Can You Get a Car Loan with a 630 Credit Score? Your Comprehensive Guide to Driving Away Confidently

Can You Get a Car Loan with a 630 Credit Score? Your Comprehensive Guide to Driving Away Confidently Carloan.Guidemechanic.com

Securing a car loan is a significant financial step, and for many, the journey begins with a glance at their credit score. If you’re wondering, "Can I get a car loan with a 630 credit score?", the short answer is yes, it’s absolutely possible! While a 630 credit score might place you in what lenders often categorize as the "fair" or "subprime" range, it certainly doesn’t close the door to car ownership.

This comprehensive guide will walk you through everything you need to know about getting an auto loan with a 630 credit score. We’ll explore the realities of your situation, equip you with strategies to improve your chances of approval, and help you navigate the lending landscape to secure the best possible terms. Our goal is to empower you with knowledge, turning a potentially challenging situation into a clear path forward.

Can You Get a Car Loan with a 630 Credit Score? Your Comprehensive Guide to Driving Away Confidently

Understanding Your 630 Credit Score: What It Means for Auto Loans

Before diving into the "how-to," let’s clarify what a 630 credit score signifies in the world of lending. Credit scores typically range from 300 to 850, and a 630 score falls squarely in the "fair" category according to FICO and VantageScore models. This means you’ve likely had some credit history, but perhaps with a few bumps along the way, or your credit file is relatively thin.

Lenders use credit scores to assess risk. A higher score indicates a lower risk of default, while a lower score suggests a higher risk. With a 630 score, lenders perceive you as a moderate risk borrower. This perception directly impacts the loan terms you’ll be offered.

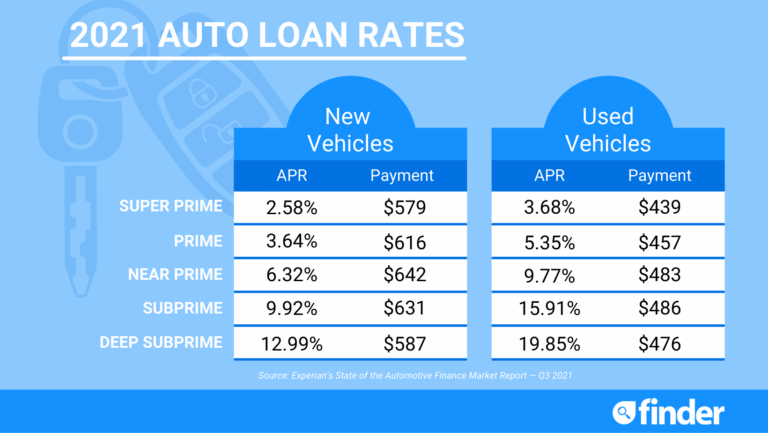

While it’s not considered "bad credit," a 630 score typically means you won’t qualify for the lowest interest rates advertised. You should expect to pay a higher Annual Percentage Rate (APR) compared to someone with excellent credit. However, it’s far from an insurmountable hurdle, and many lenders specialize in assisting individuals in your credit range.

The Reality of Getting a Car Loan with a 630 Credit Score

So, let’s cut to the chase: can you truly get an auto loan with a 630 credit score? Absolutely. Many people successfully secure car financing with scores in this range every single day. The key is to manage your expectations and prepare thoroughly.

Based on my experience as a financial blogger and working with numerous individuals navigating auto financing, a 630 credit score puts you in a position where proactive steps are crucial. You won’t simply walk into any dealership and expect prime rates, but with the right approach, you can secure a loan that fits your budget. The market for subprime auto loans is robust, reflecting the large number of consumers with fair credit scores.

What does this mean for you? It means you’ll likely encounter a wider range of interest rates, and the loan approval process might require a bit more documentation. Don’t be discouraged by initial offers; instead, use this as motivation to explore all your options and strengthen your application.

