract. A car loan, by its very nature, is a legally binding agreement between you and a lender.

This means that from a purely legal standpoint, an 18-year-old is indeed eligible to sign a loan agreement. However, legal eligibility is only one piece of the puzzle. Lenders have their own set of criteria, and this is where the real challenges and opportunities for young borrowers emerge.

Lenders primarily focus on a borrower’s ability and willingness to repay the loan. For an 18-year-old, these factors can often be less established compared to older applicants. They look at your credit history, income stability, and overall financial responsibility.

The Lender’s Perspective: Why It Can Be Challenging for Young Borrowers

While you are legally an adult, securing a car loan at 18 often presents unique challenges. Lenders are in the business of assessing risk, and several factors typically make young borrowers appear riskier. Understanding these challenges is the first step toward overcoming them.

The primary concern for most lenders is the lack of a substantial credit history. At 18, many individuals haven’t had the opportunity to establish a long track record of managing debt responsibly. This "thin file" makes it difficult for lenders to predict future repayment behavior.

Another significant factor is income stability. While an 18-year-old might have a job, it’s often an entry-level position or part-time work, which lenders might view as less stable than a more established career. A consistent and sufficient income is crucial for demonstrating repayment capacity.

Furthermore, many young adults may not have a significant down payment saved up. A larger down payment reduces the loan amount, lowers the lender’s risk, and shows a commitment to the purchase. Without one, the loan becomes riskier for the lender.

Building Your Case: The Essential Elements for an 18-Year-Old Car Loan

Successfully obtaining a car loan at 18 hinges on strategically addressing the lender’s concerns. By focusing on key financial pillars, you can significantly strengthen your application. Let’s delve into the crucial elements you need to build a compelling case.

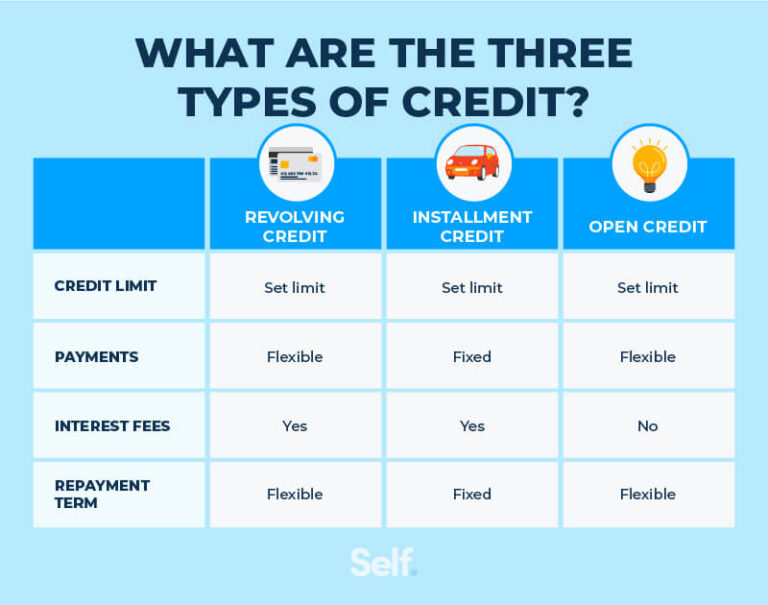

1. Establishing a Credit History: Your Financial Footprint

A solid credit history is paramount for any loan application. For an 18-year-old, this is often the most significant hurdle, as you’re likely starting from scratch. Lenders use your credit report and score to gauge your reliability as a borrower.

Starting to build credit early is incredibly beneficial. One effective way is to apply for a secured credit card. With a secured card, you put down a deposit, which often becomes your credit limit, reducing the risk for the card issuer. Using this card responsibly by making small purchases and paying them off in full and on time each month will help you build a positive payment history.

Another excellent strategy is to become an authorized user on a parent’s credit card. If your parent has good credit and uses their card responsibly, their positive payment history can sometimes reflect on your credit report. This can give you a helpful head start, but always ensure the card issuer reports authorized user activity to credit bureaus.

Pro tips from us: Aim to keep your credit utilization low, ideally below 30% of your available credit limit. For example, if you have a $500 credit limit, try not to carry a balance over $150. Consistency and timeliness are far more important than the amount you borrow.

2. Demonstrating Stable Income and Employment

Lenders need assurance that you have the financial means to make your monthly car loan payments. This comes down to your income and employment situation. A steady job with a verifiable income stream will significantly improve your chances.

If you’re employed, gather pay stubs (usually for the last few months) and bank statements that show direct deposits. Lenders want to see consistency. If you’ve recently started a new job, it might be beneficial to wait a few months to show stability before applying for a loan.

Your debt-to-income (DTI) ratio is also a key metric. This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have sufficient income left after paying existing debts to handle a new car payment. For an 18-year-old, keeping other debts minimal is a huge advantage.

