Can You Take Out A Personal Loan For A Car? The Ultimate Guide To Financing Your Ride

Can You Take Out A Personal Loan For A Car? The Ultimate Guide To Financing Your Ride Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and for many, securing the right financing is a crucial step. While traditional auto loans are the go-to option, you might be wondering: "Can you take out a personal loan for a car?" The short answer is yes, absolutely. A personal loan can be a flexible and sometimes advantageous way to finance your next vehicle, but it comes with its own set of unique considerations.

In this comprehensive guide, we’ll dive deep into everything you need to know about using a personal loan for a car purchase. We’ll explore the pros and cons, compare it to auto loans, discuss eligibility, outline the application process, and share expert tips to help you make an informed decision. Our goal is to equip you with all the knowledge to navigate this financing path confidently and drive away with a deal that truly works for you.

Can You Take Out A Personal Loan For A Car? The Ultimate Guide To Financing Your Ride

Understanding Personal Loans for Car Purchases

Before we dissect the "how-to," let’s clarify what a personal loan truly is in the context of buying a car. Unlike an auto loan, which is specifically designed for vehicle purchases and uses the car itself as collateral, a personal loan is typically an unsecured loan. This means it doesn’t require any collateral.

Lenders provide you with a lump sum of money, which you then repay in fixed monthly installments over a set period, usually with interest. The beauty of a personal loan is its versatility; once approved, you can use the funds for almost any purpose, including buying a car. This flexibility is a major reason why many people consider it.

When you secure a personal loan for a car, you essentially become a cash buyer at the dealership or from a private seller. This can give you significant leverage in negotiations, as you’re not tied to the dealer’s financing options. You receive the funds, pay the seller directly, and the car’s title is immediately in your name, without a lien from the lender.

The Pros of Using a Personal Loan for Your Car

Opting for a personal loan to finance your car comes with several distinct advantages that might make it a more attractive option for certain buyers. Let’s explore these benefits in detail.

Flexibility in Use

One of the most significant advantages of a personal loan is its incredible flexibility. Unlike an auto loan, which is strictly for the vehicle purchase, a personal loan allows you to use the funds for more than just the car’s sticker price. You could, for instance, roll in the cost of registration, taxes, initial insurance premiums, or even essential accessories like new tires or an advanced audio system.

This means you won’t have to scramble for extra cash to cover these immediate post-purchase expenses. It simplifies your financial planning by consolidating various car-related costs into a single, manageable loan payment. This level of financial freedom is rarely found with traditional auto financing.

No Collateral Required

Most personal loans are unsecured, meaning you don’t have to put up any asset, like your home or the car itself, as collateral. This can be a huge relief for many borrowers. In the unfortunate event that you struggle to make payments, the lender cannot seize your vehicle directly as they would with a secured auto loan.

While defaulting on any loan has serious consequences for your credit, the lack of collateral with a personal loan offers a degree of protection. It means you retain full ownership of your car from day one, without the lender having a claim on its title. This aspect provides peace of mind for some car buyers.

Immediate Car Title Ownership

When you use a personal loan to buy a car, you effectively become a cash buyer. This means the car’s title will be issued directly in your name without a lien holder listed. With a traditional auto loan, the lender holds the title or places a lien on it until the loan is fully repaid.

Owning the title outright from the start gives you greater control over your vehicle. You can sell it, trade it in, or modify it without needing permission from a lender. This streamlined ownership process can be particularly appealing if you value immediate autonomy over your assets.

Easier for Private Party Sales

Buying a car from a private seller can often result in a better deal than purchasing from a dealership. However, financing a private party sale with a traditional auto loan can be complicated, as many auto lenders prefer to work with established dealerships. This is where a personal loan shines.

Since you receive the cash upfront, you can simply pay the private seller directly, just as you would with cash. This eliminates the complex paperwork and verification processes often associated with auto loans for private sales. Based on my experience, this makes the entire transaction much smoother and faster for both parties involved.

Potential for Faster Funding

Many online personal loan lenders pride themselves on their quick application and funding processes. It’s not uncommon to apply for a personal loan and receive the funds in your bank account within one to two business days, sometimes even faster. This speed can be incredibly beneficial if you’ve found the perfect car and need to act quickly to secure it.

Traditional auto loans, especially through dealerships, can sometimes involve more extensive paperwork and a longer approval process. If time is of the essence, a personal loan can provide the rapid access to funds you need to seal the deal on your new ride without delay.

