Can You Get Approved For Two Car Loans? Your Ultimate Guide to Dual Vehicle Financing

Can You Get Approved For Two Car Loans? Your Ultimate Guide to Dual Vehicle Financing Carloan.Guidemechanic.com

The thought of owning two cars can be exciting, offering freedom, convenience, or meeting diverse family needs. But the practicalities of financing often lead to a crucial question: "Can you get approved for two car loans?" It’s a common query that many individuals and families face, especially when life demands an additional set of wheels.

The straightforward answer is yes, it is absolutely possible to secure approval for two car loans. However, it’s far from a simple process. Lenders view multiple loans as an increased risk, and your financial profile needs to be exceptionally strong to qualify. This comprehensive guide will explore every facet of getting approved for dual vehicle financing, from lender expectations to strategies for success and the financial implications involved. We’re here to provide an in-depth, expert perspective to help you navigate this significant financial decision.

Can You Get Approved For Two Car Loans? Your Ultimate Guide to Dual Vehicle Financing

The Possibility: Navigating the Path to Two Car Loans

Securing a second car loan isn’t about magic; it’s about demonstrating robust financial health and a low-risk profile to potential lenders. While many people successfully manage multiple vehicle payments, it requires a clear understanding of what financial institutions scrutinize. Lenders are in the business of assessing risk, and every loan application adds to their exposure.

Why might someone need two car loans? The reasons are varied. Perhaps a growing family requires a second, larger vehicle. Maybe a new job necessitates a dedicated work car, or an old vehicle simply gave out, requiring a replacement while the first loan is still active. Whatever the motivation, the core principle remains: you must convince a lender that you can comfortably afford both sets of payments, along with all your other financial obligations. It’s a significant commitment, and lenders will look for every indicator of your ability to manage it responsibly.

Key Factors Lenders Evaluate for Multiple Car Loans

When you apply for any car loan, lenders perform a thorough assessment of your financial standing. For a second car loan, this scrutiny becomes even more intense. They need to be confident that you possess the financial capacity to handle the added debt without defaulting. Let’s break down the critical factors they consider.

Your Credit Score: The Financial Report Card

Your credit score is arguably the most influential factor in any loan application, and it plays an even more pivotal role when seeking a second car loan. This three-digit number provides lenders with a snapshot of your past borrowing behavior and your overall financial reliability.

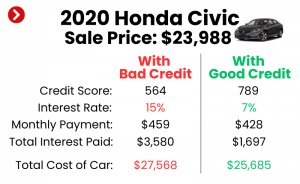

An excellent credit score, typically above 750, signals to lenders that you are a responsible borrower with a history of making timely payments. A score in this range significantly increases your chances of approval and often qualifies you for the best interest rates. Conversely, a fair or poor credit score will make securing a second loan much more challenging, as it suggests a higher risk of default. Based on my experience, lenders become very hesitant if your score is below 680 for a second loan, unless you have exceptionally high income and low existing debt.

It’s also important to understand how a second loan can initially impact your credit. Each application results in a "hard inquiry," which can cause a slight, temporary dip in your score. Furthermore, if approved, the new loan adds to your total debt, which might also affect your credit utilization or debt-to-income ratio. However, with consistent, on-time payments on both loans, your credit score can ultimately improve, demonstrating your enhanced ability to manage multiple credit obligations responsibly.

Pro Tip: Before even thinking about applying, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion). Review it meticulously for any errors or inaccuracies that could be unfairly dragging down your score. Disputing and correcting these can significantly boost your approval chances.

Debt-to-Income (DTI) Ratio: Your Financial Balancing Act

Your Debt-to-Income (DTI) ratio is a crucial metric that directly reflects your ability to take on additional debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Lenders use DTI to understand how much of your income is already committed to existing debts, leaving a clearer picture of what you have available for new obligations.

For a second car loan, your DTI becomes incredibly important because the existing car loan payment is already factored into your current ratio. The new car loan payment will directly increase your DTI. Lenders generally prefer a DTI ratio below 36%, although some might extend approval up to 43% for applicants with otherwise strong profiles. If your current DTI is already high, adding a second car payment could push it into an unacceptable range, making approval very difficult. Based on my experience, this is often the single biggest hurdle for most applicants seeking a second car loan. You might have excellent credit, but if your DTI is too high, the lender will view the new loan as an unmanageable burden.

