Can You Get a Car Loan Without a Job? Your Ultimate Guide to Navigating the Challenge

Can You Get a Car Loan Without a Job? Your Ultimate Guide to Navigating the Challenge Carloan.Guidemechanic.com

Securing a car loan is a significant financial step for many, opening doors to greater independence and opportunity. However, the prospect of getting approved for a loan when you don’t have a traditional job often feels like an insurmountable hurdle. The question, "Can you get a car loan without a job?" is one we hear frequently, and it’s a valid concern for anyone navigating today’s dynamic job market or relying on alternative income streams.

While it’s undeniably more challenging, the answer isn’t a simple "no." It’s more nuanced than that. This comprehensive guide will delve deep into the realities of obtaining a car loan without conventional employment, offering expert insights, practical strategies, and crucial advice to maximize your chances of approval. We’ll explore how lenders assess risk, what alternative income sources they consider, and the proactive steps you can take to present yourself as a reliable borrower.

Can You Get a Car Loan Without a Job? Your Ultimate Guide to Navigating the Challenge

Understanding the Lender’s Perspective: Why a Job Matters

Before we dive into solutions, it’s vital to understand the lender’s point of view. When you apply for a car loan, lenders are primarily concerned with one thing: your ability to repay the debt. A stable, verifiable job is traditionally the clearest indicator of consistent income, which directly translates to repayment capacity.

Lenders use various criteria, often referred to as the "5 Cs of Credit": Character, Capacity, Capital, Collateral, and Conditions. Your employment status directly impacts "Capacity" – your ability to make payments – and "Character" – your willingness to pay, often reflected in your credit history. Without a job, their primary assurance of regular income is missing, significantly increasing their perceived risk.

Based on my experience in the financial sector, lenders are inherently risk-averse. Their business model relies on borrowers making timely payments. When that primary income source is absent, they need compelling evidence from other areas of your financial life to mitigate that risk. This doesn’t mean it’s impossible; it just means you need to work harder to build a strong case.

Defining "No Job": More Nuance Than You Think

The term "without a job" can mean many different things, and how a lender views your situation depends heavily on what your specific circumstances are. It’s crucial to differentiate these scenarios because each presents a unique set of challenges and opportunities.

Simply saying "I don’t have a job" isn’t enough; you need to articulate your actual financial standing. Lenders aren’t just looking for a W-2; they’re looking for proof of sustainable income, regardless of its source. Understanding this distinction is your first step towards building a successful loan application.

Truly Unemployed (No Income)

If you have absolutely no income coming in, obtaining a car loan is exceedingly difficult, if not impossible. Lenders require some form of verifiable income to approve a loan. In this scenario, your best bet might be to focus on securing employment or an alternative income source before applying.

Self-Employed or Freelancer

Many individuals today work for themselves, without a traditional employer. While you don’t receive a regular paycheck, you definitely have income. The challenge here is proving the consistency and stability of that income. Lenders will typically require several years of tax returns (often two to three) and bank statements to verify your earnings.

Retired

Retirees often have stable, predictable income from pensions, Social Security, 401(k) distributions, or other investment vehicles. Lenders generally view these as reliable income sources, making it very possible to secure a car loan. The key is to provide clear documentation of these benefits.

Receiving Disability Benefits

Individuals receiving Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) have a consistent income stream. Lenders often consider these benefits as legitimate and stable sources of income for loan qualification. You’ll need official statements from the Social Security Administration.

Students

Many students don’t have full-time jobs, but some might have part-time employment, student loan disbursements, or financial support from parents. Lenders will assess these income sources, but a co-signer is often a strong recommendation for students due to potentially limited income and credit history.

Relying on Other Income Sources

This category encompasses a wide range of situations, from individuals receiving alimony or child support to those living off investment dividends or rental property income. Each of these can be valid income for a loan, provided you can offer robust documentation.

Alternative Income Sources Lenders Will Consider

The good news is that traditional employment isn’t the only path to proving income. Lenders are becoming more flexible in what they recognize as verifiable income, especially with the rise of the gig economy and diverse financial landscapes. The key is proving that these sources are stable, recurring, and sufficient to cover your loan payments.

