Can You Get a Car Loan with Derogatory Marks? Your Comprehensive Guide to Driving Away Despite Bad Credit

Can You Get a Car Loan with Derogatory Marks? Your Comprehensive Guide to Driving Away Despite Bad Credit Carloan.Guidemechanic.com

Getting a car is often more than just a convenience; for many, it’s a necessity for work, family, and daily life. But what happens when your credit history isn’t perfect, marred by what financial institutions call "derogatory marks"? The thought of applying for a car loan can feel daunting, even impossible. You might be asking yourself, "Can I really get a car loan with derogatory marks on my credit report?"

The short answer is yes, it is absolutely possible. However, the path isn’t always straightforward, and it requires a strategic approach. As an expert blogger and professional SEO content writer who has seen countless individuals navigate these waters, I understand the challenges and the proven solutions. This comprehensive guide will equip you with the knowledge, strategies, and confidence to secure a car loan, even when your credit has taken a hit. We’ll delve deep into understanding derogatory marks, exploring your options, and offering actionable advice to put you in the driver’s seat.

Can You Get a Car Loan with Derogatory Marks? Your Comprehensive Guide to Driving Away Despite Bad Credit

What Exactly Are Derogatory Marks on Your Credit Report?

Before we dive into getting a loan, it’s crucial to understand what we’re up against. Derogatory marks are essentially negative entries on your credit report that indicate a failure to meet your financial obligations. These marks signal to lenders that you’ve had trouble managing credit in the past, making you a higher risk.

These entries can significantly lower your credit score and remain on your report for several years. The type and severity of the derogatory mark determine its impact and how long it stays. Knowing what’s on your report is the first step toward addressing it.

Common Types of Derogatory Marks

Based on my experience, these are the most frequently encountered derogatory marks that impact car loan eligibility:

- Late Payments (30, 60, 90+ Days Past Due): This is perhaps the most common derogatory mark. Even a single payment missed by 30 days can hurt your score. The longer the payment is late, the more severe the impact.

- Collection Accounts: When an original creditor gives up on collecting a debt, they may sell it to a third-party collection agency. A collection account on your report indicates that a debt was so overdue it was sent to collections.

- Charge-Offs: Similar to collections, a charge-off occurs when a creditor deems a debt uncollectible and writes it off as a loss. This doesn’t mean you’re off the hook for the debt, but it’s a severe negative mark.

- Bankruptcies (Chapter 7 or 13): A bankruptcy is a legal process to discharge or restructure debts. It’s one of the most severe derogatory marks and can stay on your report for up to 10 years, significantly impacting your ability to get new credit.

- Foreclosures: This occurs when a lender repossesses a home due to the borrower’s failure to make mortgage payments. It’s a major negative event that signals significant financial distress.

- Repossessions: If you fail to make payments on a secured loan, such as an auto loan, the lender can repossess the collateral (your car). A repossession on your credit report makes future auto loans particularly challenging.

Each of these marks tells a story to potential lenders, and it’s not always a positive one. Understanding their presence and impact is vital for preparing your loan application.

The Reality: Can You Really Get a Car Loan with Derogatory Marks?

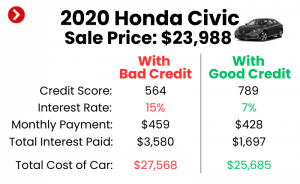

Yes, absolutely! Let me reiterate: you can get a car loan with derogatory marks. It’s not an automatic disqualifier. However, it’s important to set realistic expectations. Lenders view derogatory marks as indicators of higher risk. This often translates into specific terms for your loan.

You might face higher interest rates compared to someone with excellent credit. This is how lenders compensate for the increased risk they are taking. Additionally, you might be required to provide a larger down payment or secure a co-signer. Don’t be discouraged by these possibilities; instead, view them as steps you can take to make your loan application more appealing.

The key is to demonstrate to lenders that despite past challenges, you are now a reliable borrower. This requires preparation, transparency, and a solid strategy.

Strategies to Improve Your Chances of Approval

Navigating the car loan landscape with derogatory marks requires a proactive and informed approach. Based on my experience helping individuals secure financing, these strategies can significantly improve your odds of approval.

1. Understand and Clean Up Your Credit Report

This is your first and most critical step. You cannot fix what you don’t know is broken.

- Obtain Your Free Credit Reports: You are entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once every 12 months. Visit AnnualCreditReport.com to get yours.

- Scrutinize for Errors: Carefully review every entry. Mistakes, such as incorrect payment dates, accounts that aren’t yours, or debts that have passed their reporting period, are surprisingly common.

- Dispute Inaccuracies: If you find errors, dispute them immediately with the credit bureau and the creditor. Removing inaccurate derogatory marks can provide an instant boost to your credit score. This simple step can make a world of difference.

2. Save for a Substantial Down Payment

A larger down payment is one of the most powerful tools in your arsenal when applying for a car loan with derogatory marks.

- Reduces Lender Risk: A significant down payment reduces the amount of money you need to borrow, thereby lowering the lender’s risk. If you default, they lose less.