Income Stability and Amount: The Foundation of Affordability

Lenders need irrefutable evidence that you earn enough money to comfortably cover all your expenses, including two car payments. This isn’t just about the total amount; it’s also about the stability and reliability of your income.

Steady employment with a consistent income stream is highly favored. Lenders will typically ask for proof of income, such as recent pay stubs, W-2 forms, or tax returns (especially for self-employed individuals). They want to see that your income is sufficient to handle both loan payments, insurance, maintenance, and your other living expenses without putting undue strain on your finances. A history of job hopping or inconsistent earnings can raise red flags, making lenders question your long-term ability to repay.

Payment History on Your Existing Loan: A Track Record of Reliability

How you’ve managed your first car loan provides a critical insight into your financial habits. A spotless payment history—meaning every payment made on time, every month—is a significant asset. It demonstrates to lenders that you are reliable and committed to your financial obligations.

Conversely, late payments, missed payments, or a history of repossessions on your first car loan will severely hinder your chances of getting approved for a second. Lenders will see this as a strong indicator that you might struggle with the added responsibility of another loan. Your track record speaks volumes about your financial discipline.

Down Payment: Reducing Risk, Boosting Chances

Making a substantial down payment on the second vehicle can significantly improve your chances of approval. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and decreases the overall risk for the lender.

From the lender’s perspective, a sizable down payment shows your commitment to the purchase and your financial stability. It also immediately creates equity in the vehicle, making it less likely that the car will be "underwater" (where you owe more than it’s worth) early in the loan term. While 10-20% is often recommended for a single car loan, aiming for an even higher percentage for a second loan can make your application much more appealing.

Loan-to-Value (LTV) Ratio: The Vehicle’s Worth

The Loan-to-Value (LTV) ratio compares the amount you borrow to the market value of the vehicle. For example, if a car is worth $20,000 and you borrow $18,000, your LTV is 90%. Lenders generally prefer lower LTV ratios, as it means they have less risk if the vehicle needs to be repossessed and sold.

A larger down payment directly results in a lower LTV, which is another reason why it’s so beneficial for a second car loan. If you’re buying a brand-new car, the LTV is typically lower initially. For used cars, especially older models, the LTV might be a concern if the car’s value depreciates quickly or if you’re not putting much down.

Vehicle Type and Age: The Asset’s Value

The type and age of the vehicle you intend to purchase for your second loan can also play a role. Lenders are generally more comfortable financing newer, more reliable vehicles with established resale values. These cars represent less risk in terms of potential repair costs for the borrower and better collateral for the lender.

If you’re looking to finance an older, high-mileage, or less common vehicle for your second car, lenders might be more cautious. Such vehicles often have higher maintenance costs and depreciate more rapidly, potentially increasing the risk profile of the loan.

Strategies to Improve Your Chances of Approval

Knowing what lenders look for is the first step; actively improving your financial standing is the next. Here are actionable strategies to bolster your application for a second car loan.

1. Improve Your Credit Score

This is foundational. A higher credit score makes you a more attractive borrower.

- Pay Bills on Time: This is the single most effective way to build and maintain good credit. Even one late payment can have a significant negative impact.

- Reduce Other Debts: Lowering your credit card balances and paying off other small loans can improve your credit utilization ratio, which positively affects your score.

- Dispute Errors: Regularly check your credit report for inaccuracies. If you find any, dispute them immediately with the credit bureaus.

- Avoid New Credit Inquiries: In the months leading up to your application for a second car loan, try to avoid opening new credit cards or applying for other types of loans, as each hard inquiry can temporarily lower your score.

2. Lower Your Debt-to-Income Ratio

As discussed, DTI is a major hurdle for multiple loans.

- Pay Down Existing Debts: Focus on aggressively paying down high-interest debts like credit cards and personal loans. Even a small reduction can make a difference.

- Increase Income (If Possible): While not always feasible, finding ways to boost your gross monthly income—through a side hustle, overtime, or a raise—will directly lower your DTI.

3. Save for a Larger Down Payment

This strategy offers multiple benefits.

- Reduce Loan Amount: A larger down payment means you borrow less, making the loan more manageable for you and less risky for the lender.

- Lower Monthly Payments: Less borrowed principal translates to lower monthly payments, which helps your DTI and overall budget.

- Show Commitment: It demonstrates your financial discipline and serious intent to own the vehicle. Aim for 20% or more if possible.

4. Choose an Affordable Second Vehicle

Don’t overextend yourself.

