Can You Finance Two Cars with One Loan? The Ultimate Guide to Multiple Vehicle Financing

Can You Finance Two Cars with One Loan? The Ultimate Guide to Multiple Vehicle Financing Carloan.Guidemechanic.com

The dream of driving home two new (or new-to-you) cars at once is an exciting one. Perhaps you need a family SUV and a commuter sedan, or maybe you and your partner are upgrading your vehicles simultaneously. As you start crunching numbers, a common question arises: "Can I finance two cars with one loan?" It’s a logical thought – consolidating everything into a single payment seems simpler, right?

Based on my experience in the automotive finance world, this is one of the most common misconceptions buyers have. While the idea of a single, convenient loan for multiple vehicles is appealing, the reality of how auto loans are structured makes it an extremely rare, if not impossible, scenario. In this comprehensive guide, we’ll dive deep into why a single loan for two cars typically isn’t an option, and more importantly, explore the practical, proven strategies for successfully financing multiple vehicles.

Can You Finance Two Cars with One Loan? The Ultimate Guide to Multiple Vehicle Financing

Let’s buckle up and navigate the complexities of multiple vehicle financing, ensuring you drive away with the knowledge to make the best financial decisions.

The Straight Answer: Why One Loan for Two Cars is (Mostly) a No-Go

Let’s address the elephant in the showroom upfront: generally speaking, you cannot finance two cars with one single loan. While the concept might sound efficient, the fundamental structure of an auto loan simply doesn’t accommodate it.

An auto loan is a specific type of secured loan, meaning it’s backed by collateral. In this case, the car you’re buying serves as the collateral. This single-collateral principle is at the heart of why combining two vehicles into one loan doesn’t work for lenders.

Understanding the Mechanics of a Traditional Auto Loan

To truly grasp why lenders shy away from a "two-for-one" auto loan, it’s essential to understand how a standard car loan operates.

Every traditional auto loan is meticulously tied to a single, specific vehicle. This connection is established through the vehicle’s unique identification number (VIN) and documented on the car’s title. The lender places a "lien" on this title, indicating their ownership stake until the loan is fully repaid.

This lien is the lender’s security. If you, as the borrower, default on your payments, the lender has the legal right to repossess the specific vehicle listed as collateral to recoup their losses. This straightforward, one-to-one relationship between a loan and its collateral is crucial for lenders to manage their risk effectively.

The Lender’s Perspective: Why It’s Too Risky

From a lender’s viewpoint, offering one loan for two separate cars presents a myriad of logistical, legal, and risk assessment nightmares.

- Collateral Confusion: Imagine if you default on a single loan tied to two cars. Which car would the lender repossess? Both? Just one? How would they then determine the remaining balance owed, or which portion of the loan was tied to which vehicle? The process of splitting collateral and calculating remaining debt would be incredibly complex and costly for the lender.

- Valuation and Depreciation: Each vehicle has its own distinct market value, depreciation rate, and insurance requirements. Lenders underwrite loans based on these individual factors. A single loan would struggle to account for the differing values and risks associated with two separate assets that depreciate at different rates.

- Legal Complexities: The legal framework for repossessions and liens is built around single-collateral loans. Creating a legal document that clearly defines the lender’s rights and responsibilities for two distinct assets under one loan would be an unprecedented challenge, adding significant legal risk and administrative burden.

- Increased Default Risk: Financing two cars naturally involves a larger sum of money and, consequently, higher monthly payments. This inherently increases the overall financial risk for the borrower, which translates into a higher default risk for the lender. They prefer to mitigate this by assessing each loan independently.

For these reasons, lenders overwhelmingly prefer the clarity and security of a separate loan for each vehicle. It simplifies risk assessment, collateral management, and potential repossession processes, making it the industry standard.

Navigating the Road to Multiple Vehicle Ownership: Your Real Options

While a single loan for two cars is off the table, don’t despair! There are several practical and widely accepted strategies for financing multiple vehicles. The key is to understand each option and choose what best fits your financial situation.

