Can You Get a Car Loan With Poor Credit? Your Ultimate Guide to Driving Away Confidently

Can You Get a Car Loan With Poor Credit? Your Ultimate Guide to Driving Away Confidently Carloan.Guidemechanic.com

Are you dreaming of a new set of wheels, but a quick glance at your credit score leaves you feeling deflated? The question, "Can I get a car loan with poor credit?" is one that echoes in the minds of many. It’s a valid concern, and for a long time, having less-than-perfect credit seemed like an insurmountable barrier to vehicle ownership.

But here’s the good news: Yes, you absolutely can get a car loan with poor credit. It might require a bit more effort, strategic planning, and a deep understanding of the process, but it is far from impossible. In fact, countless individuals with credit challenges successfully secure auto financing every single day.

Can You Get a Car Loan With Poor Credit? Your Ultimate Guide to Driving Away Confidently

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. Based on my experience and extensive research, I know that navigating the landscape of car loans with poor credit can feel like walking through a maze. My goal with this comprehensive guide is to equip you with the knowledge, strategies, and confidence you need to secure a car loan, even when your credit score isn’t pristine. We’ll cover everything from understanding your credit to finding the right lenders and making smart financial decisions.

Let’s break down the myths, uncover the opportunities, and pave your way to car ownership.

Understanding "Poor Credit" and Its Real-World Impact on Car Loans

Before we dive into solutions, it’s crucial to understand what "poor credit" actually means in the eyes of a lender. Your credit score is essentially a three-digit report card on your financial reliability. It tells lenders how likely you are to repay your debts.

What Defines Poor Credit?

Credit scores, most commonly FICO scores, range from 300 to 850. Generally, scores fall into these categories:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

If your score falls into the "fair" or "poor" categories, lenders typically consider you a higher risk. This doesn’t mean you’re uncreditworthy; it simply means your financial history might show some late payments, high credit utilization, or past defaults.

Why Lenders Are Hesitant with Poor Credit

Lenders operate on risk assessment. When you have a lower credit score, it signals a higher probability of defaulting on a loan. To compensate for this increased risk, lenders often:

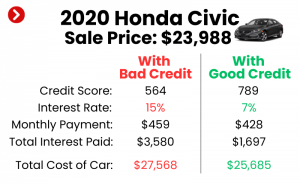

- Charge Higher Interest Rates: This is the most common consequence. A higher Annual Percentage Rate (APR) means you’ll pay significantly more over the life of the loan.

- Require Larger Down Payments: A substantial down payment reduces the loan amount and shows your commitment, thereby lowering the lender’s risk.

- Offer Shorter Loan Terms: While a shorter term means higher monthly payments, it reduces the overall interest paid and the lender’s exposure to risk.

- Impose Stricter Qualification Criteria: You might need to provide more documentation or meet specific income requirements.

It’s important to manage your expectations. While securing a car loan with poor credit is achievable, it’s unlikely you’ll qualify for the lowest interest rates or the most flexible terms. Your goal should be to find the best possible terms given your current credit situation.

The Good News: Yes, You Can Secure a Car Loan with Poor Credit

Let’s reiterate: the answer to "Can you get a car loan with poor credit?" is a resounding yes. Many lenders specialize in what are known as "subprime auto loans" – loans designed for borrowers with less-than-perfect credit. These lenders understand that life happens and that a past financial stumble doesn’t define your future ability to pay.

The key is to approach the process strategically. You need to present yourself as the most reliable borrower possible, even with your credit challenges. This involves proactive steps to mitigate risk in the eyes of potential lenders.

Key Strategies to Improve Your Chances of Car Loan Approval

Securing a car loan with poor credit isn’t about magic; it’s about smart preparation and demonstrating your readiness. Here are the most effective strategies based on my experience.

1. Improve Your Credit Score (Even a Little Helps!)

While a complete credit overhaul takes time, even small improvements can make a difference in your loan terms. A few points can sometimes move you into a better credit tier.

- Pay Bills On Time: This is the single most impactful action. Lenders want to see a consistent history of timely payments. Start immediately with all your current obligations.

