Can’t Get A Car Loan Anywhere? Your Ultimate Guide to Turning No into YES!

Can’t Get A Car Loan Anywhere? Your Ultimate Guide to Turning No into YES! Carloan.Guidemechanic.com

Facing a car loan rejection can be incredibly frustrating. You’ve found the perfect vehicle, imagined yourself driving it, only to be met with a resounding "no" from lenders. If you’re thinking, "I can’t get a car loan anywhere," you’re not alone. Many people experience this disheartening situation, often without fully understanding the underlying reasons.

But here’s the good news: being denied a car loan doesn’t mean car ownership is out of reach forever. It simply means you need to re-evaluate your approach, understand the lending landscape better, and implement strategic changes. This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to navigate the challenges of auto financing, even when it feels like all doors are closed. We’ll delve deep into why denials happen and, more importantly, how you can turn those rejections into approvals.

Can’t Get A Car Loan Anywhere? Your Ultimate Guide to Turning No into YES!

The Harsh Reality: Why Are You Being Denied a Car Loan?

Before you can fix a problem, you need to understand its root cause. Lenders use a set of criteria to assess risk, and if you don’t meet their minimum thresholds, you’ll likely face a denial. Let’s break down the most common reasons why you might be struggling to secure an auto loan.

1. Low Credit Score / Poor Credit History

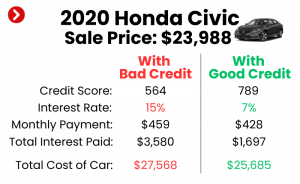

Your credit score is arguably the most critical factor lenders consider. It’s a three-digit number that summarizes your creditworthiness, essentially telling lenders how likely you are to repay borrowed money. A low score signals higher risk, making lenders hesitant to approve your application.

Poor credit history often stems from past financial missteps. This could include a pattern of late payments, defaults on previous loans, accounts sent to collections, or even significant charge-offs. These negative marks stay on your credit report for several years, actively impacting your score and influencing a lender’s decision.

Based on my experience as a long-time automotive financing consultant, many applicants underestimate the impact of even a few missed payments. Lenders look for consistency and reliability. If your history shows instability, they’ll naturally be more cautious, even if your current income seems sufficient.

2. Insufficient Income or High Debt-to-Income Ratio (DTI)

Lenders need to be confident that you have the financial capacity to comfortably make your monthly car payments. This isn’t just about your gross income; it’s about your income relative to your existing debts, a metric known as your Debt-to-Income Ratio (DTI).

Your DTI is calculated by dividing your total monthly debt payments (credit cards, student loans, mortgage/rent, etc.) by your gross monthly income. Lenders prefer a DTI below a certain percentage, often around 40-50%, including the proposed car payment. If your DTI is too high, it indicates that too much of your income is already allocated to other obligations, leaving little room for a new car payment.

Even if your income seems substantial, a high DTI can be a deal-breaker. Lenders want to ensure that adding another monthly payment won’t push you into financial strain, increasing the likelihood of default. They’re looking for stability and the ability to manage your finances responsibly.

3. No Credit History (Thin File)

It might seem unfair, but having no credit history can be almost as challenging as having bad credit. This situation, often referred to as a "thin file," means you haven’t taken out loans or credit cards in the past, so lenders have no track record to evaluate. Without any data, they can’t assess your repayment behavior, making you an unknown risk.

This is a common hurdle for young adults, recent immigrants, or individuals who prefer to use cash for everything. While being debt-free is commendable, it doesn’t help when a lender needs to see evidence of your ability to handle credit responsibly. They have no way of predicting how you’ll manage a new auto loan.

Common mistakes to avoid are applying for a car loan as your very first credit product. While not impossible, it’s significantly harder without any prior credit history. Building a small credit footprint first, even with a secured credit card, can make a huge difference.

4. Recent Bankruptcy, Repossession, or Foreclosure

Major derogatory marks like bankruptcy, repossession, or foreclosure are significant red flags for lenders. These events signal severe financial distress and a failure to meet past obligations. They remain on your credit report for several years (7-10 years for bankruptcy) and will heavily influence any new loan applications.

While the sting of these events fades over time, their immediate impact is profound. Lenders view them as indicators of high risk, often requiring a significant period of rebuilding credit and demonstrating financial stability before they’ll consider approving a new auto loan. The more recent the event, the more challenging it will be to get approved.

Even if you’ve been diligently working to rebuild your credit since such an event, lenders will still scrutinize the dates and circumstances. They need to see a consistent, extended period of positive financial behavior to regain trust.

5. Large Down Payment Insufficiency or High Loan-to-Value (LTV)

The amount of money you put down on a car loan, your down payment, plays a crucial role. A smaller down payment means you’re borrowing more relative to the car’s value, resulting in a higher Loan-to-Value (LTV) ratio. Lenders prefer a lower LTV because it reduces their risk.

