Can You Get An 84 Month Car Loan? The Ultimate Guide to Extended Car Financing

Can You Get An 84 Month Car Loan? The Ultimate Guide to Extended Car Financing Carloan.Guidemechanic.com

In today’s dynamic automotive market, the dream of owning a new car often comes with a hefty price tag. As vehicle costs continue to climb, many prospective buyers find themselves searching for ways to make their desired vehicle more affordable. This is where the concept of an extended car loan, particularly an 84-month car loan, comes into play. But the burning question remains: can you get an 84-month car loan, and more importantly, is it a wise financial decision?

This comprehensive guide will dive deep into the world of extended car financing, exploring everything you need to know about 84-month car loans. We’ll unpack the advantages and disadvantages, reveal common pitfalls, and provide expert insights to help you make an informed choice. Our goal is to equip you with the knowledge to navigate this complex financial landscape, ensuring you drive away with clarity and confidence.

Can You Get An 84 Month Car Loan? The Ultimate Guide to Extended Car Financing

The Rise of the 84-Month Car Loan: What’s Driving the Trend?

The automotive industry has witnessed a significant shift towards longer loan terms over the past decade. What was once considered an unconventional financing option, an 84-month car loan (which translates to seven full years), is now increasingly common. Several factors contribute to this growing trend.

Firstly, rising vehicle prices are a primary driver. The average cost of both new and used cars has surged, making traditional 60-month or 72-month loans result in monthly payments that are simply out of reach for many consumers. Secondly, the desire for higher-end vehicles, equipped with advanced technology and luxury features, pushes buyers towards options that lower their immediate financial burden. An extended loan term achieves this by spreading the total cost over a longer period.

This shift isn’t just about affordability; it also reflects a change in consumer financial behavior. Many individuals prioritize lower monthly outlays to maintain their cash flow, even if it means paying more over the long haul. Lenders, in turn, have responded to this demand by making extended car financing more readily available, broadening the spectrum of potential car buyers.

Understanding the Mechanics: How an 84-Month Car Loan Works

At its core, an 84-month car loan functions much like any other installment loan. You borrow a principal amount to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined number of months. The key difference, of course, is the extended repayment period.

When you opt for an 84-month term, the total amount you borrow is divided into 84 equal monthly payments, with interest calculated and added to each installment. This longer duration directly impacts the size of your monthly payment, making it considerably lower than what you’d pay on a shorter loan for the same principal amount. While this appears attractive on the surface, it’s crucial to understand that the total interest paid over seven years will be significantly higher.

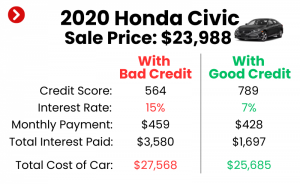

The interest rate applied to your loan is determined by several factors, including your credit score, the vehicle’s age, and market conditions. Even a slightly higher interest rate, when compounded over 84 months, can add thousands of dollars to the total cost of your car. This extended period of repayment fundamentally alters the financial dynamics of your vehicle purchase, making it essential to look beyond just the monthly payment figure.

The Allure: Advantages of an 84-Month Car Loan

It’s easy to see why 84-month car loans have become so popular. They offer several compelling advantages, particularly for buyers facing specific financial situations or those with particular vehicle aspirations. Understanding these benefits is the first step in deciding if this type of extended car financing aligns with your needs.

Lower Monthly Payments

The most significant and immediate benefit of an 84-month car loan is the reduced monthly payment. By stretching the repayment period over seven years, the principal and interest are spread out, resulting in a considerably smaller bill each month compared to a 60-month or even 72-month loan. This can be a game-changer for budget-conscious consumers.

Lower payments free up more of your disposable income each month. This extra cash flow can be used for other essential expenses, savings, investments, or simply to alleviate financial pressure. For many, this is the primary reason they consider long-term car loans, making their desired vehicle fit within a tight budget.