3. The Power of a Down Payment: Reducing Risk, Lowering Payments

A significant down payment is one of the most powerful tools an 18-year-old can use to secure a car loan. It directly addresses the lender’s risk concerns and offers numerous benefits to you.

When you put down a substantial amount of money upfront, the lender has less to lose if you default on the loan. This makes your application more attractive. A good rule of thumb is to aim for at least 10-20% of the car’s purchase price.

Beyond reducing risk for the lender, a larger down payment also reduces your total loan amount. This translates to lower monthly payments, less interest paid over the life of the loan, and potentially a shorter loan term. Saving diligently for this initial investment shows financial foresight and responsibility.

4. Considering a Co-signer: Sharing the Responsibility

If your credit history is thin or your income is not yet robust, bringing a co-signer on board can dramatically improve your chances of approval. A co-signer is someone, typically a parent or guardian with good credit and stable income, who agrees to be equally responsible for the loan.

The co-signer’s credit history and income are considered alongside yours, providing the lender with additional security. This can help you get approved for a loan you might not qualify for on your own, and potentially at a more favorable interest rate.

However, choosing a co-signer is a serious decision. The co-signer is legally obligated to make payments if you fail to. This can impact their credit score if payments are missed. Common mistakes to avoid are not fully understanding the co-signer’s responsibilities or taking their help for granted. Ensure open communication and a clear agreement on payment expectations to protect your relationship.

Navigating Loan Options: Types of Car Loans for Young Borrowers

When you’re ready to apply for a car loan at 18, understanding the different types of lenders and their offerings can help you find the best fit. Each option has its own advantages and potential drawbacks for young borrowers.

1. Traditional Bank Loans

Major banks are a common source for auto loans. They typically offer competitive interest rates to well-qualified borrowers. However, their lending criteria can be stricter, often requiring a more established credit history and higher income levels.

If you or your co-signer already have an existing relationship with a bank, such as a checking or savings account, it might be a good starting point. They might be more willing to work with existing customers.

2. Credit Union Loans

Credit unions are often a great option for young borrowers. As non-profit financial cooperatives, they tend to be more community-focused and may offer more flexible lending terms or slightly lower interest rates than traditional banks, especially for members.

To get a loan from a credit union, you usually need to become a member, which often involves meeting certain eligibility criteria (e.g., living in a specific area, working for a particular employer, or being part of an association). Membership is typically easy to obtain and can offer long-term benefits beyond just a car loan.

3. Dealership Financing

Many car dealerships offer financing directly through their own finance departments. This can be convenient, as you can arrange the loan at the same place you’re buying the car. Dealerships often work with multiple lenders (both captive finance companies associated with car brands and third-party banks) to find you a loan.

While convenient, dealership financing might sometimes come with higher interest rates, especially if you haven’t shopped around beforehand. It’s crucial to compare any offer from the dealership with pre-approvals you’ve received elsewhere.

4. Online Lenders

The digital age has brought a rise in online lenders that specialize in auto loans. These platforms can offer quick application processes and a wide range of loan options, sometimes even for borrowers with limited credit.

However, it’s essential to research online lenders thoroughly. Look for reputable companies with transparent terms and positive customer reviews. Always compare their rates and fees carefully with traditional institutions.

Step-by-Step: Successfully Getting a Car Loan at 18

Armed with knowledge about eligibility and loan types, let’s outline a practical, step-by-step approach to securing your first car loan at 18. This structured process will maximize your chances of approval and help you find the best possible terms.

Step 1: Understand Your Budget and Total Cost of Ownership

Before you even think about a specific car, determine how much you can truly afford. This isn’t just about the monthly car payment. Consider the total cost of ownership, which includes insurance, fuel, maintenance, and potential repairs.

Pro tips from us: Car insurance for an 18-year-old can be significantly more expensive than for older drivers. Get insurance quotes before you commit to a car to ensure the overall monthly cost fits comfortably within your budget. A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 15-20% of your gross monthly income.

Step 2: Build or Improve Your Credit Score

As discussed, this is foundational. If you haven’t started, get a secured credit card or become an authorized user. If you already have some credit, ensure all payments are made on time and keep your credit utilization low.

Regularly check your credit report (you can get one free report annually from each of the three major bureaus: Equifax, Experian, and TransUnion via AnnualCreditReport.com). Look for any errors and dispute them immediately, as inaccuracies can negatively impact your score.

Step 3: Save for a Substantial Down Payment

The more you can put down, the better. Start saving early and aggressively. Even a few thousand dollars can make a big difference in loan approval and terms. It demonstrates financial discipline and reduces the amount you need to borrow.

