Can You Still Get A Car Loan With Bad Credit? Your Definitive Guide to Driving Away with Confidence

Can You Still Get A Car Loan With Bad Credit? Your Definitive Guide to Driving Away with Confidence Carloan.Guidemechanic.com

The dream of owning a car, or simply needing reliable transportation, often clashes with the reality of a less-than-perfect credit score. Many people find themselves asking, "Can you still get a car loan with bad credit?" It’s a common and valid concern, filled with anxiety and uncertainty.

The short answer is a resounding yes, it is absolutely possible to secure a car loan even with bad credit. However, it requires a strategic approach, a clear understanding of the lending landscape, and a commitment to demonstrating your reliability. This isn’t just about finding any loan; it’s about finding the right loan for your situation, one that helps you, rather than hinders your financial recovery.

Can You Still Get A Car Loan With Bad Credit? Your Definitive Guide to Driving Away with Confidence

As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing. Based on my experience, navigating the bad credit car loan market can feel like a minefield. But with the right knowledge and preparation, you can successfully drive off the lot. This comprehensive guide will arm you with everything you need to know, transforming apprehension into empowerment. We’ll explore your options, demystify the process, and provide actionable steps to secure a car loan that fits your budget and helps rebuild your financial future.

The Reality of Bad Credit Car Loans: Addressing the Elephant in the Room

Let’s start by defining what "bad credit" typically means in the eyes of an auto lender. While there’s no universal cutoff, credit scores are generally categorized. A FICO score, for instance, typically considers anything below 600-620 as "subprime" or "bad credit."

This score is a numerical representation of your creditworthiness, reflecting your payment history, outstanding debts, credit length, and new credit applications. A lower score signals higher risk to lenders, making them more hesitant to approve loans, or leading them to offer less favorable terms.

Why Lenders Are Hesitant: Understanding the Risk

From a lender’s perspective, a low credit score indicates a higher probability of default. They see a history of missed payments, high debt, or past bankruptcies, which suggests you might struggle to repay a new loan. This isn’t personal; it’s purely a risk assessment based on statistical data.

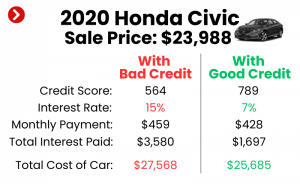

Because of this perceived risk, lenders often compensate by offering loans with higher interest rates. This helps them offset the potential losses if a borrower defaults. It’s a crucial point to understand: while you can get a loan, it will likely come with a higher price tag.

The Myth of "Guaranteed Approval" Car Loans

One common mistake to avoid is falling for advertisements promising "guaranteed car loan approval for bad credit" or "no credit check car loans." Based on my experience, these offers are often too good to be true and can lead to predatory lending situations. Reputable lenders always perform some level of credit assessment, even if it’s a "soft pull" that doesn’t impact your score.

While some "buy here, pay here" dealerships might seem to offer guaranteed approval, they often come with extremely high interest rates, unfavorable terms, and may not report to credit bureaus, thus doing little to improve your credit score. Always approach such claims with extreme caution and skepticism.

Your Options Aren’t Gone: Types of Bad Credit Car Loans

Even with a low credit score, you have several avenues to explore for securing an auto loan. Understanding these options is your first step toward finding the best fit. Each type comes with its own set of advantages and considerations.

1. Subprime Auto Loans

These are loans specifically designed for individuals with poor credit histories. Many lenders specialize in this market, understanding that people sometimes face financial setbacks. While accessible, subprime auto loans typically come with higher interest rates compared to standard loans.

The key benefit here is access to financing when traditional banks might turn you away. Moreover, consistently making on-time payments on a subprime loan can actually help rebuild your credit score over time, opening doors to better rates in the future. It’s a stepping stone, not a permanent solution.

2. Buy Here, Pay Here (BHPH) Dealerships

BHPH dealerships finance the car themselves, rather than through a third-party lender. This can be appealing because their approval process is often less stringent, focusing more on your income stability than your credit score. They often cater specifically to those with bad credit or no credit.

However, pro tips from us: be extremely cautious with BHPH dealers. They often charge significantly higher interest rates, and the vehicles might be older with higher mileage, potentially leading to more maintenance issues. Furthermore, not all BHPH dealers report payments to credit bureaus, meaning your timely payments might not help improve your score. Always ask about their reporting practices.

