Can’t Afford Car Loan Anymore? Your Comprehensive Guide to Regaining Financial Control

Can’t Afford Car Loan Anymore? Your Comprehensive Guide to Regaining Financial Control Carloan.Guidemechanic.com

Finding yourself in a situation where you can no longer afford your car loan payments can feel like hitting a brick wall. The stress, anxiety, and fear of losing your vehicle are very real, and it’s a predicament far more common than many realize. Whether due to an unexpected job loss, a sudden medical emergency, or simply an overzealous car purchase, the feeling of financial strain can be overwhelming.

But here’s the crucial truth: you are not alone, and you have options. This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate this challenging period. We’ll delve deep into understanding your situation, exploring every viable solution, and outlining proactive steps to safeguard your financial future. Our ultimate goal is to help you move from a place of panic to a position of informed action, preventing dire consequences and preserving your financial well-being.

Can’t Afford Car Loan Anymore? Your Comprehensive Guide to Regaining Financial Control

The Alarming Signs: How Did You Get Here?

Before we explore solutions, it’s vital to understand the common culprits behind this financial strain. Recognizing the root cause can help you avoid similar situations in the future and approach your current problem with clarity.

Based on my experience as a financial blogger, most people who struggle with car payments fall into one of several categories. Often, it’s a combination of factors that snowball into an unmanageable situation.

One common scenario is unexpected life changes. This could be a sudden job loss, a significant reduction in income, a major medical expense, or even a costly home repair. These unforeseen events can quickly deplete savings and make regular payments impossible.

Another frequent cause is poor initial budgeting and overspending. Many individuals are enticed by low monthly payments without fully considering the total cost of the loan, including interest, insurance, and maintenance. They might have stretched their budget too thin from the start, leaving no room for error.

Lastly, rising interest rates or variable loan terms can also catch borrowers off guard. While less common with fixed-rate car loans, some personal loans used for car purchases might have variable rates, leading to escalating payments that become unaffordable over time. Understanding these underlying issues is the first step toward effective problem-solving.

Don’t Panic: Your Immediate First Steps

The moment you realize you can’t afford your car loan anymore, your immediate reaction might be fear or avoidance. However, inaction is your biggest enemy here. Taking swift, decisive steps can significantly improve your outcome.

Step 1: Review Your Entire Financial Picture.

Before you do anything else, sit down and meticulously review your income, expenses, and current budget. Create a detailed spreadsheet or use a budgeting app to track every dollar coming in and going out. Identify areas where you can immediately cut back, even temporarily. This clear snapshot of your finances will be invaluable when discussing options with your lender.

Step 2: Understand Your Loan Agreement.

Pull out your original car loan contract and read it carefully. Pay close attention to clauses regarding late payments, default, repossession, and any options for deferment or modification. Knowing the terms of your agreement will help you understand your rights and obligations, and prepare you for discussions with your lender.

Step 3: Contact Your Lender – Immediately!

This is arguably the most crucial step. As soon as you anticipate missing a payment, or have already missed one, reach out to your lender. Do not wait for them to contact you. Proactive communication demonstrates responsibility and a willingness to resolve the issue. Lenders are often more willing to work with borrowers who are upfront and communicative.

Pro tips from us: When you call, be prepared to explain your situation clearly and concisely, and have your financial review (from Step 1) ready. Ask about all available options, and take detailed notes of who you spoke with, the date, and what was discussed.

Exploring Your Options: A Detailed Breakdown

Once you’ve taken the immediate steps, it’s time to delve into the various solutions available. Each option has its own implications, and the best choice for you will depend on your specific financial situation and the terms of your loan.

Option 1: Negotiating with Your Lender

Your lender doesn’t want to repossess your car; it’s a costly and time-consuming process for them. This means there’s often room for negotiation, especially if you reach out early.

A. Loan Deferment or Forbearance:

Many lenders offer temporary relief programs, especially for borrowers facing short-term financial hardships. A deferment allows you to postpone one or more payments, often by adding them to the end of your loan term. Forbearance is similar, temporarily reducing or suspending payments for a set period.

It’s important to understand that interest usually continues to accrue during these periods, so your total cost might increase slightly. This option is ideal if you anticipate your financial situation improving in a few months, such as after a temporary layoff or a short-term medical leave. Always clarify the exact terms, including how interest will be handled and when payments will resume.

B. Loan Modification:

For more long-term financial difficulties, your lender might be willing to modify the terms of your loan. This could involve extending the loan term to lower your monthly payments, or, in some rare cases, adjusting the interest rate.

A loan modification aims to make your payments more manageable on an ongoing basis. However, extending the loan term means you’ll pay more interest over the life of the loan. Carefully weigh the reduced monthly burden against the increased overall cost before agreeing to a modification.