Step 4: Gather All Necessary Documents

Being prepared shows responsibility and speeds up the application process. You’ll typically need:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, bank statements, employer contact info)

- Proof of residence (utility bill, lease agreement)

- Social Security number

- References (sometimes required, especially with limited credit)

Step 5: Get Pre-Approved for a Loan

This is a critical step that empowers you as a buyer. Apply for pre-approval with a few different lenders (banks, credit unions, online lenders). Pre-approval means a lender has conditionally agreed to lend you a certain amount at a specific interest rate, subject to final verification.

With a pre-approval in hand, you know your budget and can walk into a dealership as a cash buyer. This gives you significant negotiation power on the car’s price, as you’re not reliant on their financing options.

Step 6: Shop Around for the Best Car Loan Rates

Don’t settle for the first offer. Compare interest rates, loan terms (e.g., 36, 48, 60 months), and any fees from multiple lenders. Even a small difference in interest rate can save you hundreds or thousands of dollars over the life of the loan.

When comparing offers, pay attention to the Annual Percentage Rate (APR), which includes the interest rate plus certain fees, giving you a truer picture of the loan’s total cost.

Step 7: Choose the Right Car

With your budget and pre-approval in hand, select a car that is reliable, affordable, and meets your needs. For a first car loan, it’s often wise to choose a used, dependable vehicle rather than stretching your budget for a brand-new model. Consider makes and models known for lower insurance costs and good fuel efficiency.

Common Pitfalls and How to Avoid Them When Getting a Car Loan at 18

While the goal is to get approved, it’s equally important to avoid financial traps that can turn your dream car into a burden. Young borrowers are particularly susceptible to certain pitfalls.

1. High-Interest Rates

With limited credit history, you might be offered higher interest rates. While it’s tempting to accept any approval, a high APR means you’ll pay significantly more over time. If rates are too high, consider waiting, building more credit, or increasing your down payment.

2. Long Loan Terms

A common tactic to make monthly payments seem affordable is to extend the loan term (e.g., 72 or 84 months). While this lowers your monthly payment, it dramatically increases the total interest paid and puts you at a higher risk of being "upside down" on your loan (owing more than the car is worth). Common mistakes to avoid are prioritizing a low monthly payment over the total cost of the loan. Aim for the shortest term you can comfortably afford.

3. Buying Too Much Car

It’s easy to get caught up in the excitement and opt for a car that’s beyond your financial means. Stick to your budget, which includes the total cost of ownership. Overspending on a car can strain your finances and hinder your ability to save or pursue other financial goals.

4. Ignoring the Fine Print

Always read the entire loan agreement carefully before signing. Understand all terms, conditions, fees, and penalties for late payments. Don’t be afraid to ask questions until everything is clear. If something seems unclear or too good to be true, it probably is.

5. Not Factoring in Car Insurance

As mentioned, insurance for an 18-year-old can be prohibitively expensive. Failing to get quotes beforehand can lead to sticker shock and make your car unaffordable. Always include insurance costs in your budget calculations. For more detailed guidance on managing vehicle expenses, you might find our article on Smart Budgeting for Your First Car Purchase helpful. (Internal Link 1)

Alternatives and Building Financial Prudence

If getting a car loan at 18 seems too challenging or the terms aren’t favorable, remember that you have other options. Patience and strategic financial planning can pay off immensely in the long run.

Consider saving up to buy an affordable, reliable used car with cash. This eliminates interest payments entirely and means you won’t have a monthly car payment burden. It’s a fantastic way to avoid debt and build savings.

Exploring public transportation, ride-sharing, or borrowing a family car are also viable short-term solutions. Focus on using this time to build a strong credit history, save money, and increase your income. By the time you’re 20 or 21, you’ll likely be in a much stronger financial position to secure a car loan with excellent terms. For further reading on financial responsibility, consider visiting reputable sites like the Consumer Financial Protection Bureau for resources on managing credit and debt. (External Link)

Moreover, building a solid financial foundation now will benefit you for years to come. Understanding credit, managing debt, and saving for future goals are invaluable skills. You might also find value in our article, The Ultimate Guide to Building Excellent Credit in Your Early Twenties, which offers more strategies for young adults. (Internal Link 2)

Conclusion: Driving Towards Financial Independence

So, can you take out a car loan at 18? Absolutely. It’s a journey that requires careful preparation, financial literacy, and a strategic approach, but it is entirely achievable. By focusing on establishing a positive credit history, demonstrating stable income, making a substantial down payment, and wisely considering a co-signer, you can significantly improve your chances of approval.

Remember to shop around for the best rates, understand all the terms, and avoid common pitfalls like excessively long loan terms or buying a car beyond your means. Your first car loan isn’t just about getting a set of wheels; it’s a foundational step in building your financial independence and creditworthiness. Approach it with knowledge and confidence, and you’ll be well on your way to enjoying the freedom of the open road responsibly. Start planning today, and you’ll be driving off the lot with a smart car loan that sets you up for future financial success.