Access to More Expensive Vehicles

With lower monthly payments, an 84-month car loan can open the door to purchasing a more expensive vehicle than you might otherwise afford. If you have your heart set on a specific model, a luxury brand, or a car with advanced features, an extended loan term can make those dreams a reality without significantly increasing your immediate financial burden.

Based on my experience, many buyers use this strategy to upgrade their vehicle choice. Instead of settling for a base model on a shorter term, they can afford a higher trim level or even a different class of vehicle entirely. This allows them to enjoy a car that better meets their preferences and needs, enhancing their driving experience.

Budget Management and Flexibility

For some, the predictability of a lower, consistent monthly payment offers a sense of financial stability. It makes budgeting easier and can prevent the stress associated with higher car payments. This stability is particularly valuable for individuals or families with fluctuating incomes or those managing multiple financial commitments.

The flexibility provided by reduced payments can also be beneficial in the event of unexpected expenses. Having more breathing room in your monthly budget means you’re better prepared for emergencies, rather than being stretched thin by a high car payment. This financial buffer can contribute significantly to overall peace of mind.

The Hidden Pitfalls: Disadvantages and Risks

While the advantages of an 84-month car loan are appealing, it’s crucial to look beyond the surface and understand the inherent disadvantages and risks. Failing to consider these can lead to significant financial difficulties down the road. Common mistakes to avoid are focusing solely on the monthly payment and overlooking the total cost.

Higher Total Interest Paid

This is arguably the most significant drawback of any long-term car loan. While your monthly payments are lower, you end up paying significantly more in total interest over the life of the loan. The longer you take to repay the principal, the more interest accrues.

For instance, a $30,000 car loan at 5% interest over 60 months might result in total interest of around $3,900. The same loan over 84 months could see you paying over $5,500 in interest, an increase of $1,600 or more. This additional cost means you’re effectively paying a much higher price for the same vehicle, simply for the convenience of lower monthly payments.

Extended Period of Indebtedness

Committing to an 84-month car loan means you’ll be in debt for seven years. This is a substantial period, longer than many people keep their vehicles. Being tied to a car payment for such an extended time can limit your financial flexibility in other areas of your life.

This long commitment can impact your ability to save for other goals, such as a down payment on a house, retirement, or even another significant purchase. It also means you’re carrying a substantial debt burden for a prolonged period, which can affect your debt-to-income ratio and future borrowing capacity.

Vehicle Depreciation and Negative Equity

Cars are depreciating assets, meaning they lose value rapidly from the moment they are driven off the lot. With an 84-month car loan, the rate at which your car depreciates often outpaces the rate at which you pay down the loan principal. This can quickly lead to a situation known as "negative equity" or being "upside down" on your loan.

Being upside down means you owe more on your car loan than the car is actually worth. This becomes a significant problem if your car is totaled in an accident or if you need to sell or trade it in before the loan is paid off. You’ll still owe the difference, potentially requiring you to pay out of pocket or roll the negative equity into a new loan, further compounding your debt. Based on my experience, this is one of the most common and painful financial traps for those with extended loans.

Higher Risk of Mechanical Issues

A car that is seven years old is much more likely to experience significant mechanical issues than a newer vehicle. Many factory warranties expire after three to five years, meaning that for a substantial portion of your 84-month car loan term, you’ll be responsible for all repair costs out of pocket.

These unexpected repair expenses can quickly negate any perceived savings from lower monthly payments. If you’re still making car payments on a vehicle that constantly needs expensive repairs, it can become a serious financial drain. This risk is amplified if you don’t factor in a robust emergency fund for vehicle maintenance.

Is an 84-Month Car Loan Right for You? Key Considerations

Deciding whether an 84-month car loan is the right choice requires careful introspection and a thorough evaluation of your personal financial situation. It’s not a one-size-fits-all solution, and what works for one person may be detrimental to another. Pro tips from us include always running the numbers comprehensively.

Your Financial Situation and Stability

Before considering an extended car financing option, honestly assess your income, expenses, and overall financial stability. Do you have a steady job with a reliable income stream? What is your current debt-to-income ratio? A lower monthly payment might seem appealing, but if your job security is uncertain or you have other significant debts, adding a seven-year commitment might be too risky.

