Can You Get Another Car Loan After A Repossession? Your Comprehensive Guide to Getting Back on the Road

Can You Get Another Car Loan After A Repossession? Your Comprehensive Guide to Getting Back on the Road Carloan.Guidemechanic.com

A car repossession can feel like a financial dead end. The sting of losing your vehicle, coupled with the immediate damage to your credit score, often leaves individuals wondering if they’ll ever qualify for financing again. It’s a challenging situation, no doubt, but here’s the crucial truth: while difficult, getting another car loan after a repossession is absolutely possible.

This article is designed to be your definitive guide, offering a deep dive into navigating the aftermath of a repossession and charting a clear path toward securing new auto financing. We understand the frustration and the urgent need for reliable transportation. Our goal is to equip you with the knowledge, strategies, and confidence to get back on the road.

Can You Get Another Car Loan After A Repossession? Your Comprehensive Guide to Getting Back on the Road

The Stark Reality: How Repossession Impacts Your Financial Future

Before we discuss getting another loan, it’s vital to understand the landscape you’re operating in. A repossession isn’t just about losing a car; it’s a significant marker on your financial record. It signals a default on a loan, and lenders view this as a high-risk indicator.

What Exactly is a Repossession?

In simple terms, repossession occurs when a lender takes back an asset, like a car, because the borrower has failed to make their loan payments as agreed. This action is usually a last resort for lenders, often after multiple missed payments or breaches of the loan contract. Once the car is repossessed, the lender typically sells it to recoup their losses. If the sale price doesn’t cover the outstanding loan balance, you could still owe a "deficiency balance."

The Lingering Shadow: How Long Does Repossession Stay on Your Credit Report?

A repossession is a serious negative mark, and it will remain on your credit report for approximately seven years from the date of the first missed payment that led to the repossession. This duration is consistent across all three major credit bureaus: Experian, Equifax, and TransUnion. For those seven years, it will significantly influence your credit score and your perceived creditworthiness.

The Immediate Aftermath: Impact on Your Credit Score

Based on my experience as a financial content writer, the immediate impact of a repossession on your credit score can be devastating. It can cause a substantial drop, often by 100 points or more, depending on your credit history before the event. This lower score makes it significantly harder to qualify for new credit, including car loans, mortgages, and even some rental agreements. Lenders see that repossession and immediately flag you as a higher risk.

The Short Answer: Yes, But It’s a Uphill Battle

So, can you get another car loan after a repossession? The definitive answer is yes, you can, but it’s crucial to manage your expectations. It will likely be more challenging than applying for a loan with a clean credit history, and the terms offered will reflect the increased risk lenders perceive.

The good news is that lenders understand that life happens. They also know that people need vehicles for work, family, and daily life. While a repossession is a major red flag, it doesn’t permanently disqualify you from future financing. Your ability to secure a new loan will depend on a combination of factors, including how much time has passed, your current financial situation, and the steps you take to improve your credit profile.

Key Factors Lenders Consider After a Repossession

When you apply for a car loan after a repossession, lenders will scrutinize your application even more closely. They want to assess whether the previous repossession was an isolated incident or indicative of ongoing financial instability.

Here are the critical factors they will evaluate:

- Time Elapsed Since Repossession: This is often the most significant factor. The further in the past the repossession occurred, the less impact it generally has. Lenders prefer to see that you’ve had time to recover and demonstrate responsible financial behavior since the event. If it happened just a few months ago, securing a loan will be exceptionally difficult.

- Current Credit Score and History Since: While the repossession stays on your report for seven years, your actions since the repossession matter immensely. Have you been making other payments on time? Have you reduced other debts? Lenders will look for signs of credit rebuilding and stability.

- Reason for Repossession: While not always explicitly asked, sometimes there are mitigating circumstances. Was it due to a sudden job loss, a medical emergency, or a divorce? Or was it due to consistent financial mismanagement? While lenders primarily focus on the numbers, understanding the "why" can sometimes play a small role, especially with smaller, local lenders or credit unions.

- Income and Employment Stability: Lenders want assurance that you can afford the new loan payments. A stable job history, ideally with the same employer for a significant period, and a consistent income stream are crucial. They’ll look for proof of steady earnings that comfortably cover the proposed car payment along with your other monthly expenses.

- Down Payment Size: A substantial down payment is a powerful tool in your favor. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your commitment and ability to save money.

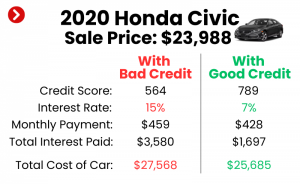

- Debt-to-Income (DTI) Ratio: Your DTI ratio is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Lenders want to see a low DTI, ideally below 36-43%, to ensure you have enough disposable income to handle a new car payment comfortably. A high DTI signals that you might be overextended.

Pro tips from us: Understand that lenders are assessing risk. Your job is to present yourself as the lowest possible risk, despite your past. Every positive financial action you take from today forward helps your case.

Steps to Prepare for a Car Loan Application After Repossession

Preparation is paramount when seeking a car loan after a repossession. Don’t just walk into a dealership or bank expecting an immediate approval. Strategic planning can significantly improve your chances.

