Can You Get A Car Loan Without A Driver’s License? Your Ultimate Guide

Can You Get A Car Loan Without A Driver’s License? Your Ultimate Guide Carloan.Guidemechanic.com

The open road, the freedom of movement, the convenience of owning your own vehicle – these are aspirations many of us share. But what if you don’t possess a driver’s license? The question "Can you get a car loan without a license?" is a common one, often leading to confusion and doubt. Many people mistakenly believe that a driver’s license is a non-negotiable requirement for securing vehicle financing.

Let me tell you straight away: the answer is a resounding yes, it is absolutely possible to get a car loan without a driver’s license. While it presents a unique set of challenges and requires a strategic approach, it’s far from an impossible feat. As an expert in car financing, I’ve guided countless individuals through this very process. This comprehensive guide will debunk myths, illuminate the path, and provide you with all the essential information to navigate securing a car loan, even without a driver’s license.

Can You Get A Car Loan Without A Driver’s License? Your Ultimate Guide

The Core Question: Can You Get a Car Loan Without a Driver’s License? (YES!)

It’s a prevalent misconception that a driver’s license is a mandatory document for car loan approval. The underlying reason for this belief often stems from the logical connection between owning a car and driving it. However, from a lender’s perspective, the primary concern isn’t whether you’ll be the one behind the wheel, but rather your ability and willingness to repay the loan.

Lenders are in the business of assessing financial risk. When you apply for a car loan, they are primarily evaluating your creditworthiness, your income stability, and your overall financial responsibility. Your driver’s license proves your legal ability to operate a vehicle, but it doesn’t directly speak to your capacity to honor a financial agreement.

Based on my experience working with numerous clients seeking financing, the absence of a driver’s license is rarely a deal-breaker on its own. It simply means you’ll need to satisfy other identity verification and financial criteria more rigorously. The key is understanding what lenders actually need from you and how you can provide it.

Why Lenders Ask for Identification (And Why It Doesn’t Have to Be a Driver’s License)

Every financial transaction, especially one involving a significant loan, requires robust identity verification. This isn’t just a lender’s preference; it’s often a legal mandate. Regulations like the Patriot Act require financial institutions to "know your customer" (KYC) to prevent fraud, money laundering, and terrorist financing.

When a lender asks for identification, they are looking to confirm that you are who you say you are. They need to ensure that the person applying for the loan is a real individual, legally capable of entering into a contract, and that they can be reliably contacted. A driver’s license is merely one of many acceptable forms of government-issued identification that fulfills these requirements.

Pro tips from us: The focus should always be on providing clear, verifiable proof of identity, regardless of whether it’s a driving permit or another official document. Don’t assume a license is the only way; instead, prepare to present equally valid alternatives.

Alternative Forms of Identification for a Car Loan

While a driver’s license is convenient, it’s certainly not the only path to proving your identity. Many other government-issued documents are widely accepted by lenders. Understanding these alternatives is crucial for anyone looking to get a car loan without a license.

1. State-Issued Identification Card (Non-Driver ID)

This is often the most straightforward and universally accepted alternative to a driver’s license within the United States. A state ID card is issued by your state’s Department of Motor Vehicles (DMV) or equivalent agency and serves solely as proof of identity and residency, without granting driving privileges. It contains the same vital information as a driver’s license – your photo, name, address, and date of birth – making it an ideal substitute for lenders.

Applying for a state ID is typically a simple process, requiring proof of identity (e.g., birth certificate, Social Security card), proof of residency, and sometimes proof of signature. This document is recognized by virtually all financial institutions and serves as strong evidence of your legal identity.

2. Valid U.S. Passport or Passport Card

A U.S. Passport is an internationally recognized form of identification and is highly respected by lenders. It verifies your identity and citizenship, making it an excellent alternative to a driver’s license. The passport card, a smaller, wallet-sized version, also serves this purpose, though it’s primarily for land and sea travel to specific areas.

Lenders appreciate the security features and rigorous application process associated with passports, making them a very reliable form of ID. If you have a current passport, it should be at the top of your list of documents to present.

3. U.S. Military Identification Card

For active-duty service members, veterans, or their dependents, a valid U.S. Military ID card is a strong form of identification. These cards are issued by the Department of Defense and are widely accepted for various official purposes, including financial transactions. They contain clear photographic identification and personal data, making them suitable for loan applications.

The credibility of military ID cards makes them an unquestionable choice for lenders seeking to verify an applicant’s identity. They represent a high level of government-issued authentication.

4. Consular Identification Card (Matrícula Consular)

For non-U.S. citizens residing in the country, a consular ID card, such as a Matrícula Consular issued by a foreign consulate, can sometimes be accepted. Acceptance varies more widely among lenders for these documents compared to state IDs or passports. However, some financial institutions, particularly those with diverse customer bases or located in areas with large immigrant populations, are more accustomed to processing loans with these forms of identification.

It’s crucial to confirm with your chosen lender if they accept such identification. You might need to provide additional supporting documents to strengthen your application if this is your primary form of ID.

