Can You Combine Two Car Loans? Your Ultimate Guide to Smarter Auto Debt Management

Can You Combine Two Car Loans? Your Ultimate Guide to Smarter Auto Debt Management Carloan.Guidemechanic.com

Are you juggling two car payments every month, perhaps for your daily commuter and a family SUV? Maybe you co-signed for a child’s vehicle, or simply found yourself needing a second set of wheels sooner than expected. The financial reality of managing multiple auto loans can be a complex and sometimes stressful affair. You might be asking yourself, "Can I combine two car loans into one simpler payment?"

This is a question many car owners ponder, and it’s a smart one to ask. While the idea of literally merging two separate car titles under a single new auto loan is generally not how standard auto lending works, there are powerful strategies to effectively combine the debt or streamline your payments to achieve financial relief and simplify your life.

Can You Combine Two Car Loans? Your Ultimate Guide to Smarter Auto Debt Management

As an expert blogger and professional SEO content writer with years of experience navigating the intricacies of personal finance, I’ve seen firsthand how confusing this can be. My goal in this comprehensive guide is to cut through the jargon, provide actionable insights, and equip you with the knowledge to make the best decision for your financial situation. We’ll explore the real meaning behind "combining" car loans, the methods available, and the pros and cons of each, ensuring you get real value and clarity.

What Does "Combining Car Loans" Actually Mean? Unpacking the Concept

When people ask if they can "combine two car loans," they’re usually looking for one of two things:

- Simplifying Payments: The desire to make a single, manageable payment instead of tracking two separate due dates and amounts.

- Saving Money: The hope of securing a lower overall interest rate, reducing the total amount paid over time, or lowering monthly outgoings.

It’s crucial to understand that a traditional auto lender typically secures a loan against a single vehicle’s title. This means getting one new auto loan that is secured by two different cars is generally not an option for most consumers. Each car is a distinct asset.

However, the good news is that there are several effective financial strategies that achieve the effect of combining your car loan debt, leading to simplified payments and potential savings. These methods fall under the umbrella of debt consolidation or strategic refinancing. We’ll delve into these powerful tools in detail.

Why Would You Consider Combining Your Car Loan Debt? The Driving Forces

There are compelling reasons why someone might explore consolidating their car loan debt. Based on my experience, the motivation usually stems from a desire for greater financial control and efficiency.

1. Simplify Your Financial Life

Managing multiple loan payments can be a headache. You have different due dates, different interest rates, and different lenders to keep track of. Consolidating these debts into a single payment significantly streamlines your monthly financial routine, reducing the chance of missed payments and the associated fees.

2. Potentially Lower Your Overall Interest Rate

This is often the primary driver for many. If your credit score has improved since you took out your original loans, or if market rates have dropped, you might qualify for a new loan with a much lower interest rate. A lower rate across the board means you pay less money in interest over the life of the loan.

3. Reduce Your Monthly Payment

By extending the loan term or securing a lower interest rate, you can often decrease the total amount due each month. This can free up cash flow, providing much-needed breathing room in your budget, especially if you’re facing other financial pressures.

4. Improve Your Debt-to-Income (DTI) Ratio

While consolidating debt doesn’t magically eliminate it, securing a lower monthly payment can improve your DTI ratio in the eyes of future lenders. A better DTI can be beneficial if you plan to apply for a mortgage or other significant loans down the line.

5. Gain Better Loan Terms

Perhaps one of your current loans has unfavorable terms, like a high penalty for early repayment or restrictive clauses. Consolidating can allow you to escape these terms and secure a new loan with conditions that better suit your financial goals.

Common Scenarios Where Combining Makes Sense

From years in the financial industry, I’ve observed several common situations where people consider consolidating their car loan debt:

- You Purchased a Second Vehicle: Perhaps you bought a new family car, or an additional work vehicle, and now have two separate auto loans to manage.

- You Co-Signed for Someone Else: If you co-signed a loan for a family member or friend, and now find yourself responsible for payments, combining or consolidating might be a way to manage that obligation more effectively.

