Can You Have Two Car Loans? Navigating the Road to Multiple Vehicle Financing

Can You Have Two Car Loans? Navigating the Road to Multiple Vehicle Financing Carloan.Guidemechanic.com

The idea of owning two cars, or even more, is a common aspiration for many households. Perhaps you need a reliable daily commuter and a rugged weekend adventurer. Maybe your partner needs their own vehicle for work, or your growing family demands more space. Whatever the reason, a fundamental question arises: Can you have two car loans simultaneously?

The short answer is yes, it’s absolutely possible. However, the path to securing a second car loan is often more intricate than the first, requiring careful financial planning and a deep understanding of lender expectations. As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate these waters. In this comprehensive guide, we’ll explore everything you need to know about taking on multiple vehicle loans, from lender considerations to smart financial strategies and common pitfalls to avoid.

Can You Have Two Car Loans? Navigating the Road to Multiple Vehicle Financing

The Simple Truth: Yes, But With Conditions

Having two car loans at the same time is not inherently prohibited by lenders or financial institutions. Many people successfully manage multiple vehicle loans. The primary hurdle isn’t a hard "no," but rather a comprehensive assessment of your financial health and capacity to repay by potential lenders.

Lenders are in the business of assessing risk. When you apply for any loan, they want to be confident that you can meet your repayment obligations without undue stress. Adding a second car loan significantly increases your monthly debt burden, which naturally elevates the perceived risk. Therefore, while the possibility exists, the approval process will scrutinize your finances with a much finer comb.

What Lenders Look At: The Pillars of Approval

When you apply for a second car loan, lenders don’t just glance at your application. They perform a thorough deep dive into several key financial indicators. Understanding these factors is crucial for improving your chances of approval.

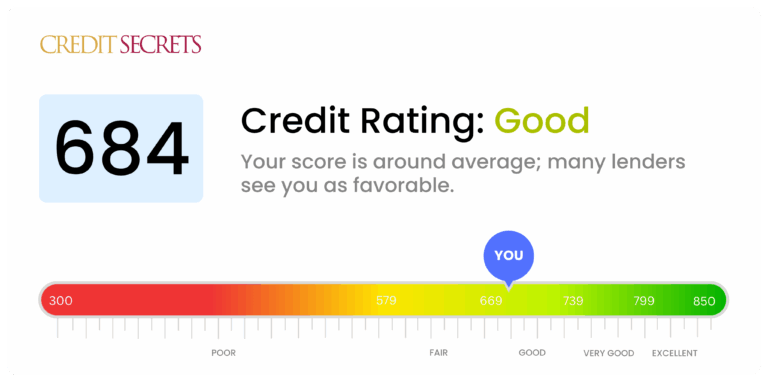

1. Your Credit Score: The Foundation of Trust

Your credit score is arguably the most critical factor. It’s a numerical representation of your creditworthiness, reflecting your payment history, debt levels, length of credit history, and types of credit used.

Based on my experience, a strong credit score (typically 700 and above) is paramount when seeking a second car loan. It signals to lenders that you are a responsible borrower who pays debts on time. A lower score might not automatically disqualify you, but it will likely result in higher interest rates or stricter loan terms.

2. Debt-to-Income (DTI) Ratio: Your Financial Capacity

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders use to assess your ability to manage monthly payments. It compares your total monthly debt payments to your gross monthly income.

Pro tips from us: To calculate your DTI, sum up all your recurring monthly debt payments – this includes your first car loan, mortgage or rent, credit card minimums, student loan payments, and any other loan payments. Then, divide this total by your gross monthly income (before taxes and deductions). For a second car loan, most lenders prefer a DTI ratio of 36% or lower, though some might go up to 43% for well-qualified borrowers. A high DTI indicates that a significant portion of your income is already allocated to debt, making a second loan a risky proposition.

3. Income Stability and Employment History: A Steady Stream

Lenders want to see a consistent and reliable income stream. This often means stable employment history, ideally with the same employer for at least two years.

Proof of income, such as pay stubs, W-2s, or tax returns for self-employed individuals, will be required. A fluctuating income or frequent job changes can raise red flags, suggesting an unreliable ability to make consistent loan payments.

4. Existing Debt Load: The Full Picture

Beyond your DTI, lenders will look at the composition of your existing debt. How much is secured debt (like your first car loan or mortgage) versus unsecured debt (like credit cards)?

A significant amount of high-interest credit card debt, even if your DTI is acceptable, can be a deterrent. It indicates a potential struggle with managing revolving credit, which can be a warning sign for future loan repayment.

5. Down Payment: Reducing Lender Risk

Making a substantial down payment on your second vehicle can significantly improve your chances of approval and secure a better interest rate. A larger down payment reduces the loan amount, thereby lowering the lender’s risk.

It also demonstrates your financial discipline and commitment to the purchase. Common mistakes to avoid are thinking a down payment is optional; it’s often a strategic move for a second loan.

6. Vehicle Value and Type: The Collateral Factor

The type and value of the car you’re looking to finance for the second loan also play a role. Lenders view newer, more reliable vehicles as less risky collateral.