Pro tips from us: When negotiating, always ask for any agreed-upon changes in writing. Don’t rely solely on verbal agreements. Be persistent but polite, and clearly articulate your ability to pay a reduced amount if that’s what you’re proposing.

Option 2: Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan, ideally with better terms. This can be a very effective solution if your credit score has improved since you took out the original loan, or if interest rates have dropped.

A. When Refinancing Makes Sense:

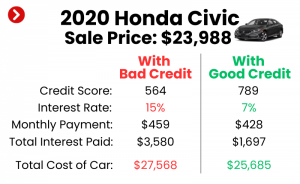

If you have a higher interest rate on your current loan, a good credit score, and stable income, refinancing could significantly lower your monthly payments or reduce the total interest paid over time. It’s also an option if you want to change your loan term, either to extend it for lower payments or shorten it to pay off the car faster.

B. Eligibility Factors:

Lenders will typically look at your credit score, debt-to-income ratio, and the value of your car. If your car is "upside down" (you owe more than it’s worth), refinancing can be more challenging but not impossible, especially if you have excellent credit. Some lenders specialize in these situations.

C. Common Mistakes to Avoid:

Don’t refinance into a loan with a significantly longer term just to get a lower payment if you can avoid it. While it provides immediate relief, you’ll end up paying much more in interest over time. Also, shop around with multiple lenders to ensure you get the best possible rate and terms.

(Internal Link Placeholder: For a deeper dive into refinancing, check out our guide: .)

Option 3: Selling Your Car (with a Loan)

Selling your car, even if you still owe money on it, is a viable option, though it requires careful planning, especially if you have negative equity.

A. If You Have Positive Equity:

If your car is worth more than what you owe on the loan (positive equity), selling it can be straightforward. You sell the car, use the proceeds to pay off the loan, and keep the difference. This can be done through a private sale or by trading it in at a dealership. A private sale typically yields a higher price.

B. If You Have Negative Equity (Upside Down):

This is a more common and challenging scenario. If you owe more on the car than its market value, you’ll need to cover the difference out of pocket when you sell it. For example, if you owe $15,000 but the car is only worth $12,000, you’ll need to come up with $3,000 to satisfy the loan after the sale.

This "deficiency" must be paid to the lender to release the lien on the title. Sometimes, a dealership might roll this negative equity into a new car loan, but this is generally not recommended as it puts you further behind from the start.

Pro tips from us: If you’re upside down, explore options like a small personal loan to cover the deficiency, or save up the difference before selling. Being honest about the situation with potential buyers or dealerships is crucial for a smooth transaction.

Option 4: Voluntary Repossession

Voluntary repossession, also known as a "voluntary surrender," is when you proactively return the vehicle to the lender because you can no longer afford the payments. While it might seem like an easy way out, it’s generally considered a last resort before involuntary repossession.

A. What It Is and Its Process:

You contact your lender, inform them you can’t make payments, and arrange to return the car. They will then sell the vehicle at auction.

B. Pros and Cons:

The "pro" is that it might slightly lessen the negative impact on your credit score compared to an involuntary repossession, as it shows you took responsibility. However, it still severely damages your credit score, typically staying on your report for seven years.

C. Deficiency Balance:

Crucially, if the car sells for less than what you owe on the loan (which is often the case at auction), you will still be responsible for the "deficiency balance" – the difference between the sale price and your outstanding loan amount, plus any fees and collection costs. The lender can pursue you legally to collect this amount. This is a significant risk to be aware of.

Option 5: Debt Consolidation

If your car loan is one of several debts you’re struggling with, debt consolidation might be an option. This involves taking out a new, larger loan (e.g., a personal loan or home equity loan) to pay off multiple smaller debts, including your car loan.

A. When It Might Be Suitable:

Consolidation can simplify your finances by combining multiple payments into one, potentially with a lower overall interest rate if you have excellent credit. It can also free up cash flow if the new loan has a longer term or lower rate.

B. Risks Involved:

The biggest risk is that you might secure the new loan using collateral, like your home (home equity loan). If you default on that loan, you could lose your home, a far more severe consequence than losing your car. Personal loans can also have high interest rates if your credit isn’t stellar. Carefully assess if consolidation truly improves your overall financial standing or just shifts the problem.

Option 6: Legal Assistance or Bankruptcy (Last Resort)

When all other options are exhausted, or if you’re facing overwhelming debt beyond just your car loan, seeking legal advice or considering bankruptcy might be necessary. This should always be a last resort.

A. When to Consider It:

If you’re facing multiple creditors, significant wage garnishments, or simply cannot see a path out of your debt spiral, a bankruptcy attorney can advise you on your options.