3. Credit Unions

Credit unions are member-owned financial institutions that often have more flexible lending criteria than traditional banks. Because they are non-profit, they sometimes offer more competitive rates and personalized service, even for borrowers with less-than-perfect credit.

If you’re a member of a credit union, or eligible to join one, it’s always worth checking their auto loan options. Their focus on member welfare can sometimes translate into a more understanding approach to your credit situation.

4. Co-Signers

Having a co-signer with good credit can significantly increase your chances of approval and help you secure a better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default. This reduces the risk for the lender.

While a co-signer can be a huge help, it’s crucial to understand the implications for them. If you miss payments, their credit score will also be negatively affected. It’s a serious financial commitment for both parties and should only be pursued with someone you trust implicitly and after thorough discussion.

5. Joint Applications

Similar to a co-signer, a joint application involves applying for the loan with another individual, typically a spouse or partner. Both applicants are equally responsible for the loan, and the lender will consider both credit histories and incomes. If the other applicant has good credit and stable income, it can bolster your application.

This option works best when both individuals are committed to the vehicle and the repayment. It offers a shared responsibility that can be advantageous for securing better loan terms.

Preparing for Success: What Lenders Look For (Beyond Just Your Credit Score)

While your credit score is a major factor, it’s not the only piece of the puzzle. Lenders specializing in bad credit car loans look at a holistic picture to assess your ability to repay. Understanding these additional factors and preparing them can significantly improve your chances.

1. Income Stability and Proof of Employment

Lenders want to see that you have a consistent and reliable source of income. This demonstrates your capacity to make regular monthly payments. They will typically ask for proof of employment, such as recent pay stubs, W-2 forms, or bank statements showing direct deposits.

The longer you’ve been at your current job, the better. This signals stability. If you’re self-employed, be prepared to provide tax returns and bank statements to prove your income over a longer period.

2. The Power of a Down Payment

Making a significant down payment is one of the most effective ways to improve your chances of approval and secure better loan terms. A down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It also shows your commitment to the purchase.

Based on my experience, even 10-20% down can make a substantial difference. It reduces your monthly payments, lessens the total interest paid over the life of the loan, and can even help you avoid being "upside down" on your loan (owing more than the car is worth) early on.

3. Debt-to-Income Ratio (DTI)

Your Debt-to-Income (DTI) ratio is a critical metric lenders use. It compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A lower DTI indicates that you have more disposable income available to cover your new car payment, making you a less risky borrower.

Lenders generally prefer a DTI below 43%, though some subprime lenders might go higher. Pro tips from us: before applying, try to pay down other debts to improve this ratio. This shows financial responsibility and improves your borrowing capacity.

4. Payment History on Other Debts

Even with a low credit score, a recent history of consistent, on-time payments on other accounts (like rent, utilities, or small personal loans) can work in your favor. This demonstrates a current commitment to financial obligations, despite past credit issues.

Lenders might look for recent positive payment trends. If you’ve been diligently paying bills for the last 6-12 months, highlight this to your potential lender. It shows you’re actively working to improve your financial habits.

5. Realistic Vehicle Choice

When you have bad credit, aiming for a brand-new luxury vehicle is often unrealistic. Lenders prefer to see you choose a reliable, moderately priced used car. This is because the loan amount will be lower, and the car will likely depreciate less rapidly than a new one.

Focus on a vehicle that meets your needs without stretching your budget. A more modest choice signals financial prudence to the lender and increases your likelihood of approval.

A Step-by-Step Guide to Getting Your Car Loan with Bad Credit

Navigating the car loan process with bad credit requires a methodical approach. Follow these steps to maximize your chances of success and secure a loan that works for you.

Step 1: Check Your Credit Report and Score

Before you do anything else, obtain copies of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and check your credit score. You can get free annual reports from AnnualCreditReport.com.

Carefully review each report for errors. Disputing inaccuracies can potentially boost your score. Knowing your score upfront also helps you understand where you stand and manage your expectations. It’s the foundation of your entire strategy.

Step 2: Determine Your Budget

Don’t just think about the monthly car payment. Factor in insurance, fuel, maintenance, and potential repair costs. Use an online car loan calculator to estimate payments at various interest rates and loan terms.