- Shows Financial Commitment: It demonstrates to the lender that you are financially committed to the purchase and have the discipline to save money.

- Lower Monthly Payments & Interest: A larger down payment also translates to lower monthly payments and less interest paid over the life of the loan. Pro tips from us: Aim for at least 10-20% of the car’s value, or even more if possible.

3. Find a Reliable Co-signer

A co-signer with good credit can be a game-changer. This individual agrees to be equally responsible for the loan if you fail to make payments.

- Mitigates Risk: The co-signer’s good credit history provides an extra layer of security for the lender, making them more comfortable approving your application.

- Potential for Better Terms: With a co-signer, you might qualify for a lower interest rate and more favorable loan terms than you would on your own.

- Choose Wisely: Select a co-signer you trust implicitly and who understands the significant responsibility they are undertaking. Their credit will be affected if you miss payments.

4. Consider a Secured Loan

While most auto loans are secured by the vehicle itself, if your credit is severely damaged, some lenders might require additional collateral or offer specific secured loan products.

- Collateral Reduces Risk: If you have another asset, like a savings account or a certificate of deposit (CD), a lender might allow you to use it as collateral for the loan. This further reduces their risk.

- Not Always Necessary for Auto Loans: Remember, auto loans are typically secured loans already, meaning the car itself acts as collateral. However, if your credit is very challenging, showing additional assets can strengthen your application.

5. Demonstrate Financial Stability

Lenders look beyond just your credit score. They want to see your current ability to repay.

- Stable Income: A steady job with consistent income shows you have the means to make payments. Be prepared to provide pay stubs or tax returns.

- Employment History: A long history with the same employer indicates stability and reliability.

- Residency History: Demonstrating stable residency (e.g., living at the same address for several years) can also be viewed favorably.

- Low Debt-to-Income Ratio: Your debt-to-income (DTI) ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to manage new debt. Paying down existing debts before applying can improve this ratio.

Types of Lenders to Consider When You Have Derogatory Marks

Not all lenders are created equal, especially when it comes to bad credit car loans. Knowing where to look can save you time and frustration.

1. Subprime Lenders and Dealerships

These lenders specialize in working with individuals who have less-than-perfect credit.

- Focus on Risk Assessment: They have different underwriting criteria that weigh factors beyond just your credit score, such as your income, employment stability, and the size of your down payment.

- Higher Interest Rates: Expect to pay higher interest rates, as this is how they mitigate the increased risk associated with lending to subprime borrowers.

- Dealership Financing: Many dealerships have relationships with multiple subprime lenders, allowing you to apply for financing directly at the dealership. This can streamline the process.

2. Credit Unions

Credit unions are member-owned financial institutions known for their customer-centric approach.

- Potentially More Flexible: They often have more flexible lending criteria than traditional banks and may be more willing to work with members who have derogatory marks, especially if you have a long-standing relationship with them.

- Competitive Rates: While not always as low as prime rates, credit unions often offer more competitive interest rates than other subprime lenders.

- Membership Required: You typically need to be a member to apply for a loan, which usually involves meeting specific eligibility requirements (e.g., living in a certain area, working for a particular employer).

3. Online Lenders Specializing in Bad Credit

The digital age has brought forth a host of online lenders who cater specifically to borrowers with bad credit.

- Convenience: The application process is often quick and entirely online, allowing you to get pre-qualified from the comfort of your home.

- Wide Network: Many online platforms act as aggregators, connecting you with multiple lenders who are willing to offer loans to individuals with derogatory marks.

- Varying Terms: Terms and rates can vary widely, so it’s essential to compare offers from several online lenders.

4. Buy Here, Pay Here (BHPH) Dealerships

These dealerships offer in-house financing, meaning they are both the seller and the lender.

- Last Resort Option: While they often approve borrowers regardless of credit history, BHPH dealerships typically come with significant drawbacks.

- Very High Interest Rates: Interest rates at BHPH dealerships are notoriously high, often reaching the maximum legal limit.

- Limited Vehicle Selection: The vehicles are often older, higher mileage, and may not come with extensive warranties.

- Predatory Practices: Common mistakes to avoid are falling into the trap of predatory lending. Some BHPH places have less transparency and can lead to a cycle of debt. Use this option only if all others have been exhausted.

The Application Process: What to Expect

When you’re ready to apply for a car loan with derogatory marks, knowing what to expect can ease the stress.

1. Gather All Necessary Documents

Lenders will want to verify your identity, income, and residency. Be prepared with:

- Proof of Income: Recent pay stubs (last 1-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Identification: Driver’s license or state ID.

- Proof of Insurance: You’ll need this before driving off the lot.

- References: Some lenders might ask for personal or professional references.

2. Understand Pre-qualification vs. Full Application

- Pre-qualification: This is a soft credit check that doesn’t harm your credit score. It gives you an idea of what loan amount and interest rate you might qualify for. Pro tips from us: Use pre-qualification to shop around without impacting your score.