- Realistic Budget: Be honest about what you can truly afford for a second car payment, factoring in insurance, fuel, and maintenance for two vehicles.

- Consider Used: A reliable used car can significantly reduce the loan amount compared to a brand-new model, making approval easier and the financial burden lighter.

5. Maintain a Stellar Payment History on Your First Loan

Consistency is key.

- Never Miss a Payment: Your existing auto loan history is a direct reflection of your reliability. Ensure every payment is made on time, every month, without fail. This demonstrates your ability to manage an auto loan responsibly.

6. Shop Around for Lenders

Not all lenders have the same criteria or risk appetite.

- Explore Options: Check with traditional banks, credit unions (which often offer competitive rates and more flexible terms), and online lenders.

- Pre-qualification: Many lenders offer pre-qualification options that allow you to see potential loan terms without a hard credit inquiry. This helps you gauge your chances and compare offers without damaging your credit score.

- Pro Tip: Credit unions are often more relationship-oriented and might be more willing to work with members who have a strong financial history with them, even for a second loan.

7. Consider a Co-signer

If your financial profile is borderline, a co-signer with excellent credit and a low DTI can significantly boost your application.

- Shared Responsibility: A co-signer legally agrees to be responsible for the loan if you default. This reduces the risk for the lender.

- Common Mistakes to Avoid: Only choose a co-signer you trust implicitly and who understands the full implications. If you miss payments, it will damage their credit as well, and they will be legally obligated to pay. This can strain relationships severely.

Potential Pitfalls and Common Mistakes to Avoid

While getting a second car loan is achievable, there are several common mistakes that can derail your efforts or lead to significant financial strain down the road. Being aware of these pitfalls can help you navigate the process more smoothly.

1. Overestimating Your Affordability

This is perhaps the biggest and most dangerous mistake. Many people focus solely on the monthly loan payment, forgetting the broader financial picture. You’re not just taking on a second car payment; you’re taking on double the associated costs.

Consider:

- Insurance: Two vehicles mean two insurance premiums, which can be substantial.

- Fuel: Your fuel budget will likely double, or at least significantly increase.

- Maintenance: More moving parts mean more potential for repairs and routine servicing.

- Registration & Taxes: Double the annual fees.

Failing to account for these cumulative costs can lead to severe budget strain, making it difficult to meet all your financial obligations.

2. Applying Everywhere at Once

When eager for approval, it’s tempting to submit applications to multiple lenders simultaneously. However, this is a common mistake that can backfire. Each "hard inquiry" on your credit report can temporarily lower your credit score. Multiple inquiries in a short period signal to lenders that you might be desperate for credit or a high-risk borrower, making them less likely to approve you.

Instead, use pre-qualification tools to gauge your eligibility without affecting your score, and then apply only to the lenders where you have the best chance of approval.

3. Ignoring the Total Cost of Ownership

Beyond the monthly loan payment, the total cost of ownership (TCO) for two vehicles can be a shock if not properly budgeted. TCO includes depreciation, interest, insurance, fuel, maintenance, repairs, and fees. Two cars mean effectively doubling these costs.

A failure to account for the full TCO can quickly deplete your emergency savings, hinder other financial goals, or even lead to defaulting on one or both loans.

4. Not Checking Your Credit Report Thoroughly

As mentioned earlier, credit report errors are more common than you might think. Everything from incorrect addresses to mistaken late payments or even fraudulent accounts can appear. Not checking your report means you might be applying for a loan with an unfairly low credit score, reducing your chances of approval or resulting in higher interest rates. Always review your reports from all three bureaus well in advance.

5. Falling for High-Interest Loans

If your financial profile is borderline, you might be approved for a second car loan but with an exceptionally high interest rate. While tempting to accept just to get the vehicle, a high-interest loan can significantly increase the total cost of borrowing and make your monthly payments almost unmanageable.

Pro Tip from us: If the interest rate offered is exorbitant, it’s a strong indicator that the loan might be beyond your comfortable means. Reconsider if taking on such expensive debt is truly in your best financial interest. Sometimes, waiting, saving more, or choosing a less expensive vehicle is the smarter move.

The Financial Implications of Managing Two Car Loans

Successfully securing two car loans is just the beginning. The ongoing management of this dual debt carries significant financial implications that demand careful planning and disciplined execution.

