Can You Still Get a Car Loan With a Repossession? Your Comprehensive Guide to Getting Back on the Road

Can You Still Get a Car Loan With a Repossession? Your Comprehensive Guide to Getting Back on the Road Carloan.Guidemechanic.com

Facing a car repossession can feel like a financial dead end, leaving you wondering if you’ll ever qualify for another auto loan. It’s a disheartening experience that significantly impacts your credit, but it doesn’t necessarily mean the door to future vehicle ownership is permanently closed. The good news is, you can still get a car loan with a repossession on your record, though it requires a strategic approach, patience, and a clear understanding of the challenges ahead.

This in-depth guide is designed to empower you with the knowledge and actionable steps needed to navigate the landscape of auto financing after a repossession. We’ll explore what lenders look for, how to prepare your finances, and where to find potential loan opportunities, ensuring you have the best possible chance to get back behind the wheel.

Can You Still Get a Car Loan With a Repossession? Your Comprehensive Guide to Getting Back on the Road

Understanding Repossession and Its Lasting Impact

Before diving into how to secure a car loan, it’s crucial to grasp the full implications of a repossession. This event isn’t just about losing your vehicle; it leaves a significant mark on your financial history.

A repossession occurs when a lender takes back an asset, like a car, that was used as collateral for a loan, typically because the borrower failed to make agreed-upon payments. This action is a direct result of defaulting on your loan agreement.

The immediate consequence is the loss of your vehicle, which can disrupt your daily life, especially if you rely on it for work or family responsibilities. More importantly, a repossession is reported to the major credit bureaus.

It remains on your credit report for up to seven years from the date of the original delinquency. This negative mark severely lowers your credit score, signaling to future lenders that you represent a higher risk.

The psychological toll can also be profound, leading to feelings of shame or hopelessness. Financially, it makes securing new lines of credit, including car loans, significantly more challenging and often more expensive due to higher interest rates.

The Core Question: Can You Still Get a Car Loan With a Repossession? The Honest Truth

The definitive answer is yes, it is possible to get a car loan after a repossession. However, it’s important to manage your expectations and understand that it won’t be as straightforward as applying with a pristine credit history. The path forward will likely involve higher interest rates, stricter terms, and a more thorough vetting process by lenders.

While a repossession undeniably makes you a "high-risk" borrower in the eyes of many traditional lenders, there are financial institutions and strategies specifically designed for individuals in your situation. These often fall under the umbrella of "subprime lending."

Subprime lenders specialize in offering loans to borrowers with less-than-perfect credit scores. They understand that financial setbacks happen and are willing to take on more risk, albeit with conditions that reflect that increased risk.

Your success in securing an auto loan will largely depend on several key factors, including how much time has passed since the repossession, your current financial stability, and the proactive steps you take to improve your creditworthiness. Don’s give up hope; preparation is your most powerful tool.

Key Factors Lenders Consider After a Repossession

When you apply for a car loan with a repossession on your record, lenders will scrutinize various aspects of your financial profile. Understanding these factors can help you prepare your application effectively.

Time Since Repossession

The amount of time that has elapsed since your repossession is a critical factor. The further in the past the repossession occurred, the less impact it generally has on a lender’s decision. Lenders prefer to see that you’ve had time to rebuild your financial footing.

A repossession from six months ago will be viewed much differently than one from three or four years ago. Each year that passes without further negative marks demonstrates a renewed commitment to financial responsibility.

Based on my experience, most lenders prefer to see at least one to two years pass since the repossession before considering a new auto loan. The longer the gap, the better your chances and potentially more favorable terms.

Reason for Repossession

While your credit report won’t detail the "why" behind the repossession, lenders may ask you to explain the circumstances. There’s a difference between a repossession caused by unforeseen hardships versus one stemming from consistent financial mismanagement.

Life events such as job loss, a medical emergency, or a divorce can lead to financial distress that results in a repossession. Lenders might be more understanding if you can demonstrate that the repossession was due to an isolated, unavoidable event rather than a pattern of irresponsible spending.

Be prepared to explain your situation clearly and concisely, focusing on how you’ve addressed the underlying issues. Honesty and transparency are paramount in building trust with a potential lender.