- Reduce Existing Debt: High credit utilization (using a large percentage of your available credit) negatively impacts your score. Pay down credit card balances if possible.

- Check Your Credit Report for Errors: Mistakes on your credit report are surprisingly common. Get free copies of your report from AnnualCreditReport.com and dispute any inaccuracies. Correcting errors can boost your score quickly.

- Avoid New Credit Applications: Each new credit application can temporarily ding your score. Focus on improving your existing credit.

Pro tips from us: Before even thinking about a car loan, dedicate a month or two to optimizing your credit score. Even a 20-point jump can lead to better loan offers. (Hypothetical Internal Link)

2. Save for a Substantial Down Payment

A larger down payment is arguably one of the most powerful tools you have when seeking a car loan with poor credit. It benefits you and the lender in several ways:

- Reduces Loan Amount: Less money borrowed means smaller monthly payments and less interest over the loan’s life.

- Lowers Lender Risk: A significant upfront payment reduces the lender’s exposure. They see you as more invested and less likely to default.

- Builds Equity Faster: You start with more equity in the vehicle, reducing the risk of being "upside down" (owing more than the car is worth).

Based on my experience: Aim for at least 10% of the car’s value, but 20% or more is ideal. If you can put down a quarter of the purchase price, you’ll significantly increase your approval chances and potentially secure a lower interest rate.

3. Consider a Co-signer

A co-signer with excellent credit can be a game-changer. They essentially vouch for you, lending their creditworthiness to your application.

- Benefits: A co-signer can help you qualify for a loan you otherwise couldn’t get and may secure a lower interest rate.

- Risks: This is a serious commitment. If you miss payments, it negatively impacts their credit score, and they become legally responsible for the debt. This can strain relationships if not handled carefully.

- Who Makes a Good Co-signer: Someone with a strong credit history, stable income, and who fully understands the responsibility they are undertaking.

Common mistakes to avoid are: Co-signing with someone who isn’t financially stable themselves or not having a clear, written agreement with your co-signer about payment responsibilities.

4. Shop for the Right Vehicle

When your credit is poor, buying the most expensive, brand-new car on the lot is usually not a wise decision. Focus on affordability and reliability.

- Stay Within Your Budget: Determine what monthly payment you can truly afford, considering insurance, fuel, and maintenance. Don’t let a salesperson push you into a vehicle beyond your means.

- Consider Used Cars: Used vehicles are generally less expensive, which means you’ll need to borrow less money. This reduces your overall financial burden and the risk to the lender.

- Reliability is Key: Opt for a reliable used car that won’t rack up expensive repair bills, further straining your budget. Research models known for their longevity.

Pro tips from us: A well-maintained used car can be a fantastic investment, especially when you’re trying to build or rebuild your credit.

5. Gather Necessary Documentation

Being prepared makes you look responsible and streamlines the application process. Have all your financial documents ready before you even step foot in a dealership or apply online.

- Proof of Income: Pay stubs (recent 2-3 months), tax returns (if self-employed), bank statements.

- Proof of Residence: Utility bills, lease agreement, mortgage statements.

- Proof of Identity: Driver’s license, passport.

- References: Sometimes requested by subprime lenders.

The more transparent and organized you are, the smoother the process will be.

Where to Look: Lenders Who Specialize in Bad Credit Car Loans

Not all lenders are created equal, especially when it comes to poor credit. Knowing where to look can save you time and frustration.

1. Dealership Financing (Buy Here, Pay Here)

"Buy Here, Pay Here" (BHPH) dealerships are often a last resort for individuals with very poor credit or no credit history. They finance loans directly from the dealership, often without traditional bank involvement.

- Pros: High approval rates, even with significant credit challenges. Convenient, as you get the loan and car in one place.

- Cons: Extremely high interest rates (often the maximum allowed by law). Limited vehicle selection, typically older, higher-mileage cars. Payments might not be reported to credit bureaus, meaning it won’t help build your credit.

- Common mistakes to avoid are: Not scrutinizing the contract carefully, accepting incredibly high rates, and not confirming if payments are reported to credit bureaus.