Here are some alternative income streams that lenders commonly accept:

1. Social Security Benefits (Retirement or Disability)

If you’re retired and receiving Social Security, or if you’re on SSDI or SSI, these benefits are considered very stable income. Lenders will typically accept your official award letters and bank statements showing direct deposits as proof of income. This is often one of the strongest alternative income types.

2. Pension and Retirement Account Distributions

For retirees, pensions are a clear, consistent income source. Similarly, regular distributions from 401(k)s, IRAs, or other retirement accounts can be used to qualify. You’ll need statements or letters detailing the frequency and amount of these payments.

3. Alimony or Child Support Payments

These court-ordered payments can be considered income, but lenders often have stricter requirements. They typically want to see a consistent history of payments (e.g., 6-12 months of bank statements), and the payments must be legally enforceable and likely to continue for the duration of the loan.

4. Rental Property Income

If you own rental properties, the income you receive from tenants can be counted. Lenders will usually require copies of lease agreements and bank statements showing consistent rent deposits, along with your tax returns detailing your rental income and expenses.

5. Investment Income (Dividends, Interest)

Regular dividends from stocks, bonds, or mutual funds, or interest income from savings accounts or CDs, can be used. This usually requires a substantial portfolio to generate enough income to cover loan payments, and lenders will want to see consistent historical payouts.

6. Annuity Payments

Structured settlements or annuities that provide regular, guaranteed payments are excellent forms of verifiable income. You’ll need documentation from the issuing company detailing the payment schedule and amounts.

7. Unemployment Benefits (with caveats)

While unemployment benefits provide income, they are generally viewed as temporary. Some lenders might consider them if you have a very short-term loan, a strong credit score, and other mitigating factors, but it’s much harder to qualify solely on this. It’s often best to secure a new job first.

8. Self-Employment Income

For freelancers, independent contractors, or small business owners, your income is your business’s revenue minus expenses. Lenders typically require two to three years of tax returns (Schedule C for sole proprietors) and bank statements to demonstrate consistent, profitable income. Proving stability here is crucial.

Pro tips from us: Always gather as much documentation as possible for any alternative income source. The more verifiable and consistent you can prove your income to be, the stronger your application will be. Lenders need confidence that your income stream won’t suddenly dry up.

Strategies to Improve Your Chances (Even Without a Traditional Job)

Even with alternative income, the absence of a traditional W-2 job means you need to bolster other aspects of your application. Here are several powerful strategies to enhance your appeal to lenders.

1. Cultivate an Excellent Credit Score

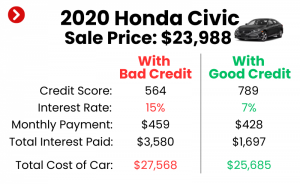

Your credit score is paramount. A high credit score (generally 700+) signals to lenders that you have a history of managing debt responsibly and making payments on time. It acts as a powerful counterbalance to the lack of a traditional job.

Common mistakes to avoid are not checking your credit score before applying or having errors on your credit report. Get a copy of your credit report from one of the major bureaus (Experian, Equifax, TransUnion) and dispute any inaccuracies. A strong score can significantly improve your chances and lead to better interest rates. (For more details, you might want to read our article on Improving Your Credit Score: A Comprehensive Guide – simulated internal link).

2. Make a Substantial Down Payment

Putting down a significant portion of the car’s price upfront drastically reduces the lender’s risk. The less money they have to lend you, the less risk they assume. A down payment of 20% or more can make your application much more attractive, even without a traditional job.

It shows financial stability and serious commitment to the purchase. Moreover, a larger down payment means you’ll finance less, resulting in lower monthly payments, which further eases the burden on your non-traditional income.

3. Find a Creditworthy Co-signer

A co-signer is someone who agrees to be equally responsible for the loan if you default. If your co-signer has a strong credit score and a stable income (preferably a traditional job), their financial standing can significantly strengthen your application.

However, understand the implications: the loan will appear on their credit report, and any missed payments will negatively affect both of your credit scores. Choose a co-signer (like a trusted family member) who fully understands this responsibility.