A very old, high-mileage vehicle might be harder to finance, especially if its market value is low. The lender needs to be confident that the vehicle can be resold to cover the loan balance if you default.

7. Loan-to-Value (LTV) Ratio: Equity in the Vehicle

The Loan-to-Value (LTV) ratio compares the amount of the loan to the market value of the vehicle. For instance, if a car is worth $20,000 and you borrow $18,000, your LTV is 90%.

A lower LTV (meaning you’ve put down a larger down payment) is always more favorable to lenders, as it provides them with a greater buffer should they need to repossess and sell the vehicle.

Why Someone Might Need Two Car Loans

People consider a second car loan for a variety of legitimate reasons, reflecting diverse lifestyle and professional needs.

- Household Needs: In a two-income household, it’s often essential for both partners to have their own reliable transportation for commuting to work or managing family responsibilities.

- Business Use: An individual might need a personal vehicle and a separate, specialized vehicle for their business – perhaps a truck for contracting or a fuel-efficient car for sales calls.

- Specific Utility: One car might be ideal for daily city driving, while a second vehicle (like an SUV or truck) is needed for weekend hobbies, towing, or hauling.

- Family Growth: As families expand, the need for a larger, safer vehicle often arises, while the existing smaller car might still be perfectly functional for other purposes.

- Different Commutes: If one partner has a long highway commute and the other has a short city commute, two different types of vehicles might make economic sense (e.g., a hybrid for one, a standard sedan for the other).

These scenarios highlight practical needs, not just desires, which lenders understand. However, the ability to finance these needs is where the scrutiny lies.

Potential Benefits of Having Two Car Loans (If Managed Well)

While taking on more debt always comes with risks, there can be genuine advantages to managing two car loans successfully.

- Enhanced Flexibility: Two vehicles provide unparalleled flexibility for a household. It means independence for multiple drivers and the ability to meet diverse transportation needs without compromise.

- Meeting Specific Needs: As mentioned, having distinct vehicles for different purposes (work, family, recreation) can significantly improve efficiency and quality of life.

- Building Credit History: Consistently making on-time payments for two separate car loans can be a powerful way to strengthen your credit score. It demonstrates to credit bureaus that you can responsibly manage multiple lines of credit. This can open doors to better rates on future loans, like a mortgage.

- Emergency Preparedness: In the event one car breaks down or is in an accident, having a second vehicle provides immediate backup, preventing disruptions to work or family routines.

The Risks and Challenges of Managing Multiple Car Loans

While the benefits are clear, it’s crucial to acknowledge the significant risks involved in managing two car loans. Ignoring these challenges can lead to serious financial strain.

- Increased Financial Burden: This is the most obvious risk. Your total monthly debt payments will escalate significantly, reducing your disposable income and potentially impacting your ability to save for other goals or handle emergencies.

- Higher Interest Rates: If your DTI is already elevated or your credit score isn’t top-tier, the second loan might come with a higher interest rate. This means you’ll pay more over the life of the loan.

- Impact on Credit Score (Negative): While timely payments build credit, missing even one payment on either loan can severely damage your credit score. With two loans, the risk of a missed payment (and its negative repercussions) is effectively doubled.

- Reduced Financial Flexibility: A larger portion of your income tied up in car payments means less money available for discretionary spending, investments, or unexpected expenses. This can make your financial situation more fragile.

- Exacerbated Maintenance and Insurance Costs: It’s not just the loan payments. Remember that two cars mean double the insurance premiums, registration fees, and routine maintenance costs (oil changes, tires, brakes). Fuel costs will also be higher.

- Depreciation: Cars are depreciating assets. Owning two means you’re losing value on two fronts simultaneously, which isn’t ideal for long-term wealth building.

Strategies for Successfully Obtaining and Managing Two Car Loans

If you’ve assessed the risks and determined that a second car loan is a necessary and manageable step, here are some expert strategies to improve your chances of approval and ensure long-term success.

1. Boost Your Credit Score Proactively

Before even applying, take steps to improve your credit score. Pay down existing credit card balances, ensure all your bills are paid on time, and check your credit report for any errors.

A higher score will not only increase your approval odds but also secure you a more favorable interest rate, saving you money in the long run.

2. Reduce Existing Debt

Focus on paying down other high-interest debts, especially credit cards, before applying for a second car loan. This directly impacts your DTI ratio, making you a more attractive borrower.

Even small reductions can make a difference in how lenders view your overall financial picture.

3. Save for a Larger Down Payment

Aim for a down payment of at least 20% on the second vehicle, if not more. This significantly reduces the loan amount and the lender’s risk.

A substantial down payment also means you’ll likely have a lower monthly payment and pay less interest over the loan term.

4. Shop Around for the Best Rates

Don’t settle for the first offer. Contact multiple lenders – banks, credit unions, and online lenders – to compare interest rates and loan terms.

Based on my experience, credit unions often offer some of the most competitive auto loan rates. Get pre-approved if possible, as this gives you negotiating power at the dealership.

5. Consider a Co-signer (With Caution)

If your credit isn’t perfect or your DTI is borderline, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better rate.