Pro tips from us: aim for a total car cost (payment, insurance, fuel) that doesn’t exceed 10-15% of your take-home pay. This ensures the car remains affordable and doesn’t strain your finances further.

Step 3: Save for a Down Payment

As discussed, a down payment is your secret weapon. The more you can put down, the better your chances of approval and the more favorable your loan terms will be. It significantly reduces the lender’s risk.

Consider delaying your car purchase for a few months if it means you can save up a substantial down payment. This patience often pays off in the long run through lower interest and better terms.

Step 4: Gather Necessary Documents

Being prepared shows responsibility and streamlines the application process. Have these documents ready:

- Proof of income (pay stubs, W-2s, tax returns for self-employed)

- Proof of residency (utility bill, lease agreement)

- Driver’s license

- Proof of insurance (you’ll need this before driving off the lot)

- References (sometimes required)

- Trade-in title (if applicable)

Step 5: Explore Your Lender Options

Don’t limit yourself to the first place you find. Shop around!

- Online Lenders: Many online lenders specialize in bad credit auto loans and can offer quick pre-approvals.

- Credit Unions: As mentioned, they can be more flexible.

- Dealerships: Most dealerships work with multiple lenders, including subprime lenders.

- Traditional Banks: While less likely to approve a direct loan with bad credit, it’s worth checking if you have an existing relationship.

Step 6: Get Pre-Approved (Soft Pull)

Seek pre-approval from a few lenders. Many offer pre-qualification processes that involve a "soft credit pull," which won’t impact your credit score. This gives you an idea of the loan amount and interest rate you might qualify for.

Pre-approval strengthens your negotiating position at the dealership, as you’ll know your borrowing power beforehand. Aim to get all your pre-approvals within a 14-day window to minimize the impact of multiple hard inquiries on your credit score.

Step 7: Choose the Right Vehicle

With your pre-approval in hand and a clear budget, select a vehicle that aligns with your financial reality. Focus on reliability and affordability. A pre-owned certified vehicle can be a good compromise, offering a warranty and peace of mind.

Remember, the goal is not just to get a car, but to get a car that you can comfortably afford, allowing you to make payments on time and improve your credit.

Step 8: Negotiate Smartly

When at the dealership, focus on the out-the-door price of the vehicle, not just the monthly payment. Dealerships often try to distract you with low monthly payments, which can hide high interest rates or extended loan terms.

Pro tips from us: negotiate the car price first, then discuss your financing options. If you have a pre-approval, use it as leverage to see if the dealership can beat the rate. Be prepared to walk away if the terms aren’t favorable.

Understanding the Terms: What to Expect with a Bad Credit Loan

Securing a car loan with bad credit often comes with specific terms that differ from those offered to borrowers with excellent credit. It’s crucial to understand these aspects fully.

Higher Interest Rates

This is the most significant difference. Because you represent a higher risk, lenders charge more for the money they lend you. Expect interest rates that could be significantly higher than the national average for auto loans.

While unavoidable, understand that these higher rates are often temporary. By consistently making on-time payments, you can improve your credit score and potentially refinance to a lower rate in the future.

Shorter vs. Longer Loan Terms

Lenders might offer shorter loan terms (e.g., 36-48 months) to reduce their risk. This means higher monthly payments but less total interest paid over the life of the loan. Conversely, some lenders might push for longer terms (e.g., 60-72 months) to make monthly payments seem more affordable.

While longer terms mean lower monthly payments, you’ll pay significantly more in interest over time. Common mistakes to avoid are extending the loan term too much just to get a lower monthly payment. This can lead to being "upside down" on your loan for a longer period.

Potential for Additional Fees

Be vigilant for additional fees that can inflate the total cost of your loan. These might include origination fees, document fees, or charges for optional add-ons like extended warranties or GAP insurance (which can be beneficial but should be purchased knowingly).

Always ask for a complete breakdown of all costs and fees. Don’t be afraid to question anything you don’t understand or feel is unnecessary.

Importance of Reading the Fine Print

Every loan agreement has fine print for a reason. Before signing anything, read the entire contract carefully. Understand all the terms, conditions, penalties for late payments, and prepayment clauses.

If you have any questions, ask for clarification. Don’t feel rushed or pressured. It’s your financial commitment, and you have the right to understand every detail.

