Can You Combine 2 Car Loans? Unlocking Your Path to Simpler Finances and Savings

Can You Combine 2 Car Loans? Unlocking Your Path to Simpler Finances and Savings Carloan.Guidemechanic.com

Are you juggling payments for two separate car loans every month? Perhaps you’re tired of tracking different due dates, managing varying interest rates, and feeling the pinch of multiple financial commitments. If this sounds like your current situation, you’re likely wondering: "Can I combine my two car loans into one?"

The short answer is yes, you can – but it’s not always as simple as literally "merging" two existing auto loans into a single new one that covers both vehicles directly. The process often involves strategic refinancing or debt consolidation, which can lead to significant financial benefits if done correctly. This comprehensive guide will explore the various pathways to consolidating your car loan debt, helping you understand the "how," "when," and "why" behind this crucial financial move.

Can You Combine 2 Car Loans? Unlocking Your Path to Simpler Finances and Savings

Why Even Consider Combining Two Car Loans? The Benefits You Could Reap

Before diving into the mechanics, let’s understand why you might want to explore combining your car loans. From my experience helping countless individuals navigate their debt, the motivation typically boils down to a few compelling advantages.

1. Simplified Payments and Reduced Stress

Managing two separate car payments means two different due dates, two different interest rates, and two different principal balances to track. This complexity can be a significant source of stress and can easily lead to missed payments if you’re not meticulous. By consolidating, you boil everything down to a single, manageable monthly payment. This simplification can dramatically reduce mental clutter and free up valuable time you might otherwise spend on financial administration.

2. Potential for Lower Interest Rates

When you took out your original car loans, your credit score, financial situation, or even market interest rates might have been different. If your credit has improved since then, or if current market rates are lower, consolidating could allow you to secure a single loan with a significantly lower Annual Percentage Rate (APR). A lower APR translates directly into less money paid in interest over the life of the loan, saving you hundreds or even thousands of dollars.

3. Lower Monthly Payments

A common goal for those considering consolidation is to reduce their overall monthly outflow. By extending the loan term or securing a better interest rate, you can often achieve a lower combined monthly payment. This frees up cash flow, which can be crucial for meeting other financial obligations, building an emergency fund, or simply enjoying a bit more breathing room in your budget. However, it’s vital to balance a lower payment with the total interest paid, as extending the term too much can sometimes mean paying more interest overall.

4. Faster Debt Freedom (If Managed Strategically)

While some consolidate to lower monthly payments by extending the loan term, others use it as a springboard for faster debt payoff. If you consolidate into a loan with a lower interest rate, you could potentially keep your monthly payment similar to what you were paying before, but more of that payment would go towards the principal. This accelerates your path to becoming debt-free, allowing you to reallocate those funds to other financial goals sooner.

Understanding the "How": Methods for Combining Your Car Loans

It’s important to clarify that directly "merging" two auto loans secured by two different vehicles into a single new auto loan that lists both cars as collateral is extremely rare, if not impossible, with most traditional lenders. Auto loans are typically tied to a single vehicle identification number (VIN). Instead, "combining" or "consolidating" car loans usually refers to different financial strategies that achieve the effect of a single payment or a simplified debt structure.

Let’s explore the most viable methods based on my professional experience.

Method 1: Refinancing Each Car Loan Individually for Better Terms

This isn’t a true "combination" into one single loan, but it’s often the most practical and beneficial first step. If your goal is to reduce interest rates or monthly payments on both vehicles, you can refinance each car loan separately.

How it works: You apply for a new auto loan for Car A with a different lender (or even your current one if they offer better terms) and do the same for Car B. While you’ll still have two separate loans, the new terms might significantly improve your financial standing for both.

Why it’s effective: This approach works well if you’ve improved your credit score, market rates have dropped, or you simply found more competitive lenders since taking out your original loans. It allows you to tailor the best possible terms for each vehicle based on its individual value, mileage, and your specific financial profile. You maintain the secured nature of auto loans, which generally means lower interest rates than unsecured options.

Method 2: Consolidating with a Personal Loan (Unsecured)

This method offers a true consolidation into a single loan, but it changes the nature of your debt. A personal loan is an unsecured loan, meaning it’s not backed by collateral like your cars.

How it works: You apply for a personal loan large enough to cover the remaining balances of both your car loans. If approved, the personal loan funds are used to pay off both existing auto loans. You then have a single monthly payment for the personal loan.

Pros:

- One Payment: You achieve the primary goal of having a single payment to manage.