Option 1: Two Separate Auto Loans (The Most Common Approach)

This is by far the most straightforward and frequently used method for financing two cars. You simply apply for and secure an individual auto loan for each vehicle.

- How it works: You’ll go through the loan application process twice, once for each car. Each loan will have its own terms, interest rate, and monthly payment schedule. You might secure both loans from the same lender, or you might find better rates by using two different financial institutions.

- Pros: Each loan is tied to its specific collateral, making it clear and manageable for both you and the lender. This is the standard practice in the industry.

- Cons: You’ll have two separate monthly payments to track, and applying for two loans simultaneously might result in multiple "hard inquiries" on your credit report, which could temporarily ding your credit score.

- Pro Tip from us: When applying for multiple loans close together, try to do so within a short timeframe (e.g., 14-45 days, depending on the credit bureau model). This allows credit scoring models to recognize it as "rate shopping" for the same type of loan, often grouping inquiries together and minimizing the impact on your score.

Option 2: Personal Loans (Unsecured)

While not ideal for financing the entire purchase of two expensive cars, a personal loan can be a viable option in specific circumstances.

- How it works: A personal loan is an unsecured loan, meaning it doesn’t require collateral. Lenders approve these based primarily on your creditworthiness and income. You receive a lump sum, which you then use to purchase one or both vehicles.

- Pros: Flexibility – you can use the funds for anything, including buying a car. No lien is placed on the vehicle itself.

- Cons: Because there’s no collateral, personal loans typically come with significantly higher interest rates than secured auto loans. The loan amounts are also often lower, making it difficult to finance two expensive vehicles this way. It’s usually better suited for a smaller, inexpensive car or for making a large down payment on a second vehicle.

- Common mistake to avoid: Relying solely on a personal loan for two high-value vehicles can lead to very high monthly payments and substantial interest costs over the life of the loan.

Option 3: Home Equity Loan or Line of Credit (HELOC)

If you own a home with substantial equity, you might consider leveraging that equity to finance one or both cars.

- How it works: A home equity loan provides a lump sum, while a Home Equity Line of Credit (HELOC) offers a revolving credit line up to a certain limit. Both use your home as collateral.

- Pros: These loans often come with lower interest rates compared to unsecured personal loans, and the interest may even be tax-deductible in some cases (consult a tax professional). You can potentially access a larger sum of money.

- Cons: This is a significant decision. You are putting your home at risk. If you default, you could lose your home. Using your home, which is an appreciating asset, to finance depreciating assets (cars) requires careful consideration.

- Pro Tip from us: Only consider this option if you have a very stable financial situation and are comfortable with the inherent risk. It’s crucial to ensure your car payments don’t jeopardize your housing security.

Option 4: Lease One, Finance One

For many households, a mix-and-match approach offers the best of both worlds.

- How it works: You could choose to lease one vehicle, typically a newer model that you want to drive for a few years without the long-term commitment of ownership. For the second vehicle, which you intend to own outright, you would secure a traditional auto loan.

- Pros: Leasing often results in lower monthly payments compared to financing, freeing up cash flow. This allows you to drive a new car more frequently. Financing the second vehicle gives you ownership.

- Cons: Leased vehicles have mileage restrictions and wear-and-tear clauses. You don’t build equity with a lease.

- Pro Tip from us: This strategy works well if one driver prefers driving a new car every few years, while the other values long-term ownership and perhaps drives fewer miles.

Option 5: Cash Purchase (for one car)

If you have significant savings, buying one car outright in cash while financing the other can be an excellent strategy.

- How it works: You use your savings to purchase one vehicle entirely, eliminating one loan payment. You then apply for a traditional auto loan for the second car.

- Pros: Reduces your overall debt burden and frees up monthly cash flow. You avoid interest payments on the cash-purchased vehicle.

- Cons: Requires substantial savings that you might prefer to keep for emergencies or other investments.

