Can You Get a Car Loan at 18? Your Ultimate Guide to Driving Off with Independence

Can You Get a Car Loan at 18? Your Ultimate Guide to Driving Off with Independence Carloan.Guidemechanic.com

The dream of hitting the open road, the freedom of your own set of wheels, and the undeniable symbol of independence – for many 18-year-olds, getting a first car is a major milestone. But as exciting as the prospect is, the practicalities often bring a dose of reality, especially when it comes to financing. The burning question on many young minds is: Can you get a car loan at 18?

The short answer is yes, it’s absolutely possible. However, it’s rarely as straightforward as walking into a dealership and driving away. Securing an auto loan at such a young age comes with unique challenges, primarily due to a lack of established credit history and financial track record. Based on my experience in the automotive and finance industries, lenders typically view 18-year-olds as higher-risk borrowers. But don’t let that deter you! With the right preparation, understanding, and strategic approach, you can significantly boost your chances of approval.

Can You Get a Car Loan at 18? Your Ultimate Guide to Driving Off with Independence

This comprehensive guide is designed to be your pillar of knowledge, breaking down every aspect of securing a car loan as an 18-year-old. We’ll explore what lenders look for, effective strategies to overcome common hurdles, and how to manage your loan responsibly, setting you up for future financial success. Let’s navigate the road to your first car loan together.

The Legalities and Realities of Getting a Car Loan at 18

Before diving into the "how-to," it’s crucial to understand the foundational aspects of car loans for young adults.

The Legal Age for Contracts

First and foremost, the good news: at 18, you are legally considered an adult in the United States and can enter into binding contracts, including loan agreements. This means you have the legal capacity to apply for and be approved for a car loan in your own name. This is a fundamental starting point, distinguishing an 18-year-old from a minor who cannot legally sign such agreements.

However, legal capacity doesn’t automatically equate to lender approval. It simply means the door is open for you to apply.

Why Lenders Are Hesitant: Understanding Risk Perception

While you can legally sign, most lenders operate on a system of risk assessment. When an 18-year-old applies for a car loan, they often present a higher perceived risk compared to older, more established borrowers. This isn’t personal; it’s purely based on data and financial patterns.

Lenders look for predictability and a history of responsible financial behavior. An 18-year-old typically lacks this long-term track record, which translates to a higher risk profile from their perspective. They need assurance that you will repay the loan on time, every time.

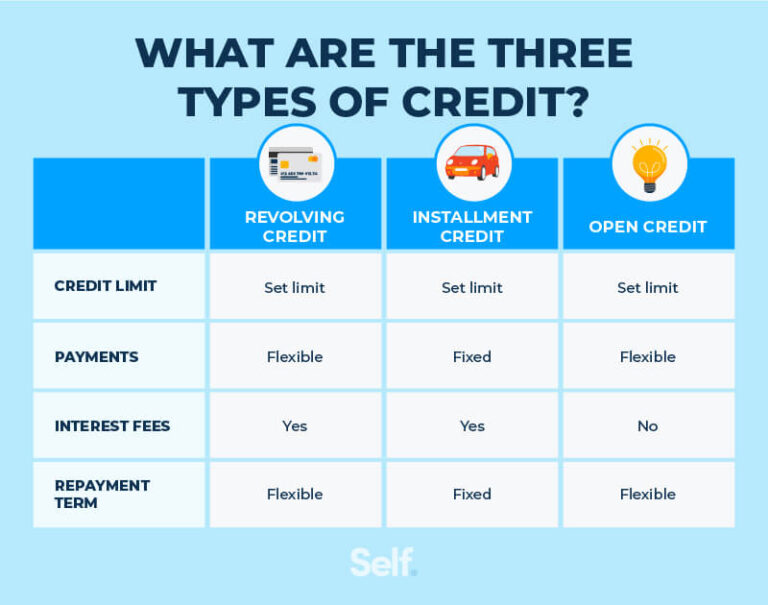

The Challenge of No Credit History

This is perhaps the biggest hurdle for young borrowers. Your credit history is essentially your financial report card, detailing how you’ve managed debt in the past. It includes information on credit cards, previous loans, and payment timeliness.

Most 18-year-olds are just starting their financial journey, meaning their credit report is often a blank slate. While "no credit" is better than "bad credit," it still makes it difficult for lenders to assess your reliability. They have no past performance to gauge your future behavior, making them more cautious.

Building Your Foundation: What Lenders Look For

To increase your chances of getting a car loan at 18, you need to understand the key factors lenders scrutinize. Think of these as the building blocks of your loan application.