Current Financial Stability

Lenders want to see evidence that you are now in a stable financial position to handle new debt. This includes your current income, employment history, and your debt-to-income (DTI) ratio.

A steady job with a consistent income for an extended period (e.g., 6-12 months at the same employer) signals reliability. Lenders want assurance that you have the regular cash flow necessary to make your monthly car payments.

Your DTI ratio, which compares your monthly debt payments to your gross monthly income, is also crucial. A lower DTI indicates that you have more disposable income available to take on a new loan without being overextended.

Down Payment

The power of a substantial down payment cannot be overstated when applying for a car loan after a repossession. A significant down payment reduces the amount you need to borrow, thereby lowering the lender’s risk.

It demonstrates your financial commitment to the purchase and indicates that you have savings. Lenders view a larger down payment as a sign of a more responsible borrower, even with past credit issues.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price, if not more. This can often be the single most influential factor in getting your loan approved and potentially securing a lower interest rate.

Co-Signer

Having a creditworthy co-signer can significantly improve your chances of approval. A co-signer, typically a family member or close friend with excellent credit, agrees to be legally responsible for the loan if you fail to make payments.

This arrangement provides an additional layer of security for the lender, mitigating the risk associated with your past repossession. Their good credit essentially "backs up" your application.

However, choosing a co-signer is a serious decision. Ensure they understand the full implications, as their credit will also be affected if you default. This should only be pursued with someone you trust implicitly and who understands the risks involved.

Other Credit History

Lenders will look beyond the repossession to see if you have any other credit accounts, especially positive ones, since the incident. This shows a pattern of rebuilding.

Have you opened a secured credit card and made timely payments? Are there any other loans (like personal loans) that you’ve managed responsibly? Any positive credit activity, no matter how small, can help offset the negative impact of the repossession.

This demonstrates to lenders that you are actively working to improve your credit and are capable of managing debt responsibly now. Every on-time payment you make post-repossession helps to slowly mend your credit profile.

Steps to Take Before Applying for a Car Loan

Preparation is key when seeking an auto loan after a repossession. Taking these steps beforehand will not only increase your chances of approval but also help you secure the best possible terms.

Review Your Credit Report

Your first and most critical step is to obtain and thoroughly review copies of your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. This will give you a clear picture of your current credit standing.

Look for any inaccuracies or outdated information. If you find errors, dispute them immediately with the credit bureau. Correcting mistakes can potentially boost your credit score.

Understanding exactly what lenders will see on your report allows you to anticipate their concerns and prepare your explanations. You can access your free credit reports annually at .

Improve Your Credit Score (Even Marginally)

While a repossession significantly impacts your score, you can start taking steps to improve it, even if incrementally. Every point counts.

Focus on making all current bill payments on time, every time. This includes utilities, credit cards, and any other loan obligations. Payment history is the most significant factor in your credit score.

If you have outstanding debts, try to pay them down, especially credit card balances. A lower credit utilization ratio (how much credit you’re using versus how much is available) can positively impact your score. Consider opening a secured credit card if you don’t have one, and use it responsibly.

Save for a Substantial Down Payment

As mentioned earlier, a large down payment is your best asset when applying for a loan with a repossession. Start saving diligently now.

The more money you can put down upfront, the less you’ll need to borrow, which reduces the lender’s risk and your monthly payments. This also shows financial discipline and commitment.

Pro tips from us: Even if it means waiting a few extra months to save more, it’s often worth it. A 20% down payment on a used car can make a significant difference in approval odds and interest rates.

Create a Realistic Budget

Before you even look at cars, sit down and create a comprehensive budget. Understand exactly how much you can truly afford for a monthly car payment, including insurance, fuel, and maintenance costs.

Don’t just consider the principal and interest. Factor in all associated expenses to avoid future financial strain. Overextending yourself on a car payment is a common mistake to avoid, especially after a repossession.

Having a clear budget will help you set realistic expectations for the type of vehicle you can purchase and prevent you from falling into another financial predicament. can offer more insights into budgeting for a vehicle.

Gather Necessary Documentation

Lenders will require various documents to verify your identity, income, and residency. Having these ready will streamline the application process.

Typical documents include: government-issued ID, proof of residence (utility bill), recent pay stubs or bank statements to verify income, and possibly a list of references. Be prepared to provide detailed employment history.