5. Foreign Government-Issued ID with Additional Verification

Similar to consular IDs, a passport or national ID card issued by a foreign government can sometimes be used. However, this often requires additional layers of verification, such as proof of legal residency in the U.S. (e.g., a green card, visa, or employment authorization document). Lenders will want to ensure you have the legal right to reside and work in the country and are capable of entering into a binding contract under U.S. law.

Always be prepared to offer supplementary documents if you are using a foreign-issued ID. Transparency and a willingness to provide extra verification can significantly help your case.

What Lenders Really Look For (Beyond the License)

Once identity is established, lenders shift their focus to your financial profile. This is where the core of your loan application will be evaluated. Understanding these critical factors will empower you to present a stronger case for a car loan without a driver’s license.

1. Creditworthiness: Your Credit Score and History

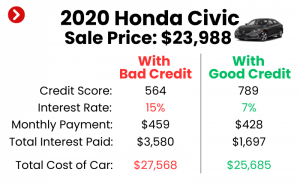

Your credit score is essentially a financial report card. It’s a three-digit number that summarizes your credit history and predicts your likelihood of repaying debt. Lenders use it as a primary indicator of your financial responsibility. A strong credit score (generally 670 and above) signals to lenders that you are a reliable borrower.

Your credit history, which includes details about past loans, credit cards, and payment patterns, is equally important. Lenders want to see a consistent history of on-time payments and responsible credit management. Even without a driver’s license, excellent credit can open many doors. Conversely, a poor credit history can make securing a loan more challenging, regardless of your ID.

2. Income and Employment Stability

Lenders need assurance that you have a steady and sufficient income to cover your monthly car loan payments. They will typically ask for proof of employment and income, such as recent pay stubs, W-2 forms, tax returns, or bank statements. The longer and more stable your employment history, the better.

Demonstrating a consistent income stream minimizes the lender’s risk. They want to see that you have a reliable source of funds to meet your financial obligations. Irregular or unverified income can be a red flag, making it harder to get approved.

3. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your capacity to take on additional debt. A lower DTI ratio indicates that you have more disposable income available to make car loan payments, making you a less risky borrower.

Typically, lenders prefer a DTI ratio below 36%, though some may go higher depending on other factors. If your existing debts (mortgage, student loans, credit cards) consume a large portion of your income, adding a car loan might stretch your finances too thin in the eyes of a lender.

4. Down Payment

Making a substantial down payment can significantly increase your chances of approval, especially when you’re seeking a car loan without a license. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment to the purchase and indicates financial discipline.

Pro tips from us: Aim for at least 10-20% of the car’s purchase price as a down payment. This demonstrates financial commitment and reduces the loan-to-value (LTV) ratio, which is favorable to lenders.

5. Collateral (The Car Itself)

The car you’re buying serves as collateral for the loan. If you default on payments, the lender has the right to repossess the vehicle to recover their losses. Lenders will assess the car’s value, age, and condition to ensure it’s adequate collateral for the loan amount. They typically don’t want to lend more than the car is worth.

Common mistakes to avoid are choosing a vehicle that is significantly older or has very high mileage, as these cars can be seen as higher risk due to potential maintenance issues and faster depreciation, making them less desirable collateral.

Strategies to Secure a Car Loan Without a License

Knowing what lenders look for is the first step; the next is implementing strategies to meet their requirements. Here are several effective approaches to help you get a car loan without a driver’s license.

1. Get a State ID Card

As mentioned, obtaining a state-issued identification card is often the simplest and most effective way to address the ID requirement. This document is specifically designed for non-drivers and is accepted by virtually all financial institutions. It eliminates any ambiguity about your identity.

Make this your priority if you don’t have a passport or military ID. It streamlines the application process significantly.

2. Use a Co-signer with Good Credit

If your credit history is limited or your income isn’t as robust as lenders prefer, applying with a co-signer can dramatically improve your chances of approval. A co-signer is someone with good credit and a stable income who agrees to be equally responsible for the loan. If you default, the lender can pursue the co-signer for payment.

The co-signer’s credit profile acts as a safety net for the lender, reducing their risk. This strategy is particularly effective for first-time borrowers or those with a less-than-perfect credit score. Ensure your co-signer understands their full legal responsibility.

3. Work with Dealership Financing

Many car dealerships offer in-house financing or have established relationships with multiple lenders. These finance departments often have more flexibility and experience working with diverse applicant profiles, including those without a driver’s license. They might be more willing to find a solution, especially if you have strong income or a good down payment.

Dealerships are motivated to sell cars, so they often go the extra mile to facilitate financing. They can act as intermediaries, presenting your case to various lenders who might have specific programs for unique situations.

4. Explore Credit Unions and Smaller Banks

Credit unions are non-profit organizations owned by their members. They are often more community-focused and may offer more personalized service and flexible lending criteria compared to large commercial banks. If you’re a member of a credit union, or eligible to join one, it’s worth exploring their loan options.

Smaller local banks might also be more willing to consider individual circumstances rather than strictly adhering to rigid rules. They might take a more holistic view of your financial situation.

5. Secure the Loan with a Larger Down Payment

As discussed, a significant down payment reduces the loan amount and, consequently, the lender’s risk. This strategy becomes even more powerful when you’re missing a driver’s license. It shows the lender that you are financially stable, serious about the purchase, and have less to borrow, making the loan less risky for them.