- Common mistake to avoid: Draining your entire emergency fund to pay cash for one car. Always ensure you maintain a healthy savings cushion.

Option 6: Dealership Financing vs. Bank/Credit Union (for each loan)

When you’re ready to get your individual loans, you’ll generally have two main avenues.

- Dealership Financing: Dealerships often work with multiple lenders and can offer convenient one-stop shopping. They might even have special incentives or lower rates for specific models.

- Banks and Credit Unions: It’s always wise to get pre-approved for a loan from your bank or credit union before stepping into a dealership. This gives you a benchmark rate and strengthens your negotiating position. Credit unions, in particular, often offer competitive rates.

- Pro Tip from us: Always compare offers. Getting pre-approved elsewhere provides leverage, even if you end up taking the dealership’s offer.

Key Factors Influencing Your Approval for Multiple Car Loans

Securing even one auto loan requires meeting certain criteria, but financing two simultaneously (even with separate loans) puts a greater spotlight on your financial health. Here are the crucial factors lenders will scrutinize:

1. Your Credit Score

This is the cornerstone of any loan application. Your credit score is a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt.

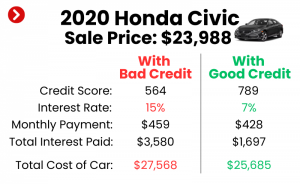

- Impact: A higher credit score (typically 700+) indicates to lenders that you are a low-risk borrower, making you eligible for better interest rates and more favorable loan terms. A lower score might still get you approved, but with significantly higher interest rates.

- Why it matters for two cars: Lenders will assess your ability to manage multiple significant debt obligations. A strong credit score across the board is paramount.

- Internal Link Idea: For an in-depth look at improving your financial standing, read our comprehensive guide on "Boost Your Credit Score: Our Top Tips for Financial Success".

2. Debt-to-Income (DTI) Ratio

Your DTI ratio is a critical metric that lenders use to assess your ability to handle new debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income.

- Impact: Lenders generally prefer a DTI ratio below 36%, though some may go up to 43% for well-qualified borrowers. When you add two new car payments, your DTI will increase significantly.

- Why it matters for two cars: If your DTI is already high before applying for new loans, adding two car payments could push it into an unacceptable range, leading to denial. Lenders want to ensure you have enough disposable income to comfortably make all your payments.

- Internal Link Idea: To learn more about this vital metric, check out "Understanding Debt-to-Income Ratio: What It Means for Your Loan Applications".

3. Income Stability and Employment History

Lenders want assurance that you have a consistent and reliable source of income to repay your loans.

- Impact: A stable job history (typically at least two years with the same employer or in the same industry) and verifiable income (pay stubs, tax returns) demonstrate your ability to meet your financial obligations.

- Why it matters for two cars: The higher the total loan amount, the more critical your income stability becomes. Lenders need to see that you can comfortably afford the combined payments of both vehicles.

4. Down Payment

Making a substantial down payment on each vehicle can significantly improve your chances of approval and secure better terms.

- Impact: A larger down payment reduces the amount you need to borrow, lowering your monthly payments and decreasing the lender’s risk. It also shows your commitment to the purchase.

- Why it matters for two cars: When financing two cars, every little bit helps. Even a 10-20% down payment on each vehicle can make a considerable difference in loan approval and interest rates.

5. Loan Term

The length of your loan (the term) impacts your monthly payment and the total interest you’ll pay over time.

- Impact: Shorter loan terms mean higher monthly payments but less interest paid overall. Longer terms result in lower monthly payments but accumulate more interest.

- Why it matters for two cars: While longer terms might make two car payments seem more affordable monthly, be wary of extending them too far. You could end up owing more than the car is worth (being "upside down") as vehicles depreciate quickly.