Being organized and presenting a complete application package demonstrates your seriousness and preparedness, which can leave a positive impression on lenders.

Finding the Right Lenders

Not all lenders are created equal, especially when you have a repossession on your credit report. You’ll need to target those who specialize in or are more open to working with borrowers in your situation.

Subprime Lenders/Specialty Finance Companies

These lenders are your primary target. Subprime lenders specialize in providing loans to individuals with poor credit, including those with bankruptcies or repossessions.

They assess risk differently than traditional banks, often focusing more on your current income and ability to pay rather than solely on your past credit score. Their business model accounts for higher risk, which means higher interest rates for you.

Research reputable subprime lenders online or ask for recommendations from dealerships that cater to bad credit customers. Be wary of any lender that guarantees approval without checking your credit or demands upfront fees.

Credit Unions

Credit unions are member-owned financial institutions known for their more personalized approach and often more flexible lending criteria compared to large banks.

If you are a member of a credit union, or eligible to join one, it’s worth exploring their auto loan options. They might be more willing to consider your individual circumstances and offer slightly better rates due to their non-profit nature.

Building a relationship with a credit union by opening a savings account and demonstrating responsible financial behavior can be beneficial when applying for a loan.

Buy Here, Pay Here Dealerships

These dealerships offer in-house financing, meaning they are both the seller and the lender. They often approve customers with very poor credit or no credit history at all.

While convenient, "buy here, pay here" dealerships typically come with significant drawbacks. Common mistakes to avoid include not scrutinizing their interest rates, which are often very high, and being stuck with limited vehicle options.

Always read the contract carefully, understand all fees, and compare their offers with other lenders if possible. The convenience often comes at a steep price.

Online Loan Marketplaces

Several online platforms connect borrowers with a network of lenders, including those who specialize in bad credit auto loans. These marketplaces can be a good starting point for comparing offers without visiting multiple dealerships.

You can often get pre-qualified without a hard inquiry on your credit, allowing you to see potential rates and terms. This can save you time and multiple credit inquiries, which can further ding your score.

Always ensure the online platform is reputable and secure before submitting your personal information. Read reviews and look for transparent terms and conditions.

Avoid Predatory Lenders

Unfortunately, some lenders prey on individuals desperate for a loan. Be cautious of anyone promising guaranteed approval regardless of credit, demanding large upfront fees, or pushing you into a loan you clearly can’t afford.

If an offer seems too good to be true, it probably is. Always verify a lender’s legitimacy and licensing, and never feel pressured into signing a contract you don’t fully understand.

The Application Process: What to Expect

Once you’ve done your homework and found potential lenders, it’s time to apply. Knowing what to expect can help you navigate the process with confidence.

Be Honest and Transparent

When filling out your application and speaking with lenders, always be honest about your past repossession. Trying to hide it will only lead to distrust and likely a denial.

Lenders will see it on your credit report anyway. Instead, be prepared to explain the circumstances surrounding the repossession and highlight how you’ve improved your financial situation since then.

This transparency builds credibility and shows that you are taking responsibility for your past and are committed to a better financial future.

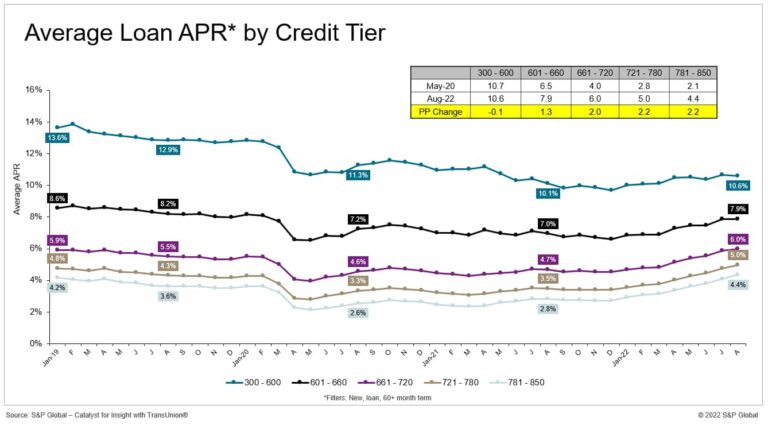

Expect Higher Interest Rates

It’s a reality that with a repossession on your credit report, you will likely face higher interest rates than someone with excellent credit. Lenders view you as a higher risk, and the interest rate reflects that.

