Can You Get A Car Loan With A 620 Credit Score? Your Comprehensive Guide to Approval

Can You Get A Car Loan With A 620 Credit Score? Your Comprehensive Guide to Approval Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and for many, the journey begins with a credit score check. If you’re wondering, "Can you get a car loan with a 620 credit score?", you’re not alone. This is a common question, and the answer, while not a simple "yes" or "no," is overwhelmingly positive: yes, it is absolutely possible to get a car loan with a 620 credit score.

However, simply getting approved isn’t the whole story. With a 620 credit score, you’ll likely face different terms and interest rates than someone with excellent credit. This comprehensive guide will equip you with all the knowledge, strategies, and insider tips you need to navigate the process successfully, ensuring you get the best possible deal for your situation. We’ll delve deep into understanding your credit, preparing your finances, and approaching lenders with confidence.

Can You Get A Car Loan With A 620 Credit Score? Your Comprehensive Guide to Approval

Understanding Your 620 Credit Score: What It Means for Auto Loans

Before diving into the specifics of car loans, it’s crucial to understand what a 620 credit score signifies in the eyes of lenders. Credit scores typically range from 300 to 850, and a 620 score falls squarely into the "Fair" or "Subprime" category.

This score indicates to lenders that while you have a credit history, there might be some past financial challenges or a limited credit profile. It suggests a higher level of risk compared to borrowers with "Good" or "Excellent" scores. Consequently, lenders will approach your application with more scrutiny.

Based on my experience as a financial blogger and consultant, many people misunderstand that a "fair" score means "unworthy" of a loan. This simply isn’t true. It just means you need to be more strategic and prepared. Lenders are in the business of lending money, and they have products tailored for a wide range of credit profiles, including those with a 620 score.

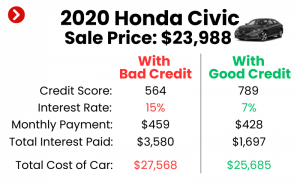

The primary impact of a 620 credit score will be on the interest rate you’re offered. Lenders compensate for the perceived higher risk by charging a higher Annual Percentage Rate (APR). This translates to higher monthly payments and a greater total cost of the loan over its term.

The Good News: Yes, Approval is Achievable!

Let’s reiterate the encouraging news: getting approved for a car loan with a 620 credit score is very much within reach. The auto lending market is vast and diverse, with numerous lenders specializing in subprime auto loans. These lenders understand that life happens, and a credit score doesn’t always tell the full story of someone’s current financial stability.

The key is to approach the process with realistic expectations and a well-thought-out strategy. While you might not walk into any dealership and get a 0% APR offer, you absolutely can secure reliable transportation with manageable terms. Your goal should be to minimize the cost of borrowing as much as possible, even with a fair credit score.

Many factors beyond your credit score influence a lender’s decision. By focusing on these other aspects, you can significantly strengthen your application and improve your chances of approval. This proactive approach will set you apart from other applicants in a similar credit bracket.

Key Factors Lenders Consider Beyond Your Credit Score

While your 620 credit score is a major piece of the puzzle, it’s not the only one. Lenders look at a holistic view of your financial health to assess risk. Understanding these additional factors and optimizing them can dramatically improve your approval odds and potentially secure better terms.

1. Your Income and Employment Stability

Lenders want to see that you have a consistent and reliable source of income to make your monthly car payments. They’ll typically look for:

- Proof of Income: Pay stubs, tax returns, bank statements.

- Employment History: How long have you been at your current job? A stable work history (e.g., 1-2 years at the same employer) signals reliability.

- Income Level: Is your income sufficient to cover the car payment comfortably, along with your other monthly expenses?

Even with a 620 credit score, a strong income and stable employment can be a powerful mitigating factor. It demonstrates your capacity to repay the loan, which is paramount for any lender.

2. Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric. It’s calculated by dividing your total monthly debt payments (credit cards, student loans, mortgage/rent, etc.) by your gross monthly income. For example, if your total monthly debt payments are $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Lenders prefer a DTI ratio below 40%, and ideally even lower, as it shows you’re not overextended. A high DTI suggests that adding another monthly payment, like a car loan, could strain your finances and increase the risk of default. If your DTI is on the higher side, consider paying down some existing debts before applying.