Consider your emergency fund. Do you have at least three to six months’ worth of living expenses saved? This fund can act as a buffer if unexpected events impact your ability to make payments or if your car requires costly repairs. Without a solid financial foundation, an 84-month loan could quickly become a burden.

Your Credit Score and Interest Rate

Your credit score plays a pivotal role in the interest rate you’ll be offered. Borrowers with excellent credit (typically 720+) will qualify for the lowest rates, which somewhat mitigates the impact of higher total interest on an 84-month car loan. However, if your credit score is fair or poor, the interest rate can be significantly higher, dramatically increasing your total cost.

Always shop around for the best interest rates. Don’t just accept the first offer from the dealership. Get pre-approved by several lenders, including banks and credit unions, before you even set foot on a car lot. This allows you to compare offers and leverage them for a better deal. For more details on improving your credit score before applying, check out our guide on Boosting Your Credit Score for Car Loans.

The Vehicle’s Durability and Resale Value

If you’re considering an 84-month car loan, the specific vehicle you choose becomes even more critical. Opt for a car known for its reliability, durability, and strong resale value. Research brands and models that have a track record of lasting well beyond seven years with minimal major issues.

A vehicle that holds its value better will reduce your risk of negative equity down the line. Conversely, a car with a poor reliability record or rapid depreciation will amplify the financial risks associated with an extended car loan. Investing in a high-quality, dependable vehicle is paramount when committing to such a long payment term.

Your Driving Habits and Future Plans

How long do you typically keep your cars? If you tend to trade in or sell your vehicles every three to five years, an 84-month car loan is almost certainly not for you. You’ll likely be upside down on the loan when you’re ready to move on, creating a significant financial hurdle for your next purchase.

Consider your future plans as well. Do you anticipate major life changes, such as starting a family, moving, or changing careers, within the next seven years? Such events can alter your financial priorities and make a long-term car payment feel restrictive. If you’re someone who enjoys frequently upgrading your vehicle, an 84-month loan will severely limit that flexibility.

Alternatives to the 84-Month Car Loan

While an 84-month car loan might seem like the only way to afford your desired vehicle, several alternatives can offer better long-term financial outcomes. Exploring these options can help you achieve your automotive goals without falling into potential debt traps.

Shorter Loan Terms

The most straightforward alternative is to opt for a shorter loan term, such as 60 or 72 months. While this will result in higher monthly payments, it significantly reduces the total interest paid and accelerates the timeline to becoming debt-free. You’ll build equity faster and minimize the risk of negative equity.

If the monthly payments on a 60 or 72-month loan are too high, consider adjusting your vehicle choice rather than extending the loan term further. Sometimes, a slightly less expensive car on a shorter, more manageable loan is a far better financial decision.

Buying a Less Expensive Vehicle

Re-evaluating your needs versus your wants can lead to substantial savings. Do you truly need the top-trim model with all the bells and whistles, or would a more modest version suffice? Choosing a car that fits comfortably within a shorter loan term’s payment structure is a financially prudent move.

Remember, a car is primarily a mode of transportation. While comfort and features are nice, the core function can often be met by a more affordable vehicle. This approach allows you to avoid the long-term commitment and higher interest costs of an 84-month loan.

Saving for a Larger Down Payment

One of the most effective ways to reduce your monthly payments and total interest is to make a larger down payment. The more you put down upfront, the less you need to borrow, which directly translates to smaller loan amounts and shorter repayment periods.

Saving diligently for a substantial down payment might delay your car purchase by a few months, but the long-term financial benefits are often well worth the wait. It immediately builds equity in your vehicle and reduces the risk of being upside down on your loan.

Exploring the Used Car Market

The used car market offers incredible value, especially given how quickly new cars depreciate. A two or three-year-old used car often comes at a significantly lower price point, allowing you to afford a better model or trim level than you could new, while still benefiting from modern features and reliability.