4. Opt for a Lower-Priced Vehicle

Resist the urge to buy more car than you need or can realistically afford. A less expensive car means a smaller loan amount, which translates to lower monthly payments. This makes it easier to qualify and lessens the financial strain on your alternative income.

Lenders are more likely to approve a smaller, less risky loan. Demonstrating financial prudence by choosing an affordable vehicle can work in your favor.

5. Offer Additional Collateral (Secured Loan)

While car loans are typically secured by the car itself, some lenders might allow you to offer additional collateral, such as a savings account or another asset, to secure the loan. This is less common for car loans but can be an option for very specific situations or with certain lenders. This further reduces the lender’s risk.

6. Show Proof of Substantial Savings

Even if your income isn’t from a traditional job, having a healthy savings account or other liquid assets demonstrates financial prudence and a safety net. It reassures lenders that you have funds to fall back on if an unexpected expense arises, bolstering your ability to make payments.

Bank statements showing consistent savings can act as a powerful form of "capital" in the lender’s eyes.

7. Present a Job Offer Letter

If you’re currently unemployed but have recently received a firm job offer, some lenders might consider it. You’ll need an official offer letter detailing your start date, salary, and employment terms. While not all lenders accept this, it’s worth exploring, especially if your start date is imminent.

8. Explore Dealership Financing vs. Bank/Credit Union

Don’t limit yourself to just one type of lender. Dealerships often work with a variety of lenders, some of whom might have more flexible criteria for non-traditional income. Credit unions, known for their community focus, can sometimes be more willing to work with members on a case-by-case basis. Online lenders are also an option, as some specialize in a broader range of credit profiles.

Types of Lenders to Approach

Not all lenders are created equal, especially when you’re looking for a car loan without a traditional job. Knowing where to focus your efforts can save you time and increase your chances of approval.

1. Credit Unions

Credit unions are often more flexible and member-focused than traditional banks. They might be more willing to look beyond strict employment criteria and consider your overall financial picture and relationship with them. If you’re a member of a credit union, start there. They often offer competitive rates too.

2. Local Banks

If you have an existing relationship with a local bank – perhaps where you keep your savings or checking account – they might be more inclined to work with you. They have access to your financial history and might be more understanding of your specific circumstances. Personal relationships can sometimes make a difference.

3. Online Lenders

Many online lenders use sophisticated algorithms that might weigh different factors more heavily than traditional lenders. Some specialize in borrowers with non-traditional profiles or those with less-than-perfect credit. Do thorough research, read reviews, and compare terms carefully, as some might have higher interest rates.

4. "Buy Here, Pay Here" Dealerships

These dealerships offer in-house financing, meaning they are both the seller and the lender. They are often a last resort because they cater to individuals with poor credit or no proof of traditional income. While approval rates are high, they typically come with significantly higher interest rates, longer loan terms, and potentially unfavorable conditions. Proceed with extreme caution and ensure you understand every aspect of the agreement.

The Application Process: What to Expect and How to Prepare

Applying for a car loan without a traditional job requires thorough preparation and transparency. Lenders need to feel confident in your ability to repay, and your application package should reflect that.

1. Gather All Necessary Documentation

Before you even speak to a lender, have all your documents in order. This includes:

- Proof of Identity: Driver’s license, passport.

- Proof of Residency: Utility bills, lease agreement.

- Proof of Income (Alternative): Social Security award letters, pension statements, tax returns (for self-employed), bank statements showing consistent deposits from rental income, investments, alimony, etc.

- Bank Statements: Show consistent cash flow and savings.

- Credit Report: Be prepared to discuss anything on it.

- Down Payment Funds: Proof you have the funds readily available.

2. Be Honest and Transparent

Don’t try to hide your employment situation or exaggerate your income. Lenders will verify your information, and any discrepancies can lead to immediate denial or, worse, accusations of fraud. Be upfront about your lack of a traditional job and clearly explain your alternative income sources.

3. Be Prepared to Explain Your Situation

Lenders might ask questions about your financial stability, future plans, and why you need a car now. Have a clear, concise, and confident explanation ready. Demonstrate your understanding of your financial situation and your commitment to making payments.

4. Apply for Pre-Approval

Getting pre-approved from a few different lenders can give you leverage. It tells you exactly how much you can borrow and at what interest rate, allowing you to shop for a car with a clear budget. This also separates the financing process from the car-buying process, reducing pressure at the dealership.