Credit History and Score: Your Financial Footprint

As mentioned, a lack of credit history is a major obstacle. A strong credit score (typically FICO scores range from 300-850, with 670+ considered good) signals to lenders that you are a responsible borrower. Since you’re just starting, your goal is to demonstrate potential responsibility.

How an 18-Year-Old Can Start Building Credit:

- Secured Credit Card: This is often the easiest way. You deposit money (e.g., $300), and that becomes your credit limit. Use it for small, regular purchases and pay it off in full and on time every month. This demonstrates responsible usage.

- Authorized User: If a parent or trusted guardian has excellent credit, they might add you as an authorized user on one of their credit cards. Their positive payment history can then appear on your credit report, giving you a boost. Ensure they are highly responsible with their credit, as their missteps could also affect you.

- Small Installment Loans: Some local credit unions offer "credit builder" loans. These are small loans designed specifically to help you establish credit.

- Student Loans: If you’re attending college, student loan payments (once repayment begins) can also contribute to your credit history, though this is usually further down the line.

Pro tips from us: Start building your credit as early as possible. Even a few months of responsible credit card use can make a difference. Every on-time payment is a step towards a higher credit score.

Income and Employment Stability: Can You Afford It?

Lenders need assurance that you have a consistent and sufficient income to make your monthly car payments. They want to see proof of employment and a steady income stream.

What Lenders Look For:

- Proof of Income: This typically means recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if you’re self-employed.

- Employment Stability: Lenders prefer to see that you’ve been employed at your current job for a reasonable period, often 6 months to a year or more. This indicates stability and reliability.

- Full-Time vs. Part-Time: While part-time income can count, full-time employment with a higher, consistent income will always strengthen your application.

If you’ve recently started a new job, it might be wise to wait a few months to establish a track record before applying for a loan. This shows greater stability.

Down Payment: Lowering the Lender’s Risk

A significant down payment is one of the most powerful tools an 18-year-old has to secure a car loan. It demonstrates financial responsibility and commitment, while also reducing the amount you need to borrow.

Why a Down Payment Helps:

- Reduces Loan-to-Value (LTV): The LTV ratio compares the loan amount to the car’s value. A lower LTV means less risk for the lender. If you default, they’re more likely to recoup their losses.

- Lowers Monthly Payments: A larger down payment directly translates to a smaller loan amount, resulting in lower monthly payments and potentially less interest paid over the life of the loan.

- Shows Commitment: Lenders see a substantial down payment as a sign that you are serious about the purchase and financially capable.

Common mistakes to avoid: Not saving enough for a down payment. Aim for at least 10-20% of the car’s purchase price. The more you put down, the better your chances and terms will be.

Debt-to-Income Ratio (DTI): Keeping Other Debts Low

Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage monthly payments and take on new debt.

Understanding DTI for Young Adults:

- For an 18-year-old, it’s crucial to keep any existing debts (like student loan payments, credit card minimums, or other personal loans) as low as possible.

- A low DTI (ideally below 36%, with less than 20% being excellent) shows lenders you have plenty of disposable income to comfortably handle a new car payment.

- If you have no existing debt, your DTI will be very favorable, which is a significant advantage.

Focus on minimizing other financial obligations before applying for a car loan.

Strategies to Boost Your Chances of Car Loan Approval at 18

Even with the challenges, there are several effective strategies you can employ to significantly improve your odds of approval.

The Power of a Co-Signer

For many 18-year-olds, a co-signer is the game-changer that makes a car loan possible. A co-signer is typically a parent or guardian with a strong credit history and stable income who agrees to be equally responsible for the loan.

Who Can Be a Co-Signer?

- Someone with excellent credit (670+ FICO score).

- Someone with a stable income and low DTI.

- Someone you trust implicitly, as their financial well-being is tied to your loan.

How it Helps:

- Leveraging Their Credit: The lender considers the co-signer’s credit history and income alongside yours, significantly mitigating the risk associated with your lack of credit.

- Better Terms: With a strong co-signer, you’re more likely to secure a lower interest rate and more favorable loan terms than you would on your own.

Responsibilities and Risks for Both Parties:

- Equal Responsibility: Both you and your co-signer are legally obligated to repay the loan. If you miss payments, it impacts both your credit scores, and the lender can pursue either of you for payment.

- Trust is Key: This arrangement requires immense trust and clear communication. Ensure both parties understand the full implications before proceeding.

Based on my experience, a responsible co-signer is often the most direct path to approval for an 18-year-old, especially for their first significant loan. It’s a way for lenders to bridge the gap created by a thin credit file.

Starting Small: Used Cars vs. New Cars

When you’re just starting, aiming for a brand-new, expensive car might not be the most realistic or financially prudent option.

Why a Used Car is a Smarter Choice:

- Lower Price Point: Used cars are generally much cheaper than new ones, meaning you’ll need a smaller loan amount.