2. Subprime Lenders (Specialized Banks and Finance Companies)

Many traditional banks and credit unions have dedicated subprime lending divisions or work with finance companies that specialize in bad credit car loans.

- Pros: Generally offer better terms than BHPH lots. They typically report payments to credit bureaus, helping you rebuild credit. You’ll often have a wider selection of vehicles.

- Cons: Interest rates are still significantly higher than for prime borrowers. Qualification criteria, while more lenient than prime loans, are stricter than BHPH.

You can often find these lenders through a dealership’s finance department, or by searching online for "bad credit auto loans" from reputable financial institutions.

3. Online Lenders

A growing number of online platforms specialize in connecting borrowers with poor credit to various lenders.

- Pros: Convenience (apply from home), quick pre-approval process, ability to compare multiple offers without visiting multiple dealerships. Many report to credit bureaus.

- Cons: It’s crucial to research the legitimacy of online lenders to avoid scams. Ensure they are reputable and secure.

- Pro tips from us: Use comparison sites that don’t impact your credit score with multiple hard inquiries until you’re ready to commit.

4. Credit Unions

Credit unions are member-owned financial institutions known for their customer-focused approach and often more flexible lending criteria.

- Pros: May offer more competitive rates and terms than traditional banks, even for those with poor credit, because they are not-for-profit. They are often willing to look beyond just your credit score.

- Cons: You usually need to become a member to qualify for a loan. Membership criteria can vary.

Based on my experience: If you’re already a member of a credit union, or eligible to join one, it’s always worth checking with them first. They might offer a more personal approach to your situation.

Understanding Your Loan Terms and Protecting Yourself

Once you start receiving offers, it’s easy to get excited. However, this is where careful scrutiny is paramount. Understanding the terms of your car loan with poor credit is crucial to avoid financial pitfalls.

1. Interest Rates (APR)

This is the most critical factor when you have poor credit. Your Annual Percentage Rate (APR) includes the interest rate plus any other fees charged by the lender.

- Expect Higher Rates: With poor credit, an APR in the high teens or even 20s is not uncommon. While this is high, it’s often the cost of getting approved.

- Compare Offers: Don’t accept the first offer. Shop around and compare APRs from multiple lenders. Even a percentage point or two difference can save you hundreds, if not thousands, over the life of the loan.

Pro tips from us: Focus on the total cost of the loan, not just the monthly payment. A lower monthly payment over a longer term often means paying much more in interest. (Hypothetical Internal Link)

2. Loan Term

The loan term is the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months).

- Shorter Terms: Higher monthly payments, but significantly less interest paid overall. This is often preferable if you can afford it.

- Longer Terms: Lower monthly payments, but you’ll pay much more in interest over time. You also risk being "upside down" on your loan for a longer period.

Based on my experience: While longer terms can make a car loan with poor credit seem more affordable monthly, they are a common trap. Always prioritize the shortest term you can comfortably manage.

3. Hidden Fees and Clauses

Always read the fine print of any loan agreement. Lenders sometimes include fees or clauses that can add to your costs.

- Prepayment Penalties: Some loans charge a fee if you pay off your loan early. This is less common now but still exists.

- Add-ons: Dealerships might try to sell you extended warranties, GAP insurance, or other add-ons. While some can be useful, ensure they are necessary and not overpriced. You can often purchase these separately and sometimes cheaper.

4. Read the Fine Print and Don’t Rush

Never feel pressured to sign anything on the spot. Take the contract home, review it carefully, and ask questions about anything you don’t understand. If possible, have a trusted advisor review it with you.

The Application Process with Poor Credit: What to Expect

The application process for a car loan with poor credit might feel a bit more rigorous, but being prepared will make it smoother.

- Get Pre-Approved: This is a crucial first step. Pre-approval lets you know how much you can borrow and at what interest rate before you even set foot in a dealership. This empowers you to negotiate confidently. Many online lenders and credit unions offer quick pre-approval with a soft credit inquiry, which doesn’t harm your score.

- Gather Documents: As mentioned, have all your income, residence, and identification documents ready.

- Be Transparent: Don’t try to hide your credit issues. Be honest about your financial situation. Lenders appreciate transparency.

