Can I Use My Car to Get a Loan? A Comprehensive Guide to Auto-Secured Lending

Can I Use My Car to Get a Loan? A Comprehensive Guide to Auto-Secured Lending Carloan.Guidemechanic.com

Life often throws unexpected financial curveballs. From emergency medical bills to sudden home repairs or even a crucial business opportunity, sometimes you need quick access to funds. If you own a vehicle, you might be wondering: "Can I use my car to get a loan?" The answer is a resounding yes, but it comes with a unique set of considerations, benefits, and significant risks.

As an expert blogger and SEO content writer with years of experience navigating the complexities of personal finance, I’ve seen countless individuals explore this option. My goal with this in-depth guide is to provide you with all the essential information you need to make an informed decision, ensuring you understand the landscape of car-secured loans thoroughly. We’ll delve into the mechanics, the pros and cons, eligibility, the application process, and crucial advice to protect your financial well-being.

Can I Use My Car to Get a Loan? A Comprehensive Guide to Auto-Secured Lending

Understanding Car-Secured Loans: What Are They?

At its core, a car-secured loan, also known as an auto collateral loan or a title loan, is a type of secured loan where your vehicle serves as collateral. Unlike unsecured loans, which are based solely on your creditworthiness, secured loans require an asset to back the borrowed amount. If you fail to repay the loan according to the terms, the lender has the legal right to repossess and sell your car to recover their losses.

This fundamental difference is crucial. It means the lender takes on less risk, which can sometimes translate into more accessible funds or potentially better terms for borrowers who might not qualify for traditional unsecured loans due to credit history. However, it also places your valuable asset directly on the line.

How Do Car-Secured Loans Differ from Unsecured Loans?

The distinction between secured and unsecured loans is paramount in personal finance. An unsecured loan, like a personal loan based on credit score or a credit card, relies entirely on your promise to repay and your financial history. There’s no physical asset tied to the debt. If you default, the lender’s recourse is typically limited to reporting to credit bureaus, collections, or legal action, but they can’t seize an asset directly.

A secured loan, on the other hand, is directly linked to collateral. When you take out a mortgage, your house is the collateral. With an auto loan to buy a car, the car itself is the collateral. In the context of "using your car to get a loan," you’re leveraging an asset you already own outright or have significant equity in. This collateral provides a safety net for the lender, which significantly changes the lending dynamics.

Types of Loans Where Your Car is Collateral

While the umbrella term is "car-secured loan," there are a few distinct types you might encounter:

1. Auto Title Loans

This is perhaps the most common and widely recognized form of car-secured lending. With a title loan, you temporarily hand over your car title to the lender in exchange for a lump sum of cash. You retain possession of your car and can continue driving it, but the lender holds a lien on the title. Once the loan is fully repaid, the title is returned to you.

Title loans are often characterized by their speed and minimal credit checks, making them attractive to individuals with poor credit. However, based on my experience, they also typically come with extremely high-interest rates and short repayment periods, often 15 to 30 days. This combination can make them incredibly challenging to repay, leading to a cycle of debt.

2. Car Equity Loans (Refinancing)

A car equity loan is essentially a form of refinancing where you borrow against the equity you’ve built in your vehicle. If you’ve been making payments on your car loan for some time, or if you bought your car outright, you have equity – the difference between your car’s market value and what you still owe on it (if anything).

Unlike title loans, which are usually for smaller, short-term amounts, car equity loans can sometimes offer larger sums and potentially more favorable interest rates, especially if you have a decent credit score. You’re effectively taking out a new loan using your car as collateral, often with the original lender or a new one, to free up cash.

3. Auto Pawn Loans

While less common for cars than for smaller valuable items, auto pawn loans exist. In this scenario, you physically surrender your vehicle to the lender (pawn shop) for the duration of the loan. You cannot drive your car while the loan is active. Upon full repayment, your car is returned. These loans also tend to have high costs and short terms, and the inconvenience of not having your vehicle is a major drawback.

The "Can I Use My Car" Question – A Deeper Dive

So, you understand the types, but under what specific conditions can you actually leverage your vehicle for a loan? It’s not just about owning a car; several factors come into play.

When Is It Possible to Use Your Car for a Loan?

- Clear Title/Significant Equity: For a title loan, you typically need to own your car outright, meaning you have a "clear title" free of any liens. For a car equity loan, you need to have substantial equity built up. Lenders won’t lend you more than your car is worth.

- Vehicle Condition and Value: Your car’s make, model, year, mileage, and overall condition significantly impact its market value. Lenders will appraise your vehicle to determine how much they are willing to lend against it. Older, high-mileage, or damaged vehicles will yield less.

- Proof of Income: Even with collateral, lenders want to see that you have a reliable source of income to repay the loan. They need assurance that you can meet the scheduled payments without defaulting.

- Identification: You’ll need a valid government-issued ID, like a driver’s license, to prove your identity.

Who Offers These Loans?

The landscape of lenders offering car-secured loans is diverse:

- Specialized Title Loan Companies: These are often storefront operations or online platforms that focus specifically on high-interest, short-term title loans.