- Credit Score Improvement: Your credit score has significantly improved since you took out your original loans, making you eligible for better interest rates.

- Interest Rate Fluctuations: General interest rates have dropped, presenting an opportunity to refinance at a lower rate.

- Budget Strain: You’re finding it difficult to manage two separate payments, and need to reduce your monthly financial commitments.

These scenarios highlight the practical need for flexible financial solutions when dealing with multiple vehicle debts.

Methods for Effectively Combining Car Loan Debt

While you can’t typically get a single auto loan for two separate cars, you can effectively combine the debt or streamline your payments through several proven methods. Let’s explore each in depth.

Method 1: Refinancing One or Both Car Loans Individually

This is often the most straightforward approach, though it doesn’t result in a single payment for both cars unless you only had one car loan initially. If you have two separate auto loans, you would treat each one independently.

How it works:

You apply for a new car loan to pay off an existing car loan. The new loan will ideally have a lower interest rate or more favorable terms. You can do this for one car, or for both cars. The goal is to optimize each loan separately.

Pro tips from us:

Focus on the car loan with the highest interest rate first, as this will yield the most significant savings. If both loans have high rates, consider refinancing both, even if it means still having two separate payments, but at much better terms.

Example:

Let’s say you have Loan A at 7% APR and Loan B at 5% APR. If you can refinance Loan A down to 4% APR, you’ve saved a substantial amount of money. You would still have two distinct car payments, but your overall cost of borrowing would be significantly reduced.

Eligibility:

Lenders will look at your credit score, debt-to-income ratio, the age and mileage of your vehicle, and the loan-to-value (LTV) ratio. A car that is too old or has very high mileage might be difficult to refinance.

Method 2: Using a Personal Loan for Debt Consolidation

This method is perhaps the closest you can get to "combining" two car loans into a single payment. A personal loan is typically an unsecured loan, meaning it’s not backed by collateral like your car or home.

How it works:

You apply for a personal loan large enough to cover the outstanding balances of both your existing car loans. If approved, the personal loan funds are used to pay off both auto loans entirely. You then make a single monthly payment to the personal loan lender.

Benefits:

- One Payment: This is the primary advantage, simplifying your finances immensely.

- Potentially Lower Interest: If your credit score is excellent, you might qualify for a personal loan interest rate that is lower than the combined average of your car loans.

- Unsecured Debt: Since it’s unsecured, your cars are no longer collateral for the debt.

Common mistakes to avoid are:

Taking out a personal loan with a higher interest rate than your current car loans. This would defeat the purpose and cost you more money in the long run. Also, be wary of extending the loan term so much that you end up paying more interest overall, even with a lower monthly payment.

Eligibility:

Personal loan eligibility heavily depends on your credit score, income, and existing debt. Lenders want to see a strong repayment history and a manageable debt-to-income ratio.

Method 3: Home Equity Loan or Home Equity Line of Credit (HELOC)

If you own a home and have significant equity, a home equity loan or HELOC can be a powerful tool for debt consolidation. This is a secured loan, using your home as collateral.

How it works:

You borrow against the equity in your home. The funds from the home equity loan or HELOC are then used to pay off your existing car loans. You will then have one payment for your home equity debt, separate from your primary mortgage.

Benefits:

- Potentially Very Low Interest Rates: Because your home secures the loan, interest rates for home equity products are often much lower than those for auto loans or unsecured personal loans.

- Tax Deductible Interest: In some cases, the interest on a home equity loan can be tax-deductible (consult a tax professional).

Crucial Warning:

This is a significant step with substantial risk. Pro tips from us: Never use your home as collateral lightly. If you default on a home equity loan, you could lose your home. Based on my experience, this option should only be considered if you have a very stable financial situation and are confident in your ability to make payments. It’s not for everyone.

Eligibility:

Requires substantial home equity, a good credit score, and a stable income. Lenders will assess your overall financial health and the value of your home.

The Eligibility Checklist: Are You a Good Candidate for Combining?