3. The Power of a Down Payment

Making a substantial down payment is one of the most effective strategies to improve your chances of approval and secure better loan terms with a 620 credit score. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. Not only does it make you a more attractive borrower, but it also reduces your monthly payments, decreases the total interest paid over the life of the loan, and helps prevent you from being "upside down" (owing more than the car is worth) early in the loan term. It’s a win-win situation.

4. Vehicle Choice

The type of car you choose also plays a role. Lenders are more comfortable financing vehicles that retain their value well. They’ll assess the loan-to-value (LTV) ratio, which compares the loan amount to the car’s actual market value.

Choosing a more affordable, reliable used car rather than a brand-new luxury vehicle will make your application much stronger. An expensive car might push your monthly payments and LTV ratio into a risky zone for a lender, especially with a 620 credit score. Focus on what you need and can truly afford, not just what you want.

5. Loan Term

The loan term refers to the length of time you have to repay the loan (e.g., 36, 48, 60, or 72 months). While a longer loan term means lower monthly payments, it also means you’ll pay significantly more in total interest.

With a 620 credit score, lenders might be more inclined to offer longer terms to make payments more affordable, but be cautious. Evaluate if a shorter term, even with slightly higher payments, is feasible to save money on interest in the long run. Always calculate the total cost of the loan for different terms before committing.

Strategies to Improve Your Chances of Approval

Even with a 620 credit score, you have several powerful strategies at your disposal to boost your approval odds and potentially land a better deal. Being proactive and strategic is key.

1. Save for a Larger Down Payment

As mentioned, this is arguably the most impactful step you can take. A larger down payment reduces the loan amount, lowers the lender’s risk, and shows your financial commitment. It signals responsibility and makes you a more attractive borrower.

If you can save an extra 5% or 10% beyond your initial target, it could translate into hundreds or even thousands of dollars saved on interest over the loan term. This small delay in purchasing could lead to significant long-term savings.

2. Get a Cosigner

A creditworthy cosigner with a good credit score and stable income can dramatically improve your chances of approval and help you secure a lower interest rate. A cosigner essentially guarantees the loan; if you default, they are legally responsible for the debt.

While this can be a huge benefit, it’s a serious commitment for the cosigner. Ensure both you and your cosigner fully understand the responsibilities and potential risks involved. This should typically be someone you trust implicitly, like a close family member.

3. Improve Your Credit Score (Pre-Application)

Even a small bump in your credit score can make a difference. Before applying, take steps to clean up your credit profile:

- Check Your Credit Report: Obtain free copies from Equifax, Experian, and TransUnion via AnnualCreditReport.com. Dispute any errors or inaccuracies immediately.

- Pay Bills On Time: Payment history is the biggest factor in your credit score. Make sure all your bills are paid punctually for at least 6-12 months leading up to your application.

- Reduce Existing Debt: Lowering your credit card balances can improve your credit utilization ratio, which is another major scoring factor. Aim to keep balances below 30% of your credit limit.

- Avoid New Credit Inquiries: Don’t open new credit accounts in the months leading up to your car loan application, as this can temporarily ding your score.

Even modest improvements can shift you into a slightly better risk category for lenders.

4. Choose the Right Vehicle (Affordable & Reliable)

Resist the temptation to overspend. Focus on a car that fits comfortably within your budget, both in terms of purchase price and ongoing costs (insurance, maintenance, fuel). A reliable, used vehicle that holds its value well is often the smartest choice for someone with a 620 credit score.

An affordable car minimizes the loan amount you need and reduces your monthly financial burden. This approach demonstrates financial prudence to lenders and helps ensure you can consistently make your payments.

5. Provide All Necessary Documentation

Be prepared with all the paperwork lenders will request. This typically includes:

- Proof of income (pay stubs, tax returns)

- Proof of residence (utility bills, lease agreement)

- Driver’s license

- Social Security number

- Bank statements

- References (sometimes)

Having everything organized and ready to go streamlines the application process and shows you are serious and responsible. Delays in providing documents can sometimes lead to less favorable offers.

Common mistakes to avoid are applying everywhere at once, which can lead to multiple hard inquiries and further drop your score. Instead, focus on gathering pre-approvals within a short window (typically 14-45 days) to minimize credit score impact.