Our professional advice is to save as much as possible for a down payment. It can be a game-changer for your application.

6. Build or Repair Your Credit First

If you’re not in a hurry, taking time to build or improve your credit score can make the entire process smoother. A strong credit history demonstrates reliability and will make lenders much more comfortable approving your application, even without a driver’s license.

Consider opening a secured credit card, becoming an authorized user on someone else’s credit card, or taking out a small credit-builder loan. Consistently making on-time payments for a few months can significantly boost your score.

The "Catch" – Car Insurance Without a License

While getting a car loan without a license is feasible, owning a car comes with another critical requirement: insurance. This is often the biggest hurdle after securing the loan. Lenders will typically require proof of full coverage insurance before finalizing the loan, as the car is their collateral.

Can you insure a car if you don’t have a driver’s license? Yes, but with a nuance. You can purchase an insurance policy as the "named insured" or "owner" of the vehicle. However, insurance companies primarily underwrite policies based on who will be the "primary driver" of the vehicle. If you don’t have a license, you cannot be listed as the primary driver.

This means you will need to list a licensed driver on your policy who will be the primary operator of the vehicle. This could be a spouse, a family member, or a close friend who lives with you and will regularly drive the car. The insurance premium will be based on their driving record, age, and other factors. Without a licensed driver on the policy, it will be extremely difficult, if not impossible, to obtain coverage, as there would be no one legally able to operate the insured vehicle.

Step-by-Step Guide to Applying for a Car Loan Without a Driver’s License

To maximize your chances of success, follow this structured approach when applying for a car loan:

1. Gather All Necessary Documents

Preparation is key. Compile a comprehensive portfolio of documents, including:

- Your chosen alternative ID (State ID, Passport, Military ID).

- Proof of income (recent pay stubs, W-2s, tax returns, bank statements).

- Proof of residency (utility bills, lease agreement).

- Bank account statements.

- Any co-signer’s information (if applicable).

Having everything organized will demonstrate your seriousness and readiness to the lender.

2. Check Your Credit Score

Before approaching lenders, get a free copy of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) and check your credit score. This allows you to identify any errors and understand your financial standing from a lender’s perspective. Knowing your score helps you set realistic expectations and address any issues beforehand.

3. Save for a Down Payment

As emphasized, a substantial down payment can be your strongest asset when applying for a car loan without a license. Start saving early and aim for at least 10-20% of the vehicle’s cost. This not only reduces the loan amount but also signals financial responsibility.

4. Research Lenders

Don’t just walk into the first dealership you see. Research lenders who are known for flexibility or have experience with unique financial situations. This includes credit unions, smaller local banks, and dealerships that offer in-house financing. Call ahead and explain your situation before making a formal application.

5. Explain Your Situation Clearly

When you speak with lenders, be upfront and transparent about not having a driver’s license. Explain why you need the car (e.g., for a licensed family member to drive, for business use where a licensed employee drives it, etc.) and clearly present your alternative forms of identification and strong financial standing. Honesty builds trust.

6. Prepare for Insurance Questions

Lenders will invariably ask about insurance. Be ready to explain how you plan to insure the vehicle, specifically mentioning the licensed driver who will be listed on the policy as the primary operator. Having a quote or even a preliminary policy in place can further reassure the lender.

Common Misconceptions & Clarifications

Let’s address a few more common myths that can hinder your progress:

- "I need a license to register the car." This is generally false. Vehicle registration primarily requires proof of ownership, proof of insurance, and payment of fees. Your state ID or other acceptable identification is typically sufficient to register a car in your name. The registered owner doesn’t always have to be the licensed driver.

- "Lenders won’t trust me because I don’t drive." Lenders trust financial stability and repayment capacity. If you demonstrate strong credit, stable income, and a solid alternative ID, your lack of a driver’s license becomes a secondary concern. Their primary goal is to ensure the loan is repaid.

- "It’s illegal to get a car loan without a license." Absolutely not. There is no law preventing you from obtaining a loan for a vehicle if you don’t possess a driver’s license. The legal requirement pertains to operating the vehicle, not owning or financing it.

Conclusion: Your Road to Car Ownership is Open

The journey to securing a car loan without a driver’s license might seem daunting at first, but as we’ve explored, it is entirely achievable with the right knowledge and preparation. The key lies in understanding that lenders prioritize your financial stability, your ability to repay the loan, and verifiable proof of identity over your driving credentials.

By focusing on providing strong alternative identification, demonstrating a healthy credit profile, showcasing stable income, and potentially utilizing a co-signer or making a significant down payment, you can significantly enhance your chances of approval. Remember to plan for the insurance aspect by having a licensed driver available to be listed on your policy.

Don’t let the absence of a driver’s license deter you from your goal of car ownership. With strategic planning and a clear understanding of the process, you can navigate the financing landscape successfully. The road to getting a car loan without a license is open – all you need to do is prepare and drive forward with confidence!

Share your experiences or questions in the comments below. Have you successfully secured a car loan without a license? What strategies worked for you?