- Negotiate: With a pre-approval in hand, you can negotiate the car’s price separately from the financing. This is a powerful position to be in.

- Close the Deal: Once you agree on the car and the loan terms, you’ll sign the paperwork. Ensure everything matches your understanding.

Pro tips from us: Use an auto loan calculator to understand how different interest rates and loan terms affect your monthly payments and total cost. This helps you visualize affordability.

Building Credit Through Your Car Loan

Here’s an exciting prospect: a car loan, even one with poor credit, can be a powerful tool for rebuilding your financial reputation.

- On-Time Payments: Every single on-time payment you make gets reported to the major credit bureaus. This demonstrates your reliability and consistently improves your payment history, which is the biggest factor in your credit score.

- Credit Mix: A car loan adds a new type of credit (installment loan) to your credit report, diversifying your credit mix. This can also positively influence your score over time.

- Path to Refinancing: After 12-18 months of consistent, on-time payments, your credit score will likely improve. At that point, you might be eligible to refinance your car loan at a much lower interest rate, saving you a significant amount of money. This is often the "light at the end of the tunnel" for bad credit car loans.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Navigating the world of car loans with poor credit is tricky. Here are some common pitfalls to sidestep:

- Not Checking Your Credit Report: Going into the process blind is a huge mistake. Know your score and review your report for errors.

- Accepting the First Offer: It’s tempting to grab the first "yes," but comparison shopping is crucial. Always get multiple quotes.

- Buying More Car Than You Can Afford: This is the most common mistake. Don’t let a low monthly payment over a long term trick you into buying an expensive car. Factor in insurance, maintenance, and fuel.

- Ignoring the Total Cost of the Loan: Focus on the overall interest paid and the total amount you’ll repay, not just the monthly payment.

- Falling for "Guaranteed Approval" Scams: Be wary of lenders promising "guaranteed approval" regardless of your credit. These often come with predatory terms, hidden fees, or are outright scams. Reputable lenders will always assess your ability to pay.

- Not Considering All Your Options: Don’t limit yourself to just one type of lender or car. Explore all avenues.

Alternatives to a Traditional Car Loan

Sometimes, a traditional car loan, even a subprime one, might not be the best fit for your current financial situation. It’s important to consider all options.

- Save Up and Buy Cash: If your need for a car isn’t immediate, saving up to buy a cheap, reliable used car with cash eliminates interest payments entirely and avoids taking on more debt. This is often the smartest long-term play.

- Public Transportation/Ride-sharing: For some, especially in urban areas, relying on public transport, ride-sharing services, or even cycling can be a cost-effective alternative to car ownership.

- Borrow from Family or Friends: If you have a trusted network, borrowing money from family or friends, with clear, written terms for repayment, can be an interest-free or low-interest option. Treat it as a formal loan to protect relationships.

- Leasing (with Caution): While leasing typically requires good credit, some dealerships offer leases to individuals with fair credit. However, leasing often means you’re just renting the car, not building equity, and there can be significant fees for mileage overages or damage. It’s rarely recommended if your goal is to own a car or improve credit.

Based on my experience: While these alternatives might not be ideal for everyone, it’s always worth evaluating if they offer a less financially strenuous path than a high-interest car loan.

Conclusion: Your Roadmap to Driving Away with Confidence

The journey to securing a car loan with poor credit is undeniably challenging, but as we’ve explored, it’s a journey many successfully complete. The key is to be informed, strategic, and patient.

Remember, getting a car loan with poor credit isn’t just about obtaining transportation; it’s an opportunity to rebuild your financial standing. By making consistent, on-time payments, you’ll not only enjoy the freedom of owning a vehicle but also steadily improve your credit score, opening doors to better financial opportunities in the future.

Start by checking your credit, saving for a down payment, exploring all your lending options, and understanding every aspect of your loan terms. Don’t be afraid to ask questions, negotiate, and walk away if a deal doesn’t feel right. With careful planning and a responsible approach, you can absolutely drive away confidently, leaving your poor credit worries in the rearview mirror. Your journey to car ownership and improved financial health starts now.