- Manageable Payments: A smaller loan translates to lower monthly payments, which are easier to fit into a young adult’s budget.

- Less Risk for Lenders: A lower loan amount is less risky for lenders, making them more willing to approve your application.

- Building Credit Responsibly: Successfully paying off a smaller used car loan is an excellent way to build a positive credit history without overextending yourself financially.

Consider a reliable, affordable used car for your first purchase. It allows you to gain experience with car ownership and loan repayment.

Pre-Approval: Knowing What You Can Afford

Before you even step foot in a dealership, consider getting pre-approved for a car loan from a bank or credit union.

Benefits of Pre-Approval:

- Clear Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Stronger Negotiation Position: With a pre-approval letter in hand, you’re essentially a cash buyer at the dealership. This gives you leverage to negotiate on the car’s price, rather than just the financing.

- Focus on the Car: You can focus on finding the right vehicle, knowing your financing is already sorted.

- Understanding Terms: You’ll have a clear understanding of your potential interest rate, loan term, and monthly payments upfront.

Pre-approval often involves a "soft inquiry" on your credit, which doesn’t affect your score. Once you proceed with a specific lender, a "hard inquiry" will occur.

Credit Unions and Local Banks: Your Best Bet

While large national banks and dealership financing options are available, credit unions and smaller local banks often prove to be more flexible and accommodating for young borrowers, especially those with limited credit history.

Why They Might Be Better:

- Relationship Banking: Credit unions, in particular, are member-owned and often prioritize building relationships with their members. If you already have an account with them, they might be more willing to work with you.

- Flexible Underwriting: They sometimes have more flexible underwriting criteria than larger institutions, allowing them to consider your overall financial situation rather than just a credit score.

- Lower Interest Rates: Credit unions are known for offering competitive interest rates.

It’s always wise to compare offers from multiple lenders, including credit unions, to find the best terms.

The Application Process: Step-by-Step for 18-Year-Olds

Once you’ve done your homework and prepared, it’s time to apply. Knowing what to expect can ease the process.

Gathering Essential Documents

Before you apply, have all necessary paperwork organized. This makes the process smoother and demonstrates your preparedness.

Documents You’ll Likely Need:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, or tax returns.

- Proof of Residence: Utility bill, lease agreement, or bank statement with your address.

- Social Security Number: For credit checks.

- Bank Account Information: For setting up payments.

- Co-Signer’s Information (if applicable): Their ID, income, and SSN.

Having these documents ready will prevent delays and show lenders you are serious and organized.

Filling Out the Application Accurately

Take your time when filling out the loan application. Ensure all information is accurate and consistent with your supporting documents. Any discrepancies could raise red flags and delay or even jeopardize your approval. Be honest about your income and employment history.

What to Expect During the Review

After submitting your application, the lender will review your information, check your credit report (and your co-signer’s, if applicable), and verify your income and employment. This process can take anywhere from a few hours to a few business days. They might call you or your employer to verify details.

Understanding the Loan Offer: APR, Term, and Monthly Payment

If approved, you’ll receive a loan offer detailing the terms. It’s crucial to understand these components:

- Annual Percentage Rate (APR): This is the total cost of borrowing money, expressed as a yearly percentage. It includes the interest rate and any other fees. A lower APR means lower overall costs.

- Loan Term: This is the length of time you have to repay the loan, typically in months (e.g., 36, 48, 60, 72 months). Shorter terms usually mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more interest over time.

- Monthly Payment: This is the fixed amount you’ll pay each month. Ensure it comfortably fits within your budget, considering all other expenses.

Don’t be afraid to ask questions if anything is unclear. This is a significant financial commitment.

Beyond Approval: Managing Your Car Loan Responsibly

Getting approved is just the first step. The real test of financial responsibility comes with managing your car loan effectively.

Budgeting for Car Ownership: More Than Just the Payment

Many first-time car owners underestimate the true cost of vehicle ownership. The monthly loan payment is just one piece of the puzzle.

Hidden Costs to Budget For:

- Car Insurance: For 18-year-olds, insurance premiums can be exceptionally high due to age and lack of driving experience. Get quotes before finalizing your car purchase.

- Fuel: Factor in daily commuting and leisure driving.

- Maintenance and Repairs: Oil changes, tire rotations, unexpected repairs – set aside an emergency fund for these.

- Registration and Taxes: Annual fees vary by state.

- Parking Fees/Tolls: If applicable to your routine.

Pro tips from us: Create a detailed budget that includes all these costs. Use a spreadsheet or a budgeting app to track your income and expenses, ensuring you can comfortably afford your car and still have money for savings and other needs.