Before diving into applications, it’s wise to assess your own financial standing. Lenders will scrutinize several key factors.

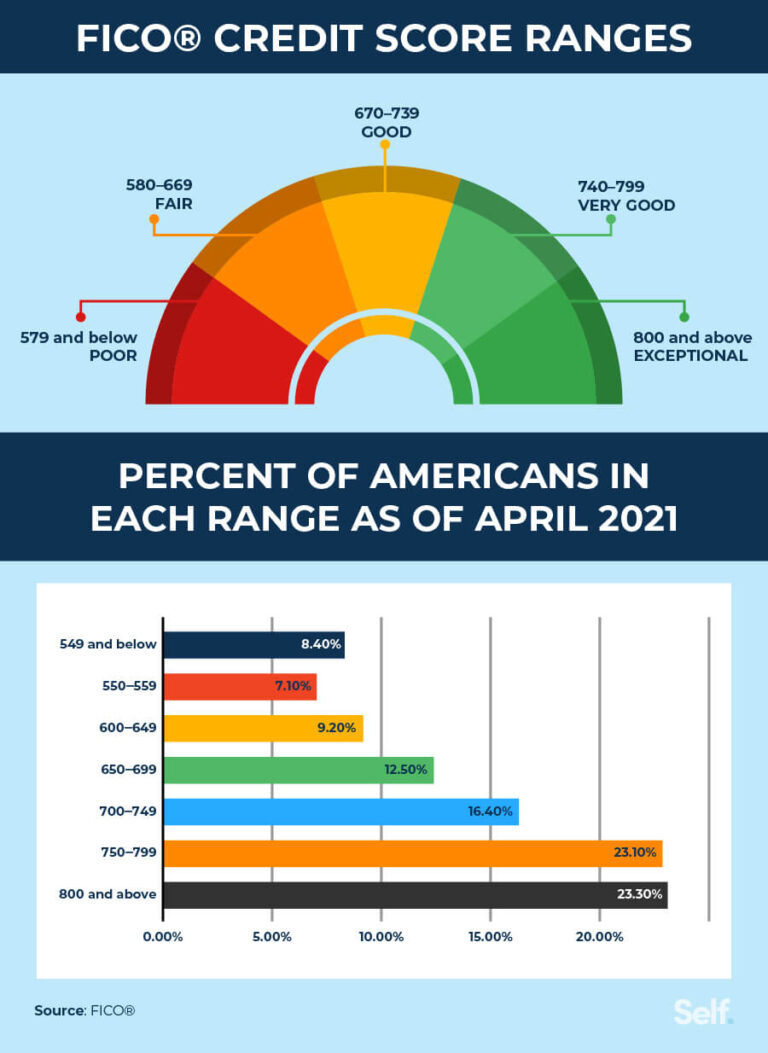

1. Your Credit Score

This is paramount. A good to excellent credit score (typically 670 and above) significantly increases your chances of approval for a new loan with favorable terms. Lenders see a higher score as an indication of responsible borrowing. If your score has improved since your original car loans, you’re in a strong position.

2. Debt-to-Income (DTI) Ratio

Your DTI is the percentage of your gross monthly income that goes towards debt payments. Lenders prefer a DTI of 36% or lower, though some may go up to 43%. A lower DTI indicates you have more disposable income to handle new debt.

3. Loan-to-Value (LTV) Ratio (for Refinancing)

When refinancing a car, lenders look at how much you owe on the car versus its current market value. If your car is "upside down" (you owe more than it’s worth), refinancing can be challenging. Lenders typically prefer an LTV of 100% or less.

4. Vehicle Age and Mileage (for Refinancing)

Most lenders have restrictions on the age and mileage of vehicles they will refinance. Older cars or those with very high mileage are often seen as higher risk due to depreciation and potential mechanical issues.

5. Stable Income and Employment History

Lenders want assurance that you have a steady income stream to make your payments. A consistent employment history demonstrates financial stability.