Step 1: Understand Your Credit Report Inside and Out

Your credit report is your financial resume. You need to know exactly what’s on it.

- Obtain Your Credit Reports: You are entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months. Visit AnnualCreditReport.com, the only federally authorized source, to get yours.

- Scrutinize for Inaccuracies: Common mistakes to avoid are not thoroughly checking your reports. Look for any errors, such as incorrect account balances, accounts that aren’t yours, or duplicate negative entries. Even small inaccuracies can drag down your score.

- Dispute Any Errors: If you find mistakes, dispute them directly with the credit bureau and the creditor. Correcting errors can sometimes provide a small boost to your score.

- Address the Repossession Entry: Understand the details of the repossession entry. Is the balance owed accurate? Is the date correct? While you can’t remove a legitimate repossession, understanding its specifics is important.

Step 2: Actively Work to Improve Your Credit Score

Even with a repossession on your record, you can build positive credit history.

- Pay All Bills On Time, Every Time: This is the most critical step. Payment history accounts for 35% of your FICO score. Consistently making on-time payments on all your current debts (credit cards, utilities, student loans, etc.) shows financial responsibility.

- Reduce Existing Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can positively impact your score. Pay down credit card balances as much as possible.

- Consider a Secured Credit Card: If traditional credit is hard to get, a secured credit card can be a great tool. You deposit money as collateral, and that becomes your credit limit. Use it responsibly and pay it off in full each month to build positive payment history.

- Avoid New Debt (Initially): While rebuilding, try to avoid opening new lines of credit unless absolutely necessary. Too many new credit inquiries can temporarily lower your score.

Step 3: Save for a Substantial Down Payment

A significant down payment is your secret weapon when applying for a car loan after repossession.

- Why It’s Crucial: Lenders see a large down payment as a sign of commitment and reduced risk. It means you’re borrowing less, and you have equity in the vehicle from day one. This makes the loan more appealing to them.

- How Much to Save: Aim for at least 10-20% of the vehicle’s purchase price, or even more if possible. The more you put down, the better your chances of approval and potentially a lower interest rate.

- Demonstrates Responsibility: Saving a substantial amount shows a lender that you are financially disciplined and serious about this new commitment.

Step 4: Demonstrate Income Stability

Lenders need assurance that you can consistently make payments.

- Consistent Employment: Try to stay with the same employer for as long as possible. Lenders prefer to see at least 6-12 months, if not longer, of stable employment.

- Proof of Income: Be prepared to provide pay stubs, W-2s, and potentially bank statements to verify your income. If you’re self-employed, tax returns from the past two years will be essential.

Step 5: Create a Realistic Budget

Before you even start looking at cars, know what you can truly afford.

- Beyond the Monthly Payment: Pro tips from us: Many people only consider the monthly car payment. Remember to factor in insurance, fuel, maintenance, and potential repair costs. A car is more than just its sticker price.

- Understand Your Limits: Don’t overextend yourself. A car payment should ideally not exceed 10-15% of your take-home pay. Creating a detailed budget will prevent you from falling into the same trap that led to the previous repossession. We have an excellent article on () that can help you with this.

Finding the Right Lender for a Car Loan After Repossession

Not all lenders are created equal, especially when you have a repossession on your credit history. You’ll need to target lenders who specialize in or are more open to working with borrowers who have less-than-perfect credit.

1. Subprime Lenders

- Who They Are: These are lenders who specialize in providing loans to borrowers with lower credit scores or challenging credit histories. They are often more willing to take on the risk associated with a past repossession.

- What to Expect: Be prepared for higher interest rates and potentially stricter loan terms compared to conventional loans. This is their way of mitigating the increased risk. However, it’s often your most accessible path to approval.

2. Credit Unions

- Member-Focused Approach: Credit unions are non-profit organizations owned by their members. They often have more flexible lending criteria and may be more willing to work with members who have a challenging credit past, especially if you have a long-standing relationship with them.

- Potential for Better Rates: While not guaranteed, credit unions sometimes offer slightly better rates or more personalized service than traditional banks, even for bad credit auto loans.

3. Dealership Financing (Special Finance Departments)

- One-Stop Shop: Many larger dealerships have "special finance" or "second chance" departments. They work with a network of subprime lenders and can help match you with a loan program that fits your situation.

- Convenience vs. Cost: While convenient, ensure you’re still comparing offers. Dealerships might mark up interest rates to profit from the financing.

4. Buy Here, Pay Here (BHPH) Dealerships

- Direct Lending: BHPH dealerships are unique because they are both the seller and the lender. You make your payments directly to them. They often have very lenient approval standards, as they primarily focus on your income and ability to make payments, rather than just your credit score.

- Pros and Cons: The primary pro is easy approval, especially if you have a recent repossession. The significant cons include very high interest rates (often the maximum allowed by law), higher vehicle prices, limited vehicle selection, and sometimes less transparent practices. Use these as a last resort.