Pro Tips for Successfully Financing Two Vehicles

Financing multiple cars requires careful planning and strategic execution. Here are some expert tips to help you navigate the process smoothly:

- Prioritize and Budget Meticulously: Before you even start shopping, determine your absolute maximum affordable monthly payment for both vehicles combined, including insurance, fuel, and maintenance. Distinguish between a "need" car and a "want" car. This helps in making trade-offs if necessary.

- Shop Around Aggressively for Each Loan: Don’t just settle for the first offer you receive. Contact multiple banks, credit unions, and even online lenders for each individual car loan. Compare interest rates, fees, and terms thoroughly. A difference of even 0.5% on two loans can save you thousands over time.

- Improve Your Credit Score First: If your credit score isn’t in the "excellent" range, take steps to improve it before applying. Pay down existing debts, dispute any errors on your credit report, and avoid opening new credit accounts. A higher score translates directly to lower interest rates on both loans.

- Save for Substantial Down Payments: Aim for at least 10-20% down on each vehicle, if possible. This not only reduces your loan amounts and monthly payments but also makes you a more attractive borrower to lenders, potentially securing you better rates.

- Consider a Mix of New and Used Vehicles: If financing two brand-new cars pushes your budget too far, consider purchasing one new vehicle and one high-quality used vehicle. Used cars generally have lower purchase prices and often lower insurance costs, making the combined payments more manageable.

- Stagger Your Applications (Carefully): While applying for loans within a short window is generally advised to minimize credit score impact, if you’re concerned about your DTI, consider purchasing one car, waiting for the account to report to credit bureaus, and then applying for the second. This needs careful timing and consideration of your overall financial picture.

- Know Your Total Cost of Ownership: Remember that car payments are just one part of the equation. Factor in insurance (for two cars!), fuel, maintenance, registration, and potential repairs. You don’t want to be "car poor," where your vehicle expenses consume too much of your income.

Common Mistakes to Avoid When Financing Multiple Cars

Even with the best intentions, it’s easy to fall into common traps when trying to finance two vehicles. Being aware of these pitfalls can save you significant headaches and financial strain.

- Overestimating Your Budget: This is perhaps the biggest mistake. It’s easy to get caught up in the excitement of new cars and commit to payments that are unsustainable in the long run. Always budget conservatively and leave room for unexpected expenses.

- Applying Everywhere at Once: While rate shopping within a short window is fine, submitting applications to dozens of lenders without proper research can lead to numerous hard inquiries, negatively impacting your credit score. Be targeted in your applications.

- Ignoring the Total Cost of Ownership: Focusing solely on the monthly payment for the cars themselves is a recipe for disaster. Failing to account for the doubled insurance premiums, increased fuel costs, and maintenance for two vehicles can quickly strain your budget.

- Settling for the First Offer: Never take the first loan offer you receive. Always compare terms and rates from multiple lenders to ensure you’re getting the most competitive deal for each individual loan.

- Not Reading the Fine Print: Auto loan agreements can be complex. Make sure you understand all the terms, fees, interest rates, and any prepayment penalties for each loan before signing on the dotted line.

Conclusion: Smart Strategies for Your Dual-Car Dream

While the dream of financing two cars with a single loan remains largely impractical due to the fundamental structure of auto lending, the good news is that owning two vehicles simultaneously is absolutely achievable. The key lies in understanding the available financing options and approaching the process with careful planning, thorough research, and a realistic assessment of your financial capacity.

By opting for two separate auto loans, exploring personal loan options for smaller purchases, leveraging home equity responsibly, or strategically combining leasing with financing, you can tailor a solution that fits your unique needs. Remember to prioritize a strong credit score, manage your debt-to-income ratio, and always budget for the total cost of ownership.

With the right strategy and a bit of diligence, you can successfully navigate the world of multiple vehicle financing and drive home in both the cars you desire. Happy driving!

Disclaimer: This article provides general financial information and is not intended as financial advice. Always consult with a qualified financial advisor or loan specialist for personalized guidance based on your individual circumstances.

External Link Suggestion:

For further general financial guidance on managing debt and improving credit, you might find valuable resources from the Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance.gov/