The Step-by-Step Process: Your Roadmap to Consolidation

Once you’ve determined that combining your car loan debt is a viable option for you, follow these steps to navigate the process effectively.

Step 1: Assess Your Current Loans

Gather all the details for both your existing car loans. This includes:

- Current outstanding balance for each

- Interest rate (APR) for each

- Remaining loan term for each

- Monthly payment for each

- Any prepayment penalties (though rare for auto loans, it’s good to check)

- Lender contact information

This comprehensive overview will be your baseline for comparison.

Step 2: Check Your Credit Score

Before applying anywhere, get a free copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your credit score. You can often get a free score from your bank, credit card company, or services like Credit Karma. Knowing your score helps you gauge what kind of rates you might qualify for. If your score isn’t where you want it to be, consider taking steps to improve it before applying. For more details on improving your credit score, check out our guide on .

Step 3: Shop Around for Lenders

Don’t settle for the first offer you receive. Research and compare offers from various financial institutions:

- Banks: Both large national banks and smaller local banks.

- Credit Unions: Often offer competitive rates and personalized service, especially if you’re a member.

- Online Lenders: Many reputable online platforms specialize in personal loans and auto loan refinancing.

Get pre-qualified if possible. This often involves a "soft" credit inquiry, which doesn’t harm your credit score, and gives you an idea of potential rates.

Step 4: Gather Required Documents

Once you’re ready to apply, lenders will typically ask for:

- Proof of identity (driver’s license)

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bill)

- Current loan statements for the car loans you wish to consolidate

- Vehicle information (VIN, mileage, make, model)

Having these ready will expedite the application process.

Step 5: Apply and Review Offers

Submit your formal applications. This will typically involve a "hard" credit inquiry, which might temporarily ding your credit score by a few points. Carefully review each offer, paying close attention to:

- Interest Rate (APR): The true cost of borrowing.

- Loan Term: How long you’ll be making payments.

- Monthly Payment: The new amount you’ll pay.

- Total Cost of Loan: Calculate the total amount you’d pay over the life of the new loan, including all interest and fees.

Step 6: Finalize the Deal

Once you’ve chosen the best offer, work with the lender to finalize the paperwork. If you’re using a personal loan, the funds will be disbursed, and you’ll use them to pay off your existing car loans. If you’re refinancing an individual car loan, the new lender will typically pay off your old lender directly. Ensure all old accounts are closed and paid in full.

Pros and Cons of Combining Car Loan Debt

Like any financial strategy, combining car loan debt has its advantages and disadvantages. A balanced perspective is crucial.

Advantages:

- Simplified Budgeting: A single payment makes financial tracking much easier.

- Potential for Lower Interest Rates: If your credit has improved, you could save significant money.

- Reduced Monthly Payments: Free up cash flow for other needs or savings.

- Streamlined Lending Relationships: Dealing with one lender instead of multiple.

- Improved Peace of Mind: Less financial complexity often leads to less stress.

Disadvantages:

- Potential for Higher Overall Cost: If you extend the loan term too much, even with a lower APR, you might pay more in interest over time.

- Impact on Credit Score: Multiple applications can temporarily lower your score.

- Risk with Secured Loans: Using your home as collateral (home equity loan) carries the risk of foreclosure if you default.

- Eligibility Challenges: Not everyone will qualify for the best rates or even for consolidation, especially with lower credit scores.

- No Guarantee of Savings: If market rates are high or your credit isn’t excellent, you might not find better terms.

Potential Pitfalls and Common Mistakes to Avoid

Based on my experience, I’ve observed several recurring errors people make when attempting to combine or consolidate car loans. Avoiding these can save you a lot of grief and money.

1. Focusing Only on the Monthly Payment

A common misconception I often encounter is that a lower monthly payment always means a better deal. While reducing your monthly outlay can be beneficial for cash flow, it often comes at the cost of extending the loan term. This can result in paying significantly more interest over the long run. Always calculate the total cost of the new loan.