Common Pitfalls and How to Avoid Them

Navigating car loans without a traditional job can be tricky. Being aware of potential pitfalls can help you avoid costly mistakes.

1. High-Interest Rates

Without a traditional job, especially if your credit isn’t stellar, you’re often considered a higher risk. This can translate into significantly higher interest rates, increasing your total cost of the loan.

- Avoidance: Work on improving your credit score, make a larger down payment, and compare offers from multiple lenders to find the best rate. A co-signer can also help secure a better rate.

2. Predatory Lenders

Some lenders specifically target high-risk borrowers with unfavorable terms, hidden fees, and exorbitant interest rates. These "predatory" loans can trap you in a cycle of debt.

- Avoidance: Research lenders thoroughly. If an offer seems too good to be true, or if a lender pressures you into signing immediately without reviewing terms, walk away. Always read the fine print and understand the total cost of the loan.

3. Taking on Too Much Debt

It’s easy to get excited about a car, but taking on a loan that stretches your budget too thin, especially with non-traditional income, can lead to financial stress and missed payments.

- Avoidance: Create a realistic budget that accounts for not just the car payment but also insurance, fuel, maintenance, and potential repairs. (Our article on Budgeting for Your First Car: What You Need to Know could be helpful here – simulated internal link). Be conservative in your estimates and aim for a payment you can comfortably afford, even if your income fluctuates slightly.

4. Not Reading the Fine Print

Loan agreements can be complex. Overlooking key clauses about penalties, late fees, or repossession terms can have severe consequences.

- Avoidance: Read every single line of the loan agreement before signing. Don’t hesitate to ask questions about anything you don’t understand. Consider having a trusted advisor review it with you if possible.

5. Damaging Co-signer Relationships

If you default on a loan with a co-signer, not only will your credit suffer, but so will theirs. This can strain or even destroy personal relationships.

- Avoidance: Only ask someone to co-sign if you are absolutely confident in your ability to repay. Maintain open communication with your co-signer and keep them informed of your payment status.

Is a Car Loan Without a Job Right for You? (Crucial Considerations)

Even if you can get a car loan without a traditional job, the question remains: should you? This is a critical self-assessment that requires honesty about your financial situation and needs.

1. Assess Your True Necessity vs. Desire

Do you absolutely need a car for work, medical appointments, or essential errands, or is it more of a want? If it’s a want, perhaps waiting until your financial situation is more stable is the wiser choice. Alternative transportation options might be a better short-term solution.

2. Long-Term Financial Stability

How stable and predictable are your alternative income sources in the long run? Will they continue for the entire loan term (typically 3-5 years)? If your income is prone to significant fluctuations, taking on a long-term debt might be risky.

3. Emergency Fund

Do you have an adequate emergency fund to cover several months of expenses, including your potential car payment, in case your income stream temporarily slows down or stops? This safety net is even more critical when you don’t have a traditional job.

4. The Total Cost of Ownership

Remember that a car loan payment is just one part of car ownership. Factor in insurance, fuel, maintenance, and potential repairs. These costs can quickly add up and impact your overall budget. A reliable external resource like the Consumer Financial Protection Bureau can offer valuable insights into car loan considerations.

Conclusion: Navigating the Road Ahead

Getting a car loan without a traditional job is a challenging endeavor, but as this guide illustrates, it’s certainly not an impossible one. It requires a strategic approach, meticulous preparation, and a deep understanding of what lenders look for. By presenting a strong case built on verifiable alternative income, an excellent credit score, a significant down payment, or the support of a creditworthy co-signer, you can significantly improve your chances of approval.

Based on my experience, the most successful applicants in this category are those who are proactive, transparent, and realistic about their financial capabilities. They don’t just hope for approval; they strategically build their application to address every potential concern a lender might have.

Remember to carefully weigh the pros and cons, consider the long-term implications, and prioritize your financial well-being above all else. With the right approach and a clear understanding of your options, you can navigate the path to car ownership, even without a traditional paycheck. Start planning today, gather your documents, and approach lenders with confidence and a well-prepared financial story.