Where to Get a Car Loan with a 620 Credit Score

Knowing where to apply for a car loan is just as important as knowing how to apply. Different lenders have different appetites for risk and specialize in various credit segments.

1. Dealership Financing

Many dealerships offer in-house financing or work with a network of lenders. This can be convenient, as you can often complete the purchase and financing in one place. Dealerships often partner with subprime lenders, making them a viable option for those with a 620 credit score.

- Captive Lenders: These are financing arms of car manufacturers (e.g., Ford Credit, Toyota Financial Services). While they often offer competitive rates for excellent credit, they may have specific programs for subprime borrowers too.

- Buy Here Pay Here (BHPH) Dealerships: These dealerships finance loans directly. While they are almost guaranteed to approve you regardless of your credit score, they typically charge extremely high interest rates and may not report to all credit bureaus, limiting your ability to rebuild credit. Pro tip: Use BHPH as a last resort.

2. Banks & Credit Unions

Traditional banks and credit unions are excellent places to start your search. If you have an existing relationship with a bank or credit union (e.g., a checking account, savings account), they may be more willing to work with you, even with a 620 credit score.

Credit unions, in particular, are known for being member-focused and often offer more flexible terms and slightly lower interest rates than traditional banks, especially for those with fair credit. It’s always worth checking with your current financial institution first.

3. Online Lenders Specializing in Subprime Loans

The digital age has brought a rise in online lenders that specialize in various credit profiles, including subprime auto loans. These lenders often have streamlined application processes and can provide pre-approvals quickly. They often have a broader network of lenders and may be able to match you with a lender willing to approve your 620 credit score.

Many online platforms allow you to get pre-qualified with a soft credit inquiry, which won’t hurt your credit score. This allows you to compare offers from multiple lenders before committing to a hard inquiry.

To explore different types of auto lenders and their unique offerings, you might find our article on Understanding Different Types of Auto Lenders helpful. (Internal Link Placeholder 1)

Understanding Interest Rates and Loan Terms

With a 620 credit score, it’s crucial to have realistic expectations about interest rates. You will almost certainly face a higher APR than someone with excellent credit. This is how lenders mitigate the increased risk associated with subprime borrowers.

Expect Higher Rates

For a 620 credit score, you might see APRs ranging anywhere from 8% to 20% or even higher, depending on the lender, market conditions, and other factors like your down payment and DTI. While this might seem high, it’s a common reality for fair credit borrowers. The goal is to find the lowest rate you can qualify for, not necessarily the lowest rate in the market.

APR vs. Interest Rate

It’s important to understand the difference. The interest rate is the percentage you pay on the principal loan amount. The APR (Annual Percentage Rate) includes the interest rate plus any additional fees or charges associated with the loan, giving you a more accurate picture of the total annual cost of borrowing. Always compare APRs when evaluating loan offers.

Impact of Loan Term

While a longer loan term (e.g., 72 months) can reduce your monthly payment, it significantly increases the total amount of interest you’ll pay over the life of the loan. For instance, a $20,000 loan at 15% APR over 72 months will cost you much more in total interest than the same loan over 48 months, even if the monthly payment is higher for the shorter term.

Always calculate the total cost of the loan for different terms. Sometimes, a slightly higher monthly payment for a shorter term is well worth the thousands of dollars saved in interest.

Negotiating Tips

Even with a 620 credit score, there’s room for negotiation. Once you have a pre-approval from one lender, use it as leverage to see if another lender (or the dealership’s finance department) can beat the offer. Be prepared to walk away if the terms aren’t favorable. Having a pre-approval gives you power.

The Application Process: What to Expect

Navigating the application process can seem daunting, but breaking it down into steps makes it manageable.

- Gather Your Documents: As mentioned, have all your financial paperwork ready before you even start looking at cars. This includes proof of income, residence, identification, and any other relevant financial statements.

- Get Pre-Qualified/Pre-Approved: This is a crucial step. Seek pre-qualification from multiple lenders (banks, credit unions, online lenders). Pre-qualification typically involves a soft credit inquiry, which doesn’t hurt your score, and gives you an idea of the loan amount and interest rate you might qualify for. A pre-approval often involves a hard inquiry but provides a firm offer.