The Cons and Potential Pitfalls

While personal loans offer attractive benefits for car purchases, they also come with significant drawbacks that warrant careful consideration. Understanding these potential pitfalls is crucial to making a wise financial decision.

Higher Interest Rates

Perhaps the most significant downside of using a personal loan for a car is the typically higher interest rate compared to a traditional auto loan. Auto loans are secured by the vehicle itself, which reduces the risk for the lender. As a result, lenders are usually willing to offer lower interest rates on auto loans.

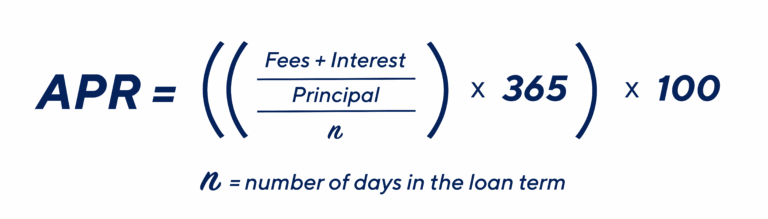

Personal loans, being unsecured, carry more risk for the lender. To compensate for this increased risk, lenders often charge higher interest rates. This means you could end up paying significantly more over the life of the loan, increasing the total cost of your car. Pro tips from us: Always compare the Annual Percentage Rate (APR) across different loan types and lenders, not just the advertised interest rate.

Stricter Eligibility for Good Rates

While personal loans are available to a broad range of borrowers, securing a personal loan with a competitive interest rate usually requires an excellent credit score. Lenders rely heavily on your creditworthiness to assess risk when there’s no collateral. If your credit score is average or below, you might still qualify for a personal loan, but the interest rates could be prohibitively high, making the car purchase much more expensive.

This can be a challenge for those who might struggle to qualify for an auto loan due to credit issues, as a personal loan might not offer a better alternative in terms of cost. Your financial profile plays a critical role in the terms you’ll be offered.

Shorter Repayment Terms

Personal loans often come with shorter repayment terms than auto loans. While auto loans can stretch for 60, 72, or even 84 months, personal loan terms typically range from 24 to 60 months. A shorter repayment period means higher monthly payments, even if the total interest paid is less.

This can put a strain on your monthly budget, especially if you’re already managing other financial commitments. It’s essential to ensure that the higher monthly payment is comfortably affordable within your budget to avoid financial stress or, worse, defaulting on the loan.

Impact on Credit Score

Applying for any loan typically involves a "hard inquiry" on your credit report, which can temporarily ding your credit score by a few points. While this is normal, multiple hard inquiries in a short period can have a more noticeable impact. Furthermore, taking on a new personal loan increases your overall debt, which can affect your debt-to-income ratio.

If you already have a high debt burden, adding a new personal loan could make it harder to qualify for other credit in the future. However, if managed responsibly with on-time payments, a personal loan can actually help improve your credit score over time.

Common Mistakes to Avoid

- Not Comparing Offers: Don’t just take the first loan offer you receive. Always shop around and compare rates, terms, and fees from multiple lenders.

- Borrowing Too Much: Only borrow what you genuinely need for the car and immediate related expenses. Over-borrowing can lead to unnecessary debt and higher interest costs.

- Ignoring the Fine Print: Always read the loan agreement thoroughly. Understand all fees, prepayment penalties (if any), and late payment charges.

- Overlooking Your Budget: Ensure the monthly payment fits comfortably within your budget, considering all your other expenses. A loan should not put you in financial distress.

Auto Loan vs. Personal Loan: A Detailed Comparison

Deciding between an auto loan and a personal loan for your car purchase requires a clear understanding of their fundamental differences. Here’s a detailed comparison to help you weigh your options:

| Feature | Traditional Auto Loan | Personal Loan (for a car) |

|---|---|---|

| Purpose | Exclusively for purchasing a vehicle | Versatile; funds can be used for any purpose, including a car |

| Collateral | Secured by the vehicle you are purchasing | Typically unsecured (no collateral required) |

| Interest Rates | Generally lower due to being secured | Generally higher due due to being unsecured |

| Ownership | Lender holds a lien on the title until loan is paid | Borrower holds the title outright from day one |

| Loan Term | Often longer (e.g., 60-84 months) | Typically shorter (e.g., 24-60 months) |

| Approval Ease | Can be easier to qualify for, especially with fair credit, due to collateral | Requires good to excellent credit for competitive rates |

| Flexibility | Limited to the car’s purchase price | Funds can cover other car-related expenses, registration, etc. |

| Private Sales | Can be more complex to arrange | Ideal for private party purchases; you pay cash |

When is an Auto Loan Better?