While it might be discouraging, focus on securing a loan you can afford with payments you can consistently make. Your priority should be getting approved and starting to rebuild your credit.

As you make on-time payments, your credit score will improve, and you may be able to refinance the loan at a lower rate in the future.

Be Prepared for Specific Loan Terms

Lenders might impose specific terms to mitigate their risk. This could include a shorter loan term (meaning higher monthly payments but less interest paid overall), a higher down payment requirement, or even a requirement for GPS tracking on the vehicle.

Understand all the terms and conditions before you sign. Ensure you are comfortable with the monthly payment and any other stipulations. Don’t rush into a deal you’ll regret later.

Focus on the total cost of the loan and your ability to make consistent payments rather than just the monthly payment amount in isolation.

Negotiating

Even with bad credit, there might be some room for negotiation, especially if you’ve prepared well with a strong down payment or a co-signer. Don’t be afraid to ask questions and discuss the terms.

Compare offers from different lenders if you have them. This can give you leverage to negotiate on interest rates or specific loan terms.

However, understand that your negotiation power will be limited compared to someone with excellent credit. Your primary goal is to secure a manageable loan that allows you to rebuild.

Pro Tips from an Expert Blogger

Navigating the world of auto loans after a repossession requires a blend of persistence, knowledge, and strategic planning. Here are some insights based on my experience helping countless individuals get back on their feet.

Based on my experience, the single most important thing you can do is demonstrate stability. Lenders want to see consistent employment, a steady income, and a clear plan for making your payments. Don’t just apply; present yourself as a responsible borrower who has learned from past mistakes.

Pro tips from us: Always start by knowing your credit report inside and out. Then, save up the largest down payment you possibly can. These two steps alone will dramatically increase your chances of approval and potentially secure better terms than you might otherwise receive. If a co-signer is an option, ensure it’s someone with excellent credit who fully understands their commitment.

Common mistakes to avoid are applying to too many lenders at once, which can further damage your credit with multiple hard inquiries. Also, resist the temptation to buy more car than you can truly afford. Start with a reliable, affordable used car that allows you to make consistent payments, proving your creditworthiness. Don’t forget to factor in insurance, which can be significantly higher with a poor credit score.

Rebuilding Your Credit with Your New Car Loan

Securing a car loan after a repossession isn’t just about getting a vehicle; it’s a golden opportunity to rebuild your credit and demonstrate financial responsibility.

Make every single payment on time, every month. This consistent positive payment history will slowly but surely start to repair your credit score. Payment history is the most heavily weighted factor in credit scoring models.

Keep the car for the full loan term, or at least for a significant period. Refinancing too early or selling the car before the loan is paid off might not allow enough time for the positive impact to fully materialize.

This new auto loan can be a powerful tool for a fresh financial start. As your credit score improves, you’ll gain access to better financial products and opportunities in the future.

Alternative Transportation Solutions (If a Loan Isn’t Possible Yet)

Sometimes, despite your best efforts, getting an affordable car loan immediately after a repossession might not be feasible. If you find yourself in this situation, don’t despair. There are alternative transportation solutions.

Consider public transportation, ride-sharing services, or carpooling with colleagues or neighbors. These options can help you get to work and run errands while you continue to save and improve your credit.

Another option is to save up enough cash to purchase a very inexpensive, reliable used car outright. While it might not be your dream car, it provides immediate transportation without incurring new debt and allows you to continue building your savings for a future, better vehicle purchase.

Conclusion

A car repossession can be a significant setback, but it is by no means the end of your journey toward vehicle ownership. While challenging, you can still get a car loan with a repossession on your record through diligent preparation, a strategic approach, and a commitment to financial responsibility.

By understanding the impact of repossession, proactively improving your credit, saving for a substantial down payment, and targeting the right lenders, you significantly increase your chances of approval. Remember to be honest, manage your expectations regarding interest rates, and use this opportunity to rebuild your credit.

Getting back on the road after a repossession is a testament to your resilience and commitment to financial health. Start today by reviewing your credit, making a budget, and taking those crucial steps toward securing your next vehicle. Your path to financial recovery begins now.