5. Online Lenders and Lending Marketplaces

- Comparison Shopping: Many online platforms specialize in connecting borrowers with bad credit to a network of lenders. This allows you to fill out one application and receive multiple offers, making it easier to compare rates and terms.

- Convenience: The application process is typically quick and can be done from home. However, always ensure the online lender is reputable and secure.

The Application Process: What to Expect

Once you’ve done your preparation and identified potential lenders, it’s time to apply. This stage requires organization and careful attention to detail.

Gathering Your Documents

Be ready with all necessary paperwork. This typically includes:

- Government-issued ID (driver’s license)

- Proof of income (pay stubs, W-2s, tax returns)

- Proof of residence (utility bill, lease agreement)

- Proof of insurance (you’ll need this before driving off with the car)

- References (sometimes requested)

- Your down payment

Pre-Approval vs. Full Application

- Pre-Approval: This is a smart first step. Many lenders offer pre-approval, which involves a soft credit pull (doesn’t hurt your score) and gives you an idea of how much you can borrow and at what interest rate. It gives you negotiating power at the dealership.

- Full Application: Once you’ve chosen a vehicle and are ready to finalize, the lender will conduct a hard credit inquiry, which will temporarily impact your score by a few points.

Understanding Loan Terms

Common mistakes to avoid are focusing solely on the monthly payment. You need to understand the full picture:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees. Even with a repossession, aim for the lowest APR possible.

- Loan Term: This is the length of the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but significantly higher total interest paid over the life of the loan.

- Total Cost of the Loan: Multiply your monthly payment by the number of months, then add any fees and the down payment. This will show you the real cost of the car.

Negotiating (If Possible)

Even with a repossession on your record, there might be some room for negotiation, especially if you come with a strong down payment and have multiple pre-approvals. Don’t be afraid to ask for a better rate or term.

The Role of a Cosigner

- Pros: If you have a trusted friend or family member with good credit who is willing to cosign, it can significantly improve your chances of approval and potentially secure a lower interest rate. Their good credit essentially offsets your past repossession.

- Cons: The cosigner is equally responsible for the loan. If you miss payments, it impacts their credit, and they are legally obligated to pay. This can strain relationships if things go wrong. Based on my experience, only consider a cosigner if you are absolutely confident in your ability to make every payment on time.

Strategies to Secure a Better Deal (Even with Bad Credit)

While you might not get prime rates right away, there are still ways to improve your loan terms.

- Maximize Your Down Payment: We can’t stress this enough. A larger down payment reduces the loan amount, decreases the lender’s risk, and can lead to a more favorable interest rate.

- Opt for a Shorter Loan Term (If Affordable): While a longer term means lower monthly payments, it costs you more in interest over time. If your budget allows, choose the shortest loan term you can comfortably manage.

- Utilize a Cosigner with Good Credit: As mentioned, a cosigner can be a game-changer for approval and rates, but use this option judiciously and with clear understanding for both parties.

- Consider a Less Expensive Vehicle: A reliable, used car that fits your budget is a far better choice than stretching for a new, expensive model. A cheaper car means a smaller loan, lower payments, and less risk for both you and the lender.

- Plan to Refinance Later: This is a smart long-term strategy. Get approved for a loan now, even if the interest rate is high. After 6-12 months of consistently making on-time payments, your credit score will likely improve. You can then apply to refinance the loan for a lower interest rate, saving you thousands over the life of the loan.

Rebuilding Your Credit and Avoiding Future Repossession

Securing a new car loan is a huge step, but the journey doesn’t end there. It’s an opportunity to build a stronger financial foundation and prevent future issues.

- Make Payments On Time, Every Time: This is non-negotiable. Set up automatic payments or calendar reminders. A single missed payment can derail your credit rebuilding efforts.

- Monitor Your Credit Report Regularly: Continue to check your credit reports annually for free. Consider using a credit monitoring service that offers monthly updates to stay on top of your financial health.

- Maintain a Strict Budget and Build an Emergency Fund: Pro tips from us: Unexpected expenses are a primary cause of missed payments. Having a robust emergency fund (3-6 months of living expenses) can be your financial safety net, preventing you from missing a car payment if a crisis arises. We have another helpful article on () that can assist you.

- Don’t Overextend Yourself: Resist the temptation to take on more debt than you can comfortably handle. Learn from past experiences and live within your means.

- Pay Down Other Debts: Continue to reduce other outstanding debts to improve your DTI ratio and overall credit health.

Conclusion: A Fresh Start is Within Reach

A repossession is a significant setback, but it is not a life sentence. While securing another car loan after a repossession presents unique challenges, it is absolutely achievable with patience, strategic planning, and diligent effort. By understanding your credit situation, actively working to improve your score, saving for a substantial down payment, and targeting the right lenders, you can successfully navigate this process.

Remember, this is an opportunity for a financial reset. Use this experience to build healthier money habits, demonstrate consistent responsibility, and ultimately regain your financial footing. The road ahead may require some extra effort, but with the right approach, you can get back behind the wheel and drive towards a more stable financial future.

Share your experiences or questions in the comments below – we’re here to help you on your journey!