2. Not Shopping Around Enough

Settling for the first offer you receive is a surefire way to miss out on better rates. Different lenders have different risk assessments and pricing models. Take the time to get quotes from at least 3-5 different institutions.

3. Ignoring Prepayment Penalties

Though rare for standard auto loans, some personal loans or very specialized auto loans might carry prepayment penalties. Ensure your current loans don’t have these, and your new loan doesn’t introduce them, especially if you plan to pay it off early.

4. Overlooking Fees

Some lenders charge origination fees, application fees, or other closing costs. These fees can eat into any savings you might achieve. Always factor all fees into your total cost calculation.

5. Falling for "Too Good to Be True" Offers

Be wary of lenders promising extremely low rates without a thorough credit check. Reputable lenders will always review your financial history. Scammers often prey on those desperate for consolidation.

6. Not Understanding the Loan Terms

Read the fine print! Make sure you fully understand the interest rate, term, monthly payment, and any specific clauses in the loan agreement before signing. Don’t be afraid to ask questions.

Pro Tips from Us: Expert Advice for Smart Consolidation

Here are some insights gleaned from years in the financial planning and lending space that can give you an edge:

- Improve Your Credit First: If your credit score is borderline, dedicate a few months to improving it before applying. Pay bills on time, reduce credit card balances, and dispute any errors on your report. Even a small increase can unlock significantly better rates.

- Consider a Co-Signer (Carefully): If your credit isn’t ideal, a creditworthy co-signer can help you qualify for better terms. However, this is a serious commitment for the co-signer, as they become equally responsible for the debt.

- Negotiate with Your Current Lenders: Sometimes, your existing lenders might be willing to offer better terms to keep your business, especially if you have a good payment history and present them with a competitive offer from another lender. It never hurts to ask!

- Set Up Autopay: Once you consolidate, immediately set up automatic payments. This ensures you never miss a payment, helps build your credit, and often qualifies you for a small interest rate discount from lenders.

- Understand the "Why": Beyond just wanting a lower payment, understand your ultimate financial goal. Is it to pay off debt faster? Reduce overall interest? Free up monthly cash? Your "why" will guide your best consolidation strategy.

- Future-Proof Your Finances: Once you’ve successfully consolidated, resist the temptation to take on new unnecessary debt. Use the extra cash flow to build an emergency fund or accelerate debt repayment.

Alternatives to Combining Car Loans

Sometimes, consolidating or refinancing isn’t the right fit. Perhaps your credit isn’t strong enough, or the potential savings aren’t significant. In such cases, consider these alternatives:

- Aggressive Debt Repayment: Focus on paying down the car loan with the highest interest rate first, while making minimum payments on the other. Once the first is paid off, roll those payments into the second loan (the "debt snowball" or "debt avalanche" method).

- Budget Optimization: Review your entire budget to find areas where you can cut expenses to free up more money for your car payments. This could involve cutting discretionary spending, finding cheaper insurance, or reducing subscription services.

- Part-Time Work or Side Hustle: Earning extra income can provide the necessary funds to tackle your car loans more aggressively without the need for new financing.

- Selling One Vehicle: If having two cars is straining your finances, and you can manage with one, selling the less essential vehicle could be a direct way to eliminate one of your loans.

If you’re considering refinancing a single car loan, we’ve covered that extensively in our article, .

Conclusion: Take Control of Your Car Loan Debt

While the direct "combination" of two physical car loans into a single new auto loan isn’t a standard financial product, the good news is that you have powerful strategies at your disposal to achieve the effect of combining your car loan debt. Whether through strategic individual refinancing, a debt consolidation personal loan, or (with extreme caution) a home equity product, you can simplify your payments, potentially lower your interest rates, and regain control of your finances.

The key lies in understanding your options, carefully assessing your financial situation, and diligently shopping around for the best terms. Don’t let the complexity deter you. By following the expert advice and detailed steps outlined in this guide, you’re well on your way to making smarter decisions about your auto debt. Take action today, explore your options, and drive towards a more streamlined and financially secure future.