An auto loan is generally better if you prioritize lower interest rates and longer repayment terms to keep monthly payments down. It’s also often more accessible for those with less-than-perfect credit because the collateral reduces lender risk. If you’re comfortable with the lender holding a lien on your car until it’s paid off, an auto loan is usually the more cost-effective option for financing a vehicle.

When is a Personal Loan Better?

A personal loan might be the superior choice if you value immediate car title ownership, need flexibility to cover additional car-related expenses (like taxes or insurance), or are buying from a private seller. It’s also a strong contender if you have an excellent credit score, which can help you secure a competitive rate, or if you prefer an unsecured loan without collateral. If you can comfortably afford the potentially higher monthly payments that come with shorter terms, a personal loan offers unique advantages.

Who is a Personal Loan For A Car Best Suited For?

While a personal loan can be used by anyone to buy a car, it’s particularly well-suited for specific individuals and situations. Understanding if you fit this profile can help you determine if it’s the right financing path for you.

Buyers with Excellent Credit

If you boast an excellent credit score (typically 740 and above), you are in the best position to secure a personal loan with a competitive interest rate. Lenders view high-credit borrowers as low risk, making them eligible for the most favorable terms. For these individuals, the interest rate difference between a personal loan and an auto loan might be minimal, making the flexibility of a personal loan very attractive.

Those Buying From Private Sellers

As we’ve discussed, financing a private party car purchase with a traditional auto loan can be cumbersome. A personal loan solves this problem entirely. It allows you to become a cash buyer, making the transaction straightforward for both you and the seller. This opens up a wider market of vehicles, often at better prices than dealerships.

Individuals Needing Flexibility for Additional Car-Related Expenses

If you anticipate needing extra funds beyond the car’s purchase price for things like immediate repairs, registration fees, or insurance, a personal loan offers unmatched flexibility. You receive a lump sum that you can allocate as needed, consolidating all your car-related costs into a single loan. This prevents the need for multiple small loans or dipping into savings for these incidental expenses.

People Who Want Immediate Car Title Ownership

For some, the idea of owning their car outright from day one, without a lien on the title, is a significant draw. A personal loan provides this immediate ownership, giving you full control over your vehicle. You can sell, trade, or modify your car without any lender restrictions, offering a sense of autonomy that a traditional auto loan doesn’t.

Eligibility Requirements for a Personal Loan

To qualify for a personal loan, lenders typically assess a range of factors to determine your creditworthiness and ability to repay the loan. Understanding these requirements is key to a successful application.

Credit Score

Your credit score is arguably the most critical factor. Lenders use it as a snapshot of your financial reliability.

- Excellent Credit (740+): You’ll have the best chance of approval with the lowest interest rates.

- Good Credit (670-739): You’ll likely qualify, but rates might be slightly higher.

- Fair Credit (580-669): Approval is possible, but expect higher interest rates. Some lenders specialize in this range.

- Poor Credit (below 580): It will be challenging to get approved for an unsecured personal loan at a reasonable rate. You might need a co-signer or a secured personal loan option.

Income and Employment Stability

Lenders want to see that you have a stable and sufficient income to comfortably make your monthly loan payments. They typically look for:

- Steady Employment: A consistent work history, often for at least one to two years, demonstrates reliability.

- Sufficient Income: Your income must be high enough to cover your living expenses plus the new loan payment. Lenders often have minimum income requirements.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, generally 36% or less, though some may go up to 43%. A high DTI indicates that you might be overextended financially, making it riskier to take on new debt. Keeping this ratio in check is crucial for approval.

Other Factors

- Age: You must be at least 18 years old (19 in some states) to enter into a loan agreement.

- Residency: Lenders typically require you to be a U.S. citizen or permanent resident with a valid Social Security number.

- Banking History: A stable banking history, without frequent overdrafts or bounced checks, can also be a positive factor.

Pro tips from us for improving your eligibility:

Before applying, take steps to improve your credit score. This could include paying down existing debts, disputing errors on your credit report, and making all payments on time. We have a detailed guide on this topic; you can read more about to boost your chances of approval and secure better rates.