Budgeting Challenges

Managing two car loans effectively requires a meticulous approach to budgeting. You’ll need to allocate funds for two monthly payments, two insurance policies, potentially double the fuel costs, and increased maintenance expenses. This can significantly reduce your discretionary income and make it challenging to meet other financial goals. It’s crucial to create a detailed budget that accounts for every dollar, ensuring you have enough liquidity to cover all your obligations without stress.

Internal Link Suggestion: For a deeper dive into managing your finances, check out our article on "Understanding Your Debt-to-Income Ratio for Loan Approvals" to see how different debts interact.

Impact on Future Financial Goals

Taking on a second car loan can have a ripple effect on your long-term financial aspirations. The substantial monthly outlay for two vehicles might mean less money available for savings, investments, retirement planning, or even a down payment on a home. Before committing, consider whether this immediate convenience outweighs your future financial security. It’s a trade-off that requires careful consideration of your priorities.

Credit Score Management

While initially, a second loan might cause a slight dip in your credit score due to the hard inquiry and increased debt, responsible management can actually strengthen your credit. Consistently making on-time payments on both loans demonstrates a high level of creditworthiness. However, the reverse is also true: missing payments on either loan can cause significant damage to your credit score, making it harder to secure future loans or credit cards. Vigilance and discipline are paramount.

Refinancing Options

Should your financial situation improve—perhaps your credit score increases, or interest rates drop—you might consider refinancing one or both of your car loans. Refinancing involves taking out a new loan to pay off an existing one, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payments or the total interest paid over the life of the loan, providing some financial relief.

Internal Link Suggestion: To learn more about this strategy, read our comprehensive "Is Car Loan Refinancing Right for You?" guide.

Alternatives to Taking Out a Second Car Loan

Sometimes, the desire for a second car is strong, but the financial strain of a second loan isn’t feasible or desirable. Fortunately, there are several viable alternatives to consider.

1. Buying a Used Car Outright (Cash)

If you have sufficient savings, purchasing a reliable used car with cash eliminates the need for a second loan entirely. This avoids interest payments, reduces your DTI, and frees up your monthly budget. While it requires a significant upfront investment, the long-term financial benefits can be substantial.

2. Leasing a Second Vehicle

Leasing offers lower monthly payments compared to buying, as you’re essentially paying for the vehicle’s depreciation during the lease term, not its full purchase price. This can be an attractive option if you only need a second car temporarily or prefer to drive newer models every few years. However, you won’t own the car at the end of the lease, and mileage restrictions can apply.

3. Ridesharing and Public Transportation

For occasional needs for a second car, or if your daily commute allows, utilizing ridesharing services (like Uber or Lyft) or public transportation can be a cost-effective alternative. This avoids all the associated costs of ownership (insurance, fuel, maintenance, parking) and only incurs expenses when you actually need the service.

4. Carpooling

If the primary reason for a second car is commuting, carpooling with colleagues or neighbors can significantly reduce transportation costs and the need for an additional vehicle. It’s also environmentally friendly!

5. Temporary Rental or Car-Sharing Services

For situations where a second car is only needed intermittently (e.g., weekend trips, moving large items), services like Zipcar or traditional car rentals can provide a flexible solution without the long-term commitment of a loan. You pay for the car only when you need it.

Conclusion: Navigating Dual Car Financing Responsibly

The journey to getting approved for two car loans is undeniably challenging, yet entirely possible for those with a strong financial foundation and a meticulous approach. It’s a decision that requires a thorough understanding of your financial capacity, a commitment to responsible borrowing, and an awareness of both the rewards and the significant responsibilities involved.

Throughout this guide, we’ve emphasized the critical role of your credit score, debt-to-income ratio, stable income, and a solid payment history. These are the pillars upon which lenders build their approval decisions. By actively working to improve these areas, making a substantial down payment, and thoughtfully shopping for lenders, you can significantly enhance your chances of securing the financing you need.

Remember, the goal isn’t just to get approved, but to manage both loans comfortably without jeopardizing your financial stability or future goals. Always consider the total cost of ownership for two vehicles, avoid common pitfalls like overextending your budget or applying everywhere, and explore alternatives if a second loan doesn’t align with your financial situation.

Ultimately, getting approved for two car loans is a testament to your financial discipline and strategic planning. Approach it with care, diligence, and a clear understanding of the implications, and you’ll be well-equipped to make the best decision for your needs.

External Link: For more general guidance on managing debt and understanding your financial health, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website, a trusted source for consumer financial information.