Purchasing a used car often means you can secure a shorter loan term with more manageable monthly payments. If you’re weighing whether a new or used car is best for an extended loan, read our comprehensive comparison: New vs. Used Car: Which is Right for Your Long-Term Loan?.

Leasing a Vehicle

Leasing is another alternative, though it operates on a different principle. When you lease, you’re essentially paying for the depreciation of the vehicle during the lease term, plus taxes and fees. Lease terms are typically shorter (24-48 months), and monthly payments can often be lower than purchasing with a loan.

However, leasing means you never own the vehicle, and there are mileage restrictions and potential fees for excessive wear and tear. While it offers predictable payments and the ability to drive a new car every few years, it’s not a path to ownership and has its own set of considerations.

Navigating the Application Process for an Extended Loan

If, after careful consideration, you decide that an 84-month car loan is the right path for you, understanding the application process is crucial. Being prepared can improve your chances of approval and help you secure the best possible terms.

Lenders evaluate several factors when considering an extended car financing application. Your credit score is paramount, as it indicates your creditworthiness and history of repaying debts. They will also look at your debt-to-income ratio to ensure you can comfortably handle the new payment alongside existing financial obligations. Stable employment and income verification are also key requirements.

Before approaching a dealership, gather all necessary documentation: proof of income (pay stubs, tax returns), proof of residence (utility bills), identification, and possibly your current insurance information. It’s always a good idea to get pre-approved for a loan from your bank or credit union first. This gives you a concrete interest rate and loan amount, which you can then use as leverage when negotiating with the dealership’s finance department. Never feel pressured to sign anything on the spot; take your time to review all terms and conditions thoroughly.

Making an Informed Decision: Our Expert Recommendations

The question, "Can you get an 84-month car loan?" is almost always yes, assuming you meet lender criteria. However, the more important question is, "Should you get an 84-month car loan?" Our expert recommendation is to approach extended car financing with extreme caution and a full understanding of the long-term implications.

While the appeal of lower monthly payments is undeniable, the financial drawbacks of higher total interest, prolonged indebtedness, and the increased risk of negative equity are substantial. In most cases, a shorter loan term or a less expensive vehicle is a more financially sound choice.

If you absolutely must consider an 84-month car loan, ensure you meet these strict conditions:

- Excellent Credit Score: To secure the lowest possible interest rate and minimize the extra cost.

- Substantial Down Payment: To reduce the principal amount borrowed and mitigate negative equity risk.

- Highly Reliable Vehicle: Choose a car known for its durability and strong resale value, minimizing repair costs and depreciation.

- Stable Financial Situation: A secure job, robust emergency fund, and low existing debt are essential buffers.

- Long-Term Ownership Plan: You must plan to keep the car for the entire seven years, if not longer.

Always calculate the total cost of the loan, not just the monthly payment. Use online calculators to compare different loan terms and interest rates. Shop around extensively for the best financing offer. Understand every clause in your loan agreement before signing. For additional resources and tools to help you compare car loan offers and understand financing terms, we recommend visiting the Consumer Financial Protection Bureau’s website on auto loans: Consumer Financial Protection Bureau – Auto Loans.

Conclusion: Weighing the Long-Term Costs of Extended Car Financing

In conclusion, while an 84-month car loan is indeed a viable option for many consumers, it comes with a unique set of trade-offs. The allure of lower monthly payments is powerful, making seemingly unaffordable vehicles within reach. However, this immediate gratification often comes at the cost of significantly higher total interest paid, a prolonged period of debt, and the heightened risk of negative equity and costly repairs.

As professional SEO content writers and expert bloggers, our mission is to provide you with truly valuable, in-depth information. Based on our comprehensive analysis, we strongly advise potential car buyers to thoroughly weigh the pros and cons of extended car financing before committing to a seven-year term. Look beyond the monthly payment to understand the true cost of the loan. Consider alternatives, prioritize financial stability, and always make an informed decision that aligns with your long-term financial well-being. Your car purchase should empower your financial future, not burden it.