Beyond the Score: Factors Lenders Consider

Your credit score is undoubtedly important, but it’s just one piece of the puzzle. Lenders look at several other factors to get a complete picture of your financial health and ability to repay a loan. Understanding these elements can significantly boost your chances of approval and help you negotiate better terms.

1. Your Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a critical metric lenders examine. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your total monthly debt (car payment, student loans, credit cards, rent/mortgage) is $1,500 and your gross monthly income is $4,000, your DTI is 37.5%.

Lenders prefer a lower DTI, typically under 43%, as it indicates you have enough disposable income to comfortably manage new debt. A high DTI, even with a decent credit score, can signal financial strain and make lenders hesitant. Proactively reducing your existing debt before applying can make a significant difference.

2. Payment History and Credit Utilization

While your 630 score reflects your overall payment history, lenders will often delve deeper into your credit report. They want to see consistent, on-time payments, especially on previous auto loans or similar installment debts. A few late payments in the past might be acceptable, but a pattern of missed payments will be a red flag.

Credit utilization – the amount of credit you’re using compared to your total available credit – also plays a role. Keeping your credit card balances low (ideally below 30% of your limit) demonstrates responsible credit management and can positively influence a lender’s decision.

3. Employment Stability and Income Verification

Lenders need assurance that you have a steady source of income to make your monthly payments. They’ll typically ask for proof of employment, such as recent pay stubs, W-2 forms, or tax returns if you’re self-employed. A consistent work history with the same employer for a year or more is generally viewed favorably.

Fluctuating income or frequent job changes might lead lenders to perceive a higher risk. If you’ve recently started a new job, be prepared to provide additional documentation or explain your employment situation clearly. Stability equals reliability in the eyes of a lender.

4. The Power of a Down Payment

Making a significant down payment is one of the most impactful strategies when you have a 630 credit score. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your commitment and financial stability.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price. Not only does it make your application more attractive, but it also reduces your monthly payments, decreases the total interest you’ll pay over the life of the loan, and helps prevent you from being "upside down" on your loan (owing more than the car is worth) early on.

5. Vehicle Choice

The type of vehicle you choose can also influence loan approval. Lenders often look at the age and mileage of the car. Newer, lower-mileage vehicles typically hold their value better, making them less risky collateral for the lender. This doesn’t mean you can’t get a loan for an older car, but it might come with stricter terms.

Additionally, the purchase price should align with your income. Trying to finance a luxury car with a moderate income and a 630 credit score is often a non-starter. Opting for a more affordable, reliable vehicle that fits comfortably within your budget will significantly increase your chances of approval.

6. The Benefit of a Co-Signer

If you’re struggling to get approved or offered unfavorable terms, a co-signer with excellent credit can be a game-changer. A co-signer legally agrees to be responsible for the loan if you fail to make payments. This significantly reduces the lender’s risk, as they have another party to pursue for repayment.

While a co-signer can open doors, it’s a serious commitment for both parties. Ensure both you and your co-signer fully understand the responsibilities and potential impact on their credit if you default. It’s a relationship decision as much as a financial one.

Strategies to Improve Your Chances of Approval (and Better Terms)

Knowing what lenders look for is the first step; the next is actively working to present yourself as the best possible borrower. Here are actionable strategies to enhance your application when seeking a car loan with a 630 credit score.

1. Check Your Credit Report Thoroughly

Before you even think about applying for a loan, pull your credit reports from all three major bureaus (Experian, Equifax, and TransUnion). You’re entitled to a free report from each once a year. Visit AnnualCreditReport.com to access yours.

Scrutinize every detail for errors. Incorrect late payments, accounts you don’t recognize, or outdated information can unfairly drag down your score. Disputing and correcting these errors can potentially boost your score quickly, making a real difference in your loan prospects.

2. Save for a Substantial Down Payment

We’ve mentioned it before, but it bears repeating: a larger down payment is your best friend with a 630 credit score. It shows lenders you have skin in the game and reduces their exposure. It also directly lowers your loan amount, which means less interest paid over time.

Consider delaying your car purchase for a few months if it means saving an extra few thousand dollars for a down payment. This patience can translate into significant savings on interest and a much smoother approval process.