- Full Application: This involves a hard credit inquiry, which will temporarily ding your score by a few points. This is done when you’re serious about a specific loan offer.

3. Be Transparent About Your Financial History

Don’t try to hide your derogatory marks. Lenders will see them.

- Honesty is the Best Policy: Be upfront about past financial challenges. Explain what happened and, more importantly, what you’ve done to improve your situation since then.

- Show Improvement: Highlight any positive changes, such as consistent on-time payments recently, or a lower debt-to-income ratio. This demonstrates accountability and a commitment to financial recovery.

4. Negotiate Terms Where Possible

Even with derogatory marks, there might be some room for negotiation, especially if you have a strong down payment or a co-signer.

- Focus on the Total Cost: Don’t just look at the monthly payment. Consider the interest rate, the loan term, and any fees. A lower monthly payment over a longer term might mean paying significantly more in interest.

- Be Prepared to Walk Away: If the terms are unfavorable or you feel pressured, don’t be afraid to walk away. There are other options.

Pro Tips for Navigating the Process

Based on my years of observing financial trends and helping people, here are some invaluable tips for securing a car loan with derogatory marks:

- Shop Around for Rates: Don’t take the first offer you receive. Apply for pre-qualification with several lenders (online, credit unions, dealerships) to compare interest rates and terms. All hard inquiries within a 14-45 day window for the same type of loan are usually counted as one for scoring purposes.

- Don’t Apply Everywhere at Once (Mind the Hard Inquiries): While shopping around is good, avoid submitting full applications to too many places over an extended period. Group your applications within a short timeframe to minimize the impact on your credit score.

- Read the Fine Print Meticulously: Understand every clause in your loan agreement. Pay attention to prepayment penalties, late fees, and what happens if you miss a payment.

- Avoid Unnecessary Add-ons: Dealerships might try to sell you extended warranties, GAP insurance, or other extras. While some can be beneficial, they also increase your loan amount and interest paid. Only opt for what you truly need and understand.

- Focus on Affordability: The goal is to get a car, but more importantly, to keep it. Ensure your monthly car payment, including insurance, fits comfortably within your budget. Don’t overextend yourself, as this can lead to further financial difficulties.

Long-Term Credit Repair: Beyond the Car Loan

Securing a car loan with derogatory marks is a significant achievement, but it’s also an opportunity to rebuild your credit for the long term. This car loan can be a powerful tool for credit repair.

- Make Timely Payments: This is paramount. Every on-time payment on your new car loan will slowly, steadily, and positively impact your credit score. It shows lenders you can manage credit responsibly.

- Keep Credit Utilization Low: If you have credit cards, try to keep your balances low relative to your credit limits. This demonstrates responsible credit management.

- Build an Emergency Fund: Unexpected expenses can derail even the best financial plans. An emergency fund provides a buffer against financial shocks, helping you avoid missing loan payments.

- Review Your Credit Report Regularly: Continue to monitor your credit reports for accuracy and progress. Seeing your score improve can be highly motivating.

For more in-depth strategies, consider exploring resources on improving your financial standing. .

Common Mistakes to Avoid When Seeking a Car Loan with Bad Credit

When you’re eager to get a car, it’s easy to overlook potential pitfalls. Being aware of these common mistakes can save you a lot of headache and money.

- Ignoring Your Credit Report: As discussed, not knowing what’s on your report or failing to dispute errors is a major oversight. It’s like going into battle blindfolded.

- Settling for the First Offer: Desperation can lead to accepting the first loan offer, even if it has exorbitant interest rates or unfavorable terms. Always compare multiple offers.

- Taking on Unaffordable Payments: Overestimating your budget or succumbing to pressure to buy a more expensive car can lead to missed payments, further damaging your credit and risking repossession.

- Falling for Predatory Lenders: Be wary of lenders who guarantee approval without any credit check, charge excessive upfront fees, or pressure you into signing without reading. These are red flags.

- Not Asking Questions: If you don’t understand something in the loan agreement, ask! A reputable lender will be happy to explain. Don’t sign anything you’re unsure about.

Conclusion: Your Road to a Car Loan is Possible

The journey to getting a car loan with derogatory marks can seem challenging, but it is far from impossible. By understanding what derogatory marks are, preparing your finances, knowing which lenders to approach, and adopting a strategic mindset, you can significantly increase your chances of approval. Remember, your past financial challenges do not define your future potential.

Take the time to check your credit report, save for a solid down payment, and consider a co-signer if needed. Be transparent with lenders and prioritize affordability over fancy features. This car loan isn’t just about getting new wheels; it’s an opportunity to demonstrate financial responsibility and rebuild your credit for a brighter future.

Don’t let past financial missteps prevent you from achieving your goals. With the right approach and a bit of perseverance, you can drive away in a car that meets your needs and helps you on your path to financial recovery. Start your journey today – the road ahead is clearer than you think!

External Link: For more information on understanding and managing your credit, visit the Consumer Financial Protection Bureau’s official website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/