- Banks and Credit Unions: Traditional financial institutions are more likely to offer car equity loans or refinancing options, usually with better rates and terms, especially if you have good credit. They generally avoid the high-risk, high-interest title loan model.

- Online Lenders: A growing number of online lenders offer various forms of secured and unsecured loans. Some specialize in title loans, while others offer more traditional car equity loans.

The Pros of Using Your Car as Collateral

While the risks are substantial, there are specific situations where using your car as collateral might seem like a viable, or even necessary, option.

1. Access to Funds When Other Options are Limited

For individuals with poor credit scores or those who have been rejected by traditional lenders, a car-secured loan can be one of the few avenues to access needed cash quickly. The collateral reduces the lender’s risk, making them more willing to lend.

2. Potentially Lower Interest Rates (Compared to Unsecured Loans for Bad Credit)

This is a nuanced point. Compared to unsecured personal loans specifically designed for bad credit (which can also have very high APRs), a car equity loan from a reputable lender might offer a slightly better rate because of the collateral. However, this absolutely does not apply to most title loans, which typically carry exorbitant interest rates.

3. Faster Approval Process

Because less emphasis is placed on a lengthy credit check and more on the value of your collateral and your ability to repay, the approval process for car-secured loans can be significantly quicker than traditional loans. Funds can often be disbursed within the same day or a few business days.

4. Credit Score Might Be Less of a Barrier

If your credit history is less than perfect, a car-secured loan can be an option when other doors are closed. Lenders are more focused on the value of your vehicle and your income stability. This doesn’t mean your credit score is irrelevant, but it often plays a secondary role compared to unsecured lending.

The Cons and Significant Risks of Using Your Car as Collateral

This section is critical. Based on my experience, the risks associated with car-secured loans, particularly title loans, are often underestimated by borrowers. Proceed with extreme caution.

1. Risk of Losing Your Car (Repossession)

This is the most significant and immediate risk. If you default on your loan payments, the lender has the legal right to repossess your vehicle without a court order in many states. Losing your car can cripple your ability to get to work, run errands, and maintain your daily life, creating a cascade of further financial problems.

2. High-Interest Rates (Especially Title Loans)

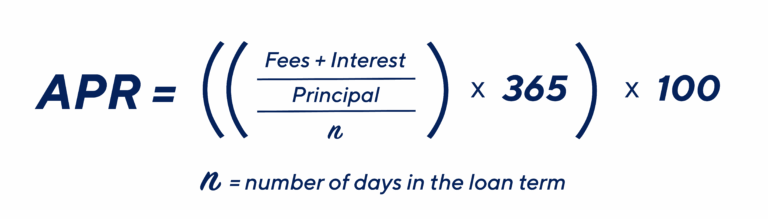

Title loans are notorious for their astronomically high Annual Percentage Rates (APRs), often ranging from 200% to 400% or even higher. To put that into perspective, a typical credit card APR might be 15-30%. These rates make it incredibly difficult to repay the principal, often leading to borrowers extending or "rolling over" the loan, incurring more fees and interest.

3. Fees and Hidden Costs

Beyond the high-interest rates, many car-secured loans come with various fees. These can include processing fees, document fees, late payment fees, repossession fees, and even storage fees if your car is repossessed. These additional charges quickly inflate the total cost of the loan.

4. Short Repayment Terms

Title loans, in particular, often have very short repayment terms, sometimes as little as 15 or 30 days. This creates immense pressure to repay a large sum of money in a very short timeframe, which is often unrealistic for borrowers already facing financial difficulties.

5. Impact on Credit Score if Not Repaid

While some title loan lenders don’t report to major credit bureaus, defaulting on any loan can still negatively impact your credit. If the lender does report, or if they pursue legal action (which can result in a judgment appearing on your credit report), your score will suffer. Furthermore, if you take out a car equity loan from a traditional lender, timely payments can help your credit, but defaults will severely damage it.

6. Predatory Lending Practices

Common mistakes to avoid are falling victim to predatory lenders. Some companies offering car-secured loans, particularly title loans, may engage in practices designed to trap borrowers in a cycle of debt. This can include aggressive sales tactics, lack of transparency about fees, and encouraging rollovers that pile on more interest. Always research a lender thoroughly and check reviews.

Eligibility Requirements: Are You Qualified?

Before even considering an application, ensure you meet the basic criteria.

1. Vehicle Ownership and Clear Title

For a title loan, you generally must own your vehicle outright, free of any existing loans or liens. For an equity loan, you need substantial equity. The car title must be in your name.

2. Vehicle Value and Condition

Lenders will appraise your car. They typically lend only a percentage of its wholesale market value, not its retail value. The loan amount will depend on your car’s make, model, year, mileage, and overall condition.

3. Proof of Income

You’ll need to demonstrate a steady income source to assure the lender you can make the payments. This could be pay stubs, bank statements, or proof of benefits.

4. Valid Identification and Insurance

A valid driver’s license or state-issued ID is mandatory. Some lenders may also require proof of valid car insurance.