3. Get Pre-Approved

One of the smartest moves you can make is to get pre-approved for a loan before stepping onto a dealership lot. Pre-approval involves a lender reviewing your financial information and giving you a conditional offer for a specific loan amount and interest rate.

Benefits of pre-approval:

- Know your budget: You’ll know exactly how much car you can afford.

- Stronger negotiation power: You become a cash buyer, negotiating on price, not just monthly payments.

- Compare rates: You can compare the pre-approved offer with dealership financing, ensuring you get the best deal.

- Reduced stress: Focus on finding the right car, not scrambling for financing.

4. Opt for an Affordable Vehicle

Resist the urge to overspend. With a 630 credit score, securing a loan for a brand-new, top-of-the-line vehicle will be challenging and likely come with prohibitive interest rates. Focus on reliable, used cars that meet your needs without stretching your budget.

A lower purchase price means a smaller loan amount, which is easier to get approved for and more manageable to repay. Remember, your goal is to build good credit history with this loan, potentially opening doors to better rates on your next vehicle.

5. Improve Your Credit Score (Long-Term Strategy)

While you might need a car now, continuously working on your credit score is always a good idea. Here are some quick tips:

- Pay all bills on time, every time. Payment history is the most significant factor in your score.

- Reduce credit card balances. Lowering your credit utilization ratio can provide a quick boost.

- Avoid opening new credit accounts right before or during your car loan application process.

- Keep old accounts open. A longer credit history is generally better.

For more in-depth strategies, you might want to check out our article on How to Improve Your Credit Score Fast (internal link placeholder).

Where to Look for a Car Loan with a 630 Credit Score

Not all lenders are created equal, especially when it comes to borrowers with fair credit. Knowing where to focus your search can save you time and help you find competitive offers.

1. Credit Unions

Credit unions are often an excellent starting point. As member-owned, non-profit organizations, they are known for being more flexible and offering more favorable rates and terms to members, even those with less-than-perfect credit. Their focus is on serving their members rather than maximizing profits for shareholders.

If you’re already a member of a credit union, or if you qualify for membership, definitely check their auto loan rates first. You might be pleasantly surprised by what they can offer.

2. Online Lenders Specializing in Subprime Loans

The digital age has brought a surge of online lenders who specialize in working with borrowers across the credit spectrum, including those with 630 credit scores. These lenders often have streamlined application processes and can provide quick pre-approvals. They also have access to a wider network of financial institutions.

Websites like Capital One Auto Finance, Carvana, and various loan aggregators can connect you with multiple lenders who are willing to work with fair credit. Always read reviews and compare offers from several different online platforms.

3. Dealership Financing

Most car dealerships offer in-house financing or work with a network of banks and finance companies. This can be convenient, as you can handle the car purchase and loan application all in one place. Dealerships often have relationships with "subprime" lenders who specifically cater to borrowers with credit scores like 630.

Pro tips from us: While convenient, be cautious. Dealerships sometimes mark up interest rates to increase their profit. Always arrive with a pre-approval in hand from another lender (like a credit union or online lender) to use as leverage for negotiation.

4. Local Banks

If you have an existing banking relationship, it’s worth checking with your local bank. While traditional banks can sometimes be stricter with their lending criteria for fair credit scores, your existing relationship might give you an edge. They already have a history with you, which can sometimes compensate for a lower credit score.

The Application Process: What to Expect

Once you’ve identified potential lenders, the application process will require some preparation. Being organized can make it much smoother.

1. Gather Your Documents

Lenders will need to verify your identity, income, and residence. Be ready to provide:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (for self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Bank Statements: To verify funds for a down payment.

- Vehicle Information: If you’ve already picked out a car (VIN, mileage, year).

2. Understand Loan Terms

Don’t just look at the monthly payment. Dive deep into the entire loan agreement:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees. Compare APRs, not just interest rates.

- Loan Duration (Term): Shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but significantly more interest over the life of the loan. With a 630 credit score, you might be offered longer terms, but weigh the total cost carefully.