Making Payments On Time: Building a Strong Credit Future

This is arguably the most critical aspect of responsible loan management. Every on-time payment you make is reported to credit bureaus and positively impacts your credit score.

Why On-Time Payments Are Crucial:

- Credit Building: A history of timely payments is the bedrock of a good credit score. This car loan can be your stepping stone to future financial products (e.g., a mortgage).

- Avoiding Late Fees: Late payments incur fees, adding to your financial burden.

- Preventing Default: Consistently missing payments can lead to default, car repossession, and severe damage to your credit for years to come.

Set up automatic payments from your bank account to ensure you never miss a due date.

Understanding Your Loan Terms: Don’t Be Surprised

Revisit your loan agreement periodically to fully understand its terms.

- Fixed vs. Variable Rates: Most auto loans are fixed-rate, meaning your interest rate and monthly payment remain constant. Variable rates can change, making your payments unpredictable.

- Prepayment Penalties: While rare for auto loans, some lenders might charge a fee if you pay off your loan early. Always check for this clause.

- Other Fees: Be aware of any late payment fees, administrative charges, or other costs outlined in your contract.

Building Credit for the Future: A Stepping Stone

Successfully managing your first car loan as an 18-year-old is an invaluable experience. It proves your financial responsibility and establishes a solid credit history. This positive track record will make it easier to secure other loans (like a mortgage or future car loans) at more favorable interest rates down the line. It’s an investment in your financial future.

For more in-depth guidance on establishing your financial foundation, you might find our article on How to Build Credit from Scratch as a Young Adult particularly helpful. (Internal Link Placeholder)

Common Pitfalls and How to Avoid Them

Even with the best intentions, young borrowers can fall into common traps. Being aware of these can help you steer clear.

Taking on Too Much Debt: The Overspending Trap

One of the biggest mistakes is buying a car that is too expensive for your budget. The allure of a fancy vehicle can be strong, but an unaffordable monthly payment is a recipe for financial stress and potential default.

Common mistakes to avoid are: Stretching your budget to the absolute limit. Remember, the goal is to afford the car comfortably, not just barely.

Ignoring Insurance Costs: A Major Oversight

As mentioned, car insurance for young drivers is notoriously expensive. Many 18-year-olds focus solely on the car’s price and loan payment, forgetting to factor in this significant recurring cost. Get multiple insurance quotes before you commit to a car.

Not Reading the Fine Print: Understanding the Full Contract

It’s tempting to skim through lengthy loan documents, but every clause is important. Understand the interest rate, term, any fees, and your rights and responsibilities. If something seems unclear, ask for clarification. Never sign a document you don’t fully comprehend.

Falling for Predatory Lenders: The High-Interest Trap

Some lenders target young or credit-challenged individuals with high-interest rates and unfavorable terms. These "buy here, pay here" dealerships or subprime lenders might approve you quickly, but often at a very high cost, potentially trapping you in a cycle of debt.

Be wary of deals that seem too good to be true, or lenders that pressure you into signing without adequate review. Always compare multiple offers.

Alternatives to a Traditional Car Loan

If a traditional car loan seems out of reach or too risky right now, consider these alternatives:

- Saving Up and Buying Cash: The most financially sound option, if possible. Buying a car outright means no interest payments, no monthly obligations, and full ownership from day one. Start with a budget and save diligently for a modest, reliable used car.

- Buying a Much Cheaper Car: Instead of aiming for a $15,000 loan, perhaps a $5,000 used car could be purchased with a smaller loan or even cash saved over a few months. This eases the financial burden significantly.

- Family Loans: If a trusted family member is willing and able, a private loan can be an option. Ensure you have a clear, written agreement outlining repayment terms to avoid misunderstandings and maintain good relationships.

- Public Transportation/Ride-Sharing: Depending on where you live, relying on public transport, cycling, or ride-sharing services for a while longer can save you money and time while you build your financial foundation.

Conclusion: Your Road to Financial Independence Starts Now

So, can you get a car loan at 18? Absolutely. It’s a journey that demands preparation, strategic thinking, and a commitment to financial responsibility. While the initial hurdles might seem daunting, they are entirely surmountable with the right approach. By focusing on building credit, securing a stable income, making a substantial down payment, and potentially utilizing a co-signer, you significantly increase your chances of approval.

Remember, this first car loan isn’t just about getting a set of keys; it’s about laying the groundwork for your financial future. Managing it responsibly will open doors to better opportunities and greater independence down the road. Take your time, do your research, and make informed decisions. Your journey toward financial independence and your first car starts today!

For further resources on understanding your credit score and managing debt, we recommend visiting the Experian Credit Education portal at https://www.experian.com/credit-education/. (External Link)