- Flexibility: Personal loans can sometimes have more flexible terms than auto loans.

- No Collateral Risk: Your cars are no longer directly tied to the loan; if you default, the lender cannot repossess your vehicles.

Cons:

- Higher Interest Rates: Because personal loans are unsecured, lenders take on more risk. This often translates to higher interest rates compared to secured auto loans, especially if your credit isn’t stellar.

- Credit Requirements: You’ll need a good to excellent credit score to qualify for a personal loan with a favorable interest rate that makes consolidation worthwhile.

- Loan Amount Limits: Lenders may have caps on personal loan amounts, which could be an issue if your combined car loan balances are very high.

Pro tips from us: Always compare the Annual Percentage Rate (APR) of the personal loan to the weighted average APR of your existing car loans. If the personal loan’s APR is higher, this strategy might cost you more in the long run. Consider this option carefully and only if the interest rate is genuinely beneficial.

Method 3: Utilizing a Home Equity Loan or Line of Credit (HELOC)

If you own a home and have accumulated significant equity, a home equity loan or a Home Equity Line of Credit (HELOC) can be a powerful tool for debt consolidation.

How it works: You borrow against the equity in your home. These funds are then used to pay off both of your car loans. You’ll then have a single, new loan payment tied to your home equity.

Pros:

- Lower Interest Rates: Home equity products are secured by your home, making them less risky for lenders. This often results in significantly lower interest rates compared to auto loans or personal loans, especially in a favorable rate environment.

- Tax Deductibility: In some cases, the interest paid on a home equity loan can be tax-deductible (consult a tax advisor for specifics).

- Larger Loan Amounts: You can typically borrow larger sums with home equity, making it suitable for consolidating substantial car loan balances.

Cons:

- Puts Your Home at Risk: This is the most significant drawback. If you default on your home equity loan, your home could be foreclosed upon. This turns unsecured car debt (after it’s paid off) into debt secured by your primary residence.

- Fees: Home equity loans often come with closing costs and other fees, similar to a mortgage.

- Longer Terms: While lower monthly payments are appealing, home equity loans often have much longer terms (10-30 years), meaning you could be paying for your cars for a very long time, significantly increasing the total interest paid.

Common mistakes to avoid are: Using your home as collateral without fully understanding the risks. Based on my experience, many people get caught up in the low monthly payment and forget the long-term implications and the increased risk to their most valuable asset.

Eligibility Criteria: Are You a Good Candidate for Consolidation?

Regardless of the method you choose, certain factors will determine your eligibility and the attractiveness of the loan terms you’re offered.

1. Credit Score

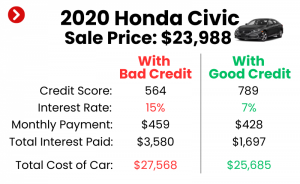

Your credit score is paramount. A good to excellent score (typically 670 and above) indicates to lenders that you are a responsible borrower, making you eligible for the best interest rates. If your score has improved since your original car loans, you’re in an excellent position to benefit from consolidation.

2. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on new debt. A DTI below 36% is generally considered favorable, though some lenders may go higher. For more on improving your credit score and managing your DTI, check out our guide on and .

3. Loan-to-Value (LTV) Ratio for Refinancing

If you’re refinancing an individual car loan, lenders will look at the vehicle’s market value versus the outstanding loan balance. If you owe significantly more than the car is worth (you’re "upside down" or have negative equity), refinancing can be challenging. Most lenders prefer an LTV of 120% or less.

4. Vehicle Age and Mileage

For individual car loan refinancing, older vehicles or those with very high mileage may be harder to refinance, as lenders perceive them as higher risk due to accelerated depreciation and potential maintenance issues. Some lenders have limits, such as a maximum age of 7-10 years or 100,000-120,000 miles.

The Step-by-Step Process to Combine Your Car Loans

Ready to take control of your car loan debt? Here’s a structured approach to guide you through the consolidation process.

Step 1: Assess Your Current Loans and Financial Situation

Gather all the details for both of your car loans: current outstanding balances, interest rates (APR), remaining loan terms, and minimum monthly payments. Take stock of your current income, expenses, and overall financial health. Understanding your starting point is crucial for making informed decisions.

Step 2: Check Your Credit Score

Obtain your credit report and score from all three major credit bureaus (Experian, Equifax, TransUnion). You can do this for free once a year at AnnualCreditReport.com. Identify any errors and understand where you stand. A better credit score will open doors to better loan offers.