B. Types of Bankruptcy and Impact on Car Loans:

- Chapter 7 Bankruptcy (Liquidation): This can discharge (eliminate) certain debts, and potentially allow you to surrender the car without owing a deficiency. However, you might lose other assets.

- Chapter 13 Bankruptcy (Reorganization): This allows you to reorganize your debts into a manageable payment plan over three to five years. You might be able to keep your car under certain conditions, potentially "cramming down" the loan balance to the car’s actual value.

C. Disclaimer: Seek Legal Advice.

Bankruptcy is a complex legal process with long-lasting consequences for your credit and future financial endeavors. It is imperative to consult with a qualified bankruptcy attorney to understand how it specifically applies to your situation. This is not a decision to be made lightly or without professional guidance.

The Consequences of Inaction: Why You MUST Act

Ignoring your car loan problem will not make it disappear. In fact, it will only escalate, leading to increasingly severe consequences that can severely damage your financial health for years to come.

A. Repossession Process:

If you consistently miss payments, your lender will eventually repossess your car. They can do this without a court order in most states once you are in default. This process can be swift and unexpected, leaving you without transportation. After repossession, the car is typically sold at auction.

B. Credit Score Damage:

Late payments, loan defaults, and especially repossessions, are severely damaging to your credit score. A repossession can drop your score by over 100 points and remain on your credit report for up to seven years, making it incredibly difficult to obtain future loans, mortgages, or even rent an apartment.

C. Deficiency Judgments:

As mentioned with voluntary repossession, if your car sells for less than what you owe, you’ll be responsible for the deficiency balance. If you don’t pay this, the lender can sue you and obtain a deficiency judgment, allowing them to garnish your wages or bank accounts. This is a very real threat that many people overlook.

D. Collection Agencies:

If the lender sells the deficiency balance to a collection agency, you will then be hounded by collectors, adding further stress and potential legal action. This is why addressing the issue early is paramount.

Proactive Steps for Future Financial Stability

Learning from past experiences is crucial. Once you’ve navigated your current car loan challenge, take steps to prevent it from happening again.

A. Build an Emergency Fund:

Based on my experience, a robust emergency fund is the single most important financial safety net. Aim for at least 3-6 months of essential living expenses saved in an easily accessible account. This fund can absorb the shock of unexpected job loss or medical bills, preventing you from defaulting on loans.

(Internal Link Placeholder: Learn how to build your safety net with our guide: .)

B. Master Your Budget and Financial Planning:

Consistently track your income and expenses. Live below your means and prioritize saving. Understand your debt-to-income ratio and ensure your monthly debt payments are a manageable percentage of your income. Regularly review and adjust your budget as your circumstances change.

C. Understand Loan Terms Before Signing:

Before taking on any new debt, especially a car loan, thoroughly understand all the terms: interest rate, APR, loan term, total cost of the loan, and any prepayment penalties. Don’t be pressured by dealerships; take your time and read the fine print.

D. Build and Maintain Good Credit:

A strong credit score gives you access to better interest rates and loan terms, making future borrowing more affordable. Pay all your bills on time, keep credit utilization low, and regularly check your credit report for errors.

Common Mistakes to Avoid

In times of financial stress, it’s easy to make emotional decisions that can worsen your situation. Be mindful of these common pitfalls:

- Ignoring the Problem: Hoping it will go away is the worst strategy. The problem will only compound with late fees, interest, and eventual repossession.

- Hiding the Car: Attempting to hide your vehicle from repossession agents is illegal and will not prevent the eventual repossession or your liability for the loan.

- Taking on More Debt: Don’t take out high-interest payday loans or other short-term debt just to make a car payment. This is a slippery slope that rarely ends well.

- Not Understanding Terms: Never sign a new loan agreement or modification without fully understanding every clause and implication. Ask questions until you’re clear.

- Avoiding Communication with Your Lender: This is a recurring theme because it’s so important. Open communication can often lead to workable solutions.

Conclusion: Take Control, Don’t Despair

Discovering you can’t afford your car loan anymore is undoubtedly a distressing experience. However, it’s not a dead end. By understanding your situation, proactively engaging with your lender, and exploring the diverse range of options available, you can navigate this challenge effectively.

Remember, the key is early action and informed decision-making. Don’t let fear paralyze you. Take that first step, contact your lender, and begin charting a course toward regaining your financial footing. With perseverance and smart choices, you can overcome this obstacle and build a more secure financial future. Your journey to financial control starts now.

External Link: For more general guidance on managing debt and financial wellness, you can consult resources from trusted government agencies like the Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance.gov/