The Application Process: Step-by-Step

Applying for a personal loan can be a straightforward process if you’re prepared. Here’s a step-by-step guide to help you navigate it.

1. Assess Your Needs and Budget

Before you even look at cars or lenders, determine how much you truly need to borrow and what you can realistically afford for a monthly payment. Factor in the car’s price, potential taxes, registration fees, and any immediate maintenance or insurance costs. Use an online loan calculator to see how different loan amounts and interest rates affect your monthly payment.

2. Check Your Credit Score

Knowing your credit score upfront is vital. It gives you an idea of what interest rates you might qualify for and allows you to address any inaccuracies on your report. You can get free copies of your credit report from AnnualCreditReport.com. Many credit card companies and banks also offer free credit score access.

3. Shop Around for Lenders

Don’t settle for the first offer. Explore options from various financial institutions:

- Banks: Traditional banks often offer personal loans to existing customers.

- Credit Unions: Known for competitive rates and personalized service, especially for members.

- Online Lenders: Many online platforms specialize in personal loans, offering quick approvals and funding. They often have competitive rates and user-friendly application processes.

Many lenders offer a "pre-qualification" option, which involves a soft credit inquiry and won’t harm your credit score. This allows you to compare potential rates without commitment.

4. Gather Required Documents

Once you’ve narrowed down your lender choices, start gathering the necessary documentation. This typically includes:

- Government-issued ID (driver’s license, passport).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residency (utility bill, lease agreement).

- Social Security number.

- Bank account information for fund disbursement.

Having these ready will expedite the application process.

5. Submit Your Application

Complete the lender’s application form accurately and thoroughly. This is where the hard credit inquiry typically occurs. Be prepared to answer questions about your employment, income, existing debts, and housing situation.

6. Review Offers

If approved, the lender will present you with a loan offer outlining the principal amount, interest rate (APR), loan term, and monthly payment. Carefully review all the terms and conditions. Pay close attention to any fees, such as origination fees or prepayment penalties.

7. Accept and Receive Funds

If you’re satisfied with the offer, sign the loan agreement. The funds will then be disbursed to your bank account, usually within one to five business days. Once the money is in your account, you can proceed to purchase your car as a cash buyer.

Pro tips from us: Get pre-approved before you start car shopping. This gives you a clear budget and allows you to negotiate with confidence. Always read the fine print; understanding every clause can save you from unexpected costs later.

Making Your Decision: Key Factors to Consider

Choosing the right personal loan for your car requires a thorough evaluation of several critical factors. Don’t rush this stage; it could save you a significant amount of money and stress in the long run.

Interest Rates and APR

This is arguably the most important factor. The interest rate determines how much extra you’ll pay on top of the principal loan amount. However, always look at the Annual Percentage Rate (APR), which includes the interest rate plus any additional fees (like origination fees) charged by the lender. A lower APR means a lower total cost of borrowing. Even a difference of one or two percentage points can translate into hundreds or thousands of dollars saved over the life of the loan. For more insights on this, refer to our article on .

Loan Terms and Monthly Payments

The loan term is the length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms result in lower monthly payments but more interest over time. Find a balance that fits comfortably within your monthly budget without extending the loan unnecessarily. Calculate your monthly payment with different terms to see the impact.

Fees

Be aware of any fees associated with the personal loan. Common fees include:

- Origination Fees: A percentage of the loan amount charged by the lender for processing the loan.

- Late Payment Fees: Charged if you miss a payment deadline.

- Prepayment Penalties: Some lenders charge a fee if you pay off your loan early, though this is less common with personal loans than with other types of loans.

- Administrative Fees: Less common but always check.

Ideally, look for loans with no origination fees or prepayment penalties to maximize your savings.

Lender Reputation and Customer Service

Research the lender’s reputation. Read reviews, check their Better Business Bureau rating, and see how they handle customer inquiries and complaints. A reputable lender with excellent customer service can make a significant difference if you encounter any issues during your loan term. Trustworthiness and transparency are paramount when dealing with financial institutions.

Your Overall Financial Situation

Finally, consider your entire financial picture. Do you have other significant debts? Is your job stable? Do you have an emergency fund? Taking on a new loan, even for a car, should not jeopardize your financial stability. Ensure the new monthly payment fits comfortably into your budget, leaving room for savings and unexpected expenses. Never borrow more than you can realistically afford to repay.

