Can You Get a Car Loan Before Chapter 7 Discharge? Navigating Auto Financing During Bankruptcy

Can You Get a Car Loan Before Chapter 7 Discharge? Navigating Auto Financing During Bankruptcy Carloan.Guidemechanic.com

Embarking on a Chapter 7 bankruptcy can feel like navigating a complex maze. It’s a period of significant financial restructuring, often leaving individuals with many questions about their daily needs, especially when it comes to transportation. One of the most pressing concerns for many is: Can you get a car loan before Chapter 7 discharge?

This is not a simple yes or no question, and the answer involves several critical factors. As an expert blogger and professional SEO content writer who has witnessed countless financial journeys, I can tell you that while challenging, securing an auto loan before your Chapter 7 discharge is indeed possible under specific circumstances. However, it requires careful planning, legal consultation, and an understanding of the unique landscape of bankruptcy financing.

Can You Get a Car Loan Before Chapter 7 Discharge? Navigating Auto Financing During Bankruptcy

This comprehensive guide will delve deep into the intricacies of obtaining a car loan during the Chapter 7 process. We’ll explore the legalities, lender considerations, common pitfalls, and pro tips to help you make an informed decision. Our goal is to provide you with a clear roadmap, offering real value and actionable insights to navigate this sensitive financial period.

Understanding Chapter 7 Bankruptcy: A Quick Overview

Before we dive into auto loans, let’s briefly clarify what Chapter 7 bankruptcy entails. This type of bankruptcy, often called "liquidation bankruptcy," aims to discharge most of your unsecured debts, such as credit card balances and medical bills. It provides a fresh financial start for individuals who cannot repay their debts.

The process typically involves a bankruptcy trustee reviewing your assets and liabilities. If you have non-exempt assets, they might be sold to pay creditors. However, most Chapter 7 filers have primarily exempt assets, meaning they get to keep most of their possessions.

A crucial component of Chapter 7 is the "automatic stay," which goes into effect immediately upon filing. This legal injunction prevents creditors from taking collection actions against you, including repossessions, lawsuits, and wage garnishments. The ultimate goal is the "discharge," a court order that legally releases you from the obligation to pay most of your debts.

The Core Question: Getting a Car Loan Before Discharge

So, back to our central question: Can you get a car loan before Chapter 7 discharge? The short answer is yes, but it comes with significant hurdles and specific requirements. It’s not the easiest path, but it’s often a necessary one for individuals who rely on a vehicle for work or essential daily activities.

The primary reason this is challenging is the impact of bankruptcy on your credit and the existence of the automatic stay. Lenders perceive individuals in active bankruptcy as high-risk borrowers. Your credit score will have plummeted, and the automatic stay prevents creditors from initiating collection activities without court permission, adding another layer of complexity.

Despite these challenges, some lenders specialize in financing for individuals in bankruptcy. They understand the unique circumstances and are willing to extend credit, albeit typically with less favorable terms. The key is knowing how to approach these lenders and what steps to take.

Why You Might Need a Car Loan During Chapter 7

Life doesn’t stop because you’ve filed for bankruptcy. There are many legitimate reasons why someone might need a new vehicle or a car loan during their Chapter 7 proceedings.

Perhaps your existing car was repossessed before filing, or it’s simply beyond repair. For many, reliable transportation is essential for getting to work, attending medical appointments, or fulfilling family responsibilities. Without a car, your ability to earn an income and manage your life can be severely compromised.

In such cases, obtaining a car loan isn’t a luxury; it’s a necessity. Understanding the options available and navigating the legal and financial requirements becomes paramount to maintaining stability during this transitional period.

Key Scenarios and Considerations for Pre-Discharge Auto Loans

Navigating an auto loan during Chapter 7 requires understanding a few key legal and financial concepts. These scenarios dictate how a new car loan, or even an existing one, might be handled.

The Role of Your Bankruptcy Attorney

Based on my experience, the single most important step you can take when considering a car loan before discharge is to consult with your bankruptcy attorney. They are your guide through this complex legal process. Attempting to secure a loan without their counsel can lead to serious complications, including potential violations of bankruptcy rules or jeopardizing your discharge.

Your attorney will advise you on the feasibility, the necessary court motions, and the specific requirements in your jurisdiction. They can also help you understand the long-term implications of taking on new debt during bankruptcy.

Reaffirmation Agreements for Existing Car Loans

While our focus is on new car loans, it’s important to understand "reaffirmation agreements" as they relate to existing car loans during Chapter 7. If you want to keep a car you already own and have a loan for, you might enter into a reaffirmation agreement with the lender.