Step 3: Research and Compare Lenders

This is a critical step that many people rush through. Don’t just go with your current bank. Shop around extensively. Look at credit unions, online lenders, and traditional banks. Compare interest rates, loan terms, fees (origination fees, prepayment penalties), and customer service. Each lender has different criteria and offers.

Step 4: Gather Necessary Documentation

Once you’ve identified potential lenders, prepare the documents they’ll likely request. This typically includes proof of income (pay stubs, tax returns), identification (driver’s license), proof of residence, and details about your current car loans (account numbers, payoff amounts).

Step 5: Apply for the New Loan

Submit applications to 2-3 top prospective lenders. Applying to multiple lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model) will typically be treated as a single hard inquiry on your credit report, minimizing the impact.

Step 6: Review Offers Carefully

Don’t just look at the monthly payment. Scrutinize the APR, the total cost of the loan over its entire term, and any hidden fees. Understand the difference between the advertised rate and your personalized rate. Ensure the new loan truly benefits you more than your existing setup.

Step 7: Finalize the Loan and Pay Off Old Debts

Once you accept an offer, the new lender will typically disburse the funds directly to your old car loan lenders to pay off those balances. Confirm that your old accounts are closed and that you receive confirmation of zero balance. Keep all documentation for your records.

Important Considerations Before You Act

While the benefits of combining car loans can be substantial, it’s essential to approach this decision with careful consideration.

Impact on Your Credit Score

Applying for new loans will result in hard inquiries on your credit report, which can temporarily lower your score by a few points. However, if you manage the new loan responsibly, your score will recover and likely improve over time as you demonstrate good payment habits and reduce your overall debt burden.

Potential Fees and Closing Costs

New loans, especially personal loans or home equity products, can come with various fees, such as origination fees, application fees, or closing costs. Factor these into your calculations to ensure the consolidation is still financially advantageous. Sometimes, these fees can negate some of the interest savings.

The True Cost: Total Interest Paid vs. Monthly Payment

It’s easy to get fixated on a lower monthly payment. However, extending your loan term significantly to achieve that lower payment often means paying more in total interest over the life of the loan. Always calculate the total cost of the new consolidated loan, including all interest and fees, and compare it to the remaining total cost of your current loans. Sometimes, a slightly higher monthly payment for a shorter term is the smarter financial move.

Car Depreciation and Loan-to-Value (LTV)

Cars are depreciating assets. Be mindful of your vehicle’s value, especially if you’re refinancing. If you consolidate using a personal loan or home equity, you decouple the debt from the car’s value, which can be both a blessing and a curse. If you refinance an individual car, ensuring you don’t go "upside down" (owe more than the car is worth) is crucial for future financial flexibility.

Alternatives to Combining Car Loans

If combining your car loans doesn’t seem like the right fit for your situation, don’t despair. There are other strategies you can employ to manage your debt effectively.

1. Aggressive Repayment on One Loan (Debt Snowball/Avalanche)

Focus all your extra payments on one of your car loans, usually the one with the smallest balance (snowball method) or the highest interest rate (avalanche method). Once that loan is paid off, roll those payments into the next loan. This method provides psychological wins and reduces total interest over time.

2. Budgeting and Cutting Expenses

Sometimes, the simplest solution is the most effective. A thorough review of your budget can reveal areas where you can cut expenses, freeing up more money to put towards your existing car loan payments. This doesn’t change your loan structure but can significantly accelerate debt repayment.

3. Selling One Car

If having two cars is a luxury you can’t comfortably afford, or if one vehicle is rarely used, selling one could be a viable option. Use the proceeds to pay off its loan entirely, or at least a significant portion, and then focus on the remaining vehicle. This can dramatically reduce your debt burden and monthly expenses.

Conclusion: Take Control of Your Car Loan Debt

Combining two car loans isn’t a single, straightforward transaction, but rather a strategic approach to managing your automotive debt. Whether you choose to refinance each car individually for better terms, consolidate with a personal loan, or leverage your home equity, the ultimate goal is to simplify your finances, reduce your interest burden, and achieve financial peace of mind.

Based on my experience, the most successful consolidations come from thorough research, careful comparison, and a clear understanding of your financial goals. Don’t rush the process, and always prioritize the total cost of the loan over the entire term, not just the appealing monthly payment. By taking these steps, you can effectively take control of your car loan debt and drive towards a more stable financial future.

Are you ready to explore your options? Start by assessing your current loans and credit score today! The path to simplified payments and potential savings is within reach.