If you default on a loan with a high LTV, the lender might not recover their full investment if they have to repossess and sell the car. This is especially true for new cars, which depreciate rapidly the moment they’re driven off the lot. A substantial down payment acts as a buffer, demonstrating your financial commitment and reducing the lender’s exposure.

From a lender’s perspective, a minimal or no down payment can signal that you’re not financially stable enough to save for a significant purchase. It increases their risk and can be a reason for denial, particularly if other aspects of your application are already weak.

6. Choosing the Wrong Car (Too Expensive/Unsuitable)

Sometimes, the problem isn’t entirely with your financial profile, but with the specific car you’re trying to finance. Lenders assess not just you, but also the asset they are lending against.

Trying to finance a car that is significantly more expensive than what your income or credit profile can reasonably support is a common pitfall. Lenders have internal guidelines on maximum loan amounts relative to income. Additionally, the age, mileage, and type of vehicle can impact approval. Some lenders are hesitant to finance very old, high-mileage vehicles because their resale value is low, and they pose a higher risk of mechanical failure, which could lead to you defaulting on the loan.

Pro tips from us: Always align the car you’re pursuing with your current financial reality. An entry-level sedan might be approved when a luxury SUV might not, simply because of the loan amount and the risk associated with the vehicle itself.

7. Multiple Recent Loan Applications

When you apply for a loan, it results in a "hard inquiry" on your credit report. A single hard inquiry has a minimal impact on your score, but multiple inquiries in a short period can raise a red flag. Lenders might interpret this as you being desperate for credit or trying to take on too much debt, both of which are considered high-risk behaviors.

While credit scoring models typically group auto loan inquiries within a short window (often 14-45 days) so they count as a single inquiry, applying to dozens of different lenders outside this window can still negatively affect your score and signal to lenders that you’re having trouble getting approved elsewhere. This makes them even more cautious.

Don’t Despair! Strategies to Turn "No" into "Yes"

Getting denied is not the end of the road. It’s a signal to pause, assess, and strategize. With the right approach, you can significantly improve your chances of securing a car loan.

1. Understand Your Credit Report & Score (and Fix It!)

The first and most crucial step is to obtain copies of your credit reports from all three major bureaus (Equifax, Experian, TransUnion). You are entitled to a free report from each annually via AnnualCreditReport.com. Scrutinize these reports for any inaccuracies or errors. Disputing and correcting these errors can quickly boost your score.

Beyond corrections, actively work on improving your credit score. Pay all your bills on time, every time. Reduce your existing debt, especially on credit cards, to lower your credit utilization ratio. Avoid opening new lines of credit unnecessarily. Over time, consistent positive behavior will strengthen your credit profile.

Based on my experience, simply understanding why your score is low is half the battle. Once you identify the specific issues, you can create a targeted plan. For instance, if high credit card balances are the problem, focus on paying them down aggressively.

2. Save for a Substantial Down Payment

A larger down payment is one of the most powerful tools you have. It reduces the amount you need to borrow, thereby lowering your monthly payments and making the loan more affordable. Crucially, it also reduces the lender’s risk.

When you put down a significant sum, you immediately establish equity in the vehicle. This lowers the Loan-to-Value (LTV) ratio, making the loan more attractive to lenders, especially those who might otherwise be wary of your credit profile. It demonstrates your financial commitment and ability to save, which are positive indicators. Aim for at least 10-20% of the car’s purchase price, if possible.

3. Consider a Co-Signer

If your credit is the primary hurdle, a co-signer with excellent credit can be a game-changer. A co-signer essentially pledges their own creditworthiness to guarantee the loan. This means if you fail to make payments, they are legally responsible for the debt.

A co-signer significantly reduces the lender’s risk, often leading to approval and potentially better interest rates. However, this is a serious commitment for the co-signer. Ensure they understand the full implications and that you are absolutely confident in your ability to make all payments on time. This approach should only be considered with someone you trust implicitly and who trusts you equally.

4. Explore Alternative Lenders (Subprime & Buy-Here-Pay-Here)

Traditional banks and credit unions typically cater to borrowers with good to excellent credit. If you "can’t get a car loan anywhere" from these institutions, it’s time to look at alternative lenders.

- Subprime Lenders: These specialize in working with borrowers who have less-than-perfect credit. They understand that life happens and are willing to take on more risk, though often at higher interest rates. Research reputable subprime lenders online or ask for recommendations from dealerships that specialize in bad credit financing.

- Buy-Here-Pay-Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They often have more lenient approval criteria since they control the entire process. However, BHPH loans typically come with very high interest rates and often require frequent payments (e.g., weekly or bi-weekly). Use BHPH as a last resort and be extremely cautious, thoroughly reviewing all terms and conditions before signing.