A reaffirmation agreement is a legal contract where you agree to continue paying a debt that would otherwise be discharged in bankruptcy. For a car loan, this means you promise to keep making payments on your vehicle, and the lender retains the right to repossess the car if you default. This agreement must be filed with the bankruptcy court and, in some cases, approved by a judge.

Pro tips from us: Reaffirming a debt means it will not be discharged, and you will be personally liable for it even after bankruptcy. Always weigh the pros and cons carefully with your attorney, as this could impact your fresh financial start.

Obtaining Court Permission for a New Loan

For a new car loan before Chapter 7 discharge, you generally need to obtain permission from the bankruptcy court. This is because the automatic stay prevents new creditors from taking action against you without court approval. A new loan could be seen as an additional debt obligation that interferes with the bankruptcy process.

Your attorney will typically file a "Motion to Incur Debt" or a similar request with the court. This motion explains why you need the car, demonstrates your ability to make payments, and shows that the new debt won’t unduly burden your fresh start. The court will review your income, expenses, and the proposed loan terms to determine if it’s in your best interest and doesn’t prejudice other creditors.

Common mistakes to avoid are: Trying to get a new loan without court permission. This can lead to the loan being invalid, or worse, facing legal repercussions from the bankruptcy court. Always follow the proper legal channels.

Factors Lenders Consider for Pre-Discharge Car Loans

Even with court permission, finding a lender willing to offer a car loan before your Chapter 7 discharge can be tough. However, some lenders specialize in this niche market. They will evaluate your situation based on several key factors:

- Your Income and Expenses (Debt-to-Income Ratio): Lenders need to see that you have sufficient stable income to afford the new car payment, along with your other necessary living expenses. Your post-bankruptcy budget will be scrutinized carefully.

- The Value of the Car: Lenders prefer to finance vehicles that are not overly expensive for your income level. They’ll assess the car’s market value to ensure it’s reasonable for the loan amount. A reliable, used vehicle is often a more realistic option than a brand-new luxury car.

- Down Payment: A substantial down payment significantly reduces the lender’s risk. If you can save up a significant sum to put down on the vehicle, your chances of approval and securing better terms will greatly increase.

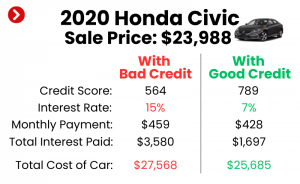

- Interest Rates: Be prepared for higher interest rates. Because of the inherent risk associated with lending to someone in bankruptcy, these loans typically come with rates higher than standard auto loans. This is the cost of securing financing during this challenging period.

- Co-signer: If you have a creditworthy co-signer, it can dramatically improve your chances of approval and potentially lead to better terms. The co-signer essentially guarantees the loan, mitigating some of the lender’s risk.

- Lender Type: Not all lenders are created equal when it comes to bankruptcy financing. You’ll likely need to seek out subprime lenders or dealerships that specialize in bad credit or bankruptcy situations. Traditional banks or credit unions might be less willing to take on this level of risk pre-discharge.

The Process of Applying for a Car Loan Pre-Discharge

Once you’ve discussed your needs with your attorney and understand the landscape, here’s a step-by-step process for applying for a car loan before Chapter 7 discharge:

Step 1: Consult Your Bankruptcy Attorney (Again!)

This cannot be stressed enough. Your attorney will confirm if a new loan is feasible, help you prepare the necessary court motions (like the Motion to Incur Debt), and guide you through the legal requirements. They are your primary resource for ensuring everything is done correctly and legally.

Step 2: Understand Your Needs and Budget

Determine what kind of car you genuinely need and what you can realistically afford. Focus on reliable, economical transportation rather than wants. Factor in not just the monthly payment, but also insurance, fuel, and maintenance costs. Creating a detailed budget will demonstrate your financial responsibility to the court and lenders.

Step 3: Research Specialized Lenders

Look for dealerships or lenders that advertise "bankruptcy auto loans" or "bad credit car loans." These lenders are more accustomed to working with individuals in your situation. You might start by searching online or asking your attorney for recommendations.

Step 4: Gather Necessary Documentation

Be prepared to provide extensive documentation. This will likely include:

- Proof of income (pay stubs, tax returns)

- Proof of residence

- Your bankruptcy case number and filing date

- A copy of your bankruptcy petition and schedules

- The court order granting permission to incur new debt (if required)

- Identification (driver’s license)

Having all your paperwork organized will streamline the application process.