However, remember that a co-signer is equally responsible for the debt. If you default, their credit will be damaged, and they’ll be on the hook for payments. This decision should only be made with extreme trust and clear communication.

6. Create a Robust Budget

A detailed budget is non-negotiable when managing two car loans. Factor in all expenses: two loan payments, two insurance premiums, double the fuel, and anticipated maintenance for both vehicles.

Pro tips from us: Use a spreadsheet or budgeting app to track every dollar. This helps you visualize your cash flow and identify areas where you can cut back if needed.

7. Automate Payments

Set up automatic payments from your bank account for both car loans. This ensures you never miss a payment, protecting your credit score and avoiding late fees.

It also takes the mental burden off remembering due dates for multiple debts.

8. Explore Refinancing Options

If your credit score improves after a year or two, or if interest rates drop, consider refinancing one or both of your car loans.

Refinancing could secure you a lower interest rate, reducing your monthly payments or the total amount of interest paid over the life of the loan.

Common Mistakes to Avoid When Getting a Second Car Loan

Even with the best intentions, people often make errors that can jeopardize their financial stability or lead to rejection.

- Ignoring Your DTI Ratio: Many applicants underestimate how critical their DTI is. Don’t just guess; calculate it accurately before applying. A DTI that’s too high is a primary reason for rejection.

- Applying to Too Many Lenders at Once: Each loan application can result in a "hard inquiry" on your credit report. Too many hard inquiries in a short period can temporarily lower your credit score, making you seem desperate for credit. Shop smart, and group your inquiries within a short window (e.g., 14-30 days) so they’re often counted as a single inquiry for scoring purposes.

- Not Budgeting for ALL Car Expenses: It’s easy to focus solely on the loan payment. But two cars mean double the insurance, registration, maintenance, and fuel. Common mistakes to avoid are underestimating these ancillary costs.

- Taking on More Debt Than You Can Handle: Be honest with yourself about your financial capacity. Don’t let the desire for a second car push you into a situation where you’re "house poor" (or "car poor") and struggling to make ends meet.

- Not Reading the Fine Print: Understand all terms and conditions of both loans, including interest rates, fees, prepayment penalties, and late payment clauses. Don’t sign anything you don’t fully comprehend.

When to Say No to a Second Car Loan

Sometimes, the most responsible decision is to hold off on taking on additional debt. Here are clear indicators that a second car loan might not be right for you right now:

- Your DTI is Already High: If your DTI is already above 40%, adding another significant monthly payment will likely push you into a financially precarious position.

- Unstable Income or Job Security: If your job is uncertain, or your income fluctuates wildly, committing to another fixed monthly payment is a risky gamble.

- You’re Struggling with Your First Loan: If you’re already having trouble making payments on your first car loan, or any other debt, a second loan will only compound your problems.

- No Emergency Fund: Without a healthy emergency fund (ideally 3-6 months of living expenses), an unexpected repair or job loss could quickly lead to defaulting on one or both loans.

- You Don’t Have a Clear "Need": If the second car is more of a "want" than a "need," and your finances are tight, it’s wise to reconsider. Financial stability should always take precedence over convenience or luxury.

Alternatives to a Second Car Loan

If a second car loan isn’t feasible or desirable, there are still ways to address your transportation needs without taking on more debt.

- Public Transportation: For urban dwellers, buses, trains, and subways can be a cost-effective alternative to a second car, especially for commuting.

- Ride-Sharing Services: Services like Uber or Lyft can provide on-demand transportation for occasional needs without the burden of ownership.

- Car-Sharing Programs: Services like Zipcar allow you to rent a car by the hour or day, providing access to a vehicle without the commitment of a loan.

- Carpooling: Coordinating with colleagues or neighbors for commutes can significantly reduce the need for a second vehicle and split fuel costs.

- Bicycle/Walking: For short distances, these are not only cost-free but also offer health benefits.

- Leasing a Vehicle: While still a monthly payment, leasing often has lower monthly payments than purchasing, and typically covers maintenance, offering a temporary solution without the long-term commitment of ownership. Read our guide on to learn more.

- Purchasing an Affordable Used Car with Cash: If you have some savings, consider buying an older, reliable used car outright. This avoids loan payments and interest entirely.

Conclusion: Drive Smart, Not Just Twice

The question "Can you have two car loans?" is met with a resounding "yes," but it comes with a significant asterisk. It’s a journey that requires meticulous financial planning, a solid credit foundation, and a deep understanding of your own income and expenses. Lenders are looking for low-risk borrowers, and demonstrating your capacity to manage increased debt is key.

Based on my experience helping individuals navigate complex financial decisions, the ultimate success of managing two car loans hinges on proactive preparation and disciplined management. Weigh the benefits against the substantial risks, be honest about your financial limits, and implement the strategies outlined in this guide. By doing so, you can confidently and responsibly add a second vehicle to your life, ensuring it enhances your lifestyle rather than becoming a financial burden. Always remember to prioritize your overall financial well-being above all else. For personalized advice, consider consulting with a trusted financial advisor or visiting resources like the Consumer Financial Protection Bureau (External Link: Consumer Financial Protection Bureau) to understand your rights and options.

For further reading on managing your finances effectively, check out our article on .