The Long Game: Improving Your Credit and Refinancing

Getting a bad credit car loan isn’t just about driving a new vehicle; it’s a powerful opportunity to rebuild your financial standing. This loan can be a stepping stone to a healthier credit score.

How a Bad Credit Car Loan Can Help Your Credit

When you consistently make your car loan payments on time, every single month, this positive activity is reported to the credit bureaus. Over time, this builds a strong history of responsible borrowing, which is a major factor in your credit score calculation. It demonstrates to future lenders that you can manage a significant debt reliably.

This positive payment history can gradually increase your credit score, making it easier to qualify for other loans or credit cards with better terms in the future. It’s an investment in your financial future.

Strategies for Credit Improvement

Beyond your car loan, actively work on improving your overall credit health:

- Pay all bills on time: This is the most critical factor.

- Reduce other debts: Especially high-interest credit card debt.

- Keep old accounts open: A longer credit history is generally better.

- Avoid new credit applications: Limit hard inquiries.

- Monitor your credit report regularly: Catch errors and identity theft early.

For more in-depth strategies, you might find helpful.

Refinancing: When and How to Do It

Once you’ve made 6-12 months of on-time payments on your bad credit car loan, and your credit score has shown improvement, consider refinancing. Refinancing means taking out a new loan, typically with a lower interest rate, to pay off your existing car loan.

This can significantly reduce your monthly payment and the total interest you’ll pay over the life of the loan. Shop around for refinance options, just as you did for your initial loan. Look for lenders who specialize in refinancing or credit unions. Understanding car loan interest rates is key, so check out for more details.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating the bad credit auto loan market can be tricky, and pitfalls abound. Avoiding these common mistakes can save you significant money and stress.

1. Not Checking Your Credit Report

Failing to review your credit report for errors before applying is a major oversight. Incorrect information can unfairly lower your score and lead to higher interest rates or even loan denial. Pro tips from us: always dispute any discrepancies you find immediately.

2. Applying Everywhere (Multiple Hard Inquiries)

Each time you apply for credit, a "hard inquiry" is recorded on your credit report. Too many hard inquiries in a short period can lower your score further. While credit scoring models group auto loan inquiries within a specific window (usually 14-45 days) to count as one, spreading your applications out too much can be detrimental.

Focus your applications on a few carefully chosen lenders after thorough research.

3. Buying More Car Than You Can Afford

It’s easy to get excited and fall in love with a car outside your budget. However, overextending yourself financially can lead to missed payments, repossession, and further damage to your credit. This is a common mistake people make, driven by emotion rather than financial prudence.

Stick to your budget, even if it means opting for a less glamorous but equally reliable vehicle.

4. Ignoring the Total Cost of the Loan

Focusing solely on the monthly payment is a dangerous trap. A low monthly payment might mean a longer loan term and a much higher total interest paid. Always calculate the total cost of the loan (principal + total interest + fees) before signing.

A slightly higher monthly payment over a shorter term can often save you thousands in the long run.

5. Falling for "Guaranteed Approval" Scams

As mentioned earlier, legitimate lenders do not "guarantee" approval without some form of credit assessment. Be wary of any offer that sounds too good to be true, especially those that pressure you into signing quickly without full disclosure of terms. These often hide exorbitant rates or unfavorable conditions.

Always verify the lender’s legitimacy and read reviews before proceeding. For more information on what affects your credit score, you can consult reliable sources like Experian: .

Conclusion: Your Journey to Driving with Confidence

The question "Can you still get a car loan with bad credit?" is not just about possibility, but about strategy, resilience, and informed decision-making. The answer, unequivocally, is yes. However, it requires you to be an active and educated participant in the process.

You now understand that securing a car loan with bad credit involves more than just filling out an application. It means preparing your finances, understanding what lenders truly look for, exploring all your options, and being a savvy negotiator. More importantly, it’s about recognizing that this loan isn’t just a means to an end; it’s an opportunity to build a stronger financial future.

By diligently making your payments, you can transform a bad credit car loan into a powerful tool for credit rebuilding. Take these steps, arm yourself with knowledge, and approach the process with confidence. Your journey to reliable transportation and improved financial health starts now. Drive smart, drive informed, and drive towards a brighter financial future.