Step 5: Be Prepared for Less Favorable Terms

As mentioned, expect higher interest rates, potentially shorter loan terms, and a requirement for a larger down payment. Understand that these are the typical conditions for pre-discharge car loans due to the higher risk involved. Focus on getting reliable transportation and making timely payments to start rebuilding your credit.

Step 6: Finalize with Court Approval

Once you find a suitable loan offer, your attorney will likely need to present the final loan terms to the court for approval, especially if you filed a motion to incur debt. The court needs to ensure the terms are fair and don’t create an undue burden.

Common Mistakes to Avoid When Seeking a Pre-Discharge Car Loan

Based on my experience, several common pitfalls can derail your efforts or create further complications during this sensitive time.

- Not Consulting Your Attorney: This is the biggest mistake. Proceeding without legal counsel can lead to unauthorized debt, jeopardizing your bankruptcy discharge, or even contempt of court.

- Applying with Too Many Lenders: Each loan application results in a "hard inquiry" on your credit report. Too many inquiries in a short period can further depress your already fragile credit score and make you look desperate to lenders.

- Overlooking the Automatic Stay: Forgetting or ignoring the automatic stay’s implications for new debt is a serious legal misstep that must be avoided. Court permission is often mandatory.

- Ignoring the Long-Term Impact: While a car might be a necessity, taking on high-interest debt before discharge can hinder your ability to truly achieve a fresh financial start. Always consider the long-term affordability.

- Getting a Car You Can’t Afford: It’s tempting to want a nicer car, but during bankruptcy, practicality is key. Taking on too large a payment can lead to default, repossession, and further credit damage.

Pro Tips for Success in Securing a Car Loan Pre-Discharge

Here are some expert recommendations to maximize your chances of success and make the best financial decision:

- Work Closely with Your Bankruptcy Attorney: This is paramount. They will guide you through the legal maze, ensure compliance, and help you present your case effectively to the court.

- Save for a Significant Down Payment: The more money you can put down upfront, the less you’ll need to borrow, which reduces the lender’s risk and can lead to better terms. It also demonstrates financial responsibility.

- Look for Less Expensive, Reliable Used Cars: Focus on functionality and reliability. A pre-owned vehicle that meets your basic transportation needs will be easier to finance and less financially burdensome than a brand-new model.

- Consider a Co-signer if Possible: If you have a trusted family member or friend with good credit who is willing to co-sign, it can significantly improve your loan terms and approval odds. Just ensure they understand their responsibility.

- Be Realistic About Interest Rates: Accept that interest rates will be higher. Your primary goal is to secure essential transportation and then focus on making timely payments to begin rebuilding your credit profile.

- Understand the "Why" Behind the Loan: Clearly articulate your need for the vehicle to your attorney and, if necessary, to the court. Demonstrate that it’s a necessity for work or essential living, not a luxury purchase.

What Happens After Discharge? A Brief Comparison

While this article focuses on pre-discharge loans, it’s worth noting that securing a car loan generally becomes easier once your Chapter 7 discharge is granted. Your credit score will still be low, but the bankruptcy proceedings are officially over. This means:

- You no longer need court permission to incur new debt.

- Lenders perceive a slightly lower risk because your old debts are gone, and you have a fresh slate.

- You can immediately begin rebuilding your credit through responsible new credit lines.

For more information on rebuilding your financial life after bankruptcy, you might find our article on (internal link placeholder) helpful. Understanding the differences can help you decide if waiting is a viable option.

Conclusion: A Challenging but Achievable Path

The question, "Can you get a car loan before Chapter 7 discharge?" has a nuanced answer: yes, it’s possible, but it requires diligent effort, careful planning, and, most importantly, the guidance of your bankruptcy attorney. It’s a path fraught with legal complexities and financial hurdles, primarily due to the automatic stay and the impact on your credit.

By understanding the need for court permission, preparing for less favorable loan terms, and working with specialized lenders, you can navigate this process successfully. Remember to prioritize necessity over luxury, save for a down payment, and always keep your legal counsel in the loop. Your goal during this time is to secure essential transportation while setting the stage for a strong financial future post-discharge.

For further reading on the broader implications of bankruptcy, you can consult trusted resources like the U.S. Courts Bankruptcy Basics. Understanding these foundational elements is key to making informed financial decisions.

Disclaimer: This article provides general information and does not constitute legal or financial advice. The specifics of your situation will depend on your individual circumstances and jurisdiction. Always consult with a qualified bankruptcy attorney or financial advisor for personalized guidance.