5. Start Small: Build Credit with a Cheaper Car

If your goal is simply to get reliable transportation and build your credit, consider financing a less expensive, used vehicle. A smaller loan amount is less risky for lenders, making approval more likely.

Successfully paying off a modest car loan on time can significantly improve your credit score. This establishes a positive payment history, making it easier to qualify for better loans (and better cars) in the future. Think of it as a stepping stone to your dream car. This demonstrates your ability to manage debt responsibly over time.

6. Secure a Pre-Approval (The Smart Way)

Instead of showing up at a dealership and letting them run your credit with multiple lenders, get pre-approved first. This involves applying to a few lenders (within the allowed credit inquiry window) to see what loan terms you qualify for before you even step foot on a car lot.

Pre-approval gives you leverage. You know your budget, interest rate, and terms upfront, allowing you to focus on negotiating the car’s price rather than the financing. It also prevents unnecessary hard inquiries and gives you a clear picture of what you can afford, avoiding the frustration of falling in love with a car you can’t finance.

7. Consider a Secured Loan

If you have an asset that can be used as collateral, a secured loan might be an option. While less common for auto loans (as the car itself is usually the collateral), some lenders might offer a secured personal loan if you have a savings account, CD, or other valuable asset you’re willing to pledge.

Using collateral significantly reduces the lender’s risk, as they have something to fall back on if you default. This can open doors to approval for those with poor credit who might otherwise be denied. However, understand the risk: if you don’t pay, you could lose your pledged asset.

8. Look Beyond Traditional Financing: Lease or Rideshare Options (Short-term)

In some cases, securing a traditional loan might be impossible in the short term. Consider temporary alternatives:

- Leasing: While still requiring a credit check, some leasing programs might be more flexible than loan approvals, especially for certain models or with specific dealerships. However, you won’t own the car, and mileage restrictions apply.

- Rideshare/Car Share: For immediate transportation needs, services like Uber, Lyft, or local car-sharing programs can be a short-term solution while you work on improving your financial situation. This avoids the need for a loan altogether for daily commuting.

Your Action Plan: Step-by-Step Towards Car Ownership

Now that you understand the "why" and the "how," it’s time to put a concrete plan into action. This structured approach will guide you from denial to approval.

1. Assess Your Current Financial Situation Honestly

Take a deep dive into your finances. What is your net income? What are all your fixed and variable expenses? List all your debts, including minimum payments and interest rates. This honest assessment will reveal your true affordability and highlight areas where you can cut back or increase income. Knowing your budget is the cornerstone of responsible car ownership.

2. Get Your Credit Reports and Scores

As mentioned, this is paramount. Pull your free reports from AnnualCreditReport.com. Review every detail meticulously. Dispute any errors or outdated information with the respective credit bureau. Understand your actual credit scores (FICO or VantageScore) and identify the specific factors negatively impacting them. This is your starting point for improvement.

3. Set a Realistic Budget

Based on your financial assessment, determine how much you can truly afford for a monthly car payment, insurance, fuel, and maintenance. Don’t just consider the car loan itself. Remember, a car comes with ongoing costs. Aim for a total car expenditure (payment, insurance, fuel, maintenance) that is no more than 10-15% of your gross monthly income. This will prevent you from being "car poor."

4. Research Lenders

Don’t limit yourself to the first bank you walk into. Research various types of lenders: credit unions (often have more lenient terms for members), traditional banks, online auto lenders, and even subprime specialists. Look for those who advertise working with individuals with challenging credit. Read reviews and compare their minimum requirements and typical interest rates.

5. Gather Necessary Documents

Be prepared before you apply. Have all your financial documents ready: recent pay stubs (2-3 months), bank statements (2-3 months), proof of residency (utility bill), driver’s license, and any other income verification documents. Being organized and having these on hand will streamline the application process and show lenders you are serious and prepared.

6. Be Prepared to Negotiate (Both Car Price & Loan Terms)

Once you’re in a position to apply, remember that everything is negotiable. Negotiate the price of the car first, independently of the financing. Once you have an agreed-upon car price, then discuss loan terms. If you have a pre-approval, use it as leverage to ensure the dealership’s financing doesn’t offer less favorable terms. Don’t be afraid to walk away if the deal isn’t right for you.

Conclusion: Your Road to Car Ownership Is Possible

The frustration of thinking, "I can’t get a car loan anywhere," is a common experience, but it doesn’t have to be your permanent reality. By understanding the reasons behind loan denials and proactively implementing strategic solutions, you can significantly improve your chances of approval.

Remember, patience and persistence are key. Rebuilding credit, saving for a down payment, and exploring all available lending options take time and effort. But with a clear action plan, realistic expectations, and a commitment to improving your financial health, you can secure the financing you need. Don’t give up on your goal of car ownership. Start taking these steps today, and you’ll be well on your way to turning those rejections into a resounding "yes!"