- Compare Offers: Don’t take the first offer you receive. Compare APRs, loan terms, and any associated fees from various lenders. Remember, you want the lowest total cost, not just the lowest monthly payment.

- Visit Dealerships (Armed with Pre-Approval): Once you have a pre-approval in hand, you become a cash buyer in the eyes of the dealership. This gives you significant leverage in negotiating the car’s price, separate from the financing. If the dealership’s finance department can beat your pre-approval, great! If not, you have your pre-approved loan ready to go.

- Understand the Fine Print: Before signing anything, read the entire loan agreement carefully. Understand the APR, loan term, any prepayment penalties, and all fees. Ask questions until you’re completely clear on every detail.

For more detailed information on understanding your credit score and its impact, the Consumer Financial Protection Bureau (CFPB) offers excellent resources on credit reports and scores. (External Link Placeholder: e.g., www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/)

Post-Approval: Managing Your Loan and Improving Credit

Getting the car loan is just the first step. Effectively managing it can significantly improve your credit score over time, opening doors to better financial opportunities in the future.

Make Timely Payments

This is the most critical aspect. Consistent, on-time payments are the most powerful way to rebuild and improve your credit score. Set up automatic payments to avoid missing due dates. Every on-time payment builds positive payment history, which is the largest factor in your credit score.

Avoid Missed Payments

A single missed payment can severely damage your credit score, undoing months of hard work. If you anticipate difficulty making a payment, contact your lender immediately to discuss options. Don’t wait until you’re already late.

Refinancing Opportunities

Once you’ve made 6-12 months of on-time payments, your credit score is likely to improve. At this point, you might be a candidate for refinancing your car loan. Refinancing allows you to replace your current loan with a new one, often with a lower interest rate, which can significantly reduce your monthly payments and total interest paid.

This is a common and highly effective strategy for those who initially secured a loan with a subprime credit score. It’s a testament to your improved creditworthiness.

To learn more about when and how to refinance your car loan, check out our in-depth guide on Refinancing Your Car Loan: When and How to Save Money. (Internal Link Placeholder 2)

Common Mistakes to Avoid When Seeking a Car Loan with a 620 Credit Score

Even with the best intentions, it’s easy to fall into common traps that can hinder your car loan process or lead to a less favorable outcome.

- Not Checking Your Credit Report: Going into the process blind is a major mistake. Always check your credit report for errors and have a clear understanding of your score before applying.

- Applying Everywhere: While comparing offers is good, indiscriminately applying to dozens of lenders can lead to multiple hard inquiries, which can temporarily lower your credit score. Focus on a few pre-qualifications first.

- Focusing Only on Monthly Payments: Don’t let a low monthly payment seduce you into a longer loan term with a significantly higher total cost. Always look at the total interest paid and the overall cost of the loan.

- Ignoring the Down Payment: Underestimating the power of a down payment can leave you with higher interest rates and a less attractive loan offer. Save as much as you can.

- Buying More Car Than You Can Afford: This is a classic pitfall. With a fair credit score, it’s even more crucial to be conservative with your budget. Overextending yourself financially can lead to payment struggles and further credit damage.

- Not Understanding the Loan Terms: Never sign a document you haven’t fully read and understood. Ask questions about every clause, fee, and condition until you are completely clear.

Conclusion: Your Road to Car Loan Approval with a 620 Credit Score

The question "Can you get a car loan with a 620 credit score?" has a resounding answer: yes, you absolutely can. While it presents a few more challenges than having excellent credit, it is a very achievable goal with the right approach.

By understanding what your 620 credit score means, focusing on factors beyond your score like income and down payment, strategically approaching various lenders, and being diligent about managing your loan post-approval, you can successfully secure a car loan. More importantly, this process can be a powerful step toward rebuilding and strengthening your credit for future financial endeavors.

Remember, preparation, patience, and a clear understanding of your financial situation are your greatest assets. Take the time to gather your documents, compare offers, and choose a vehicle and loan terms that genuinely fit your budget. Your journey to car ownership, even with a fair credit score, is well within reach.

Have you successfully secured a car loan with a 620 credit score? Share your experiences and tips in the comments below!