The Application Process: A Step-by-Step Guide

If you’ve weighed the pros and cons and decided to proceed, here’s what the typical application process looks like:

- Research Lenders: Don’t jump at the first offer. Compare interest rates, fees, repayment terms, and customer reviews from several lenders. Look for transparency.

- Gather Documents: Prepare your car title, government-issued ID, proof of income, proof of residency, and vehicle registration/insurance.

- Apply: You can apply online, in person at a storefront, or over the phone. You’ll fill out an application form providing personal and vehicle details.

- Vehicle Inspection/Appraisal: The lender will inspect your car to verify its condition and determine its market value. This can be done in person or sometimes through photos/video for online lenders.

- Review Offer and Terms: If approved, you’ll receive a loan offer detailing the principal amount, interest rate, APR, fees, and repayment schedule. Pro tip: Read every single line of this agreement carefully. Understand the total cost of the loan, not just the monthly payment.

- Sign Agreement: If you agree to the terms, you’ll sign the loan agreement. For a title loan, you’ll endorse your car title over to the lender, who will place a lien on it.

- Receive Funds: Once everything is signed, the funds are typically disbursed quickly, often within the same day or the next business day, either via direct deposit, check, or cash.

Important Considerations Before You Apply (E-E-A-T Focus)

Before you commit, take a moment for critical self-reflection and due diligence. This is where experience truly matters.

- Evaluate Your Financial Situation Thoroughly: Be brutally honest with yourself about your ability to repay the loan. Can you comfortably make the payments without jeopardizing other essential expenses? Remember, failure to pay means losing your car.

- Explore Alternatives First: Based on my experience, a car-secured loan should often be a last resort. Have you exhausted all other options? We’ll discuss alternatives below.

- Understand the APR, Not Just the Interest Rate: Lenders are legally required to disclose the Annual Percentage Rate (APR), which includes the interest rate plus most fees. This is the true cost of borrowing and is often much higher than the stated interest rate alone.

- Read the Loan Agreement (Every Single Word): This cannot be stressed enough. Common mistakes to avoid include skimming the fine print. Look for prepayment penalties, late fees, rollover clauses, and exactly what happens in case of default. Don’t be afraid to ask questions until you fully understand everything.

- Impact on Credit: While some title loan lenders don’t report to credit bureaus, taking out any form of significant debt can indirectly impact your financial standing. Defaulting will almost certainly have a negative impact, either directly through reporting or through subsequent collection actions.

- Repayment Strategy: Develop a clear plan for how you will repay the loan on time. Don’t rely on future uncertain income.

Alternatives to Car-Secured Loans

Before you put your car at risk, consider these potentially safer and less costly alternatives:

1. Personal Unsecured Loans

If your credit isn’t terrible, a traditional personal loan from a bank, credit union, or online lender might be a better option. Interest rates are usually much lower, and your car isn’t on the line.

2. Borrowing from Friends or Family

While it can be awkward, borrowing from loved ones can offer interest-free or low-interest terms and more flexible repayment schedules. Just ensure you treat it professionally with a written agreement to avoid damaging relationships.

3. Credit Cards (If Used Wisely)

For smaller amounts and if you have available credit, a credit card can be cheaper than a title loan, especially if you can pay it off quickly. Be mindful of high APRs if you carry a balance.

4. Payment Plans with Creditors

If you’re facing overdue bills, contact your creditors directly. Many are willing to work out a payment plan or temporary hardship arrangement rather than send your account to collections.

5. Debt Consolidation

If you have multiple high-interest debts, a debt consolidation loan (if you qualify) or working with a credit counseling agency can simplify payments and potentially reduce overall interest.

6. Non-Profit Credit Counseling

Organizations like the National Foundation for Credit Counseling (NFCC) offer free or low-cost advice on managing debt, budgeting, and exploring alternatives to high-cost loans. This is an excellent external resource to consider for unbiased financial guidance. (External Link: https://www.nfcc.org/)

Making an Informed Decision

Using your car to get a loan is a significant financial decision with potentially severe consequences. While it offers a pathway to quick cash when other options are scarce, the risks, particularly with high-cost title loans, are substantial. The possibility of losing your primary mode of transportation can create an even deeper financial crisis.

Always prioritize understanding the full terms and costs involved, and exhaust all safer alternatives before considering a car-secured loan. Due diligence, careful calculation, and a clear repayment strategy are not just recommendations – they are necessities. Your financial future, and your car, depend on it.

Conclusion

In summary, yes, you can use your car to get a loan, primarily through auto title loans or car equity loans. These options provide quick access to funds, especially for those with less-than-perfect credit. However, they come with significant drawbacks, most notably the high risk of repossession and exorbitant interest rates, particularly with title loans.

My strongest advice, based on years of observing financial trends and individual outcomes, is to approach car-secured lending with extreme caution. Understand every clause in the loan agreement, calculate the total cost, and critically assess your ability to repay. Most importantly, explore all other financial avenues before putting your valuable vehicle at risk. Your car is often more than just an asset; it’s a lifeline. Protect it wisely.