Alternatives to Personal Loans for Car Financing

While a personal loan is a viable option, it’s not the only way to finance a car. Exploring alternatives can help you determine the best fit for your specific needs and financial situation.

Traditional Auto Loans

This is the most common method of financing a car. Auto loans are secured by the vehicle itself, meaning the car acts as collateral.

- Pros: Generally lower interest rates, longer repayment terms, and often easier to qualify for than unsecured personal loans, especially for those with average credit.

- Cons: The lender holds a lien on the car’s title until the loan is paid off. Can be more restrictive for private party sales.

Cash Purchase

If you have sufficient savings, buying a car with cash is often the most financially sound option.

- Pros: No interest payments, immediate full ownership, no monthly payments, and potential for better negotiation leverage.

- Cons: Ties up a significant amount of your liquid assets, which might be better used for investments or emergencies.

Leasing

Leasing a car is essentially renting it for a set period, typically 2-4 years, with an option to buy at the end.

- Pros: Lower monthly payments than buying, you always drive a new car, and warranty coverage for the lease term.

- Cons: You don’t own the car, mileage restrictions, potential fees for excessive wear and tear, and you’re always making payments without building equity.

Home Equity Loans/Lines of Credit (HELOC)

If you own a home and have built up equity, you might be able to use a home equity loan or a home equity line of credit (HELOC) to finance a car.

- Pros: Typically lower interest rates than personal loans because they are secured by your home. Interest may be tax-deductible (consult a tax advisor).

- Cons: Your home is used as collateral, putting it at risk if you default. The application process can be lengthy, and closing costs may apply. This option should be approached with extreme caution.

Dealer Financing

Many dealerships offer their own financing options or work with a network of lenders.

- Pros: Convenience (one-stop shop), potential for special promotions (low or 0% APR) for highly qualified buyers.

- Cons: Rates might not always be the most competitive, and you might feel pressured into a deal. Always compare dealer financing with offers from independent lenders.

Pro Tips for Securing the Best Personal Loan for Your Car

Based on my experience in the financial landscape, navigating personal loans effectively requires strategic planning and careful execution. Here are some pro tips to help you secure the best possible personal loan for your car.

Boost Your Credit Score

This cannot be stressed enough. Your credit score is the single most influential factor in determining your interest rate. Before applying, take steps to improve it. Pay down existing credit card balances, ensure all your bills are paid on time, and check your credit report for any errors. Even a small improvement can lead to significantly better loan terms and save you hundreds, if not thousands, of dollars over the loan’s life.

Shop Around Aggressively

Do not accept the first loan offer you receive. Use online comparison tools and get pre-qualified with multiple lenders – including banks, credit unions, and online platforms. Compare not just the interest rate, but the Annual Percentage Rate (APR), which gives you the true cost of the loan including fees. Different lenders cater to different credit profiles, so shopping around ensures you find the lender offering the most favorable terms for your specific situation.

Consider a Co-signer (If Needed)

If your credit score isn’t stellar, or if you’re just starting to build credit, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer shares responsibility for the loan, so ensure both parties understand the commitment. This can be a powerful strategy, but only if both individuals are fully aware of the implications.

Automate Payments

Once you’ve secured your personal loan, set up automatic payments from your bank account. This ensures you never miss a payment, which protects your credit score and helps you avoid late fees. Consistent on-time payments are crucial for maintaining good financial health and can even improve your credit score over time.

Understand the Total Cost

Look beyond just the monthly payment. Calculate the total amount you will pay over the life of the loan, including all interest and fees. Sometimes, a slightly higher monthly payment with a shorter term can lead to substantial savings on total interest paid. Use online calculators to project the full financial impact of different loan scenarios. Based on my experience, focusing solely on the monthly payment can often lead to overlooking the true cost of borrowing.

Conclusion

So, can you take out a personal loan for a car? Absolutely. It’s a viable financing option that offers unique advantages, particularly for those with excellent credit, buyers looking at private sales, or individuals who value immediate vehicle ownership and financial flexibility. However, it’s imperative to approach this decision with a clear understanding of its potential drawbacks, especially higher interest rates compared to traditional auto loans.

By thoroughly researching, comparing offers, understanding your eligibility, and carefully evaluating your financial situation, you can make an informed choice that aligns with your needs. Remember to leverage our pro tips, such as boosting your credit score and shopping around aggressively, to secure the best possible terms for your personal loan for a car. With the right strategy, you can confidently finance your new ride and hit the road with peace of mind.