- Total Cost of the Loan: Calculate how much you’ll pay back in total (principal + interest).

For a deeper dive into how interest rates work, consider reading our article on Understanding Auto Loan Interest Rates (internal link placeholder).

3. The Impact of Multiple Inquiries

Applying for multiple loans typically results in multiple "hard inquiries" on your credit report, which can temporarily lower your score. However, credit scoring models are smart enough to recognize when you’re rate shopping for a single loan.

Most models will count multiple auto loan inquiries made within a short period (typically 14-45 days, depending on the model) as a single inquiry. This allows you to shop around for the best rates without unduly harming your score. So, get all your applications submitted within a concentrated window.

Common Mistakes to Avoid When Getting a Car Loan with Fair Credit

Navigating the auto loan process with a 630 credit score requires vigilance. Common mistakes to avoid are often rooted in a lack of preparation or succumbing to pressure. Being aware of these pitfalls can save you money and stress.

- Not Checking Your Credit Report: Going in blind is a huge disadvantage. You might miss errors or not understand your score’s components, making you less prepared to discuss your credit with lenders.

- Only Applying with One Lender: This is perhaps the biggest mistake. Without comparing offers, you have no way of knowing if you’re getting a competitive rate. Always get at least 3-4 quotes.

- Ignoring the Down Payment: As discussed, a robust down payment is your secret weapon. Skimping on it means a higher loan amount, higher monthly payments, and more interest over time.

- Falling for "Guaranteed Approval" Scams: Be wary of lenders promising "guaranteed approval" regardless of your credit score. These often come with predatory interest rates, hidden fees, or unfavorable terms designed to trap you.

- Buying More Car Than You Can Afford: It’s easy to get excited and stretch your budget for a dream car. However, an unaffordable payment can lead to financial strain, missed payments, and further damage to your credit. Stick to a budget that leaves room for other expenses.

- Not Reading the Fine Print: Always read the entire loan agreement before signing. Understand all fees, penalties for late payments, and early repayment clauses. If something isn’t clear, ask questions until it is.

Post-Approval: Managing Your Loan and Improving Your Credit

Congratulations, you’ve secured your car loan! The journey doesn’t end here. This loan is a powerful tool you can use to significantly improve your credit score and open doors to better financial opportunities in the future.

1. Make Timely Payments, Every Time

This is non-negotiable. Consistent, on-time payments are the single most effective way to build a positive credit history. Set up automatic payments, mark your calendar, or do whatever it takes to ensure you never miss a due date. Each on-time payment reinforces your reliability as a borrower.

2. Consider Refinancing Down the Line

As you make consistent payments and your credit score improves (which it will if you manage this loan well), you might become eligible for better interest rates. After 6-12 months of on-time payments, your credit score could see a significant bump.

At that point, explore refinancing your auto loan. This means taking out a new loan with a lower interest rate to pay off your current one. Refinancing can substantially reduce your monthly payments and the total interest you pay over the life of the loan.

3. How This Loan Can Help Your Credit

Successfully managing a car loan with a 630 credit score demonstrates to future lenders that you can handle installment debt responsibly. It adds a positive tradeline to your credit report, diversifies your credit mix (if you previously only had credit cards), and lengthens your credit history. All these factors contribute to a higher credit score over time, paving the way for better rates on mortgages, personal loans, and credit cards down the road.

Conclusion: Driving Forward with Confidence

So, can you get a car loan with a 630 credit score? Absolutely. While it requires a strategic approach and a bit more preparation than someone with excellent credit, it is a very achievable goal. Your 630 credit score is a starting point, not a roadblock.

By understanding what lenders look for, taking proactive steps like securing a substantial down payment and getting pre-approved, and diligently comparing offers, you can secure a loan that fits your budget. Remember to avoid common pitfalls and use this opportunity to build a stronger financial future. With careful planning and responsible management, you’ll not only drive away in your new car but also drive your credit score towards a brighter horizon.